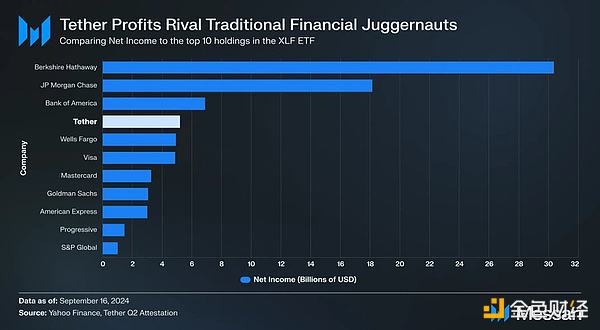

Tether上季度破纪录的盈利能力使其跻身tradfi巨头之列。但52亿美元这笔巨额利润也让它成为了那些想要分得一杯羹的新竞争对手的目标。

本文我们来深入快速发展的稳定币世界,涉及到中心化领域和去中心化领域。

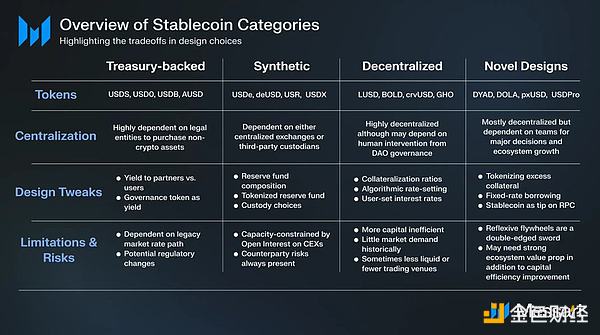

稳定币全览

我们将做以下几类的垂直细分:

PYUSD

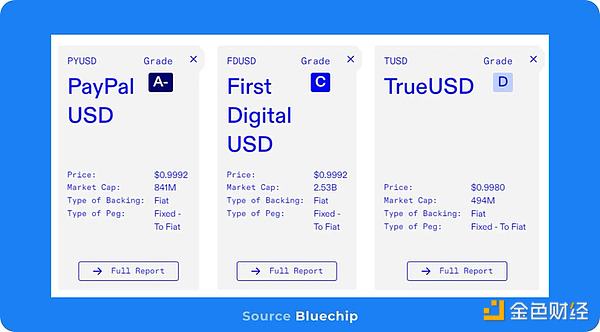

中心化稳定币往往缺乏透明度,而且往往只在具有明确激励的条件下才会出现高交易量。PYUSD是少数收获信任的10亿美元市值规模的中心化稳定币之一。

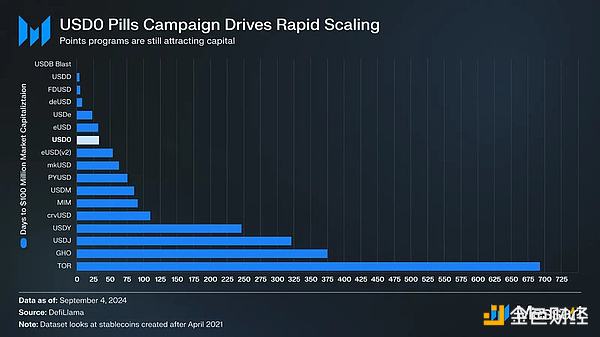

USD0

通过空投激励以及与Morpho等DeFi平台的合作整合,像USD0这样更加去中心化的金库支持型稳定币迅速增长。USD0市值约为2.5亿美元,很快就达到了这一目标。

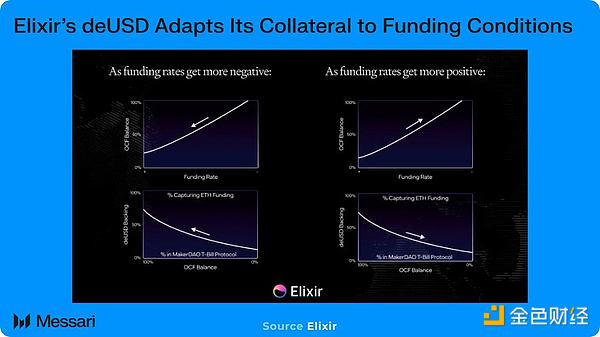

Elixir的deUSD

像USDe这样的合成稳定币使用“多头现货+空头期货头寸”来维持其挂钩。由于基差被压缩,USDe失去了市场份额。但像Elixir这样的新协议旨在通过调整其抵押品支持来改进Ethena模式。

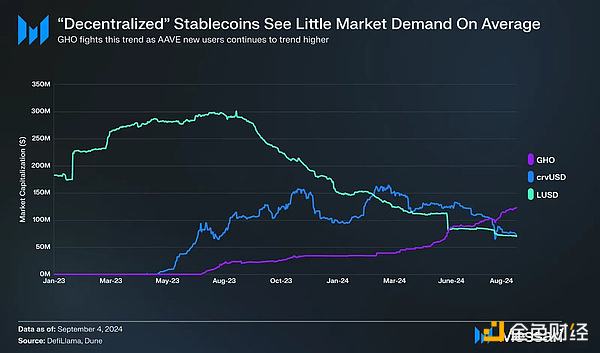

GHO

专注于最大限度地去中心化和最大限度地减少人为干预的稳定币一直以来都没有显出太多的需求。GHO可能是个例外,因为它利用了AAVE上持续增长的活跃用户群。

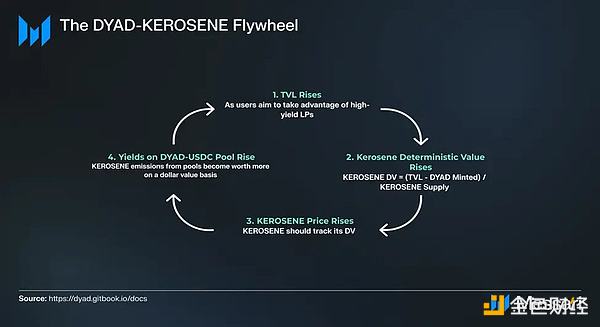

DYAD

创新的设计通常试图实现某种机制来改进典型的抵押债务。

头寸模式。DYAD就是这样的一种稳定币,它的目标是通过另一种名为KEROSENE的代币利用系统内多余抵押品。KEROSENE允许用户抵押外自己的外源资产铸造更多的DYAD。而且,NFT(NOTE)持有者的KEROSENE越多,他们从流动性池中获得的收益就越多。

这些类别的新稳定币都在收益率、可及性、流动性、稳定性和资本效率方面相互竞争。新设计或对旧设计的调整都会涉及到各种利弊权衡:

每周都有新的稳定币进入市场,稳定币领域格局也在不断发展变化。