原创 | Odaily星球日报(@OdailyChina)

作者 | Asher(@Asher_ 0210 )

继 Notcoin 破圈之后,TON 生态持续升温。尽管出现了诸如 Hamster Kombat(仓鼠)和猫猫(Catizen)等多个爆款项目,但由于这些项目尚未明确代币空投的时间,讨论热度逐渐减退。同时,伴随“门头沟”事件和“德国政府”出售比特币的影响,整个加密市场一片死寂。

就在这样的市场环境下,昨日一只黑白狗的 Telegram 邀请链接在社交媒体、各大社区疯狂刷屏,大家纷纷晒自己领到的积分。那么,这只黑白狗项目 DOGS 如何在极短时间内吸粉近 200 万呢?下面,Odaily星球日报带大家了解这款 TON 生态突然爆火、病毒式传播的“零撸”项目 DOGS。

将 Spotty 的传统带入加密世界

DOGS 项目的黑白狗形象灵感来自于 Telegram 的创始人 Pavel Durov。他在一次支持孤儿院的慈善拍卖会上画了这只标志性的狗 Spotty。根据官方 Telegram 信息,DOGS 并非普通的纪念币。它是最具 Telegram 特色的纪念币,体现了充满活力的社区精神和文化。团队将 Spotty 的传统带入加密货币世界,创造出有趣、以社区为导向、独一无二的加密货币。

Pavel Durov 的推特早在两年前就停更了,从过往发的推文内容来看,Pavel Durov 似乎对“狗”影响有所钟爱。

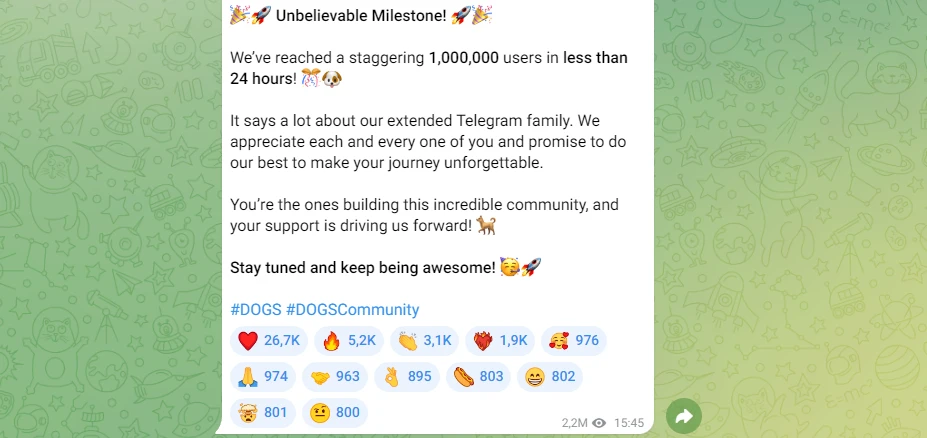

在蓬勃发展的 TON 生态的推动下,DOGS 项目迎合了当前生态中缺乏代表性 Meme 形象的需求。通过向 Telegram 用户空投代币,仅在短短一天内便吸引了超过 100 万订阅用户,且每天内容阅读量超百万,其增长速度惊人。

DOGS 在不足一天的时间获得百万订阅用户

阳光普照、人人有份

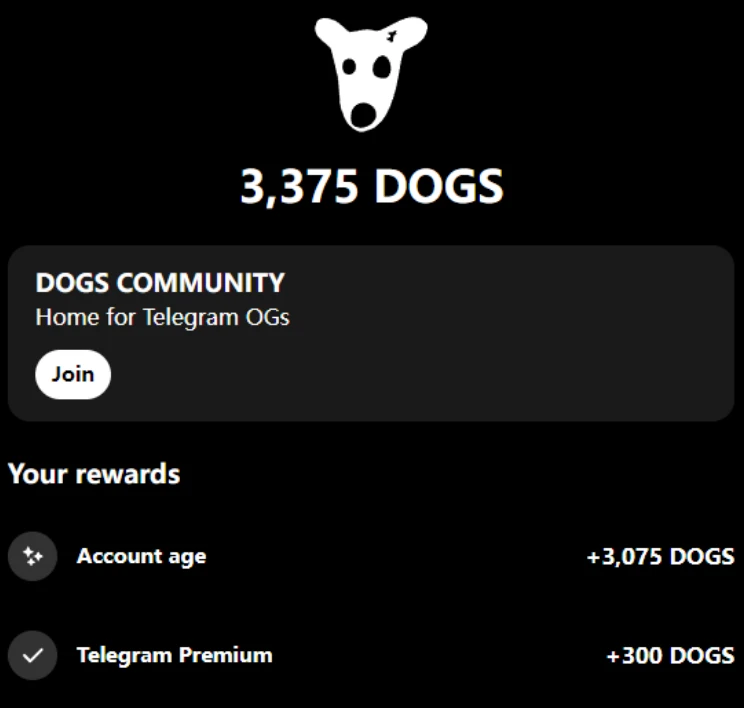

DOGS 昨日在各大社交媒体中刷屏的原因是因为其参与并领取代币积分的方式非常简单:用户只需进入 Telegram 中的 DOGS BOT 频道,系统会根据用户的 Telegram 账号注册时间和活跃度进行评级,并据此分发积分。此外,开通了 Telegram Premium 账号的用户还能获得额外的积分奖励。目前仍为领取 DOGS 代币积分的用户可点击此处跳转。

某开通 Telegram Premium 4 年账号所获代币积分

此外,DOGS 还开启了邀请获取更多代币积分的活动方式,因此各大社交媒体上开始疯狂刷屏……

尽管代币总量、空投比例、积分兑换比例等细节尚未公布,而且所获得的代币积分目前也无法交易。但由于其简单易懂的规则和操作方式,以及“零门槛”特性,DOGS 项目成功吸引了大量用户,其黑白狗的 Meme 形象也迅速传播开来。

热度火爆,场外市场吸引大量用户

尽管当前用户领取的 DOGS 代币积分无法在二级市场直接出售,但由于热度爆棚,场外交易市场上已经出现了不少买家。根据多个场外交易群调研发现,许多散户愿意以每积分 0.016 至 0.02 美元的价格进行交易。

某 DOGS 场外交易挂单情况

TON 生态+Meme 赛道为爆火创造有利条件

在本轮牛市中,表现最突出的板块是 Meme 板块,而公链中热度最高的是 TON 公链。DOGS 项目结合了“Meme”和“TON”这两大热门标签,展现出无限潜力。如果“黑白狗”的形象能够得到当前散户的广泛认可,DOGS 或许能继 Notcoin 之后成为下一个破圈项目。

此外,DOGS 项目的成功不仅依赖于其有趣的 Meme 形象和 TON 生态的支持,还得益于其巧妙的用户参与机制。通过简单的操作和诱人的积分奖励制度,DOGS 吸引了大量用户的参与和关注。再加上社交媒体上的病毒式传播,DOGS 项目的热度持续攀升,甚至引发了场外交易的活跃。

随着市场对 Meme 文化的接受度越来越高,以及 TON 公链生态的不断壮大,DOGS 项目有望在未来取得更大的成功。