经 Odaily星球日报不完全统计, 1 月 29 日-2 月 4 日公布的海内外区块链融资事件共 31 起,较上周数据(39 起)有所下降,已披露融资总额约为 1.19 亿美元,较上周数据(2 亿美元)有所下降。

上周,获投金额最多的项目为基于比特币的跨链 DEX 和钱包 Portal (3400 万美元);混合型加密货币交易平台 Cube.Exchange 也紧随其后(1200 万美元)。

以下为具体融资事件(注: 1. 依照已公布金额大小排序;2. 不含基金募资及并购事件;3. *为部分业务涉及区块链的“传统”领域公司):

基于比特币的跨链 DEX 和钱包 Portal 完成 3400 万美元种子轮融资,Coinbase Ventures 等参投

1 月 30 日,基于比特币的跨链 DEX 和钱包 Portal 宣布完成 3400 万美元种子轮融资,Coinbase Ventures、Arrington Capital、OKX Ventures 和 Gate.io Ventures 参投,据悉本轮融资的结构是简单的未来股权协议 (SAFE) 和可转换票据的组合,但该公司拒绝透露相关估值信息。

混合型加密交易平台 Cube.Exchange 以 1 亿美元估值完成 1200 万美元 A 轮融资

2 月 1 日,混合型加密货币交易平台 Cube.Exchange 宣布完成 1200 万美元 A 轮融资, 6 th Man Ventures 领投,GSR Markets、ParaFi Digital、Susquehanna Private Equity Investments、Everstake Capital 等参投,本轮融资估值达到了 1 亿美元。据悉,Cube 使用离链订单匹配和链上结算的混合模型,让用户在不必将资产转移到交易所托管账户的情况下保持资产所有权。

Delegate Labs 完成 900 万美元种子轮融资,Electric Capital 等参投

2 月 1 日,安全协议 Delegate 背后团队 Delegate Labs 宣布完成 900 万美元种子轮融资,Electric Capital、Arca、Variant 和 Arrington Capital 参投,本轮融资将用于资助 Web3 域名协议 Clusters,该协议旨在解决地址碎片化、钱包管理复杂性与域名抢占等问题。

NFT 游戏项目 Pixelmon 完成 800 万美元种子轮融资,Animoca Brands 参投

2 月 2 日,NFT 项目 Pixelmon 完成 800 万美元种子轮融资,Animoca Brands、Delphi Ventures 和 Foresight Ventures 以及 Amber Group、 9 GAG 创始人 Ray Chan 和 Immutable 联合创始人 Robbie Ferguson 等参投。

Web3社交游戏 Forgotten Playland 完成 700 万美元种子轮融资,Merit Circle 等参投

1 月 30 日,据官方消息,Web3 社交游戏 Forgotten Playland 宣布完成 700 万美元种子轮融资,Merit Circle、Spartan Group、C 2 Ventures、Paper Ventures 等参投。

PayPal 向加密支付公司 Mesh 投资 500 万美元 PYUSD 及 150 万美元现金

1 月 29 日,PayPal 旗下风投部门 PayPal Ventures 通过其稳定币 PYUSD 向加密支付公司 Mesh 投资 500 万美元。

除了以稳定币形式向 Mesh 提供的 500 万美元(记录在以太坊区块链上)之外,PayPal Ventures 还额外向其注资 150 万美元现金。

Gevulot 完成 600 万美元种子轮融资,Variant 领投

1 月 29 日,零知识证明的区块链 Gevulot 完成 600 万美元种子轮融资,Variant 领投,RockawayX、Volt Capital 和 Staking Facility 以及 Polygon Labs 首席执行官 Marc Boiron 和 Manta Network 创始人 Shumo Chu 等个人支持者参投,Gevulot 没有透露其估值。

Web3游戏公司 Saltwater 完成 550 万美元种子轮融资

2 月 1 日,Web3 游戏公司 Saltwater 宣布完成 550 万美元种子轮融资,加密投资机构 Deus X 和 Fourth Revolution Capital ( 4 RC)联合领投,新资金将用于增加员工数量、投资新技术、以及将业务扩展到新的领域。

跨链路由服务提供商 Squid 完成 400 万美元战略轮融资,Polychain Capital 领投

2 月 1 日,跨链路由服务提供商 Squid 宣布完成 400 万美元战略轮融资,Polychain Capital 领投,Nomad Capital、North Island Ventures、Maelstrom 和 Chorus One、The Department of XYZ、Breed、Binary Builders 和 Typhon Ventures 参投,同时 Squid 还获得了来自 Distributed Global、Fabric Ventures、Node Capital 和 Chapter One 的追加投资。目前 Squid 支持 60 多个链上数千种资产,此次融资使团队能够继续扩展 EVM 和 Cosmos 生态系统,并且还将与更多去中心化应用程序(dApp)建立更深入的集成。

流动性质押协议 Stride 完成 400 万美元战略融资,DBA 领投

2 月 3 日,Stride Association 宣布完成 400 万美元战略融资,以推动 Cosmos 生态流动性质押协议 Stride 在模块化生态中的发展。

该轮融资由 DBA 领投,1co nfirmation、Road Capital、Modular Capital、Chorus One 以及模块化生态主要构建者 Neel Somani(Eclipse)、Yishay Harel(Dymension)、Jon Kol 和 NoSleepJon(Hyperlane)、Cem Özer(Sovereign Labs)、Mike Neuder(Ethereum Foundation)等参投。

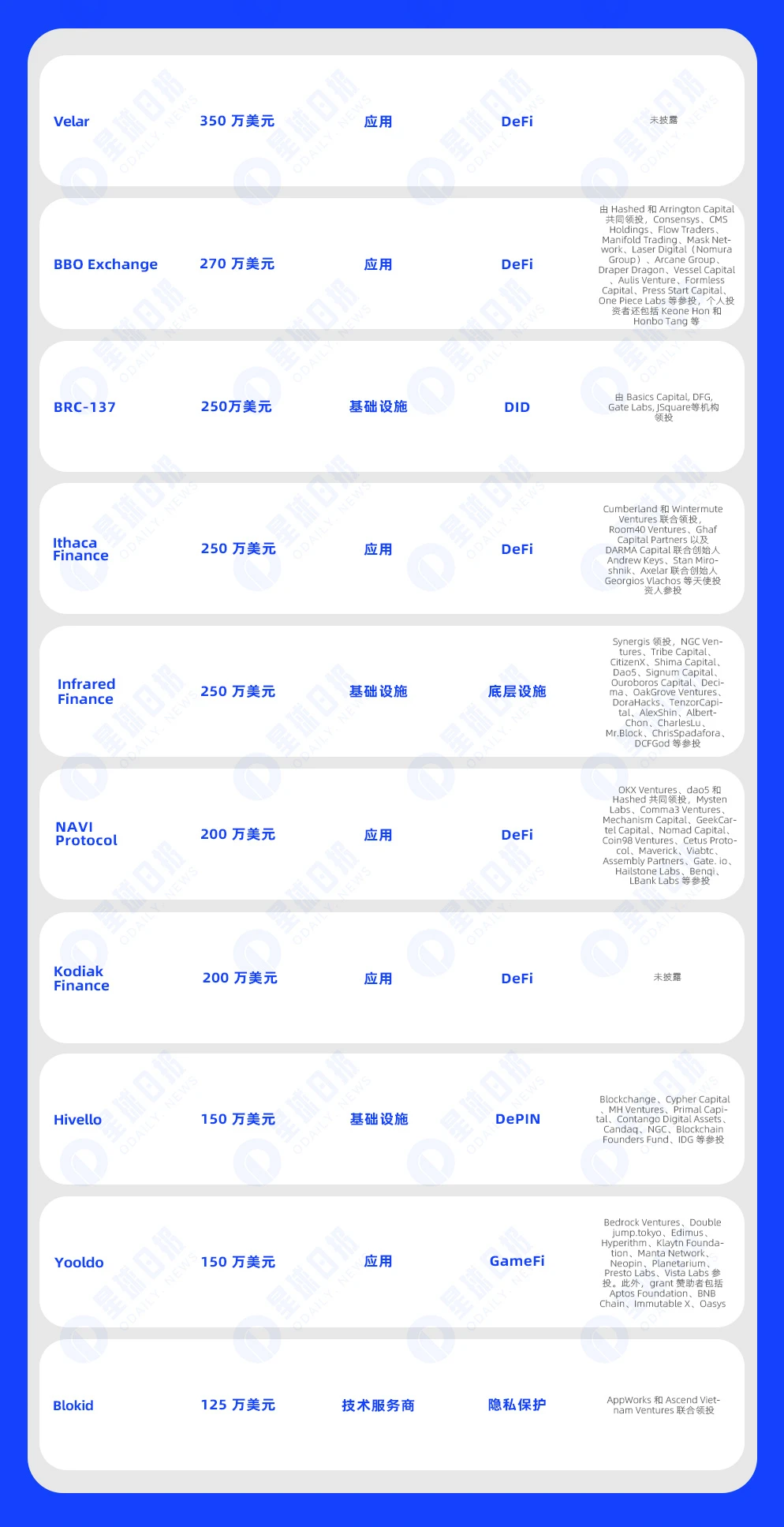

加密货币交易服务公司 Velar 完成 350 万美元新一轮融资

2 月 1 日,加密货币交易服务初创公司 Velar 宣布已完成 350 万美元新一轮融资,具体投资机构信息暂未披露。Verlar 主要为比特币 DeFi 场景构建工具,该公司首席执行官 Mithil Thakore 表示,计划利用最新融资推出支持比特币网络的永续掉期交易所。

去中心化衍生品交易平台 BBO Exchange 完成 270 万美元 Pre-Seed 轮融资,由 Hashed 和 Arrington Capital 领投

1 月 30 日,去中心化衍生品交易平台 BBO Exchange(BBOX)完成 270 万美元 Pre-Seed 轮融资,由 Hashed 和 Arrington Capital 共同领投,Consensys、CMS Holdings、Flow Traders、Manifold Trading、Mask Network、Laser Digital(Nomura Group)、Arcane Group、Draper Dragon、Vessel Capital、Aulis Venture、Formless Capital、Press Start Capital、One Piece Labs 等参投,个人投资者还包括 Keone Hon 和 Honbo Tang 等。

比特币生态可组合性 DID 协议 BRC-137 完成 250 万美元种子轮融资

2 月 3 日,比特币生态可组合性 DID 协议 BRC-137 宣布完成 250 万美元种子轮融资。该轮融资由 Basics Capital, DFG, Gate Labs, JSquare 等机构领投。资金将用于加速协议的开发完善与生态增长,以实现比特币生态原生社交宇宙。

可组合期权协议 Ithaca Finance 完成 250 万美元 Pre-Seed 融资

1 月 31 日,可组合期权协议 Ithaca Finance 宣布已完成 250 万美元 Pre-Seed 轮融资,Cumberland 和 Wintermute Ventures 联合领投,Room 40 Ventures、Ghaf Capital Partners 以及 DARMA Capital 联合创始人 Andrew Keys、Stan Miroshnik、Axelar 联合创始人 Georgios Vlachos 等天使投资人参投。据悉,目前 Ithaca Finance 已在 Arbitrum 测试网上线,本季度晚些时候全面启动之前仅邀请受邀者启动主网。

流动性证明协议 Infrared 完成 250 万美元种子轮融资

1 月 29 日,Berachain 生态流动性证明基础设施 Infrared Finance 宣布完成 250 万美元种子轮融资,Synergis 领投,NGC Ventures、Tribe Capital、CitizenX、Shima Capital、Dao 5、Signum Capital、Ouroboros Capital、Decima、OakGrove Ventures、DoraHacks、TenzorCapital、AlexShin、AlbertChon、CharlesLu、Mr.Block、ChrisSpadafora、DCFGod 等参投。

Infrared 旨在 Proof-of-Liquidity(PoL)的背景下支持 Berachain 生态的流动性质押。这些资金将用于推进其基础设施发展,包括验证者网络、PoL 保险库以及原生流动性质押代币(LST)iBGT。

NAVI Protocol 完成 200 万美元融资,OKX Ventures、Hashed 等领投

1 月 31 日,据官方消息,Sui 生态一站式流动性协议 NAVI Protocol 宣布完成 200 万美元融资,OKX Ventures、dao 5 和 Hashed 共同领投,Mysten Labs、Comma 3 Ventures、Mechanism Capital、GeekCartel Capital、Nomad Capital、Coin 98 Ventures、Cetus Protocol、Maverick、Viabtc、Assembly Partners、Gate. io、Hailstone Labs、Benqi、 LBank Labs 等参投。

NAVI Protocol 将利用此轮融资资金扩展其一站式借贷和 LSDeFi 平台。

DEX 项目 Kodiak Finance 完成 200 万美元种子轮融资

2 月 3 日,Kodiak Finance 宣布完成 200 万美元种子轮融资。Kodiak Finance 旨在成为 Berachain 社区原生 DEX。

Kodiak Finance 团队表示,此轮融资资金将使其能够进一步加快扩展 Kodiak 的速度,并继续提供 Berachain 原生交易产品。

DePIN 基础设施提供商 Hivello 完成 150 万美元新一轮融资,IDG 等参投

2 月 1 日,去中心化 DePIN 基础设施服务提供商 Hivello 宣布完成 150 万新一轮融资, Blockchange、Cypher Capital、MH Ventures、Primal Capital、Contango Digital Assets、Candaq、NGC、Blockchain Founders Fund、IDG 等参投,加上 2023 年 12 月完成的 100 万美元融资,该公司迄今融资总金额已达到 250 万美元。该公司打算利用新融资扩大其技术能力,加快产品开发,并巩固其在 DePIN 领域的市场地位。

链游平台 Yooldo 完成 150 万美元融资,Manta Network 等参投

2 月 1 日,据官方消息,链游平台 Yooldo 宣布以 1300 万美元估值完成 150 万美元融资,Bedrock Ventures、Double jump.tokyo、Edimus、Hyperithm、Klaytn Foundation、Manta Network、Neopin、Planetarium、Presto Labs、Vista Labs 参投。此外,grant 赞助者包括 Aptos Foundation、BNB Chain、Immutable X、Oasys。

新融资将用于完善技术,为平台带来更多游戏,并发展其社区。据悉,Yooldo 已被纳入 Consensys Scale Program 和 Google for Startups Program。

区块链隐私保护解决方案 Blokid 完成 125 万美元种子轮融资,AppWorks 领投

2 月 1 日,区块链驱动的隐私保护解决方案 Blokid 宣布完成 125 万美元种子轮融资,AppWorks 和 Ascend Vietnam Ventures 联合领投,该公司 2023 年 7 月成立,目前专注于为数字广告行业量身定制区块链时间戳驱动的安全服务,帮助品牌和机构能够使用先进技术验证其资产。

Web3无代码 DApp 生态协议 Forward Protocol 融资 125 万美元,Polygon、AU 21 等参投

2 月 2 日,Web3 无代码 DApp 生态协议 Forward Protocol 宣布完成 125 万美元融资,其中包括 50 万美元种子轮融资和 70 万美元私募轮融资,CVVC、AU 21、X 21 和 GDA Capital、Polygon、Bitcoin.com、以及 Utopian Capital、Marathon Capital、Cuan Ventures、Ardura Capital、MEXC、Stakez Capital、Magnus Capital、MarketAcross、Basics Capital、CRT Capital、Polygon Studios、Master Ventures、BlackDragon、Tokenova、Lotus Capital、NFT Technologies、Darkpool Capital、Octopus Capital、ZBS Capital、IBC Group、Polygon Syndicate 和 Oracles Investment Group 等参投。

1 月 30 日,流动性聚合投资策略协议 Doubler 宣布完成种子轮融资,Youbi Capital 领投,Bixin Ventures、Mask Network、Comma 3 Ventures、Pivot Labs、Continue Capital、Sanyuan Capital、Waterdrip Capital、DWF Ventures、Gate Labs、Formless Capital、MT Capital 和 CatcherVC 等机构参投,具体融资金额暂未披露。Doubler 是一个开放式的 DeFi 协议,采用马丁格尔策略来聚合市场流动性,结合了零损失对冲需求与投机者的收益需求。

以太坊流动性协议 Puffer Finance 完成新一轮融资,Binance Labs 参投

1 月 30 日,Binance Labs 宣布已投资基于 EigenLayer 构建的以太坊流动性重新抵押协议 Puffer Finance,Brevan Howard Digital、Jump Crypto 和 Lightspeed Faction 参投,具体金额暂未披露,Puffer 将利用这笔资金开发其 Layer 2 网络,该网络将作为 EigenLayer 主动验证服务运行。

RWA 生态系统 TProtocol 完成天使轮融资,Spark Digital Capital 等参投

1 月 31 日,据官方消息,RWA 生态系统 TProtocol 宣布完成天使轮融资,Summer Capital、Matrixport Venture、Spark Digital Capital 等参投,具体融资金额暂未披露。新融资将用于推动 TProtocol 发展成为全面的区块链 RWA 聚合器。

1 月 31 日,去中心化永续合约协议 Zeepr Labs 在 X 平台宣布完成由 Celestia 生态孵化器 Cincubator 领投的新一轮融资,具体融资金额未披露,投后估值达 1.5 亿美元。据悉,Zeepr 是同时支持币本位和 U 本位的去中心化永续合约协议,旨在提供无滑点、无资金费的链上永续合约交易体验。

比特币生态 DeFi 项目 Ordiswap 完成战略轮融资,DWF Labs 参投

2 月 1 日,比特币生态 DeFi 项目 Ordiswap 在 X 平台宣布已完成战略轮融资,DWF Labs 参投并与之达成合作伙伴关系,新资金将用于 Ordiswap 为比特币开发 DeFi 基础设施与生态系统。

Nibiru Chain 完成战略轮融资,Oddiyana Ventures 参投

2 月 1 日,DeFi 项目 Nibiru Chain 宣布完成战略轮融资,Oddiyana Ventures 参投,具体投资金额尚未披露。据悉 Nibiru Chain 去年曾以 1 亿美元估值完成 850 万美元种子轮融资,Tribe Capital、Republic Capital、NGC Ventures 和 Original Capital 联合领投。

专注于 AI 的Web3基础层 KIP Protocol 完成战略轮融资,Animoca Ventures 领投

2 月 1 日,专注于 AI 的 Web3 基础层 KIP Protocol 宣布完成战略轮融资,Animoca Ventures 领投,B.Army(越南)、CSP DAO(欧洲、中东和非洲)、MQdao、Spicy Capital(拉丁美洲)、Skyvision Capital(香港)和 Purechain Capital(英国)等参投。

游戏化社交平台 SoulLand 完成千万级融资,Foresight Ventures 等参投

2 月 2 日,游戏化社交平台 SoulLand 宣布完成千万级融资,参投机构包括 Foresight Ventures、Redline Labs、Zonff Partners、MEXC、Mandala Ventures Limited、Stratified Capital、Basics Capital 和 Onemax Capital。

RGB 协议基础设施 Bitlight Labs 完成种子轮融资,Gate Ventures 与 HV Capital 联合领投

2 月 2 日,RGB 协议基础设施 Bitlight Labs 宣布完成种子轮融资,将致力于推动闪电网络生态发展。本轮融资由 Gate Ventures 和 HV Capital 联合领投,参投机构包括 MH Ventures、Fundamental Labs、Oak Grove Ventures、Waterdrip Capital 等。

去中心化云计算服务提供商 Exabits.ai 完成种子轮融资,Protocol Labs 等参投

2 月 2 日,去中心化云计算服务提供商 Exabits.ai 宣布完成种子轮融资,Protocol Labs、Outlier Ventures、Jabre Capital Partners、Valkyrie Fund、Big Brain Holdings、Blockchain Builders Fund、Taisu Ventures、Fortified Ventures、LBank Labs、Paramita Capital、Moonhill Capital、IoTeX、 1 nvest 等参投,具体金额暂未披露。