修昔底德陷阱,由美国哈佛大学教授格雷厄姆·艾利森提出,意思是一个新崛起的大国必然要挑战现存大国,而现存大国也必然来回应这种威胁,这样战争变得不可避免。现在,修昔底德陷阱发生在了NFT市场OpenSea和Blur两大巨头身上。

""

Blur率先亮剑

""

2月15日,Blur原生代币BLUR上线交易,不到24小时交易额就突破了10亿美元,或许是趁着这股强劲势头,Blur开始在NFT版税战争的新篇章中与OpenSea针锋相对。

""

2月16日,即BLUR代币上线一天后,Blur就发布官方公告宣布更新版税政策,其中直截了当的推荐用户屏蔽OpenSea,只要不使用OpenSea即可享受全额版税,Blur还提议OpenSea取消对Blur上NFT项目设置可选版税的设置,如果OpenSea取消该政策,NFT项目将可以同时在两个平台上收取版税。Blur强调目前NFT项目创作者无法同时在Blur和OpenSea上收取版税,只能在OpenSea或Blur两者之一收取全部版税,但不能同时收取。

""

实际上,Blur这次亮剑并非偶然。2022年11月,OpenSea发布公告称,为了在 OpenSea 的平台上强制执行全额创作者费用,在2023年1月2日之后创建NFT智能合约的个人必须采取链上行动以使版税可执行。换句话说,OpenSea要求创作者使用链上工具禁止在不强制创作者版税的市场上销售NFT——这是一个明显针对Blur的举措,因为Blur是一个免版税的平台,创作者不得不禁止他们的NFT在Blur上出售才能在OpenSea上享受全部版税。如果不这样做,OpenSea会自动将这些NFT藏品的版税设置为“可选”,继而影响创作者收入。

""

Blur对OpenSea使用“黑名单”的打压手段提出异议,声称应该由创作者来决定他们的产品在何处销售、以及如何销售——而不是公司,但收效甚微,之后也不得不使用Seaport协议绕过限制。

""

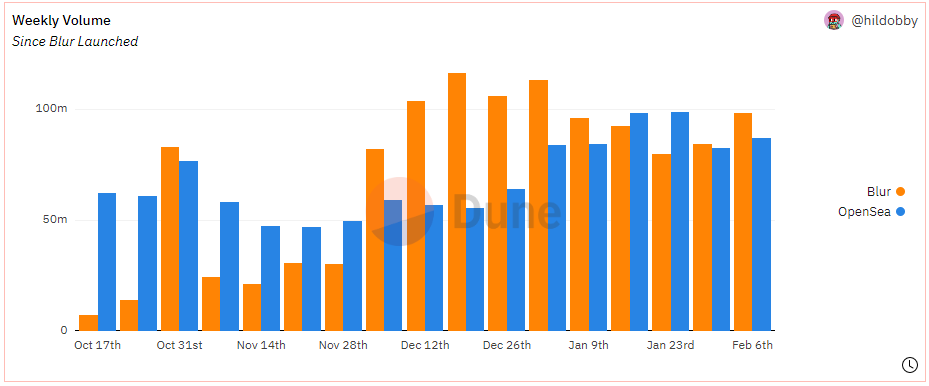

然而,所谓杀敌一千自损八百,OpenSea的如意算盘并没有成功压制住Blur快速发展态势,反而引发了用户倒戈。下图是OpenSea和Blur单周交易额对比,从中可以看出,自2022年12月初(即OpenSea开始限制Blur)以来,OpenSea只有两周的交易额高于Blur,其余时间均处于落后状态。

NFT生态“大反转”?OpenSea认怂了

""

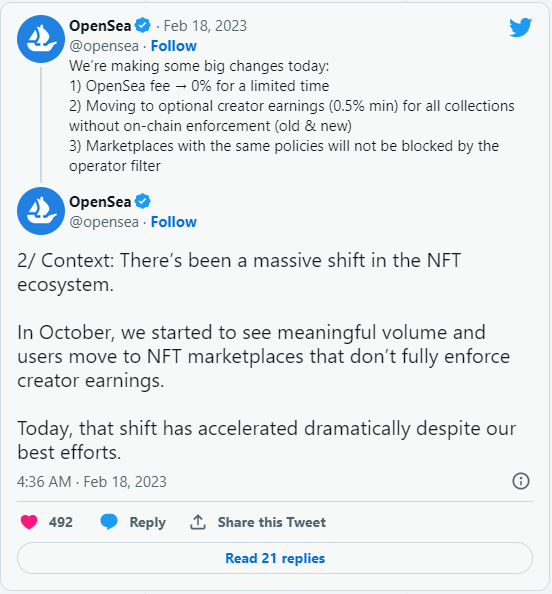

2月18日凌晨,OpenSea发布公告宣布启动限时0手续费交易,并提供最低标准为0.5%的可选版权服务且适用所有非链上强制执行版税的NFT系列,同时还更新了运营商过滤器以允许拥有相同政策的NFT市场可以共同增加市场流动性。

终于,OpenSea低头服软了。

""

OpenSea解释了做出这一决定的原因,据称是因为“NFT 生态系统发生了巨大变化”,用他们的话说:“从2022年10月开始,我们发现交易量和用户开始转向不完全执行创作者收入的NFT市场,而且这种转变仍在急剧加速。我们认为此前的举措可以促进创作者收入的广泛实施,也希望其他人可以提出更具弹性的解决方案,但事情并没有按照我们的预期发展。最近发生的事件——包括 Blur 决定降低创作者的收入(即使是过滤后的NFT藏品)以及迫使创作者在Blur或OpenSea的流动性之间做出的选择——证明我们之前的尝试并没有奏效。”

""

Blur的迅猛发展更是加剧了OpenSea的担忧,据Dune Analytics数据显示,其平台交易额已突破100万枚ETH,达到1,028,378 ETH,按照当前价格计算约合17.5亿美元,销售总量也超过了200万笔,当前达到2,027,752笔,此外Blur平台独立买家数量为109,655个。

Blur大获全胜了吗?

""

坦率地说,现在断言Blur赢得了与OpenSea的地盘争夺战还为时尚早。

""

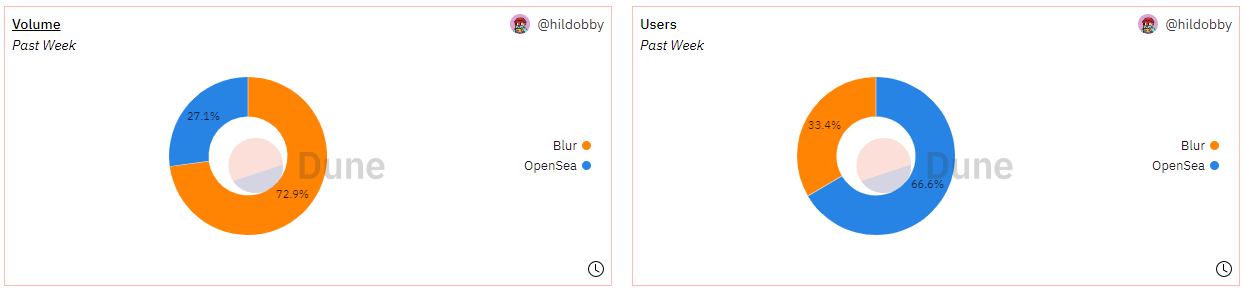

Blur近期交易额激增很大程度上与其空投BLUR代币有关,是否能够维持更长久的有机增长还不确定。需要注意的是,OpenSea的用户量几乎是Blur的两倍(如下图所示),这意味着他们依然拥有较强的用户基础,更重要的是,OpenSea至今没有发布自己的治理代币或平台币,一旦OpenSea尝试Blur的发币策略,势必给整个NFT市场格局带来影响。

Galaxy研究人员指出,NFT交易者应该密切关注OpenSea和Blur之间正在进行的“争斗”,事实上大多数Blur的头部交易者为了获得空投代币都进行过洗售交易,这表明与OpenSea相比,Blur平台上的交易量可能不是有机的。

""

另一方面,或许是为了给自己留更多退路,Blur的反击策略其实并没有太过激进,因为其更新的版税政策中也提供了不设置屏蔽OpenSea和屏蔽Blur的选项,如果创作者不设置屏蔽,Blur将收取0.5%的版税(卖家也可以选择更高版税),而OpenSea则是可选版税;如果屏蔽Blur或其他零版税/版税可选市场的NFT项目都将在OpenSea上被强制执行版税,但交易和上架仍可以在Blur上进行,需要收取最低0.5%的版税。

""

Galaxy分析师补充称:“很明显,Blur正在利用他们的影响力来迫使OpenSea与他们合作,而不是对他们表现出敌意,时间会证明 Blur 的策略是否会奏效,但无论是在指标还是在产品方面,他们都是迄今为止最成功的OpenSea竞争对手。”

""

此外,Galaxy研究人员在周五的一份最新报告中还指出:“关于Blur,有两个关键问题需要关注。首先,也是最重要的是Blur可以保留多少市场份额,因为他们的BLUR代币具有流动性。其次是交易量,短期内预计Blur交易量不会出现严重下降,因为他们的代币激励计划第二季将至少再持续30天,但这种模式能否长期奏效值得观察。”

""

总之,随着OpenSea和Blur的地盘争夺战不断升温,NFT市场竞争只会愈演愈烈,或许在这场厮杀结束后,我们能够找到一条最适合NFT创作者和交易者的发展路径。