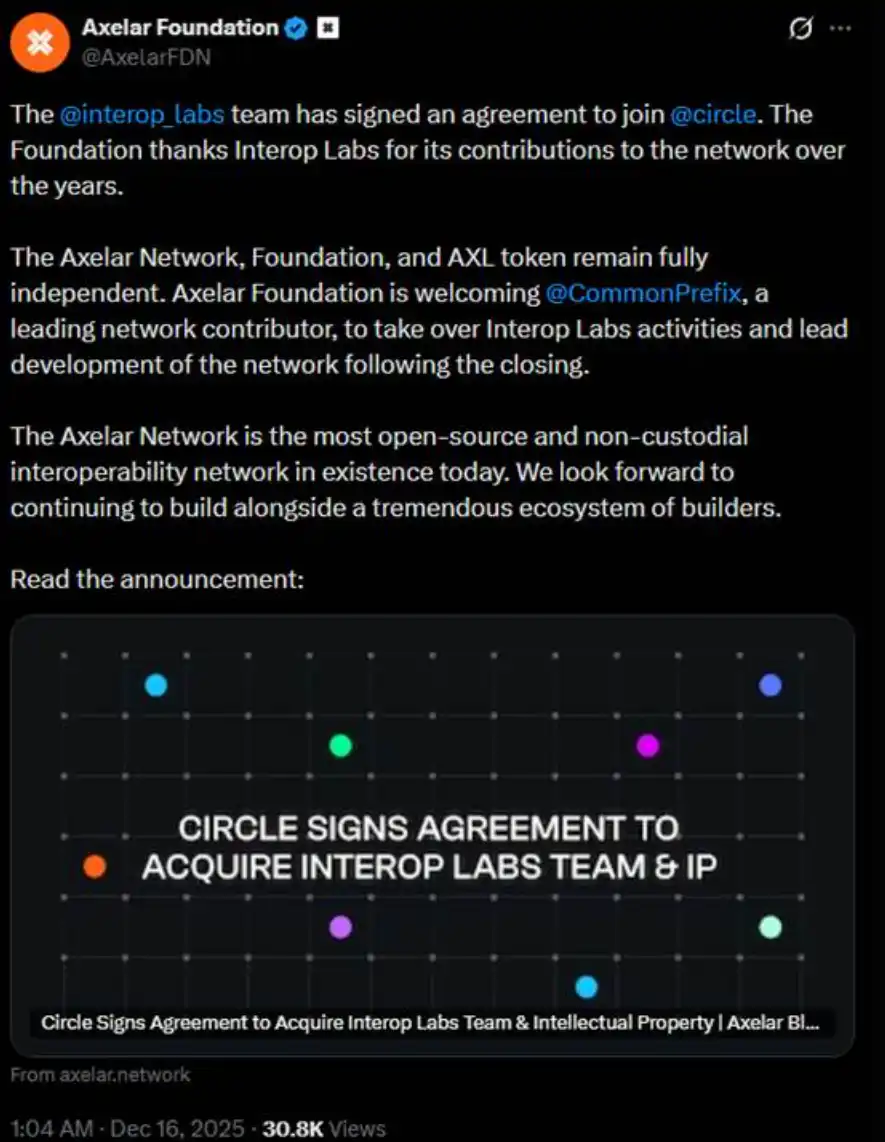

In the early hours of the day before yesterday, the Interop Labs team (the initial developer of Axelar Network) announced its acquisition by Circle to accelerate the development of its multi-chain infrastructure Arc and CCTP.

Normally, being acquired is good news. However, the further detailed explanation provided by the Interop Labs team in the same tweet caused an uproar. They stated that the Axelar network, foundation, and AXL token would continue to operate independently, with development work being taken over by CommonPrefix.

In other words, the core of this transaction is the "team merging into Circle" to promote the application of USDC in the fields of privacy computing and compliant payments, rather than a comprehensive acquisition of the Axelar network or its token system. The team and technology, Circle is taking. The original project, Circle is not managing.

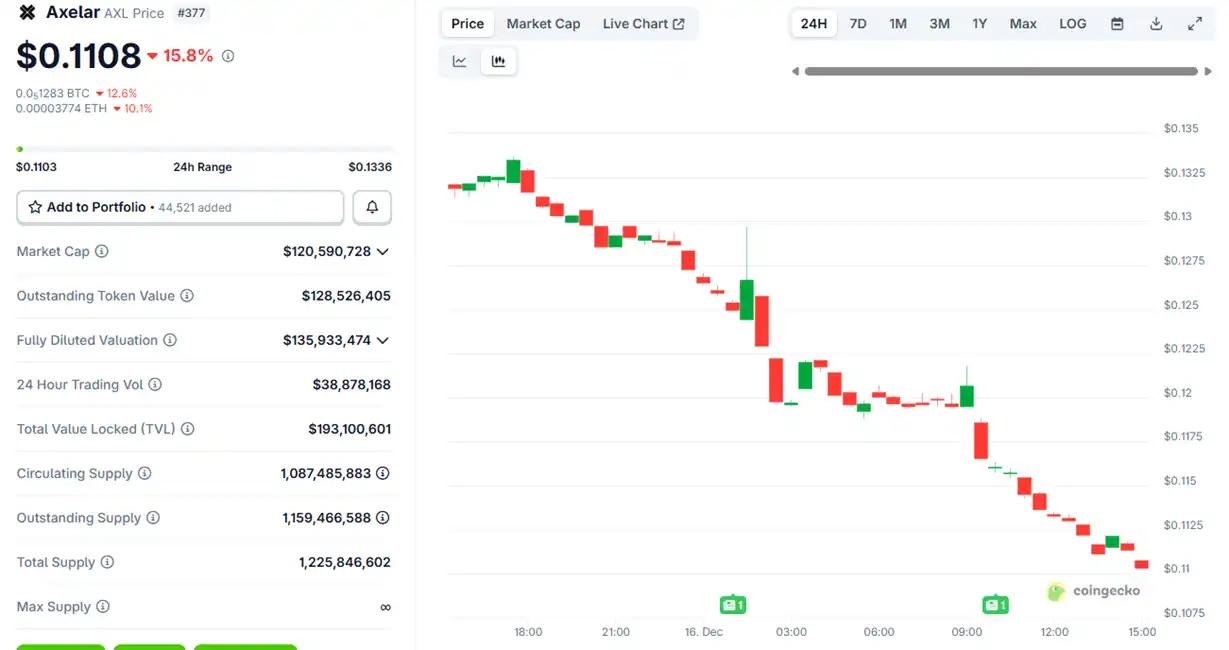

After the acquisition news was announced, the price of Axelar token $AXL first rose slightly and then began to fall, currently down about 15%.

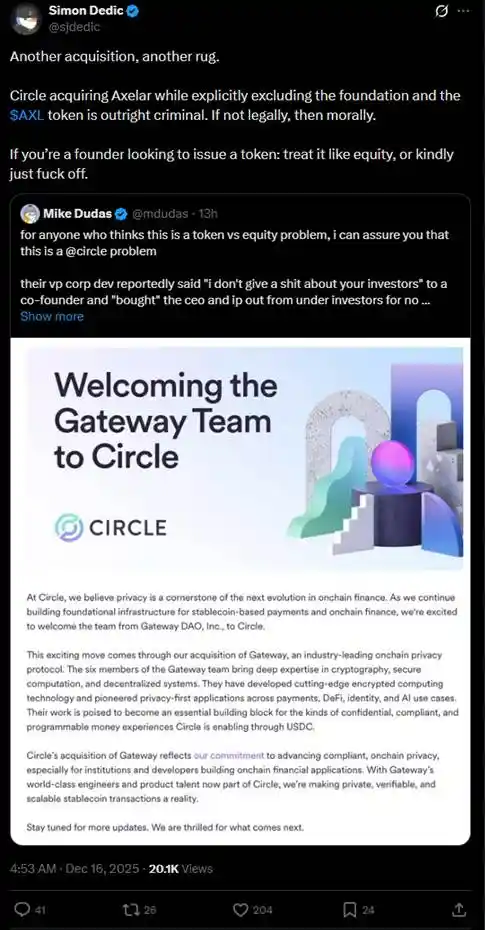

This arrangement quickly sparked intense discussions in the community about "token vs equity." Multiple investors questioned that Circle essentially acquired the core assets through the acquisition of the team and intellectual property, but bypassed the rights of AXL token holders.

Over the past year, similar cases of "acquiring the team and technology, but not the token" have occurred repeatedly in the crypto space, causing serious harm to retail investors.

In July, Ink, the Layer 2 network under Kraken, acquired the decentralized trading platform Vertex Protocol based on Arbitrum, taking over its engineering team and trading technology architecture, including the synchronous order book, perpetual contract engine, and money market code. After the acquisition, Vertex shut down its services on 9 EVM chains, and the token $VRTX was abandoned. After the news was announced, $VRTX fell more than 75% that day and gradually "went to zero" (current market cap is only $73,000).

However, $VRTX holders at least had a tiny bit of comfort because they would receive a 1% airdrop during the TGE of Ink (snapshot has ended). Next, there are even worse cases, where the token is directly invalidated without any compensation.

In October, pump.fun announced the acquisition of the trading terminal Padre. When the acquisition of Padre was announced, pump.fun also stated that the Padre token would no longer be used on its platform and directly indicated that there were no future plans for the token. Since the declaration of the token's invalidation was in the last reply of the thread, the token doubled instantly and then plummeted sharply. Currently, $PADRE has a market cap of only $100,000.

In November, Coinbase announced the acquisition of the Solana trading terminal Vector.fun built by Tensor Labs. Coinbase integrated Vector's technology into its DEX infrastructure, but did not involve the Tensor NFT market itself or the equity of $TNSR. Part of the Tensor Labs team moved to Coinbase or other projects.

The price movement of $TNSR was relatively stable among the examples, rising sharply and then falling back. The current price has returned to a level appropriate for an NFT market token and is still higher than the low before the acquisition news.

In Web2, it is legal for large companies to acquire small companies by "taking the team and intellectual property, but not the equity." This situation is called an "acquihire." Especially in the tech industry, "acquihire" allows large companies to quickly integrate excellent teams and technologies, avoiding the lengthy process of hiring from scratch or internal development, thereby accelerating product development, entering new markets, or enhancing competitiveness. Although it is unfavorable to small shareholders, it stimulates overall economic growth and technological innovation.

Nevertheless, "acquihire" must also satisfy the principle of "acting in the best interests of the company." The reason these examples in the crypto space have made the community so angry is precisely because the "small shareholders," as token holders, completely disagree that the project parties in the crypto space are "acting in the best interests of the company" for the better development of the project through acquisition. Project parties often dream of listing on the US stock market when the project itself can make big money, and then issue tokens to make money when everything is just starting or declining (the most typical example is OpenSea). After these project parties make money from the tokens, they turn around to find their next opportunity, leaving the past projects only in their resumes.

So, can retail investors in the crypto space only swallow their broken teeth? It was also the day before yesterday that Ernesto, former CTO of Aave Labs, published a governance proposal titled "$AAVE Alignment Phase 1: Ownership," firing a shot to defend token rights in the crypto space.

The proposal advocates that Aave DAO and Aave token holders clearly control core rights such as protocol IP, brand, equity, and revenue. Aave service provider representatives such as Marc Zeller publicly endorsed the proposal, calling it "one of the most influential proposals in Aave governance history."

Ernesto mentioned in the proposal, "Due to some past events, there is strong hostility towards Aave Labs in previous posts and comments, but this proposal strives to remain neutral. This proposal does not imply that Aave Labs should not be a contributor to the DAO or lacks the legitimacy or ability to contribute, but the decision should be made by Aave DAO."

According to the interpretation by crypto KOL @cmdefi, the cause of this conflict lies in Aave Labs replacing the front-end integrated ParaSwap with CoW Swap, after which the generated fees flowed to Aave Labs' private address. Accordingly, Aave DAO supporters believe this is a form of plunder because, with the existence of the AAVE governance token, all benefits should优先 flow to AAVE holders or remain in the treasury for DAO voting decisions. Additionally, previously, ParaSwap's revenue would continuously flow into the DAO. The new CoW Swap integration changed this status, further leading the DAO to believe this was a plunder.

This very directly reflects a contradiction similar to that between "shareholders and management," and again highlights the awkward positioning of token rights in the crypto industry. In the early days of the industry, many projects promoted the "value capture" of tokens (such as obtaining rewards through staking or directly sharing profits). But since 2020, SEC enforcement actions (such as lawsuits against Ripple and Telegram) have forced the industry to shift towards "utility tokens" or "governance tokens," which emphasize usage rights rather than economic rights. As a result, token holders often cannot directly share project dividends—project revenue may flow to equity held by the team or VCs, while token holders are like small shareholders contributing for free.

As in the examples mentioned in this article, project parties often sell teams, technological resources, or equity to VCs or large companies, while also selling tokens to retail investors. The final result is that resource and equity holders profit first, while token holders are marginalized or even get nothing. Because tokens do not have legally defined investor rights.

To avoid the regulation that "tokens cannot be securities," tokens are designed to be increasingly "useless." Because regulation is avoided, retail investors are placed in a very passive and unprotected position. The various cases that have occurred this year have, in a sense, reminded us that the current problem of "narrative failure" in the crypto space may not be that people no longer believe in narratives—narratives are still good, profits are still good, but when we buy tokens, what exactly can we expect?