Original | Odaily Planet Daily (@OdailyChina)

Author | jk

Introduction: Who Is Laying the Groundwork for the Next Bull Run?

The crypto bull market of 2024-2025 was, in essence, a story of institutionalization. The force that drove Bitcoin to break through $100,000 was not retail FOMO sentiment, but the net inflows from BlackRock's IBIT ETF and the ongoing bond financing for coin purchases by Strategy (formerly MicroStrategy). The underlying logic of that bull run was inseparable from the accumulation quietly completed by institutions during the 2022-2023 bear market.

History seems to be repeating itself now, but the details are截然不同 (entirely different). In Q1 2026, Bitcoin retreated over 25% from its highs, Ethereum fell even deeper, and market sentiment turned cold again. Yet, against this backdrop, a group of institutions moved in the opposite direction to the price trend: corporate treasuries are adding, sovereign wealth funds are adding, bank-affiliated ETFs are listing, and traditional European financial institutions are entering the stablecoin space. All this points to the same question: If the next major rally is still to be driven by institutional capital, then who exactly is buying during this bear market accumulation phase?

Odaily reporters conducted an in-depth investigation into the capital inflows of the crypto market in Q1.

Conclusion first: Despite a brutal market pullback in Q1, institutional capital continued to flow into the crypto market. Bitcoin fell over 25% from around $88,000 to the mid-$60,000s, Ethereum plunged as much as 35%, yet Strategy still counter-trend accumulated over $10 billion worth of Bitcoin, sovereign wealth funds like Mubadala also bought the dip, and meanwhile, about 26 single-asset crypto ETFs were issued or applied for under the SEC's new universal listing rule framework.

The buying capital in Q1 2026 showed a clear divergence: Some hedge funds significantly reduced holdings (Brevan Howard cut IBIT holdings by 85%), while corporate treasuries, university endowments, ETF issuers, and Abu Dhabi sovereign funds took the opportunity to buy the dip In terms of venture capital, while the number of deals plummeted by 49%, the quarterly financing amount remained around $5-6.8 billion, with three deals (BVNK, Kalshi, Polymarket) accounting for half of the total. Externally, the SEC's new rules in September 2025 compressed the ETF approval cycle from 240 days to 75 days; on March 17, 2026, the SEC and CFTC joint statement classified staking rewards as non-securities, triggering a wave of intensive staking ETF issuances.

Part One: Active Institutional Buyers and Capital Deployment

New Crypto ETFs (Jan-Apr 2026)

Newly launched crypto ETF products were密集 (dense) this quarter. Bitwise launched the Chainlink ETF (CLNK) on NYSE Arca on Jan 14 with $2.5 million in seed capital. Canary Capital launched two products on Jan 13: the Litecoin Spot ETF (LTCC, cumulative AUM ~$9.7 million, the first US spot LTC product) and the HBAR ETF (the first US spot Hedera product); the company subsequently launched a staking SUI ETF with rewards in February. Grayscale also launched a SUI Staking ETF in February. 21Shares launched the SUI ETF (TSUI, AUM ~$12.5 million) on Nasdaq on Feb 24, and the Polkadot ETF (TDOT, fee 0.30%, the first US spot DOT product, AUM ~$11 million in the first week) on Mar 6.

Old money also released some ETFs. BlackRock launched the iShares Ethereum Staking Trust (ETHB) on Mar 12, becoming the first major institutional staking ETH ETF, with about 82% of staking rewards distributed directly to holders. Morgan Stanley launched the Morgan Stanley Bitcoin Trust (MSBT) on Apr 8, the first US bank-affiliated spot BTC ETF, with a fee of 0.14%, attracting $34 million on the first day, and reaching a cumulative size of $133 million 8 days after listing. Additionally, ProShares launched the CoinDesk 20 Crypto Index ETF (KRYP) on NYSE Arca between Jan and Feb; NEOS launched the Enhanced Bitcoin High Yield ETF (XBCI) around Jan 29; Bitwise launched the Proficio Currency Depreciation ETF (BPRO, a BTC and precious metals combo); Nomura/Laser Digital launched the Bitcoin Diversified Yield Fund (BDYF, a tokenized yield product) on Jan 22; 21Shares launched the Strategy Yield ETP (STRC, BTC-backed) in Zurich on Feb 25; Hashdex expanded NCIQ in Q1 to cover BTC, ETH, XRP, SOL, and XLM.

In summary, New Money, meaning ETFs for smaller market cap coins, are being launched, but the ETFs from more established Old Money are still focused on high-market cap, established coins.

Notable ETF Applications (Pending approval as of Apr 23)

Morgan Stanley submitted S-1 applications for spot BTC (MSBT, listed in Apr), Solana, and ETH trusts in early January. Goldman Sachs submitted an application for a Bitcoin Premium Income/Options Strategy ETF on Apr 14. Hyperliquid (HYPE) attracted competing applications from four institutions: Grayscale (GHYP, Mar 20), Bitwise (BHYP, Apr 10), 21Shares (THYP, Apr 14), and VanEck (VHYP) are currently not approved for listing. Grayscale, VanEck, 21Shares, Bitwise, and Canary all submitted applications for ADA spot ETFs; CME's ADA futures contract also launched on Feb 9. Truth Social (Yorkville) submitted applications for a BTC+ETH combo ETF and a Cronos Yield Enhanced ETF on Feb 13. Bitwise submitted 11 crypto strategy ETFs (covering AAVE, UNI, ZEC, TAO, etc.). REX-Osprey/Defiance submitted applications for 27 crypto ETFs, including staking products and 3x leveraged products.

For now, the Hyperliquid ETF remains the most anticipated.

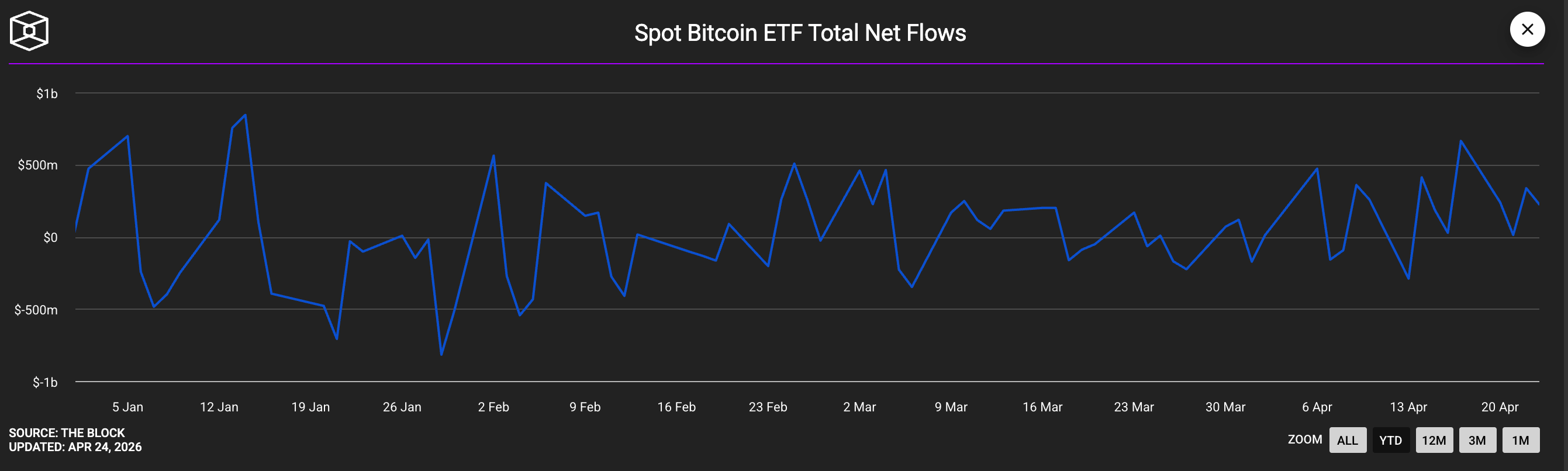

ETF Fund Flows (Q1 2026)

Spot BTC ETF flows were volatile: Net outflows of ~$1.6 billion in January (crypto.com data showed the third consecutive month of net outflows), but as buying returned in Mar-Apr, the quarter ultimately narrowed to a net positive value. BlackRock's IBIT remained the flagship product, with net inflows of ~$8.4 billion in Q1, but AUM shrank from ~$78 billion to ~$54 billion due to price decline. Ethereum ETFs set a record of 19 consecutive days of positive inflows in early January. XRP ETFs had net inflows of $1.07 billion for the quarter, with 43 consecutive days of positive inflows, significantly outperforming BTC products during the same period. Solana ETFs (BSOL, FSOL) combined AUM broke $1 billion in April; Goldman Sachs disclosed holding $108 million in SOL ETF positions.

Net inflows positive for the full quarter

Public Company Bitcoin Treasury Purchases

Strategy (MSTR) continued high-intensity accumulation this quarter. As of Apr 20, 2026, Strategy累计持有 (cumulatively held) 815,061 BTC, with an average price of $75,527, and a cost basis of ~$61.6 billion. Japanese listed company Metaplanet (3350.T) disclosed on Jan 1, 2026, purchasing 4,279 BTC at an average price of $104,638, totaling over $380 million; it added a total of 5,075 BTC in Q1, disclosing on Apr 2 a cumulative holding of 40,177 BTC, with Q1 purchase costs around $400 million.

Strive (ASST) purchased 123 BTC on Jan 13 at $91,561 each, totaling $11.3 million; subsequently completed an all-stock merger with Semler Scientific, with the merged company holding 12,798 BTC, ranking 11th among corporate treasuries; the merger was completed on Jan 16. By mid-March, Strive held ~13,628 BTC cumulatively through PIPE and the Semler merger. DDC Enterprise (NYSEAM) added ~600 BTC just in January, holding 2,383 BTC cumulatively by Mar 19, with a total value of $182 million.

BSTR Holdings (led by Adam Back, operated by Cantor SPAC) announced it would proceed with a listing backed by 30,021 BTC (worth $2.14 billion). Twenty One Capital (XXI) held 43,514 BTC (worth over $3.1 billion) as of Apr 2, making it the second-largest Bitcoin holder among public companies. Hyperscale Data (GPUS) held 663 BTC as of Apr 21, entering with $50.3 million, targeting a treasury size of $100 million.

Ethereum & Staking Related Corporate Treasuries

BitMine Immersion (BMNR) is currently the largest Ethereum corporate treasury, staking 74,880 ETH (~$219 million) via the MAVAN platform in Q1; it purchased 101,627 ETH (over $230 million) in the week of Apr 20, 2026, its largest weekly purchase in 2026 so far. As of Apr 20, the company held ~5 million ETH cumulatively, with ~3.33 million staked, AUM ~$12.9 billion. SharpLink Gaming (SBET) is the second-largest Ethereum treasury, holding ~867,000 ETH (value $1.7-$2.3 billion), nearly 100% staked, disclosed on Mar 10.

Major Sellers

Bitcoin miners were net sellers overall in Q1. MARA Holdings sold 15,133 BTC for $1.1 billion from Mar 4-25 to repurchase convertible notes; Riot Platforms sold 3,778 BTC for $290 million; Nakamoto Holdings sold 284 BTC; Genius Group liquidated its entire 84 BTC holdings on Apr 1. The Kingdom of Bhutan (Druk Holdings) transferred ~$42 million worth of BTC in small amounts throughout the year. Strategy alone accounted for 94% of the net Bitcoin accumulation by all public companies in March.

Bank & Asset Manager Moves

Morgan Stanley not only filed ETF applications; the bank applied to the OCC for a National Trust Bank Charter for digital assets in Feb 2026 and announced opening BTC/ETH/SOL trading to retail clients via E*Trade/Zerohash.

UBS announced on Jan 23 offering BTC/ETH trading services to Swiss private bank clients, covering its $7 trillion wealth management business.

Citigroup announced the launch of institutional-grade BTC custody infrastructure at the Strategy World conference on Feb 26. Standard Chartered launched institutional BTC/ETH custody services in Hong Kong in January and is reportedly in talks to acquire full ownership of its Zodia Custody unit (Apr 8).

BBVA (Banco Bilbao Vizcaya Argentaria) recommended high-net-worth clients allocate 3-7% to crypto assets.

12 European banks (BBVA, BNP Paribas, ING, UniCredit, KBC, Danske Bank, Handelsbanken, CaixaBank, DZ Bank, DekaBank, Landesbank Baden-Württemberg, Banca Sella) formed the Qivalis Euro stablecoin consortium based on the Fireblocks platform, compliant with the MiCA regulatory framework (Apr 21).

Vanguard Group opened access to third-party crypto ETFs for its 50 million brokerage clients on its $11 trillion platform. Fidelity offers a 1% BTC allocation option in its 401(k) pension plans, reportedly attracting about $800 million.

Nomura Securities, Daiwa Securities, and SMBC Nikko Securities all announced plans to launch cryptocurrency exchanges in Japan by the end of 2026.

13F Disclosures (Q4 2025 Holdings, disclosed Feb 2026)

Goldman Sachs' crypto ETF holdings totaled ~$2.36 billion, covering BTC ($1.06 billion), ETH ($1.0 billion), XRP ($152 million), SOL ($109 million), but BTC and ETH positions were cut by 39% and 27% QoQ respectively.

Mubadala (Abu Dhabi sovereign wealth fund) increased its IBIT holdings by 46% to 12.7 million shares (~$631 million), counter-trend accumulating the equivalent of ~2,300 BTC during the market downturn.

Al Warda Investments (under Abu Dhabi Investment Authority) increased IBIT holdings to 8.2 million shares (~$437 million), pushing Abu Dhabi sovereign capital's crypto exposure合计突破 (combined past) $1 billion.

Millennium increased IBIT holdings by ~67% (increase equivalent to ~8,100 BTC, making it the largest holder overall).

Jane Street increased IBIT holdings by over 50% to 20 million shares.

Harvard University reduced IBIT holdings by 21.5% but established its first ETH position (3.87 million shares of ETHA, value $86.8 million). Dartmouth College became the fourth Ivy League school to enter.

On the selling side: Brevan Howard slashed IBIT holdings by 85% (from 37.5 million shares to 5.5 million shares, equivalent to selling ~17,700 BTC); Farallon cut by 70% (cut ~2,800 BTC); Tudor reduced by ~1,300 BTC; D.E. Shaw hedge fund halved IBIT; Sculptor nearly liquidated FBTC (cut ~90%).

Sovereign Wealth Funds & Governments

Besides Mubadala and Al Warda, the Luxembourg sovereign wealth fund FSIL maintained a 1% Bitcoin allocation (~€8.5 million), becoming the first Eurozone sovereign wealth fund to hold BTC. El Salvador continued its "buy 1 BTC daily" strategy (now holds 7,547 BTC, total ~$635 million) and added $50 million in gold reserves on Jan 29. The Czech National Bank (purchased Nov 2025, continued into 2026) remains the only central bank in the world holding Bitcoin.

Zero additions to the US Strategic Bitcoin Reserve to date. CoinDesk confirmed on Mar 6 that the executive order was "progressing slowly"; the reserve still only holds ~328,372 seized BTC. White House Digital Asset Committee member Patrick Witt reiterated the commitment, but actual purchase actions have not occurred. Among US states, only Texas injected $5 million into IBIT in Nov 2025 (another $5 million remains unused). New Hampshire and Arizona have relevant legislation but have not deployed funds. Reports about CalPERS planning to allocate 1% (~$500 million) to BTC continue to circulate, but CalPERS has not officially confirmed.

Family Offices

Two surveys revealed截然相反的态势 (diametrically opposed trends): The J.P. Morgan Private Bank 2026 Family Office Report showed that among 333 surveyed institutions (average net worth $1.6 billion), 89% stated they had no Bitcoin allocation whatsoever, with AI investment being the primary focus. The BNY Mellon Wealth/NOIA survey showed that 74% of ultra-high-net-worth family offices are investing in or exploring crypto assets (significantly up from 53% the previous year), with typical allocation ratios of 2-5%, ~5% for Asian institutions, and ~2-4% for US and European institutions.

Part Two: Q1 2026 Crypto Venture Capital Financing Summary

Crypto VC financing in Q1 2026 presented a paradox: capital volume was还算稳健 (relatively robust) (down 8% YoY to 16%), but the number of deals plummeted by 49%. The most comprehensive statistics come from Crypto-Fundraising.info (Apr 1), recording 222 deals including M&A, with a total financing amount of $6.81 billion; excluding M&A, pure VC funding was 183 deals, totaling $4.77 billion. DefiLlama/DL News (Apr 4, VC only) tracked 53 deals over $10 million,合计约 (totaling approximately) $5 billion. J.P. Morgan estimated total digital asset inflows of ~$11 billion in Q1, about one-third of the Q1 2025 level. Galaxy Research's quarterly crypto VC report, regularly released, had not been published as of Apr 23, but its Q4 2025 benchmark data ($8.5 billion/425 deals) is available for sequential comparison.

Core Data

Compared to Q1 2025 (VC funding $5.37 billion, 358 deals) and Q4 2025 ($8.5 billion, 425 deals), Q1 2026 VC funding was ~$4.77 billion, down 11% YoY and down 44% QoQ; the number of deals was 183, down a sharp 49% YoY and 57% QoQ. Notably, the average VC deal size increased 76% YoY to $35.9 million (median $8 million), reflecting significant polarization: Seed stage was the most active by number of deals (37 deals, $252 million total), while the average size of four Series C rounds was as high as $108.8 million. Pre-Seed stage average was only $1.75 million, and the mid-market几乎萎缩 (almost萎缩 shrank).

Three Deals Gobbled Up Half the Quarter

Financing this quarter was extremely concentrated and heavily back-loaded. March alone generated $4.43 billion in financing (65% of the quarter), while February ended惨淡 (dismally) at $686 million.

Just the following three deals合计达 (combined reached) $3.4 billion, accounting for about half of the total disclosed financing for the quarter: payment sector M&A target BVNK ($1.8 billion, Mar 17), prediction market platform Kalshi (growth round led by Coatue, valuation $22 billion, $1.0 billion, Mar 19), and Intercontinental Exchange's strategic investment in Polymarket ($600 million, Mar 27).

The battle for prediction market leadership has intensified in the financing arena.

Other notable large financings include: Rain ($250 million Series C, stablecoin payments, led by Iconiq/Dragonfly/Galaxy, valuation ~$1.95 billion, Jan 9); BitGo completed an IPO on the NYSE, raising $213 million (Jan 22); XBTO strategic financing $217 million (Mar 25); Flying Tulip token issuance $206 million (FDV $1 billion); Whop received a $200 million investment from Tether (Feb 25); BlackOpal LatAm RWA financing $200 million (Jan 8); Kraken/Payward completed a $200 million secondary market transaction led by Deutsche Börse, valuation $13.3 billion; LMAX Group received a $150 million investment from Ripple (Jan 15); Alpaca completed a $150 million Series D; Bluesky received a $100 million Series B led by Bain Capital Crypto (Mar 19); Anchorage Digital received a $100 million investment from Tether, valuation over $4 billion (Feb).

Sector Distribution: Payments & Prediction Markets Outpace DeFi

The star sectors of the 2021 bull cycle—chain gaming, NFTs, L1 infrastructure—have almost disappeared from the top of the financing rankings.

- Payments/Stablecoins led with $2.39 billion (35% share, 17 deals);

- Prediction Markets followed with $1.72 billion (25.2%, 11 deals);

- Finance/CeFi ranked third with $835 million (12.2%, 25 deals).

- RWA (Real World Assets) financing $284 million (4.2%, 7 deals)

- Trading Markets/Platforms $255 million (3.7%, 2 deals)

- Infrastructure/L1-L2 financing $184 million (2.7%, 12 deals)

- DeFi only $89 million (1.3%, 5 deals)

- NFTs/Chain Gaming/Metaverse were almost negligible.

The top three sectors combined absorbed 72% of the quarter's disclosed capital.

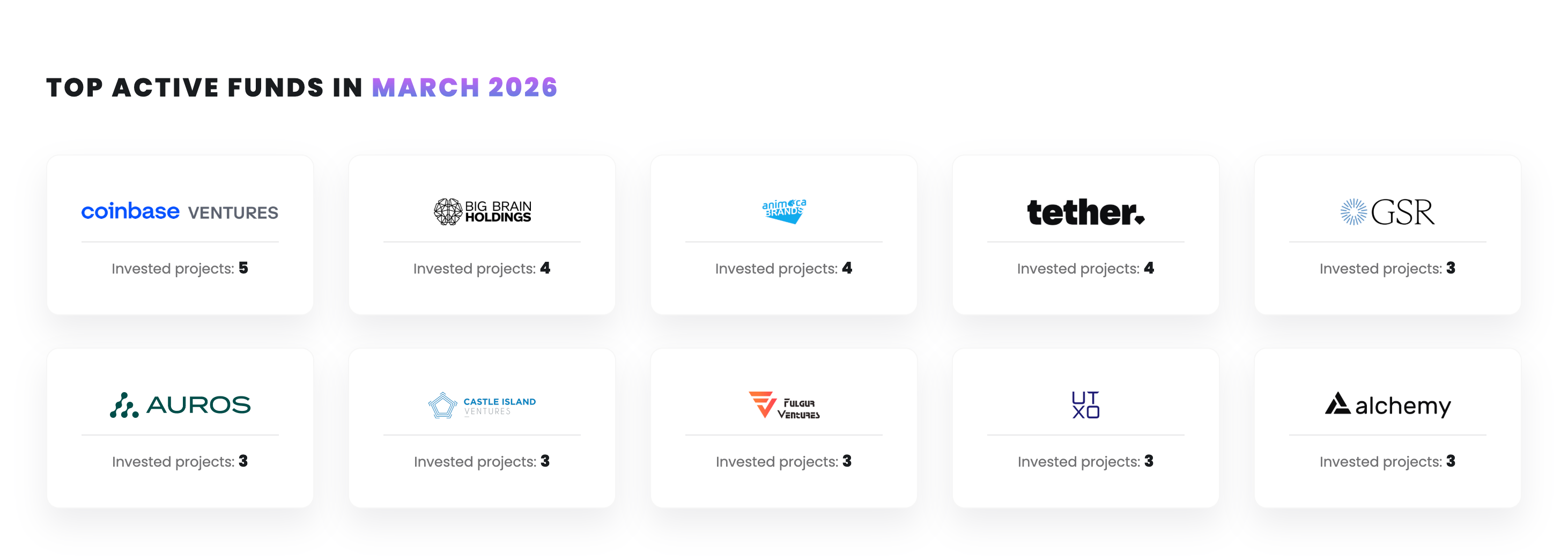

Active Investment Firms

Coinbase Ventures topped the list of institutional investors by participation count with 12 deals, more than double the second place. Followed by: Tether (8 deals), Animoca Brands (7 deals), CMT Digital (6 deals), and a16z crypto, Castle Island, Big Brain, Galaxy Digital (5 deals each) tied.

Most active funds in March

Traditional financial institutions entered the infrastructure sector with罕见力度 (rare intensity): Franklin Templeton participated in 4 deals, Intercontinental Exchange invested in Polymarket, Deutsche Börse took a stake in Kraken, Citadel Securities, Bain Capital, Sequoia Capital, and Alibaba also participated in Q1 funding rounds. Geographically, the three largest deals (BVNK, Kalshi, Polymarket) and the BitGo IPO were all from the US, showing the US share of crypto VC continued at the ~55% level seen in Q4 2025.

Conclusion: Institutional Capital Shows a Barbell Structure

In early 2026, the institutional crypto investment landscape is undergoing a two-way分化 (divergence).

On the buyer side, institutions with long-term conviction, such as Strategy, BitMine, Metaplanet, Mubadala, and the BlackRock ETF ecosystem, took advantage of the market downturn to increase their bets, while tactical hedge funds (Brevan Howard, Tudor, Farallon) and most Bitcoin miners turned into net sellers. Strategy alone bought almost more Bitcoin in Q1 than all other public companies combined, and its weekly purchase from Apr 13-19 set the third-largest record in history.

The same两极格局 (bipolar pattern) played out in venture capital: super-large financings in payments and prediction markets continued to expand, while small and medium-sized projects generally faced a financing drought. The shift in sector leadership—from DeFi/NFTs/chain gaming to stablecoins, prediction markets, and compliant CeFi infrastructure—signals that the industry's growth engine is gradually shifting from speculative crypto-native narratives towards trading models closer to regulated fintech.

The biggest uncertainty currently comes from the US Strategic Bitcoin Reserve: despite high-profile announcements at the executive level for over a year, actual capital deployment remains zero. If the 2026 National Defense Authorization Act opens a funding path in the second half of the year, it will fundamentally reshape the demand landscape. Until then, the ones真正在买单 (truly paying the bill) are corporate treasuries and sovereign wealth funds, not Washington.