Author: Xu Chao, Wall Street News

"I lost an entire year's after-tax salary today."

This was the desperate cry left by a Reddit user on the forum last Friday.

Just a few days ago, silver was seen as the "GameStop of 2026," a symbol of retail investors banding together to fight against Wall Street. Reddit forums were flooded with "Diamond Hands" memes, vowing to send silver to the moon.

However, the狂欢 (carnival/euphoria) came to an abrupt halt within just three days.

Silver prices plummeted in free fall from a high of over $120 per ounce, crashing 40% in three days, not only erasing recent gains but also leaving a terrifying cliff on the chart.

For retail investors who bought at the peak, this wasn't a correction; it was a massacre. The silver market, once承载着 (carrying/hosting) dreams of sudden wealth, has been turned into a "mass grave" where retail investors buried themselves.

How did this happen? While we were talking about a "short squeeze," Wall Street's giants had already opened their bloody maws.

The Crazy Casino: When Silver Became a "Meme Stock"

The silver market in January 2026 could no longer be described as rational.

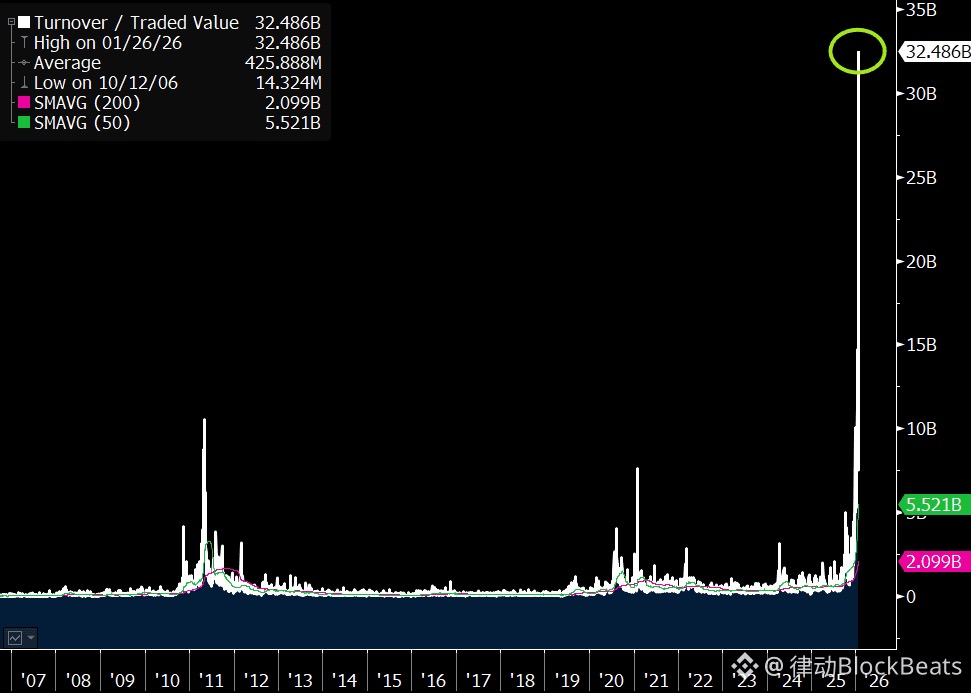

According to VandaTrack data, individual investors poured a record $1 billion net into silver ETFs in January alone.

This狂热 (frenzy) peaked on January 26th—trading volume for the silver ETF (SLV) reached a staggering $39.4 billion, almost matching the S&P 500 ETF (SPY)'s $41.9 billion.

Remember, this is an ETF for a single metal; its popularity nearly rivaled that of the entire U.S. stock market.

StoneX market analyst Rhona O’Connell was blunt: "Silver is severely overvalued, caught in a self-fulfilling madness. It's behaving like Icarus, flying too close to the sun, and will eventually get burned."

Social media acted as an accelerant for this狂欢 (carnival/euphoria).

On Reddit's WallStreetBets and Silverbugs sections, posts about silver surged to 20 times the five-year average. Retail investors, like they did rushing into GameStop in 2021, flocked en masse into this notoriously volatile market, trying to drown out fundamentals with sheer capital.

Bull and Baird market strategist Michael Antonelli told CNBC helplessly: "Silver has completely become the GameStop of 2026. The price doubled in three months, completely detached from industrial demand fundamentals, purely a vertical climb built on retail money."

But they forgot silver has a nickname: "gold on steroids." It rises疯狂 (crazily), and falls even more ruthlessly.

Crash Truth: Who Pulled the Trigger?

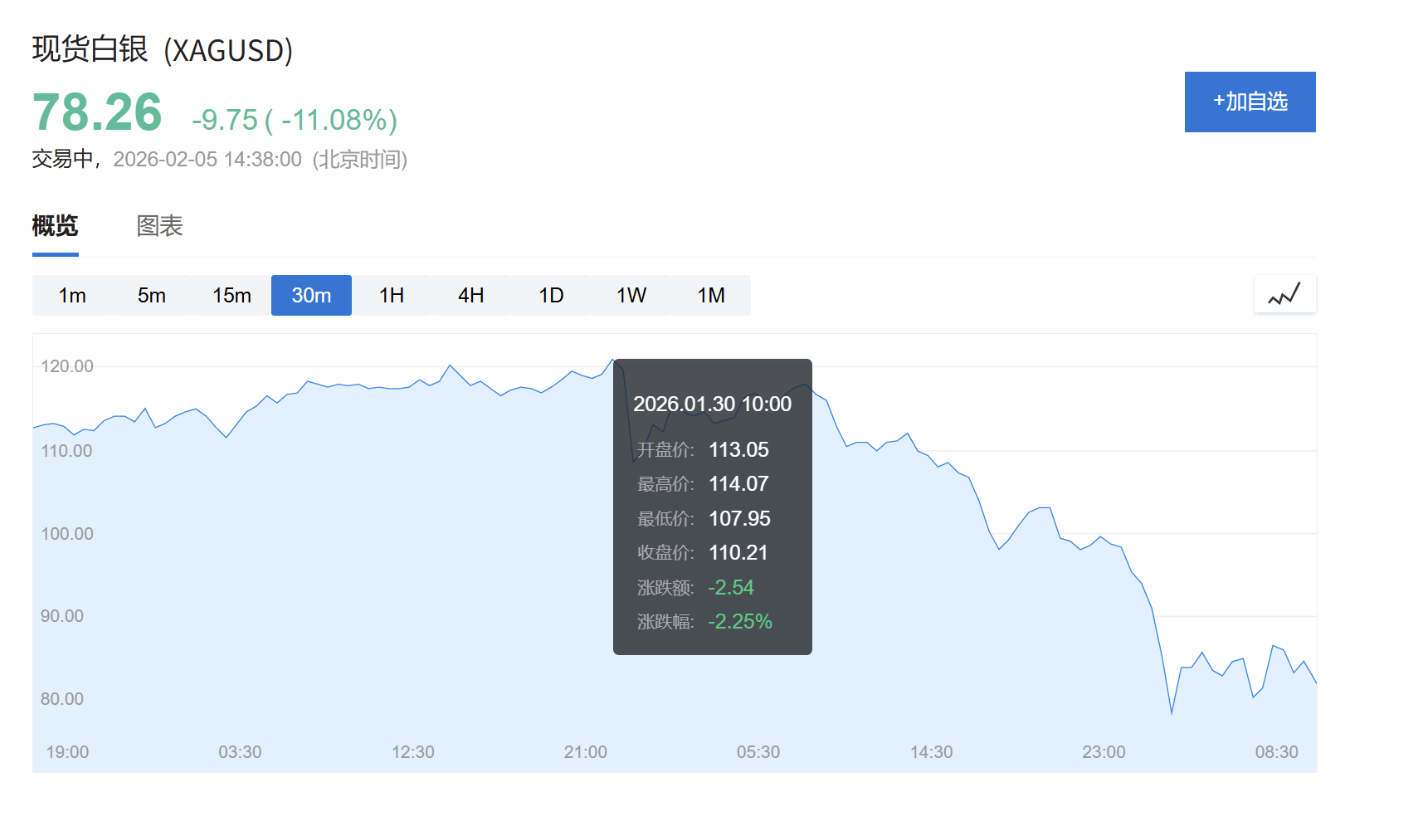

On January 30th, the惨案 (disaster) occurred. Silver experienced an epic sell-off within hours.

Media and analysts quickly found a perfect scapegoat: Kevin Warsh's nomination as Fed Chair.

The market's reasoning seemed logical: Warsh is a hawk, implying rates will stay high, which is bearish for non-yielding precious metals.

But the truth often lies in the details.

Warsh's nomination was announced at 1:45 PM ET (1:45 AM Beijing Time on Feb 1st). However, silver's crash began as early as 10:30 AM on the 30th. In the three-plus hours before the news was public, silver prices had already plunged 27%.

Blaming the Fed nomination was just a cover for the real "tool of slaughter"—margin requirements.

In reality, the true catalyst for this "mass grave" tragedy was a change in exchange rules. The Chicago Mercantile Exchange (CME) raised margin requirements for silver futures twice in the week before the crash, for a total increase of 50%.

What does this mean?

If you were a retail investor fully leveraged, your account previously only needed $22,000 to maintain the position. Suddenly, the exchange demanded you come up with $32,500. Can't produce the extra $10,500? Sorry, the system will automatically liquidate your position,不问价格 (regardless of price),不计成本 (regardless of cost).

This is why the crash was so rapid. Margin hikes triggered the first wave of forced liquidations, which caused prices to fall, which in turn triggered more people's liquidation thresholds. It's a vicious cycle, and retail investors are at the very bottom of this cycle.

An Asymmetric Game

While retail investors were wailing in the "mass grave," what were the institutions doing?

The answer might send a chill down your spine: They were waiting for retail sell-offs to buy low and profit. And this isn't illegal; it's a structural advantage built into the market's operation.

According to disclosures by columnist Luis Flavio Nunes, institutions, represented by JPMorgan, demonstrated textbook "profit-taking" methods during this crash:

Step 1: Access Emergency Liquidity.

While the exchange was raising margin requirements for retail investors, banking institutions were enjoying a "blood transfusion" from the Fed.

Data shows that on December 31st, banks borrowed a record $74.6 billion from the Fed's emergency lending window (SRF). This mechanism exists precisely to provide short-term liquidity to eligible financial institutions. Its design初衷 (original intention) is to prevent funding crises. But the reality is: Only specific institutions qualify to use this tool.

At the same time, the exchange raised silver margin requirements (by) 50% within a week. The Fed's emergency funding tool provides cash to eligible institutions at favorable rates. Retail investors have no access to equivalent channels of emergency central bank funding. This isn't favoritism. It's determined by the financial system's architecture: central banks lend to banks, not to individuals.

Step 2: Wait for the Market Chaos Caused by Margin Hikes.

The core mechanism of the silver crash lies in the difference in ability between retail and institutions to respond to increased margin requirements.

On December 26th and 30th, just before the crash, the CME raised margin requirements for silver trading by 50% in a short period. This meant a trader holding a position needed to immediately come up with 50% more cash.

For most retail investors, this sudden capital pressure directly triggered brokers' automatic liquidation mechanisms, forcing them to sell at any cost during the market plunge.

Meanwhile, institutions with access to Fed tools had more options.

They could draw on credit lines, obtain emergency loans, or quickly transfer funds between accounts. This doesn't prevent all liquidations, but it gives them more time and flexibility. Thus, retail positions were sold off during the panic, often at the worst prices. Institutional positions could be managed more strategically.

Step 3: Fully Utilize Authorized Participant Privileges for Arbitrage.

Take JPMorgan as an example. This bank plays a dual role in the silver market: they store all the physical silver for the largest silver fund (SLV), and they are also an "Authorized Participant," meaning they can create or destroy shares of that fund in large batches.

During the panic selling on January 30th, the SLV ETF's share price traded at an abnormal discount, falling to $64.50 per share, while the physical silver it represented was worth $79.53, a spread as high as 19%.

This provided huge arbitrage opportunities for institutions with "Authorized Participant" (AP) status through specific market mechanisms. Authorized Participants (a small group of large financial institutions) fully exploited this spread, buying ETF shares and redeeming them for higher-value physical silver.

Data shows approximately 51 million shares of SLV were redeemed that day, implying an arbitrage profit of about $765 million from this operation alone.

This operation helps maintain the link between the ETF price and its net asset value (NAV) and is a compliant market function, but it's a source of profit inaccessible to ordinary investors. Retail investors could see the discount but couldn't benefit from it due to lack of AP status.

Step 4: Strategic Positioning in Derivatives.

JPMorgan also held significant silver short positions, meaning they were betting on lower silver prices, or hedging other positions. As silver rose to $121 in late January, these positions were underwater.

The most ironic moment occurred at the price bottom. On January 30th, when retail investors were being forcibly liquidated at the low of $78.29 due to insufficient margin, JPMorgan stepped in. CME records show JPMorgan took over 633 contracts at this price, acquiring 3.1 million ounces of physical silver.

These crucial four steps happened almost on the same day. Did Wall Street orchestrate this series of events? This cannot be confirmed. But they were structurally positioned to benefit in multiple ways simultaneously: only institutions with their unique combination of roles and permissions could possibly do this.

"Silver is Always a Death Trap"

In this wave of行情 (market action/movement), countless retail investors like the Reddit user at the beginning of the article lost years of savings.

StoneX analyst Rhona O’Connell was right: "Silver is always a death trap."

Financial markets have never been a level playing field. When retail investors try to challenge the steel machine composed of algorithms, leverage, and rule-makers with "sentiment" and "memes," the outcome is often predetermined.

Silver is not GameStop either; it's a much more brutal arena than stocks.

Retail investors thought they were charging at Wall Street. Little did they know, they were unknowingly digging a huge "mass grave" with their own hands, then lining up to jump in.