Hyperliquid and Solana-based wallet Phantom have urged the U.S derivatives market regulator, Commodity Futures Trading Commission [CFTC], to modernize its regulations.

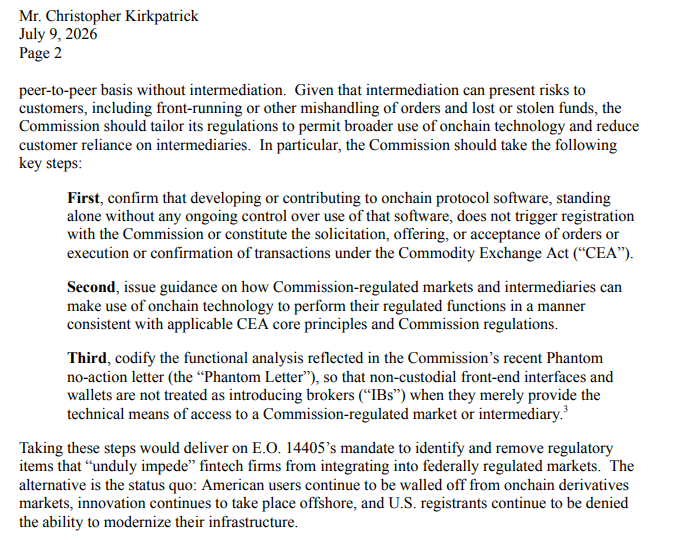

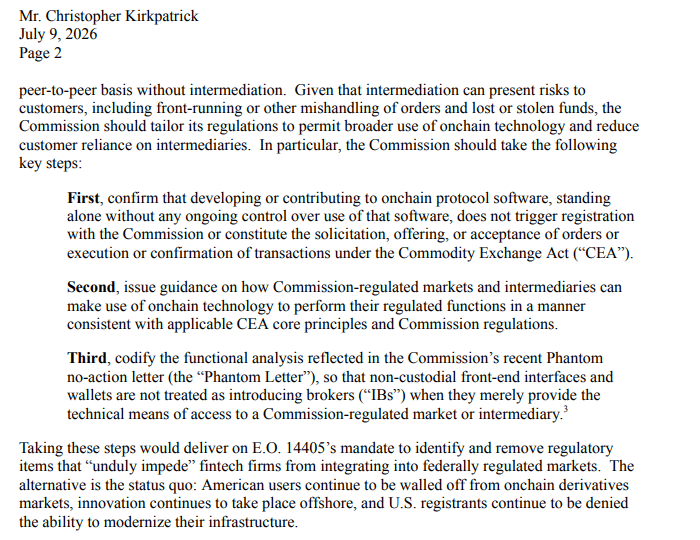

In a letter sent to the CFTC, the DeFi players requested three things. First, the agency should not treat a non-custodial software developer (users control funds, not the platform) as a broker.

In other words, creating on-chain protocols should not automatically trigger CFTC registration as an exchange or clearinghouse. Put plainly, they want developer protections.

Second, the no-action relief granted to self-custodial wallets, as issued to Phantom in March 2026, should be made formal guidance.

An industry coalition made a similar argument and pushed in April. If adopted, non-custodial DeFi front-ends like Phantom would not need broker-dealer or exchange registration to handle even U.S tokenized stocks.

Finally, they want the CFTC to create a framework that allows regulated entities to use blockchain for trading and settlement.

Why are DeFi firms seeking exemptions?

The letter was a response to the CFTC’s request for information regarding issues that are preventing fintechs from partnering with its regulated entities.

Some of the issues raised by Hyperliquid and Phantom are DeFi exemptions, some of which are being deliberated in the CLARITY Act. In fact, even the SEC is exploring a similar “innovation exemption” for tokenized assets trading.

The DeFi players cautioned that failure to explore these recommendations would reinforce the status quo, with dire consequences.

The alternative is the status quo: American users continue to be walled off from onchain derivatives markets, innovation continues to take place offshore, and U.S. registrants continue to be denied the ability to modernize their infrastructure.

Why DeFi exemptions request could be delayed

But these requests, even if granted, could trigger legal challenges from traditional market participants. The Chicago Mercantile Exchange (CME) has already sued the CFTC over its approval of Kalshi’s crypto perpetuals (perps).

CME argued that perps are swaps rather than futures, meaning the contracts should fall under its regulatory framework. That stance prompted the CFTC to reconsider how it defines swaps.

Hyperliquid Policy Center founder Jake Chervinsky called the CME lawsuit anti-competitive and a “shocking misjudgement.”

Citadel Securities and the umbrella body representing traditional exchanges have also opposed DeFi exemptions, particularly for tokenized asset trading. They argue regulators should treat every platform as a broker based on its function, not its underlying technology.

In short, DeFi platforms handling U.S. tokenized stocks should meet the same disclosure requirements and legal obligations as traditional exchanges.

Like CME, other traditional market participants could sue the agency if it grants the requested DeFi exemptions, particularly because lawmakers have not codified them and the CLARITY Act’s future remains uncertain.

Final Summary

- Hyperliquid and Phantom have requested CFTC for formalized exemptions for DeFi front-ends

- But with the CLARITY Act still in limbo, CME and other traditional players will continue to legally challenge the regulator over such requests.