There are no secrets in the crypto market, only differences in the speed of information dissemination.

It is indeed time to write a follow-up on Perp DEX. Over 20 projects are set to embark on their TGE journey by Q1 2026. From Aster's trading volume to StandX's maker points, the noise output to the market is unsettling everyone.

This should not cast doubt on Hyperliquid. The synergistic flywheel between HyperEVM and HYPE has not been successfully established, but Lighters cannot overwhelm the new king. We are immersed in firsthand accounts of the Binance and FTX rivalry, causing the Perp DEX War to become a secondhand memory.

Trapped in the New Chapter of HYPE

"Lighter isn't Lighter, Hyper is more Hyper"

Lighter is undoubtedly a successful project. It successfully landed after Hyperliquid validated the Perp赛道 (Perp赛道 is often used to refer to the perpetual futures exchange sector), creating the established impression that Hyperliquid is a counterpart to Binance, and Lighter is a counterpart to Hyperliquid.

Turtles cannot keep stacking indefinitely. Referring to the competitive landscape of exchanges themselves, OKX, outside of Binance, struggles immensely to operate OKB, and Coinbase's market capitalization is over 5 times that of Kraken's valuation.

Trading has a natural monopolistic effect. Even the second player in the industry cannot achieve self-sustaining cycles. The Perp DEX sector has already entered a red ocean phase. Large-scale market growth is impossible; what remains is merely a game of existing shares fought for the sake of TGE.

First, let's set the record straight on BNB. Binance Main站 (main platform) and BNB Chain need a connector, an action that HYPE has yet to complete.

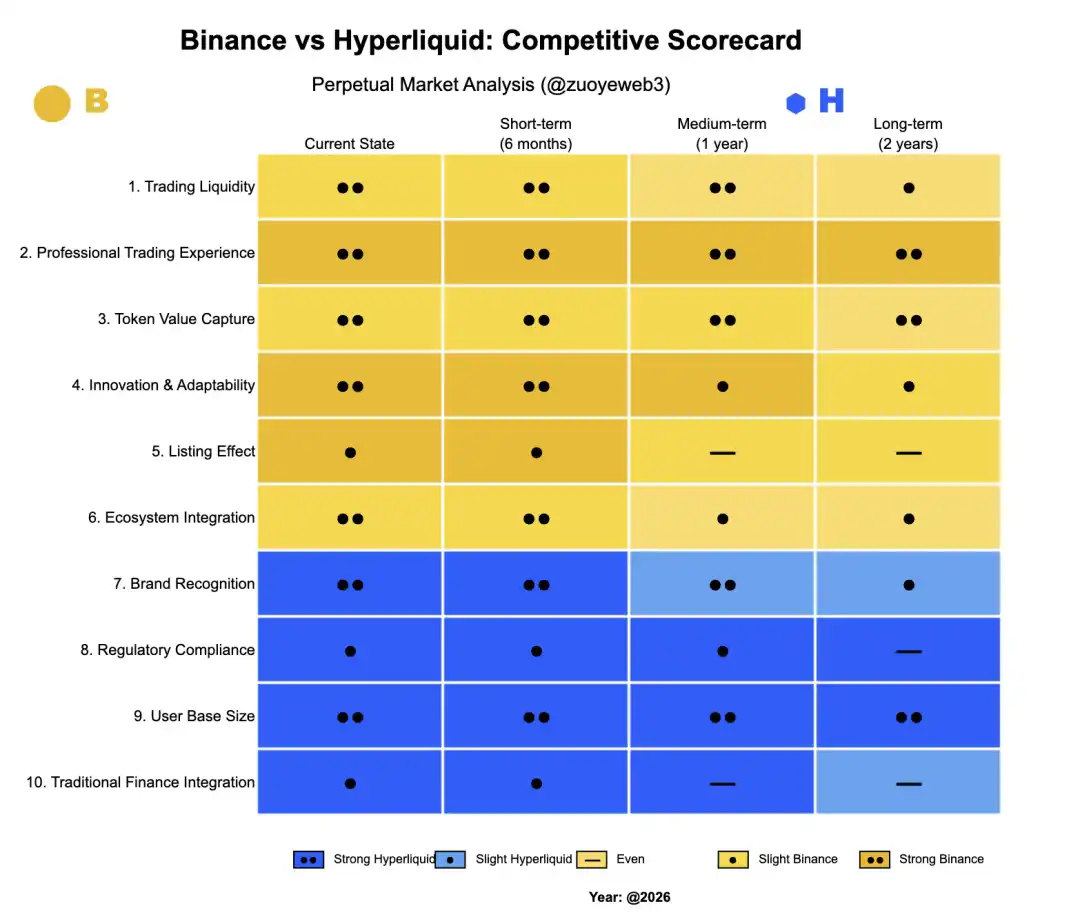

Image description: Comparison between Binance and Hyperliquid. Image source: @zuoyeweb3

Projects need Binance's "listing effect," hence they are willing to pay the highest channel fees. From Binance Main站's spot and futures trading to pre-market trading, and then to Wallet's Alpha and YZi Labs' EASY Residency, this is all true.

Binance needs projects' "traffic operations" outside the main platform to尽量延缓 (try to delay) the post-listing death curve. Therefore, favored projects on BNB Chain (like PancakeSwap and ListaDAO) need to absorb the projects' assets, using operational actions to延续 (continue) the next wave of the listing effect.

This is the real role of the entire BNB and BNB Chain for Binance. However, this is predicated on the existence of a listing effect on the Binance Main站, which conversely triggers Hyperliquid's need for self-breakthrough.

If we were to correct the logic above, Hyperliquid's rise is proof. Perps have long followed the established logic of "spot first, then futures," but Hyperliquid did not. Instead, it focused on 「trading Perps」 itself. This is based on the consensus across the industry, especially among exchanges, that the listing effect can no longer be guaranteed, and trading mainstream assets has become the norm.

-

OKX and others cannot maintain project prices after listing. They lack both liquidity and on-chain DeFi ecosystems,只能充当 (can only act as) second-tier distributors for projects. OKB lacks on-chain value capture capability and can only be used as an on-site coupon, losing the fundamental role of a token.

-

Hyperliquid provides traders with a professional experience. After FTX's collapse, HyperCore became synonymous with on-chain trading. The larger the trade, the more it needs Hyperliquid's liquidity support.

Let me add, Aster and CZ once promoted "privacy/dark pool trading," but could not shake Hyperliquid's market share. Aside from a minority need for money laundering, privacy is not a priority for traders. The need for KYC on Binance's main platform is also irrelevant.

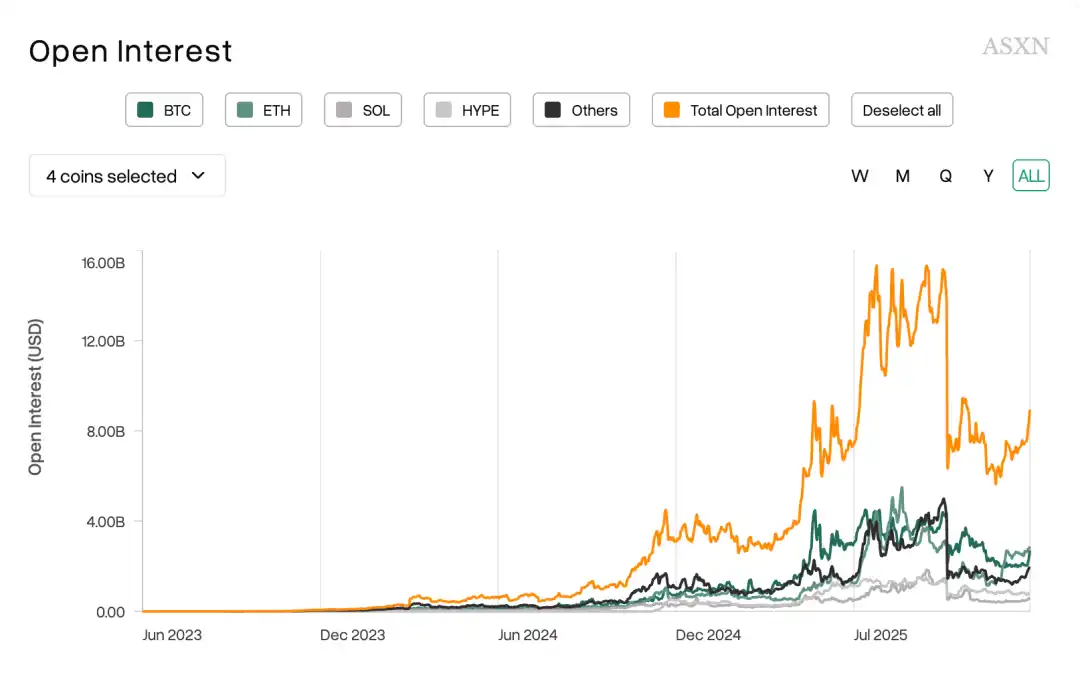

Image description: Mainly trading mainstream coins. Image source: @asxn_r

The truly fundamental and irreversible trend is that people only trade mainstream coins like BTC/ETH. New coins only have significant trading volume at launch. This holds true from BeraChain to the new generation L1s like Monad and Sonic.

The "listing effect" that top exchanges rely on for survival, and the fees that second and third-tier exchanges depend on, have无可奈何地走入历史 (helplessly become history). This might be the real reason behind exchanges operating their own Perp DEXs, promoting the trading of everything, and embracing traditional finance (stocks, forex, precious metals).

But none of this will harm Hyperliquid's liquidity. In the article 'RFQ Architecture: Market Makers, a Different Choice for Latecomer Perp DEXs', I pointed out that Variational's advantage/characteristic lies in opening the market maker architecture to ordinary retail users. This is a real market demand. However, the刷量积分赛 (volume-brushing points competition) for most Perp DEXs is a form of "前期负债" (early-stage debt), waiting to be cashed out at the TGE moment.

If you think Bitget's flashy marketing can capture Binance's derivatives market share, then StandX's maker points can challenge Hyperliquid's market share.

Markets with better liquidity naturally become the daily venue for traders. In the Perp DEX field, where the listing effect is even more lacking, the profiles of airdrop hunters and real users diverge even further. Let's not forget, most people are still relying on CEXs to buy dual-currency wins, let alone actually operate Perps on-chain.

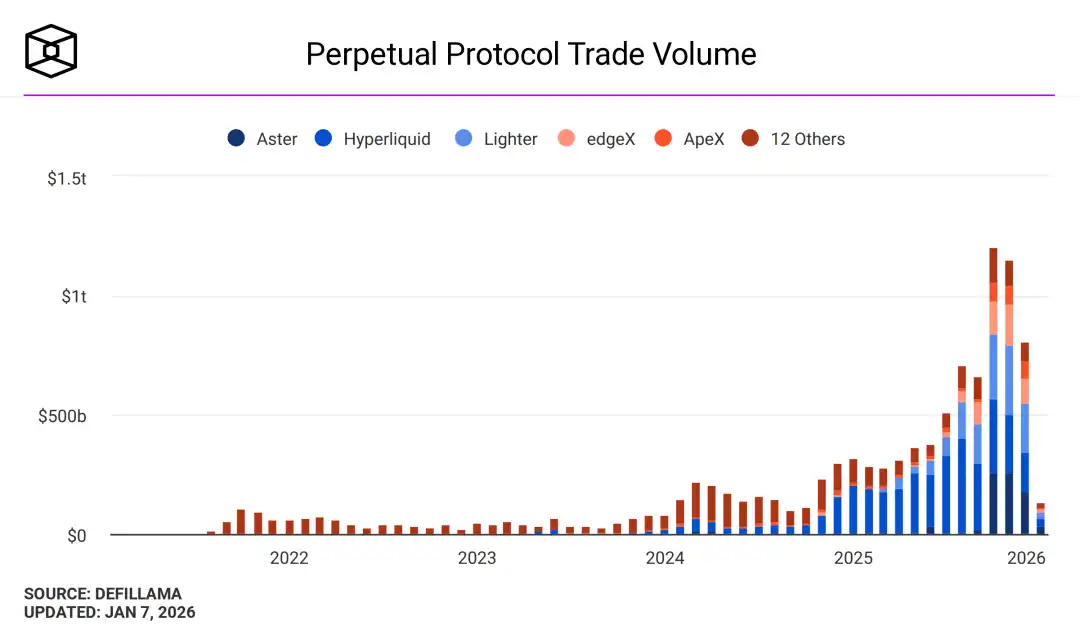

Image description: Perp DEX trading volume. Image source: @TheBlock__

Lighter accepts forex, Edge builds its own Chain. Without first overcoming HyperCore's liquidity, they have inevitably become complex to support their narratives. This will in turn reduce their token's value capture capability, evolving into something similar to OKB—an on-site coupon. Let's seriously address the expected "discount" due to regulation on Hyperliquid. From BitMEX onwards, CEXs/DEXs have never been rejected by the market due to US regulatory actions. Only incidents of theft or crashes have caused significant changes in market share.

-

Theft group: KuCoin (2020), ByBit (2025, over $1.4B stolen)

-

Crash group: BitMEX March 12, 2020, pulling the plug

-

Reputation group: Huobi—Sun Ge's pGala incident

Additionally, only SBF's FTX was FUDded to death by Coindesk, and it lost due to less江湖经验 (street smarts) compared to CZ. From this perspective, the 1011 incident is just an annual routine for veteran exchanges like Binance.

Now is a rare moment of relaxed regulation by the SEC. Binance has officially上岸 (come ashore) in Abu Dhabi. Hashkey has completed its Hong Kong IPO. Hyperliquid does not exist in a state that cannot be regulated. Even if the Hyperliquid team insists on the appearance of "decentralization," it can refer to Binance's multi-entity regulatory approach, bringing core clearing parts into the regulatory framework.

Law is an access restriction for the weak; compliance is the price of上岸 (coming ashore) for the strong.

Public Chains Need Strong Operations

"Rewind the clock of history, retro becomes the main theme."

The listing effect on CEXs and the刷量效果 (brushing volume effect) on DEXs are both declining. Hyperliquid's liquidity is not a problem. HYPE has crossed the斩杀线 (slaughter line) and will not become the second FTT.

This is not the whole story. HYPE至今和HyperEVM生态对不齐 (HYPE still doesn't align with the HyperEVM ecosystem), unable to create a 'false prosperity' similar to BNB's ecosystem, rather than a DeFi system like Ethereum's mainnet. This phenomenon was detailed in对不齐: Ethereum Bleeding, Hyperliquid Losing Speed, and won't be repeated here.

This article focuses on the causes of the phenomenon and where the way out lies.

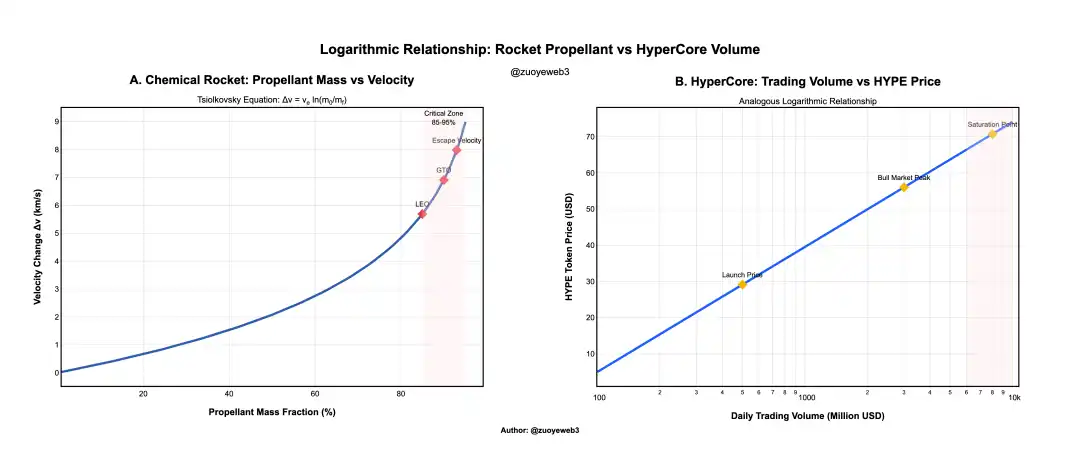

The relationship between rocket fuel and thrust is logarithmic. The relationship between HyperCore trading volume and HYPE price is also logarithmic.

Limited to the chemical rocket architecture, this means the fuel mass needs to increase exponentially to achieve linear speed improvement. Right now, HyperCore trading fees support HYPE's price. But HyperCore's trading volume cannot increase indefinitely, especially with Binance and other Perp DEXs diverting flow全力 (with full force).

Image description: Token price and trading volume. Image source: @zuoyeweb3

Note: The above is only for illustrative purposes of motion change. HYPE's initial price was in the single digits, but真正稳定在 (stabilizing at) $30 is the "initial fair valuation" in the public eye. The trading volume has also been modified to illustrate the relationship between token price and HyperCore trading volume.

Note, this does not conflict with the fact that Perp DEXs cannot卷死 (overwhelm) Hyperliquid. The only assets in the crypto circle are BTC/ETH. The overall Perp market size has already reached a阶段性触顶 (stage peak).

Let's deconstruct where the Hyperliquid team's "Buddhist系" (laid-back attitude) comes from. Maybe this reason isn't complicated, but it's cruel enough. The Hyper team still uses BTC as the public chain standard and still uses FTX as a reference for derivative exchanges. Learn from the good, avoid the bad.

The auction Ticker for USDH is very telling. Hyperliquid official nodes do not participate in voting, nor do they designate any teams, nor will they provide official liquidity support. The现状 (current situation) is that USDH lacks sufficient development potential and has no significant advantage compared to USDC and USDe.

The Hyperliquid team's "无为而治" (governing by non-interference) is the biggest problem with HyperEVM currently. This is not to say that Hyperliquid lacks operational willingness or capability. Everyone might remember that Hyperliquid first gained attention because of Meme. Subsequently, the launched Unit also had the de facto status of an "official" cross-chain bridge. USDC has long used Arbitrum to connect directly to HyperCore.

But all this is limited to HyperCore. Perhaps in the view of the Hyperliquid team, HyperCore is the product, and HyperEVM is the ecosystem. The product requires strong operations; the ecosystem needs to be open enough.

Unfortunately, times have changed. Today's public chains are more like Super Apps, and similar to internet giants, there haven't been new全民单品 (nationwide hit products) for years. TON/Monad/Berachain/Sonic are all like this. Even Plasma doesn't seem like a stablecoin chain, but more like a Vault incarnate.

The excessive maturity of on-chain infrastructure means public chains/L2s no longer have direct network effects. They either fight for存量 (existing shares) like ETH L1/Solana, or introduce RWA like Canton to offer SaaS-like services, or artificially maintain like BNB Chain.

However, Jeff wants to竭力避免 (avoid at all costs) the disaster caused by FTX's strong operations, thus adopting a conservative strategy for the HyperEVM ecosystem. This leads to projects relying solely on community autonomy, unable to build interaction with HYPE, and只能速生速死 (only having a short life cycle) after distributing HYPE.

Even the operational actions of HyperCore follow the principle of minimal intervention. You can follow the accounts of Hyperliquid, Jeff, and Hyper Foundation; they basically have no interaction with projects.

This situation was suitable for the 2017 or 2020 DeFi Summer era. The on-chain space lacked corresponding products for certain niches. Creating one meant traffic and profits, even excessive imagination about the token. These conditions have now disappeared.

Moreover, Hyperliquid doesn't need to drastically change its style. It just needs to learn from BNB's playbook to build its own unique growth flywheel.

The way out for HYPE is to imitate BNB.

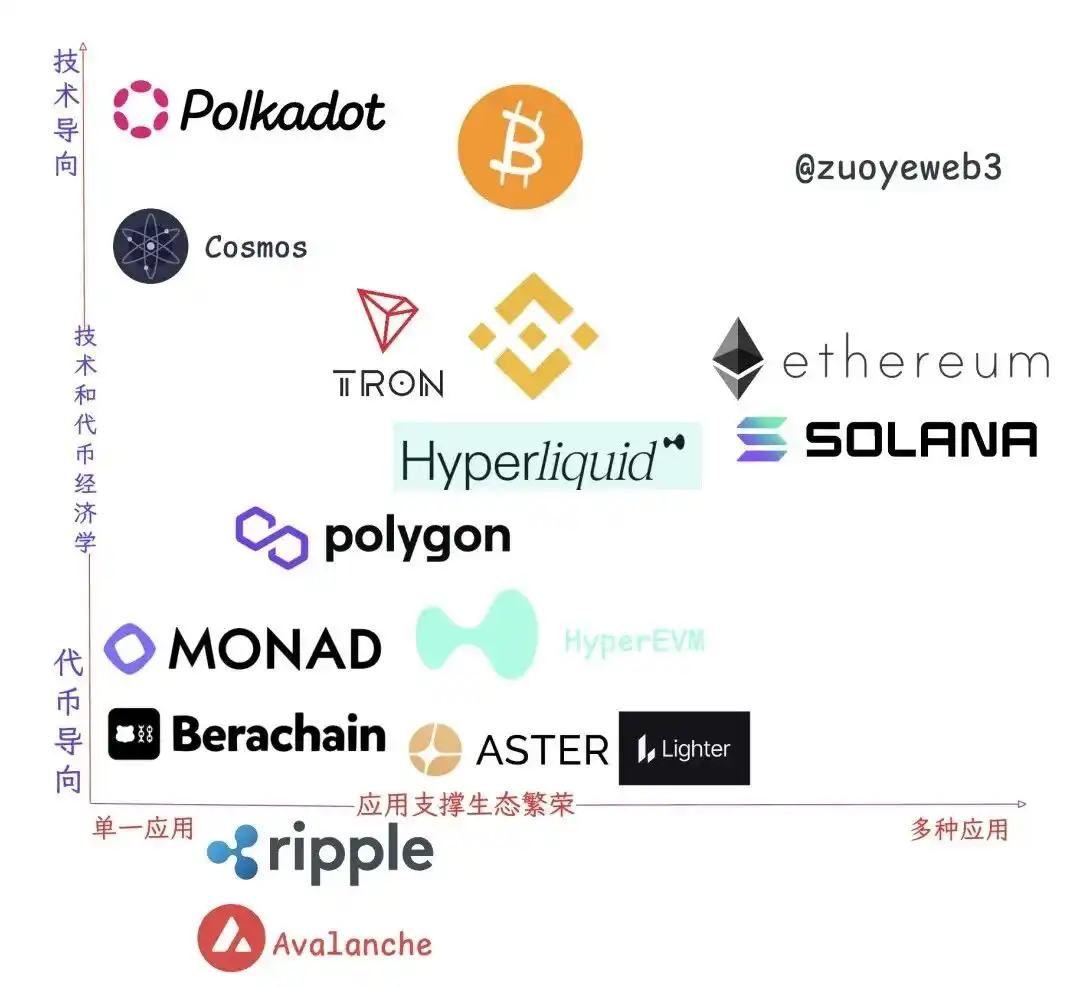

Image description: Ecosystem and application relationship. Image source: @zuoyeweb3

Observing the public chains/L2s that can survive today, it's not simply an interaction between ecological prosperity and strong mainnet token value capture. Reality is far more complex than theory. The only one that fits the既定印象 (established impression) is ETH itself. The rest basically cannot be simply categorized.

In other words, ideals are ideals precisely because they don't manifest in reality.

-

Single Application Group: TRON and Polygon survive on a single application, the former with USDT, the latter with Polymarket;

-

Tech-Oriented Group (Tears of the Era Group): Polkadot and ATOM, advanced in technology and理念 (concept), but tokens cannot capture economic value;

-

Pure Token-Oriented: Monad/Berachain, no need to elaborate, their historical mission is complete after token issuance.

-

Ecologically Prosperous Group: Solana and Ethereum

-

Existentialist Group: Ripple, Avalanche, existence is everything, everything is existence.

Further细分 (subdivision) is possible. Binance Main站 and HyperCore belong to the "bucket group." Their tokens have extremely strong value capture capabilities. Their products are multi-empowering: spot/perp trading, wealth management, staking, even transfers. They are not public chains but resemble them.

The value of BNB Chain is as a component of Binance Main站 in the form of a "public chain." Dragon Mama left, Rong Mama came. The reason Binance never gives up on BNB Chain is also here. Many things are more convenient to do on a public chain than on an exchange. The value of traffic is long-term value.

However, Hyperliquid's HIP-3 is also an overflow of HyperCore's liquidity, essentially competing with HyperEVM for traffic入口 (entry points). This internal traffic fight now happens not only among HIP-3 projects but also between Builder Code and HyperEVM projects.

Hyperliquid wants to become the AWS of liquidity, but the internal organizational structure hasn't been sorted out.

BNB Chain is not the perfect form Binance wanted, but it's sufficient for Hyperliquid to learn from.

BNB Chain is a distribution channel for Binance Main站. It cannot achieve self-hematopoiesis without strong operations, let alone feed back to Binance itself. But this is already sufficient for HyperEVM at its current stage.

Between not harming the principle of minimal operations and maintaining HyperEVM's openness, there is room to push forward. "Appointing" leaders in various tracks like lending, SWAP, and LST. The aborted HIP-5 proposal was too crude. Using回购的HYPE (repurchased HYPE) to iteratively repurchase project tokens is also not feasible.

Ecological collaboration does not violate any principles. The Hyperliquid team almost has no "dealings" with any projects. Perhaps they prefer off-chain cooperation similar to the MM alliance. But on-chain exposure is still needed.

If even the minimum level of HyperEVM operation is not done, we will likely see a $50 HYPE. Lacking the imaginative power of HyperEVM's network effects, HYPE will lose the支撑 (support) for exponential growth imagination.

Without the assistance of HyperEVM, HyperCore would need to reach OKX's level of liquidity solely on its own, but even that would not be able to build the HYPE flywheel.

In a nutshell, for the on-chain ecosystem, the "decentralized" HyperEVM has no retreat.

Conclusion

"Hyperliquid is lighter than Binance with higher capital efficiency. Lighter is not lighter than Hyperliquid. Aster is eager to become complex."

Perp DEXs that are having or approaching TGE, like Aster and Edge, will build their own L2/public chains. This is part of the plan to increase valuation, just like PumpChain is part of the token issuance plan.

Now is the critical time for Hyperliquid to become complex, using its scale advantage to换取 (exchange for) the future.

As mentioned before, Hyperliquid is not good at innovating某类产品 (certain types of products) (Jeff also worked on prediction markets). Its strength lies in the engineering ability to combine elements. If FTX is not a good learning object, then BNB Chain is a good one to imitate now.