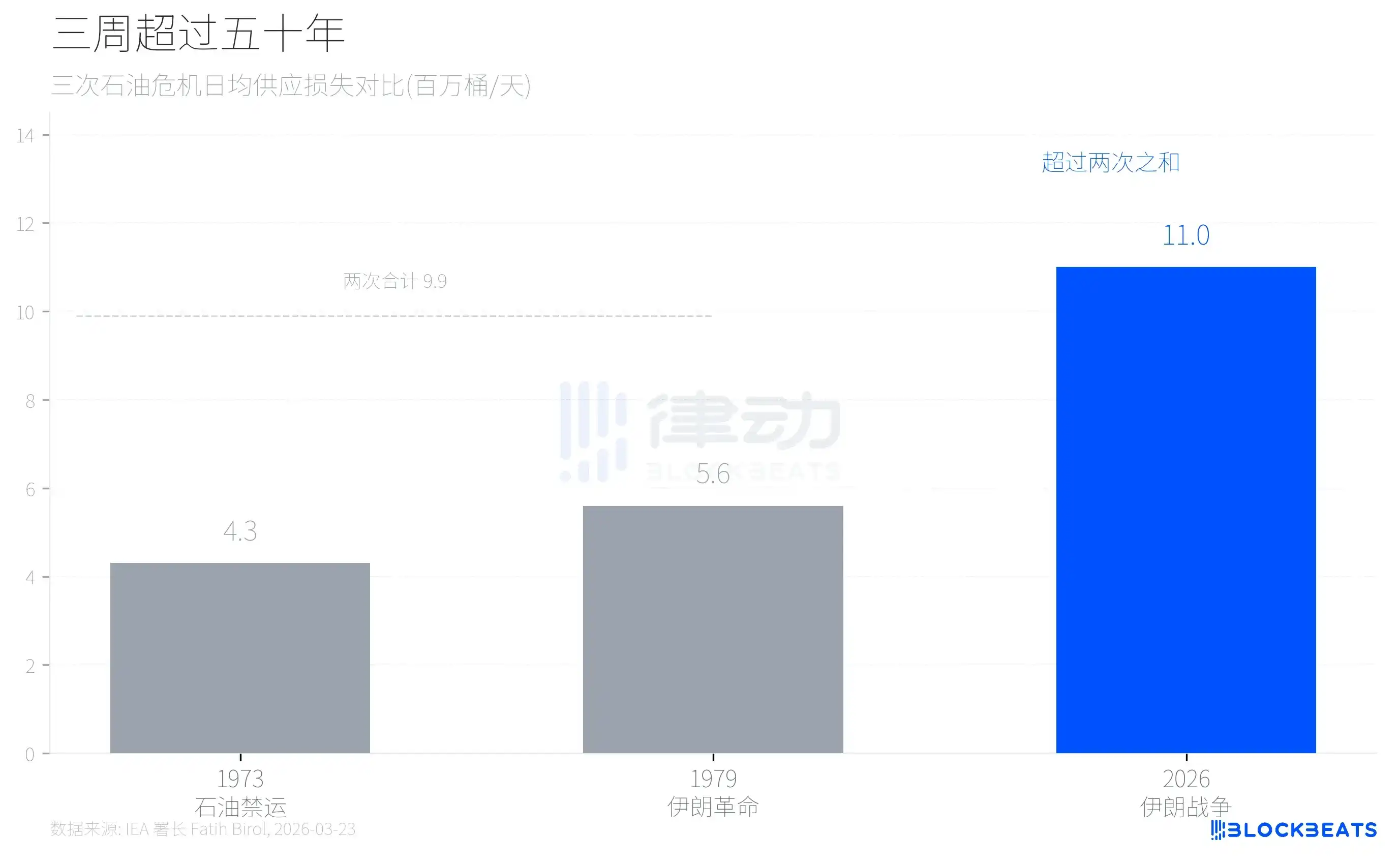

On February 28, the United States and Israel launched a military strike against Iran. Iran immediately blockaded the Strait of Hormuz, cutting off the global daily transit of 20 million barrels of oil. Three weeks later, on March 23, IEA Director Fatih Birol provided a figure at the National Press Club of Australia: the global daily oil supply loss caused by this war is 11 million barrels.

This figure exceeds the combined losses of the 1973 oil embargo and the 1979 Iranian Revolution crises.

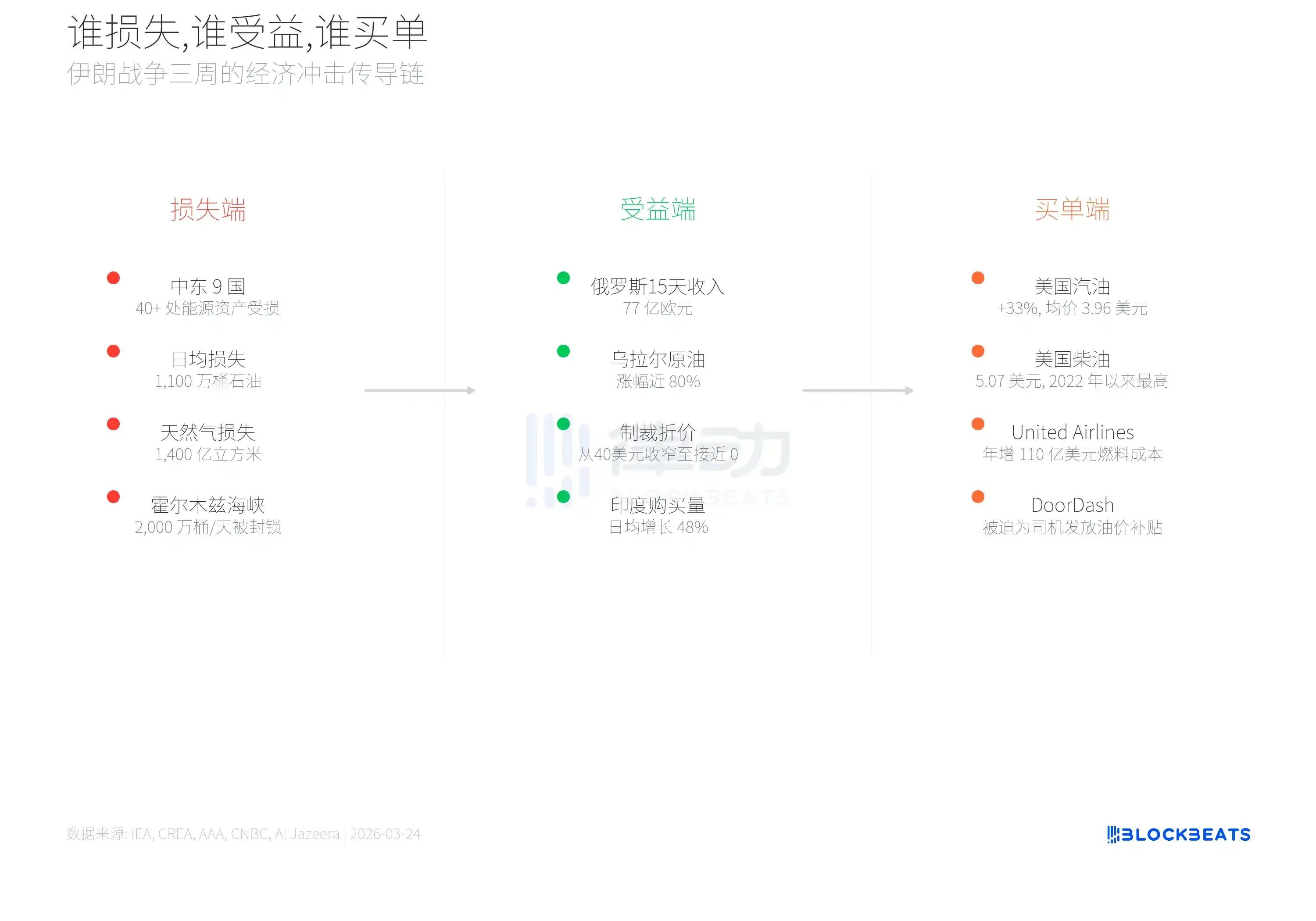

Energy infrastructure at over 40 sites across 9 Middle Eastern countries suffered varying degrees of damage. Concurrent IEA data shows that the global natural gas supply loss reached 140 billion cubic meters, nearly double the European gas loss during the Russia-Ukraine conflict (75 billion cubic meters). In just three weeks, the quantitative shock this conflict inflicted on the energy market has surpassed that of the entire 1970s.

But the supply loss is only half the story. The other half is that there are clear beneficiaries of this crisis.

Putin's Windfall

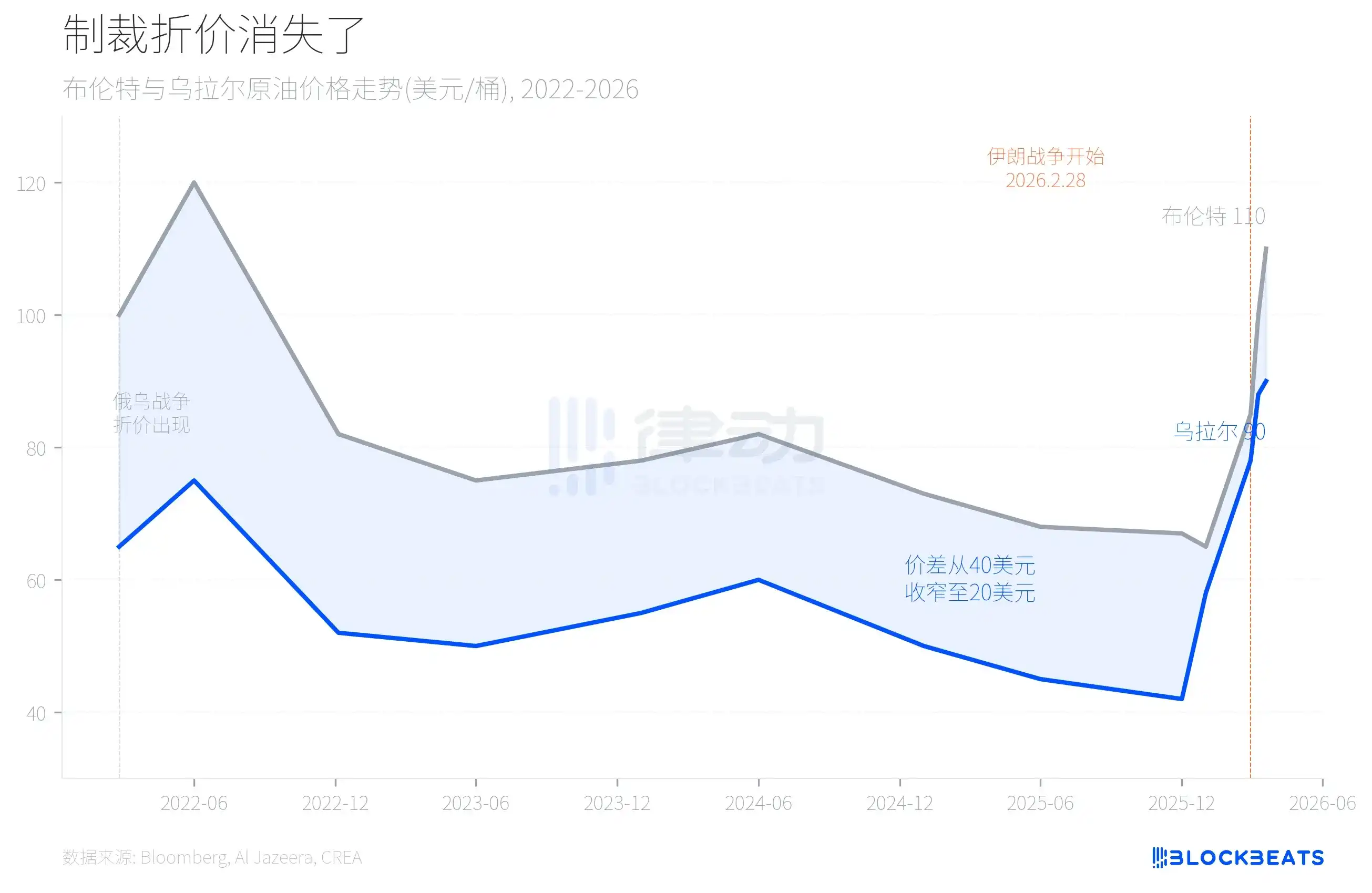

Before the Iran war began, Urals crude was trading at less than $60 per barrel. This price had been locked in for nearly three years, a direct result of Western sanctions. After the Russia-Ukraine war broke out, Europe and the US imposed a price cap on Russian oil, maintaining a long-term discount of $30 to $40 between Urals crude and the international benchmark Brent. This discount was the most直观 signal of the sanctions working.

The Iran war changed all that. Following the blockade of the Strait of Hormuz, a huge gap appeared in the global oil market, forcing buyers to seek alternative supplies. According to data from the Centre for Research on Energy and Clean Air (CREA), Russia's total fossil fuel export revenue reached 7.7 billion euros in the first two weeks of March, averaging 513 million euros per day, an 8.7% increase from February's 472 million euros per day. Daily oil export revenue averaged 372 million euros, earning an extra 672 million euros (approximately $777 million) over those two weeks.

Urals crude rose from under $60 to around $90 within three weeks, a surge of nearly 80%. As reported by Al Jazeera, energy analyst George Voloshin pointed out that Brent also rose from around $65 to over $110 during the same period, but the key is not the absolute price, but the spread between them. The discount of Urals to Brent narrowed significantly from the pre-war level of about $40. The Moscow Times reported on March 16 that Urals crude delivered to India briefly traded at a premium to Brent, something that had not happened since the sanctions took effect.

In other words, a significant part of the economic wall built by three years of Western sanctions was dismantled by three weeks of war in Iran.

The Trump administration announced a 30-day sanctions waiver on March 12, allowing countries to purchase Russian oil en route, with Treasury Secretary Scott Bessent stating it would release about 140 million barrels of supply. However, analysts widely believe the waiver's condition of "not generating significant financial benefit" is nearly impossible to enforce. Concurrently, the IEA announced the release of 400 million barrels from strategic petroleum reserves, the largest such release in history. This waiver is set to expire on April 11, at which point the market will face a new round of uncertainty.

India is the most direct actor. CREA data shows that India's purchases of Russian fossil fuels totaled 1.3 billion euros in the first two weeks of March, averaging 89 million euros per day, a 48% increase from February's daily average of 60 million euros. Al Jazeera confirmed that at least 7 tankers originally bound for China changed course to India mid-voyage, with one ship named Aqua Titan arriving at an Indian port on March 21. While the world worries about oil prices, oil trade between Moscow and New Delhi is accelerating.

Who is Paying?

Losses on the supply side and gains on the beneficiary side ultimately get passed on to the consumer. American consumers are bearing the most direct burden.

AAA data shows the US national average price for gasoline rose from $2.98 before the war to $3.96 on March 23, a 33% increase. The average price in California reached $5.56, while the lowest, in Kansas, was $3.23. The average diesel price hit $5.07, the highest since 2022.

Fortune reported that this round of oil price increases has effectively swallowed up the tax refunds American families just received.

The aviation industry was among the first to feel the impact. Platts assessment data shows US jet fuel prices rose over 60% in three weeks, doubling in some regions. United Airlines became the first major US carrier to officially announce capacity cuts. CEO Scott Kirby stated in an internal memo that the company is preparing for oil prices to probe $175 per barrel, which would mean an annual fuel cost increase of about $11 billion, more than double the company's "best annual profit in history." United will cut 5% of its flights in the second and third quarters.

The effects are spreading globally. According to a CNBC report on March 21, Delta Air Lines also warned it might reduce capacity. Euronews reports show that Qantas, SAS, and Thai Airways have already raised prices, and Air New Zealand has canceled over 1,000 flights.

Even the gig economy is affected. According to a Philadelphia Inquirer report on March 23, DoorDash began issuing weekly gas subsidies of $5 to $15 and 10% cash back on gas to drivers, in response to reduced order acceptance due to rising fuel costs. When a food delivery platform has to pay for a war in the Middle East, the length of the shock transmission chain needs no further explanation.

Three weeks into the Iran war, the world loses 11 million barrels of oil daily, Russia made nearly $800 million extra in 15 days, American consumers are paying a third more for gas, and this transmission chain will continue to lengthen after the sanctions waiver expires on April 11.