Author: imToken

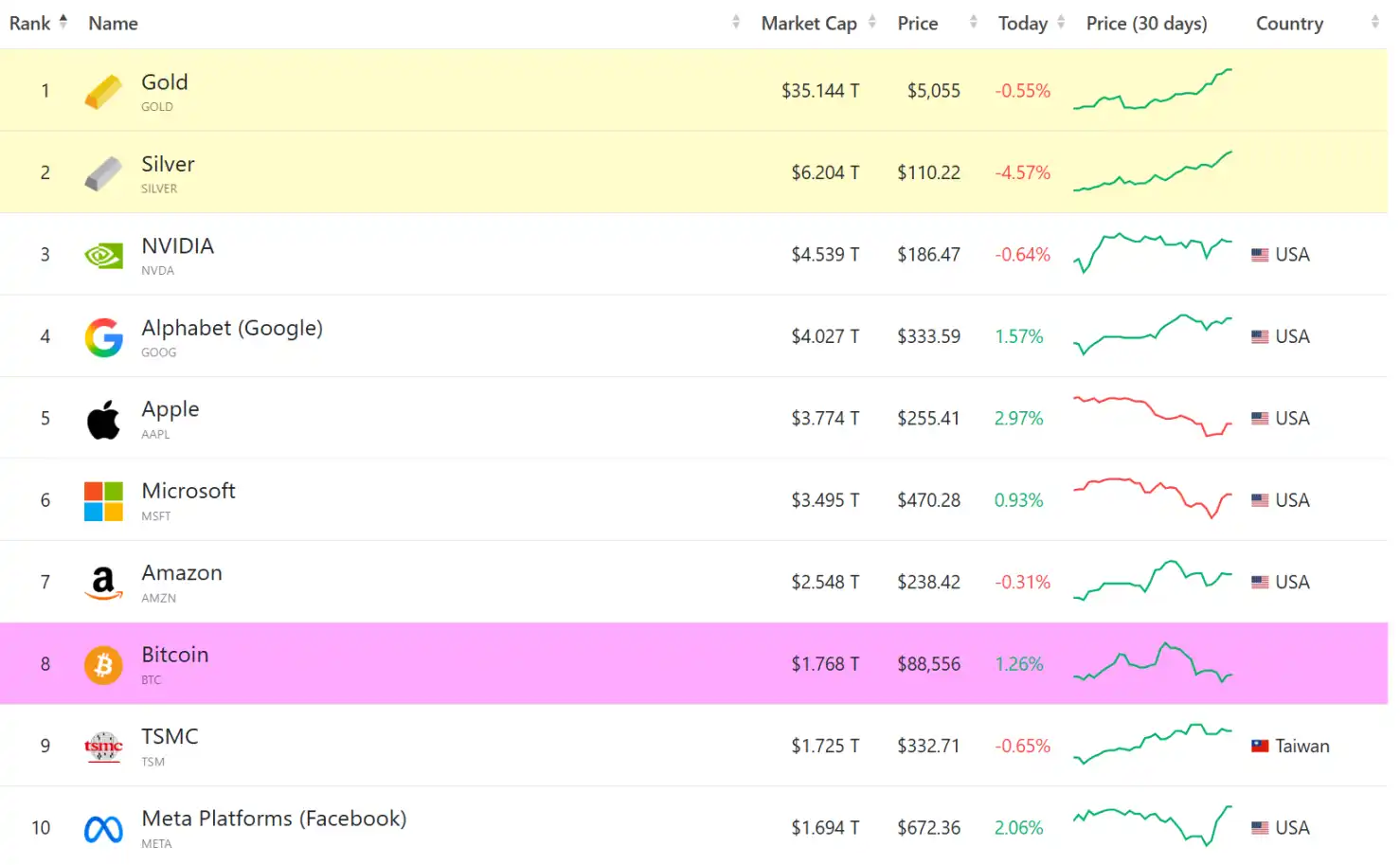

If a year ago, someone told you that gold would quickly rise to $5,000 per ounce, most people's first reaction would probably be that it was wishful thinking.

But that's exactly what happened. In just half a month, the gold market has been like a runaway horse, continuously breaking through multiple historical barriers of $4,700, $4,800, and $4,900 per ounce, and heading toward the collective market gaze of the $5,000 moment with almost no looking back.

Source: companiesmarketcap.com

It can be said that after global macro uncertainties have been repeatedly verified, gold has returned to its most familiar position—as a consensus asset that does not rely on any single sovereign promise.

But at the same time, a more practical question is emerging: As the gold consensus returns, are traditional holding methods no longer able to meet the needs of the digital age?

I. The Inevitability of the Macro Cycle: The 'Old King' Returns to the Throne

From a longer macro cycle perspective, this round of gold's upward cycle is not short-term speculation but a structural return against the backdrop of macro uncertainty and a weakening U.S. dollar:

Geopolitical risks have extended from Russia-Ukraine to key resource and shipping regions such as the Middle East and Latin America; the global trade system has been repeatedly interrupted by tariffs, sanctions, and policy games; the U.S. fiscal deficit continues to expand, and the long-term stability of the U.S. dollar's credit is being discussed more frequently. In such an environment, the market will undoubtedly accelerate its search for a value anchor that does not rely on any single country's credit and does not require others' endorsement.

From this perspective, gold does not need to prove that it can generate returns; it only needs to repeatedly prove one thing: in an era of credit uncertainty, it still exists.

This also partly explains why, in this cycle, BTC, which was once expected to be 'digital gold,' has not fully assumed the same consensus role—at least in the dimension of macro hedging, the choices of funds have already provided the answer, which will not be elaborated here (extended reading: 'From Trustless BTC to Tokenized Gold: Who Is the Real 'Digital Gold'?').

However, the return of the gold consensus does not mean that all problems have been solved. After all, for a long time, investors have almost had to choose between two imperfect holding methods.

The first is physical gold, which is secure and sovereign but almost illiquid. Locking gold bars in a safe means high storage, anti-theft, and transfer costs, and it also means that it can hardly participate in real-time trading or daily use.

The recent phenomenon of 'one safe-deposit box is hard to find' in many banks恰恰 illustrates that this contradiction is being amplified, meaning that more and more people want to hold gold in their own hands, but现实条件并不总是配合.

The second is paper gold or gold ETFs, which to some extent make up for the physical holding threshold of physical gold, such as paper gold products issued by bank accounts or brokerage systems. These are essentially a claim on financial institutions, giving you a settlement promise backed by the account system.

But the problem is that this liquidity itself is not complete—the liquidity provided by paper gold and gold ETFs is only locked within a single financial system. It can be bought and sold within a certain bank, a certain exchange, or a certain set of clearing rules, but it cannot freely flow outside this system.

This means it cannot be split, combined, or collaborate with other assets across systems, let alone be directly used in different scenarios. It is only 'in-account liquidity,' not true asset liquidity.

For example, the first gold investment product I owned, 'Tencent Micro Gold,' was like this. From this perspective, paper gold does not truly solve the liquidity problem of gold but only temporarily replaces the physical inconvenience with counterparty credit.

In the end, security, liquidity, and sovereignty have long been in a state where it is difficult to have all three. And in a highly digitalized and cross-border era, such trade-offs are becoming increasingly unsatisfactory.

It is against this background that tokenized gold has begun to enter the视野 of more people.

II. Tokenized Gold: Returning 'Complete Liquidity' to the Asset Itself

Tokenized gold, represented by XAUt (Tether Gold) issued by Tether, attempts to solve not just the surface-level problem of 'making gold easier to hold/trade,' which paper gold can also achieve, but a more fundamental proposition:

How can gold achieve the same complete liquidity and composability as crypto assets that can flow across systems, without sacrificing the 'physical gold endorsement' of gold?

If we take XAUt as an example and拆解 its design logic, we will find that it is not radical but even quite traditional and restrained: each XAUt corresponds to 1 ounce of physical gold in a London vault, and the physical gold is stored in a professional vault, auditable and verifiable. At the same time, tokenized gold holders have the right to claim the underlying gold.

This design does not introduce complex financial engineering, nor does it attempt to amplify gold's attributes through algorithms or credit expansion. On the contrary, it deliberately maintains respect for the traditional gold logic—first ensuring that the physical gold attribute is established, and then discussing the changes brought by digitization.

In the final analysis, tokenized gold like XAUt and PAXG is not 'creating a new gold narrative' but is using blockchain to repackage the oldest asset form. In this sense, XAUt is more like a 'digital physical gold' than a speculative derivative in the crypto world.

But at the same time, the more important change is that the liquidity level of gold has fundamentally shifted. As mentioned above, in the traditional system, whether it is paper gold or gold ETFs, the so-called liquidity is essentially in-account liquidity—it exists within a certain bank, a certain brokerage, or a certain clearing system and can only be bought, sold, and settled within established boundaries.

The liquidity of XAUt is directly attached to the asset itself. Once gold is mapped as an on-chain token, it naturally possesses the basic attributes of crypto assets and can be freely transferred, split, combined, and circulated among different protocols and applications without needing permission from any centralized institution.

This means that for the first time, gold no longer relies on an 'account' to prove its liquidity but circulates freely globally 24/7 in the form of the asset itself (extended reading: 'The 'Gold Godfather' Debates CZ: Who Is the Real 'Digital Gold'? A Trust Battle Across TradFi and Crypto'). In the on-chain environment, XAUt and others are no longer just 'tradable gold tokens' but basic asset units that can be recognized, called, and combined by other protocols:

- It can be freely exchanged with stablecoins and other assets;

- It can be incorporated into more complex asset allocation and组合 strategies;

- It can even be used as a value carrier to participate in consumption and payment scenarios;

This is precisely the part of 'liquidity' that paper gold has never been able to provide.

III. From 'On-Chain' to 'Usable': The True Watershed for Digital Physical Gold

For this reason, if tokenized gold only completes the step of 'going on-chain,' it is far from reaching the finish line.

The real watershed lies in whether this 'digital physical gold' can truly be easily held, managed, traded, and even used as 'currency' for consumption and payment? That is, returning to the point mentioned above, if tokenized gold remains just a string of code on the chain and is ultimately encapsulated in a centralized platform or a single entry point, then it is no different from paper gold.

Against this background, the significance of lightweight self-custody solutions like imToken Web begins to emerge. Taking imToken Web's exploration as an example, it allows users to access through a browser—like opening a webpage, instantly managing their tokenized gold and other crypto assets on any device.

Moreover, in a self-custody environment, the private key is完全 controlled by the user. Your gold does not exist on any service provider's server but is truly anchored in a blockchain address.

Additionally, thanks to the interoperability of Web3 infrastructure, XAUt is no longer a heavy metal sleeping in a safe. It can be purchased flexibly in small amounts, and when needed, its purchasing power can be released in real-time into global consumption scenarios through支付 tools like imToken Card.

Source: imToken Web

In short, in the Web3 environment, XAUt can not only be traded but also combined with other assets, exchanged, and even connected to payment and consumption scenarios.

And when gold simultaneously possesses extremely high storage certainty and modern usage potential for the first time, it truly completes the leap from an 'old-school避险品' to a 'future currency.'

After all, gold, as a consensus that can span millennia, is not inherently陈旧; what is陈旧 is only the way it is held.

So when gold enters the chain in the form of XAUt and returns to personal control through self-custody environments like imToken Web, what it continues is not a new narrative but a logic that spans eras:

In an uncertain world, true value is to rely as little as possible on the promises of others.