Entering 2026, the U.S. stock market exhibits an extreme divergence: the Nasdaq has failed to hit a new high for four consecutive months, with the valuations of AI leaders suffering in the anxious stalemate awaiting a new round of rate cuts; yet, on the other end of the market, industrial, energy, and utility stocks are breaking through first amidst the roar of the "old world."

This divergence sends a clear signal: the competition in AI has decisively shifted from an algorithm race to a physical resource race. If 2024 was the "Year of the Chip," then 2026 is the "Year One of Grid Modernization."

Currently, the revaluation of power assets is unstoppable. The market was buying the "brain" (chips) in 2023-2024, while in 2025-2026, capital is flowing to the "heart and blood vessels" (power and grid).

This article will provide a complete recap for investors on the structural changes, competitive landscape, and the opportunities within the U.S. power and grid industry.

The RockFlow investment research team believes investors should focus on three tiers: the high-margin software and automation layer represented by GEV, the high-certainty equipment manufacturing layer centered on Eaton and Schneider, and the direct harvesters of the infrastructure boom led by PWR.

1. AI Demand Shock and the U.S. Grid's "Ailments of Age"

For the past few decades, Americans had almost forgotten what "power shortage" meant. In the early 2000s, thanks to the widespread adoption of LED lighting and the mandatory enforcement of the EPA's "Energy Star" certification, energy consumption in the U.S. miraculously plateaued despite population growth.

But this stagnation was completely shattered in 2025. With the exponential growth of large-scale data centers and AI applications, the energy demand curve experienced a near-vertical inflection point:

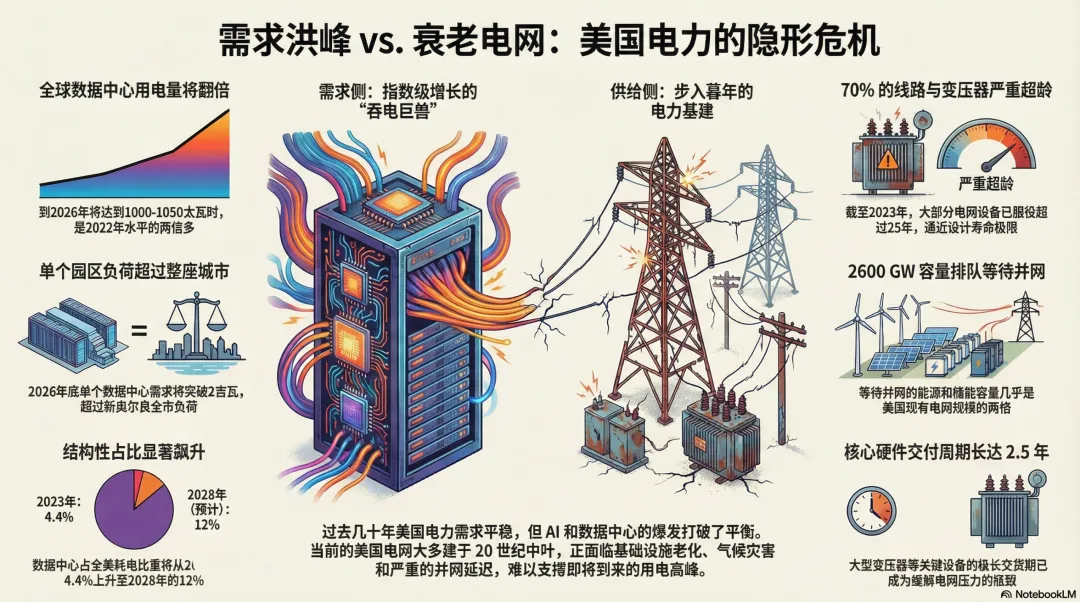

- Doubled Consumption: Global data center consumption is expected to reach 1000-1050 Terawatt-hours (TWh) by 2026, more than double the 2022 level.

- The Magnitude of a City: By the end of 2026, the power demand of a single, independent data center campus will exceed 2 Gigawatts (GW). This is equivalent to the power load of a medium-sized city.

- Structural Share: In 2023, data centers accounted for only 4.4% of U.S. electricity consumption; by 2028, this figure is projected to soar to 12%.

Beyond AI, this "power-guzzling behemoth," the reshoring of manufacturing and overall societal electrification (EVs, heat pumps, etc.) are also simultaneously increasing the load. The power industry is transitioning from a "zero-growth" boring sector into a new period of rapid expansion.

In stark contrast to this are the "ailments of age" plaguing the U.S. grid.

The current U.S. grid was not designed to support the AI era. It more closely resembles a "Frankenstein's monster" patched together with mid-20th-century technology.

The grid consists mainly of three parts: generation, transmission, and distribution. The current problems lie in:

- Aging Infrastructure: As of 2023, 70% of U.S. power lines and transformers are over 25 years old. Most of the grid was built in the 1960s and 70s, approaching the 50 to 80-year design life limit.

- Climate Change's "Final Straw": The first half of 2025 alone saw dozens of weather disasters costing billions of dollars each. Grid failures caused by extreme heat (sagging lines) and hurricanes are becoming the norm for regional blackouts.

On the other hand, we see a desperate "queueing crisis." Nearly 2600 GW of energy and storage capacity (almost twice the size of the current U.S. grid) is currently queued up waiting for grid connection.

Reportedly, lead times for large transformers have stretched to 2.5 years. Just for the 2026/27 delivery year, customers of PJM Interconnection will pay an additional $3.5 billion in capacity costs due to interconnection bottlenecks.

2. Redefining the Smart Grid

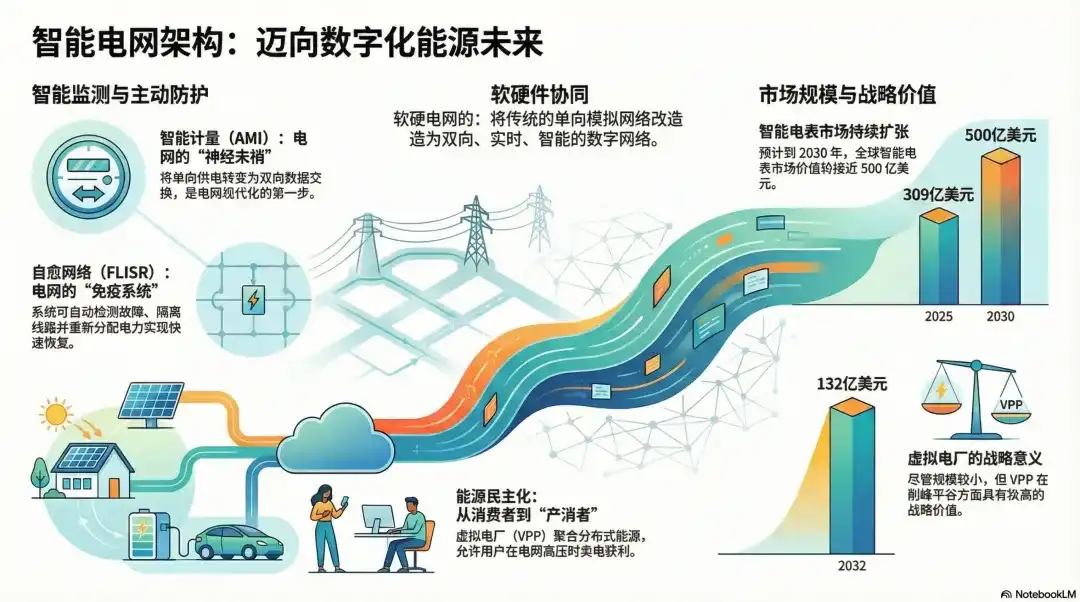

So-called grid modernization is not simply about stringing up more power lines; it's about transforming the traditional one-way analog network into a two-way, real-time, intelligent digital network.

Nerve Endings: Advanced Metering Infrastructure (AMI)

AMI is the first step in modernization. It turns one-way power supply into two-way data exchange. Its core lies in smart meters transmitting data back to the system via radio frequency or cellular networks.

Statistics show the global smart meter market was worth approximately $30.9 billion in 2025 and is expected to approach $50 billion by 2030.

Immune System: Automation and Self-Healing Networks (FLISR)

This is the infrastructure's shift from passive to active. Using software developed by companies like GE Vernova, upgraded power systems can:

1. Automatically Detect: Precisely locate the position of a fallen tree or exploding transformer.

2. Automatically Isolate: Instantly cut off the faulty line.

3. Automatically Restore: Redirect power from adjacent feeders to unaffected areas, achieving "self-healing."

Energy Democratization: Virtual Power Plants (VPP)

VPPs use cloud software to aggregate home solar systems and electric vehicle batteries. Consumers are no longer just buying electricity; they become "prosumers," selling power back to the grid for profit during times of high stress.

Although the niche market size is only in the hundreds of billions of dollars, its strategic importance for peak shaving and load balancing is immense.

3. Who is Sharing This Massive Pie?

Based on the current industry attributes and profit structure of the U.S. power grid, the RockFlow investment research team categorizes the beneficiary companies into four tiers:

Software & Automation: The Intelligent "Brain"

This is the segment with the highest profit margins and the deepest moats.

- GE Vernova (GEV): Coordinates the entire energy lifecycle through its GridOS platform. As a pure-play entity after the GE spin-off, it is the absolute leader in grid digitization.

- Siemens (SIEGY): Possesses the leading Spectrum Power system. Its latest Gridscale X platform is defining the digital standards for the distribution side.

- Itron (ITRI): The king of smart metering. Its "edge intelligence" products can detect outages in real-time without central processing, acting as the "guardian" at the distribution grid's endpoint.

Equipment Manufacturing & Power Electronics: The Critical Foundation

- Eaton (ETN): A giant in electrical distribution equipment. From circuit breakers to transformers, Eaton's product portfolio covers almost every physical node of grid modernization.

- ABB: A global expert in high-voltage products and automation. Its record order backlog is primarily driven by grid modernization projects.

- Schneider Electric (SBGSY): Focuses on smart grid technology and microgrid solutions, providing end-to-end energy management solutions to help data centers maximize energy efficiency. It deeply integrates hardware with digital management through its EcoStruxure platform, holding a dominant position, especially in data centers and microgrids.

Engineering, Procurement & Construction (EPC): The Builders

- Quanta Services (PWR): The dominant force in North American transmission and distribution contracting. Its recent massive $72 billion agreement with AEP is the best footnote to the grid upgrade trend. (Note: Corrected likely typo from 720 to 72 billion based on common scale)

- MasTec (MTZ): Focuses on renewable energy interconnection. Its $17 billion order backlog foreshadows an earnings explosion over the next two years.

Regulated Utilities: The Established "Managers"

- NextEra Energy (NEE): The largest clean energy company in the U.S., focused on wind and solar power generation. It owns extensive renewable energy assets and secures stable revenue through long-term Power Purchase Agreements (PPAs) with large customers.

- Duke Energy (DUK): Owns extensive grid infrastructure covering multiple data center clusters. By modernizing its transmission and distribution networks, the company can provide efficient, low-loss power transmission services for data centers. Additionally, DUK is investing in clean energy generation to meet data center demand for green power.

Conclusion: The "Revaluation" of Power Assets Has Begun

In 2026, the power network is no longer that forgotten "utility" but a core asset concerning national security and the outcome of the AI race.

The RockFlow investment research team believes that for investors, software-driven automation companies (GEV, ITRI) possess the highest premium capability; equipment manufacturers (ETN, ABB) have the most certain order visibility; and EPC giants (PWR) are the direct harvesters of the infrastructure boom.

In the next five years, Alpha in U.S. stocks will no longer exist solely in code, but also in the hum of every smart transformer.