Author: Deep Tide TechFlow

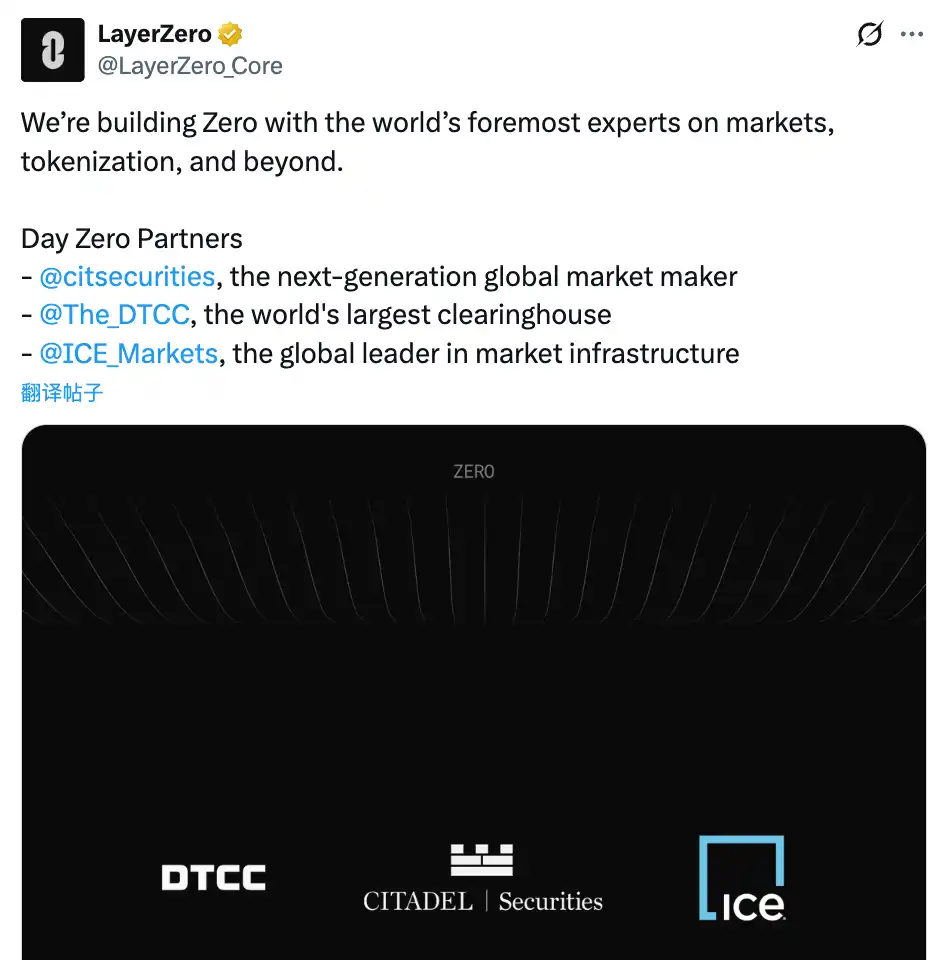

On February 10, LayerZero launched Zero in New York.

This is a self-developed Layer 1 public chain aimed at hosting institutional-grade financial market trading and clearing.

LayerZero calls it a "decentralized multi-core world computer." Let me translate that for you: a chain specifically for Wall Street.

At the same time, various Wall Street institutions began openly endorsing it, with some responses directly involving financial investment.

Among them, Citadel Securities made a strategic investment in the ZRO token.

This company handles approximately one-third of U.S. retail stock orders. CoinDesk specifically noted in its report on the matter that directly purchasing crypto tokens is not a conventional move for traditional Wall Street financial institutions like Citadel.

ARK Invest also purchased equity and tokens in LayerZero, with Cathie Wood (Cathie Wood) directly joining the project's advisory board; Tether announced a strategic investment in LayerZero Labs on the same day, though the amount was not disclosed.

Beyond token purchases and equity investments, there is a quieter signal.

DTCC (the central clearing agency for U.S. stock trading), ICE (the parent company of the New York Stock Exchange), and Google Cloud also signed joint exploration agreements with LayerZero.

So, a cross-chain bridge project, in its transformation, has simultaneously secured collective endorsement from the entire industry chain including clearing, exchanges, market makers, asset management, stablecoins, and cloud computing.

Traditional institutions are adding another move in their layout of on-chain financial pipelines.

After the news was announced, ZRO's price surged over 20% that day, currently hovering around $2.3.

No Longer a Bridge, but a Pipeline?

What LayerZero has done over the past three years is not complicated:

Moving tokens from one chain to another. Its cross-chain protocol currently connects over 165 blockchains. USDt0 (the cross-chain version of Tether's stablecoin) launched less than a year ago and has handled over $70 billion in cross-chain transfers.

This is a mature business, but the ceiling is visible.

Cross-chain bridges are essentially tools—users choose the one that is cheaper and faster. However, as the entire crypto market shrinks and trading volume declines, cross-chain functionality has become a pseudo-demand. It's understandable that LayerZero is choosing to switch tracks.

Moreover, it has the capital to do so. a16z and Sequoia have led funding rounds for the project, with total financing exceeding $300 million and a previous valuation once reaching $3 billion.

The investment portfolios of these two capital firms are essentially Wall Street's contact list. The fact that Citadel and DTCC are now willing to sit at the table to endorse LayerZero might have a lot to do with who is standing behind it.

Returning to the new L1 launched by LayerZero, Zero, it clearly isn't designed for DeFi players or meme traders.

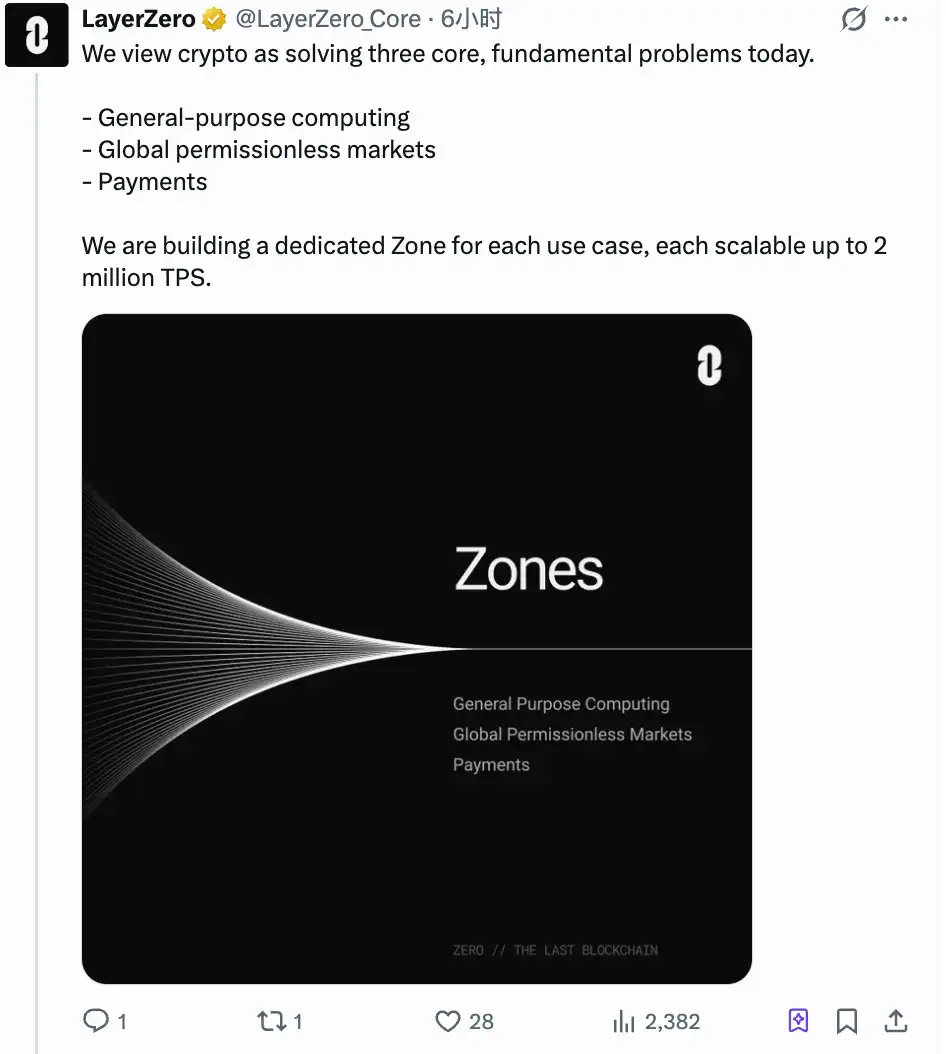

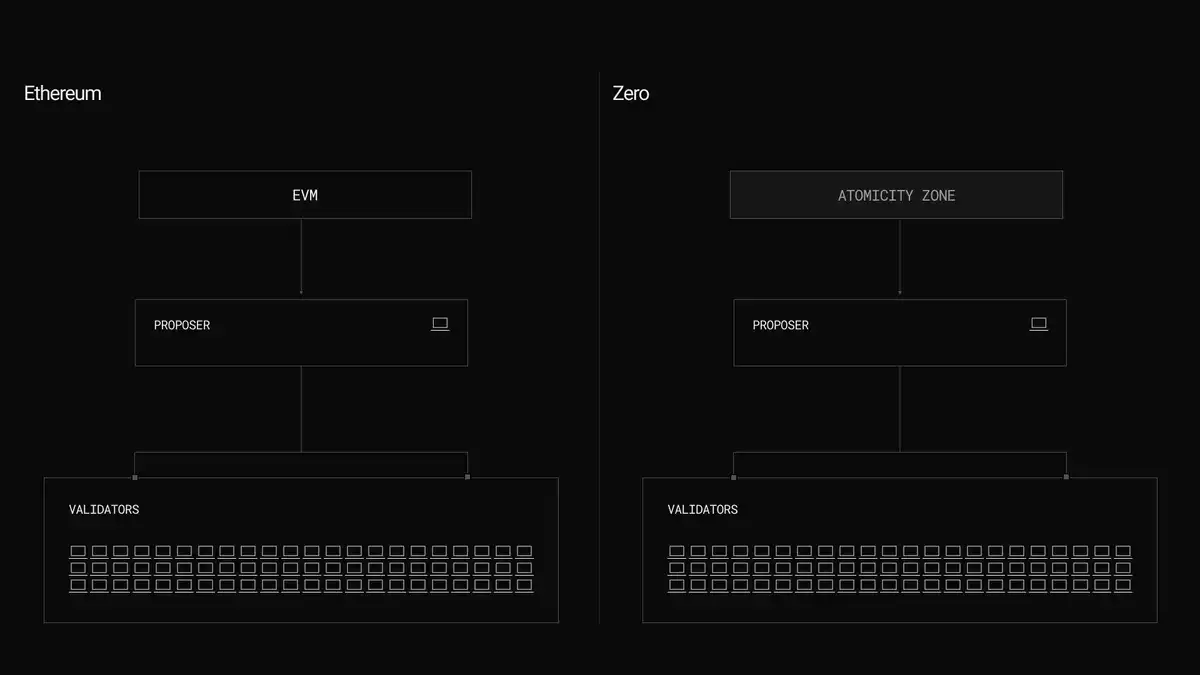

Zero's architecture is different from existing public chains. Most chains are like a single road running all vehicles; Zero splits the chain into multiple independently operating partitions, which LayerZero calls Zones.

Each Zone can be individually optimized for different scenarios without interference.

At launch, three Zones were opened: a general-purpose environment compatible with Ethereum smart contracts, a private payment system, and a dedicated trading matching environment.

These three Zones target three types of customers.

The general EVM environment retains existing crypto developers with low migration costs. The private payment system solves an old problem for institutions: trading on Ethereum allows counterparties to see your positions and strategies, and large funds are unwilling to swim naked.

The trading-specific Zone aims more directly at solving the matching and settlement of tokenized securities.

Looking back at the list of attendees makes it understandable. DTCC clears securities transactions worth millions of billions of dollars and wants to know if clearing can be faster. ICE operates the NYSE, where the stock market is only open on weekdays, and it wants to experiment with 24/7 trading. Citadel handles massive order flows, and every step faster in the post-trade process means money.

So, looking at it together, these are not the needs of the crypto industry; they are Wall Street's own pain points.

LayerZero CEO Bryan Pellegrino was quite blunt in a public interview:

"It's not that the existing things aren't good enough; it's that the scenarios truly requiring 2 million transactions per second belong to the future global economy."

Incidentally, this new Zero chain claims to achieve 2 million TPS in test environments, which could indeed meet traditional finance production-level demands. But the performance narrative of public chains has long been played out; no matter how high the performance, the author feels it's not surprising.

The story can remain the same, but the audience can change once—this time, it's the turn of the old money.

Wall Street Wants to Move Trading On-Chain, but Ethereum Can't Handle It

The background of institutions flocking to LayerZero is not the crypto bull market but Wall Street's own push for tokenization.

BlackRock's BUIDL fund was issued on Ethereum last year, with a scale exceeding $500 million. JPMorgan's Onyx platform runs on Ethereum technology and has already handled trillions in repo transactions.

Wall Street has used Ethereum for proof-of-concept, proving that tokenization is feasible. The next step is to find a place that can handle production loads.

Zero's three Zones are aimed precisely at this gap. EVM compatibility means assets and contracts can migrate from Ethereum.

This might be the real divide between LayerZero and Ethereum.

Ethereum is currently using standards like ERC-8004 to fight for definition rights, issuing on-chain IDs for AI Agents, setting rules for the future on-chain economy...

LayerZero's current move is to ignore definitions and directly build pipelines, telling institutions that their trades can run here.

One is writing the rulebook; the other is laying the pipes. They are betting on different things.

Ethereum is betting on its irreplaceability as a trust layer, backed by TVL scale, security audit ecosystems, and institutional recognition. LayerZero is betting on the replacement demand for the execution layer: Wall Street needs speed, privacy, and throughput, and will use whoever provides it first.

Whether these two paths will eventually cross is unclear now. But the flow of capital has already given a directional signal.

What Does This Mean for $ZRO?

ZRO's previous positioning was simple: the governance token for the LayerZero cross-chain protocol. Total supply is 1 billion tokens, used for voting and staking, nothing more.

After the launch of Zero, the story of this token has changed.

ZRO is the native token of the Zero chain, anchoring network governance and security. If Zero truly becomes institutional-grade financial infrastructure, ZRO's valuation logic will no longer be "how much trading volume does the cross-chain bridge have" but "how many assets are running on this chain."

You all understand the difference between these two valuation anchors—the ceiling differs by several orders of magnitude. But narrative aside, several hard variables will determine ZRO's future trend.

Supply Side: 80% of the tokens are not yet unlocked.

ZRO's current circulating supply is approximately 200 million tokens, just over 20% of the total supply. According to CoinGecko data, on February 20, approximately 25.71 million ZRO will be unlocked, worth about $50 million, accounting for 2.6% of the total supply, allocated to core contributors and strategic partners. The entire unlock cycle continues until 2027.

This unlock on February 20 is the first supply shock after the announcement; whether the market can absorb it is a litmus test for short-term sentiment.

Demand Side: The fee switch hasn't been turned on yet.

Currently, ZRO has no direct value capture mechanism. There was a governance vote last December proposing to charge a fee for each cross-chain message, with the revenue used to buy back and burn ZRO, but it failed due to insufficient voter turnout. The next vote is scheduled for June this year.

If passed, ZRO will have a burning mechanism similar to ETH, reducing circulation with each transaction. If it fails again, the token's "governance right" will remain just voting rights, without cash flow support.

So overall, players interested in ZRO can watch three key dates:

1. June, the second fee switch vote. Passing or not will directly determine whether ZRO has endogenous demand.

2. This autumn, the Zero mainnet launch.

3. ZRO tokens will not be fully unlocked until 2027. Before that, each round of unlocking will bring pressure,叠加 the current crypto bear market. News-driven positive sentiment may not necessarily drive ZRO's price up.

Finally, LayerZero calls Zero a "decentralized multi-core world computer," which is clearly对标 Ethereum's concept of a world computer, attempting to play a more important role in the settlement layer, especially the financial settlement layer, while transitioning and cutting away from the thin narrative of a cross-chain bridge.

However, the official statements from several partners are worth pondering.

Citadel calls its participation an "evaluation of how the architecture can support high-throughput workflows"; DTCC says it is "exploring scalability in tokenization and collateral."

Translation: we think this thing might be useful, but we haven't made a final decision yet.

Wall Street's money is smart—smart enough to place many small bets simultaneously to see which one pays off first. Therefore, when a project receives endorsements from various star institutions, it does not mean a complete强绑定, but rather更像 a short-term positive catalyst.

What LayerZero has obtained might be an entry ticket, or it might just be an interview opportunity.