Author: Chloe, ChainCatcher

Recently, Venezuelan leader Maduro was arrested. Before mainstream media released the news, a Polymarket account created in late December had already exited the market with a 1242% return. This incident prompted U.S. Representative Ritchie Torres to propose the "Public Integrity in Financial Prediction Markets Act of 2026," attempting to introduce traditional financial "insider trading" regulations into the crypto market.

This article will use the Maduro incident as a core case study to delve into the controversial issue of insider trading in prediction markets, re-examining whether we need an absolutely level playing field or a precise truth engine in decentralized prediction platforms.

Polymarket's "Prophet" Moment: Accurately Predicting Maduro's Downfall

In January 2026, Venezuelan leader Maduro was confirmed to have been arrested. While global mainstream media was still verifying sources, the data on the decentralized prediction market Polymarket had already provided the answer.

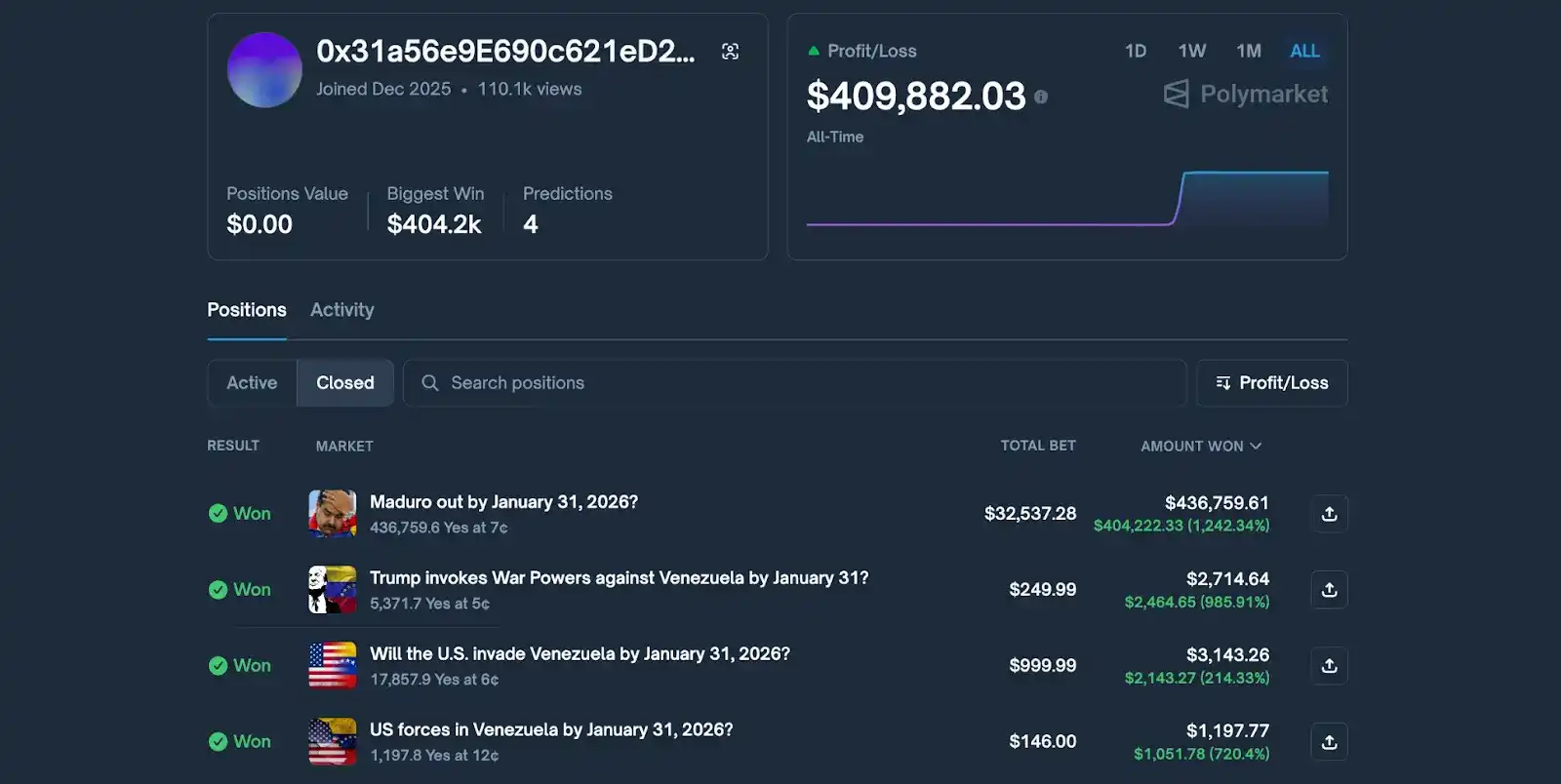

A new account created on Polymarket in late December 2025 seemed to have a god's-eye view, accurately predicting the event. The account made four predictions, all related to whether the U.S. would intervene in Venezuela, with the largest being a bet of $32,537 that "Maduro will step down by January 31." At the time, the market's expected probability for such an extreme event was in the single digits, and the account swept up contracts at the extremely low price of 7 cents.

As news of Trump confirming military action emerged early Saturday morning, these contracts instantly surged to near the $1 settlement price. The account profited over $400,000 in less than 24 hours, with a return rate of 1242%. This was not ordinary speculation but a precise snipe.

Mysterious Prophet or Insider Trading?

This god's-eye view of massive profits quickly became a focal point in the community. As discussions heated up, accusations of insider trading followed:

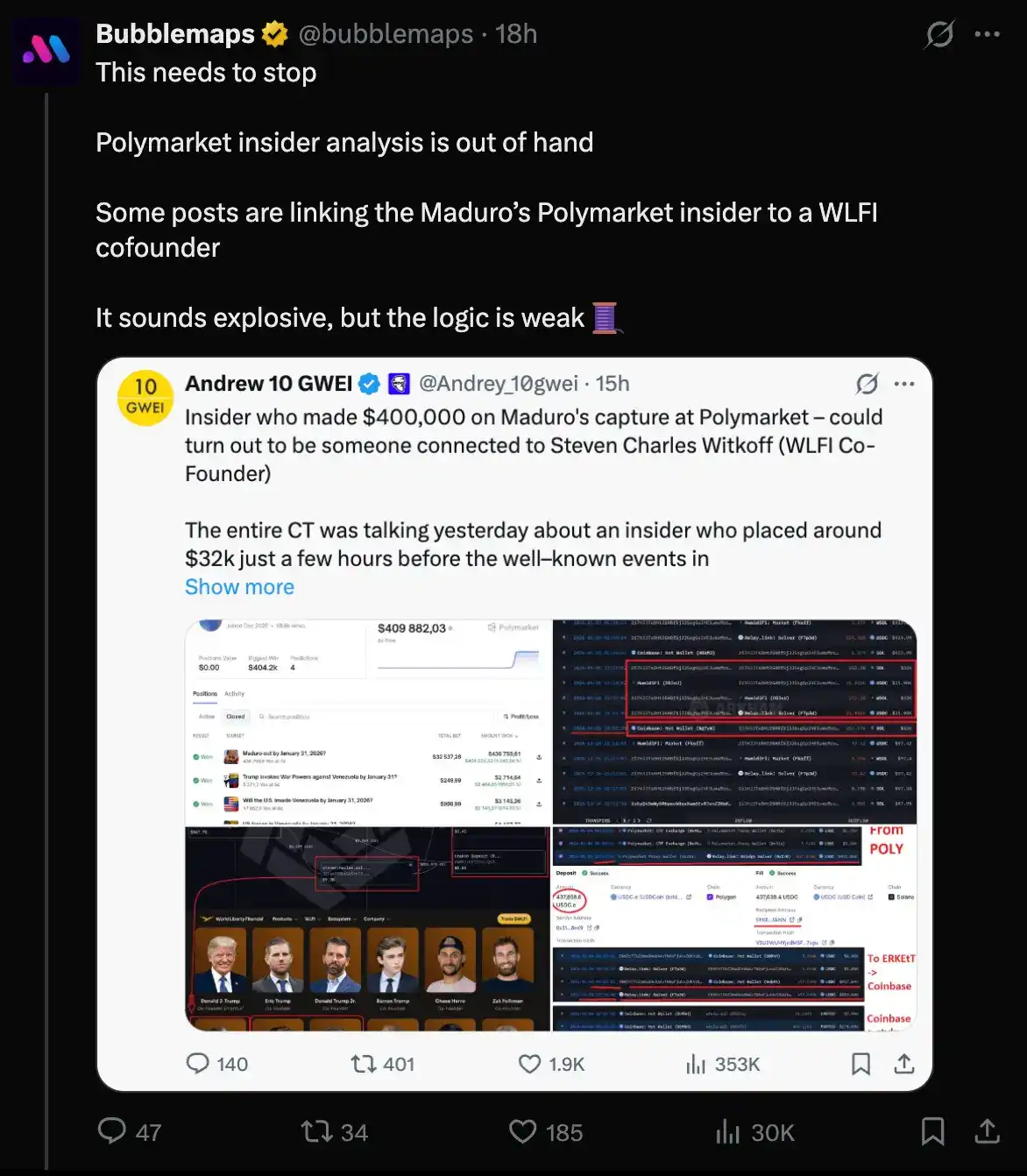

On-chain analyst Andrew 10 GWEI pointed out that the account's funding path showed high similarity: 252.39 SOL withdrawn from Coinbase on January 1 closely matched 252.91 SOL deposited by another wallet the previous day (23 hours apart),疑似通过交易所进行中转断链. More controversially, the associated wallet registered domains like StCharles.sol and had significant interactions with an address疑似 belonging to Steven Charles Witkoff, co-founder of World Liberty Finance (WLFI). Given WLFI's close ties to the Trump family, this raised strong suspicions: Was this insider trading using information from inside the White House?

On-chain analysis platform BubbleMaps later offered a different perspective. They argued that the "time and amount similarity" inference was too superficial, noting that there were at least 20 wallets on-chain that fit this pattern. They also pointed out that Andrew's argument lacked direct on-chain evidence of fund movement, so there was no reliable evidence linking the Polymarket account to the WLFI co-founder.

Congressman Proposes Integrity Act: Aiming to Regulate Insider Trading in Prediction Markets

This incident also led U.S. Representative Ritchie Torres to propose the "Public Integrity in Financial Prediction Markets Act of 2026." The core of the bill is to prohibit federally elected officials, politically appointed officials, and executive branch employees from trading in government policy-related prediction markets using "material non-public information" obtained through their official positions.

However, this bill faces a dual challenge in reality. First, the lengthy and uncertain legislative process; in the complex power dynamics of U.S. politics, such bills often undergo lengthy hearings and interest negotiations, ultimately easily becoming texts with more political posturing than substantive impact.

Second, there is an enforcement blind spot in the decentralized environment, where fund flows on-chain can easily be obscured through various privacy protocols or complex transfer mechanisms. Although the bill symbolizes the formal entry of traditional financial values into prediction markets, attempting to protect retail investors from information harvesting and maintain fair participation rights, we must consider: Will this regulatory logic, directly applied to decentralized prediction markets, conflict with core values and even cause prediction markets to fail?

The Core Value of Prediction Markets and the Paradox of Insider Trading

Returning to first principles, what is the purpose of prediction markets? Is it to give everyone a fair chance to profit, or to obtain the most accurate prediction results?

Traditional finance prohibits insider trading to protect retail investors' confidence and prevent capital markets from becoming a cash machine for the powerful. But in prediction markets, the core value may be "truth discovery."

Prediction markets are machines that aggregate fragmented information into price signals. If a market about "whether Maduro will step down" prohibits informed participants, then the market's price reflection will always be "outsiders' guesses" rather than "real probability," which would render prediction markets inaccurate.

In the Maduro incident,假设 the profiteer was not an insider but a top information analysis expert. He might have tracked abnormal radio signals at the Venezuelan border, private jet takeoffs and landings, or even the U.S. Department of Defense's public procurement lists, piecing together through model inference that military action would occur. This behavior might be highly controversial in the eyes of traditional regulation, but in the logic of prediction markets, it is an extremely valuable "information pricing behavior."

One mission of prediction markets is to break information monopolies. While各方 are interpreting ambiguous, delayed government diplomatic rhetoric, price fluctuations on prediction markets are already sending early warnings of the truth to the world. Therefore, rather than calling this insider trading, it is more accurate to say it is a博弈 that rewards hidden information surfacing through trading, thereby providing real-time risk guidance to the public.

Prediction Markets Are Tools Born from the Pursuit of Truth, Not Fair Trading Venues

The emergence of the "Public Integrity in Financial Prediction Markets Act of 2026" may reflect regulators' cognitive bias towards decentralized prediction platforms. If we pursue a "completely fair" prediction market, we will ultimately get a "completely ineffective" prediction market.

The Maduro incident profoundly reveals the true value of prediction markets: they allow hidden truths to be transformed into on-chain signals visible to all through the traces of fund flow. Blockchain transparency breaks the black box; even if we cannot immediately identify the幕后推手, when mysterious accounts heavily build positions and probabilities fluctuate剧烈, the market is actually sending a signal. This can attract smart money to quickly follow, rapidly leveling the originally unequal information gap, thereby transforming "insider information" into "public probability."

Prediction markets are not stock markets; they are essentially radars of collective human intelligence. To keep this radar accurate, it is necessary to allow the friction cost brought by information arbitrage to a certain extent. Therefore, rather than trying to block signals with bans, should we not position prediction markets as tools born from the pursuit of truth, rather than fair trading venues?