Author: Max.s

The current cryptocurrency market is undergoing a severe structural adjustment. According to the latest trading data (as shown on the chart, ETH/USDT has fallen to around $1,847.84, with a clear recent unilateral downward trend), Ethereum (ETH) is experiencing a deep correction driven by both capital flows and market expectations.

Looking back at the price movement in February 2026, ETH plummeted from above $2,360 to the $1,825 range in a short period, a drop of over 22.7%. Behind the surface of the price decline lies a comprehensive restructuring of the Ethereum network in terms of technical upgrades, organizational structure, and regulatory environment. For institutional investors and financial professionals, looking beyond short-term price fluctuations and understanding the transformation of Ethereum's underlying asset logic is the core issue at hand.

The most immediate pressure facing Ethereum currently comes from the continuous withdrawal of liquidity. This capital outflow is not a single event but a resonance of multiple sources of capital.

Net Redemptions in Spot ETFs: Risk aversion among institutional investors has significantly increased. For example, on January 29, 2026, U.S. spot Ethereum ETFs recorded a single-day net outflow of $155.7 million. Among them, Fidelity's FETH saw a net outflow of $59.2 million, BlackRock's ETHA had a net outflow of $54.9 million, and Grayscale's two funds also recorded outflows in the tens of millions of dollars. This indicates that traditional Wall Street capital is systematically reducing its exposure to Ethereum.

Concentrated Selling by Early Holders: On-chain data shows that whale accounts sold approximately 1.43 million ETH within just two weeks.

Founder's Sell-Off: This month, Ethereum co-founder Vitalik Buterin sold over 8,800 ETH, cashing out approximately $18.45 million. In traditional financial markets, intensive selling by core management is often seen as a major bearish signal, further exacerbating market panic.

Facing the market's winter, the Ethereum Foundation (EF) has made a defensive shift in its financial strategy. Vitalik Buterin announced that the foundation will enter a five-year period of "moderate austerity."

From a corporate finance perspective, this is a classic cash flow management strategy. Its core objectives are twofold: first, to ensure the foundation can continue to fund the development of Ethereum's core underlying technology in the future, avoiding threats to its independence due to excessive resource consumption; second, to ensure that Ethereum's ambitious roadmap as a high-performance "world computer" is delivered on schedule.

To support this strategy, Vitalik himself proactively severed the funding dependence of some "special projects" on the foundation. He chose to extract 16,384 ETH and use decentralized staking yields to self-fund research and development for public goods such as open-source software, hardware, and privacy protection projects. This approach of internalizing peripheral R&D expenses and focusing on core business marks a move toward maturity and restraint in Ethereum's capital operations.

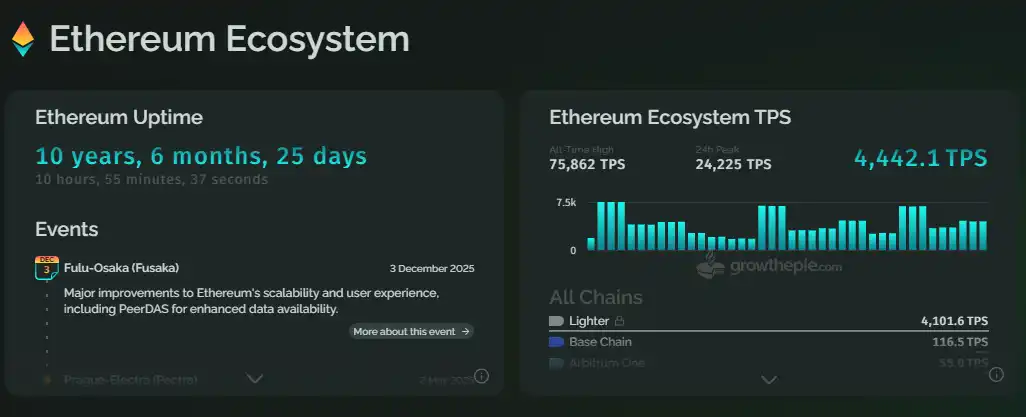

While the price is under pressure, Ethereum's technical fundamentals have shown remarkable resilience, even exhibiting a rare phenomenon of "price-volume divergence." Recently, the Ethereum network's TPS (transactions per second) reached a historic high of 75,862, far exceeding the previous peak of 58,786.

This is largely due to the Fusaka upgrade deployed last December. This upgrade introduced the PeerDAS mechanism, significantly expanding the data throughput of Layer 2 networks. However, with the explosion in data capacity, new systemic risks are emerging. Vitalik pointed out that because current block builders still need to download complete data, the network faces serious centralization risks.

To address this hidden danger, Ethereum plans to launch the Glamsterdam upgrade in 2026, which is essentially a bottom-up reform targeting internal oligopolies within the network.

ePBS Mechanism Reshapes Profit Distribution: The core of this upgrade is ePBS (in-protocol proposer-builder separation). It forcibly incorporates the block-building process into the protocol's底层, standardizing the bidding process and weakening the absolute dominance of the current few external builders over the market.

Preventing Rent-Seeking by Giants: For financial professionals, this means Ethereum is proactively intervening in its internal MEV (Maximal Extractable Value) market structure, breaking down the technical barriers of leading capital, and reconstructing the underlying logic of staking yields.

In addition to the internal structural pains, the Ethereum ecosystem also faces the impending regulatory hammer. The EU's MiCA (Markets in Crypto-Assets) regulation, set to take full effect on July 1, 2026, requires all crypto businesses operating within the EU to meet strict compliance standards.

The implementation of this regulation will directly impact the vast number of DeFi protocols, liquidity providers, and related derivative markets on the Ethereum chain that lack the backing of traditional corporate entities. The sharp rise in compliance costs and the early withdrawal of some non-compliant funds are the deep-seated macro reasons behind the recent sustained bleeding in the spot market.

Ethereum is in a period of divergence: on one side, there is the ruthless selling by short-term capital and the pre-pricing of strict regulations; on the other, there is the robust expansion of technical infrastructure and a self-driven revolution against internal monopolies. This is a typical "deleveraging" process, trading short-term pain for long-term systemic stability.