Author: Oluwapelumi Adejumo, CryptoSlate

Compiled by: Saoirse, Foresight News

Original title: 2025 Crypto 'Wealth Creation List': 12 Big Winners, Who Made the Right Bet?

If 2024 was the "year of recovery" for the cryptocurrency industry, then 2025 is the year the industry's "infrastructure finally gains recognition."

This year, the emerging industry started in January with cautious optimism and by December had gained clear federal regulatory support.

The result is a complete shift in the industry narrative from "cryptocurrency equals a casino" to "cryptocurrency is capital market infrastructure."

During this period, trading volume shifted on-chain, policymaking entered the White House's purview, and large asset managers no longer hesitated—Vanguard's policy reversal earlier this month is the most vivid proof, as the company now allows cryptocurrency ETFs on its platform.

However, this year, despite record inflows and legislative victories for the industry, the gains were not shared equally by all participants.

The winners of 2025 are not just assets whose prices rose, but also protocols, figures, and products that have firmly established themselves in the future financial landscape.

Based on CryptoSlate's analysis, here are the 12 clear winners of the year and why they matter:

1. The United States and the Trump Administration

Discussing the cryptocurrency landscape in 2025 is impossible without acknowledging the massive impact of the shift in the US stance. For years, the cryptocurrency industry has been in a state of "ready to leave," viewing Dubai or Singapore as potential "safe havens."

But in 2025, the US firmly closed this "exit," and all parties in the industry were happy to accept the change. Therefore, this victory belongs both to the US jurisdiction and to the top-level forces driving this transformation.

The administration of the 47th US President, Donald Trump, achieved many long-standing demands of the cryptocurrency industry in less than 12 months, effectively "bringing the digital asset economy back home."

Multiple pro-digital asset executive orders set the tone, and strategic victories were reflected in specific policies:

The GENIUS Act signed on July 18 provided the first federal-level definition for stablecoins;

The "Strategic Bitcoin Reserve" executive order issued in March sent a clear signal to global sovereign wealth funds—digital assets have become an important national security issue.

Crucially, by pushing for leadership changes at the US SEC and CFTC, the Trump administration dispelled the fog of "regulation by enforcement."

In essence, Trump's series of actions set the tone for the US to "become the global cryptocurrency hub."

2026 Outlook: Consolidation of US Hegemony

The US is expected to actively export its newly established industry standards. Additionally, an executive order effective January 1 explicitly prohibits the issuance of a central bank digital currency (CBDC), clearing the way for private sector innovation: the future dollar will still go digital, but the issuers will be companies like Tether, Circle, and various banks, not the Federal Reserve.

2. US Spot ETFs

(Represented by IBIT, including ETH, SOL, XRP ETF camps)

As the primary vehicle for institutional entry into the cryptocurrency market, cryptocurrency spot ETFs not only "survived their second year" in 2025 but thrived even amid Bitcoin's underperformance.

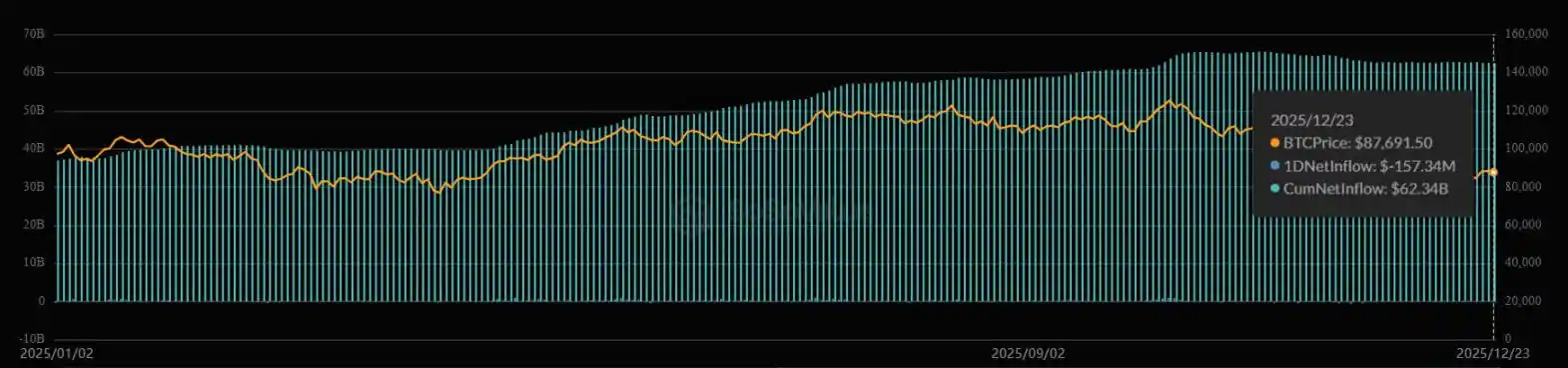

BlackRock's iShares Bitcoin Trust (IBIT) became one of the top ten US ETFs by inflows, even surpassing traditional giants like the Invesco QQQ Trust and the SPDR Gold Trust (GLD), is the most direct proof.

IBIT Cumulative Net Inflows (Source: SoSo Value)

Beyond Bitcoin, Ethereum spot ETFs also solidified their position as the "default entry channel" for wealth management institutions—making debates like "not your keys, not your coins" irrelevant among institutional investors.

September was a key turning point: the SEC approved a "universal listing standard." This technical but crucial policy victory significantly reduced the approval process for future products, eliminating the need to file separate 19b-4 forms for each new ticker.

Subsequently, the market saw a flood of new products focused on other digital assets (like Solana, XRP), all of which performed strongly this year.

2026 Outlook: Product Diversification and Risk Reduction

With Vanguard opening access to cryptocurrency ETFs on December 1, a wave of "basket ETFs" and "covered call ETFs" is expected. A more developed options market will begin to reduce actual volatility, ultimately making the cryptocurrency asset class acceptable to conservative pension funds.

3. Solana (SOL)

In 2025, Solana completely shed its "high-risk beta asset" label; the old narrative of "fast but prone to failure" is history.

Simultaneously, Solana accomplished the most difficult transformation in the cryptocurrency industry this year: transitioning from a "Meme coin casino" to a "liquidity layer for global markets."

While maintaining its dominance in the cultural sphere, CoinGecko data shows Solana has been the world's most watched blockchain ecosystem for two consecutive years (2024-2025).

Today's Solana network no longer revolves solely around speculative tokens but is a "hub for efficient capital."

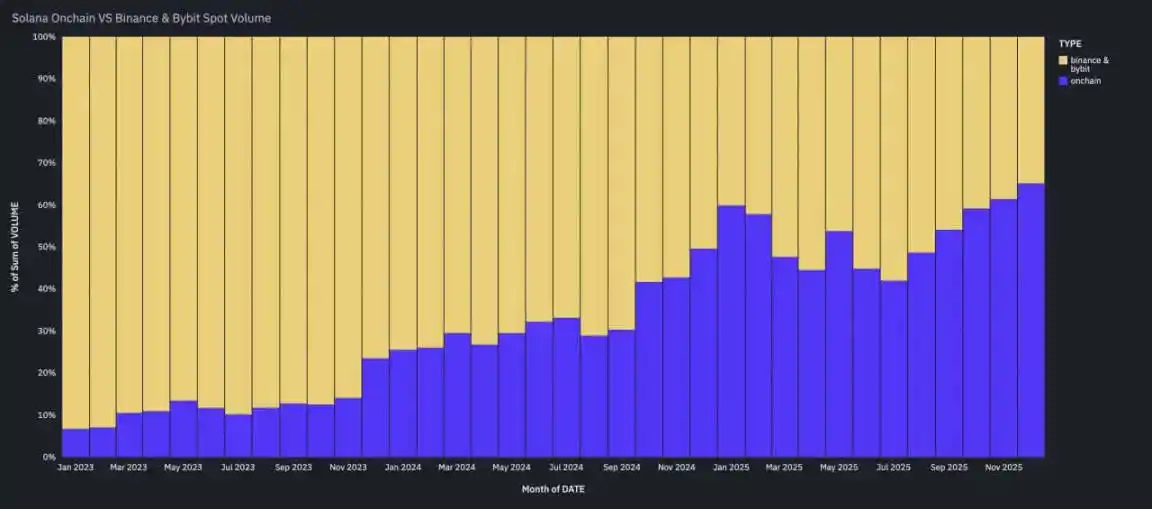

According to Artemis data, Solana has become a core liquidity layer: its on-chain SOL-USD trading volume exceeded the combined SOL spot trading volume of Binance and Bybit (two of the top three centralized exchanges by global volume) for three consecutive months.

Solana On-Chain Volume Surpasses Binance and Bybit Spot Volume (Source: Artemis)

In essence, Solana has positioned itself as the "primary venue for activities sensitive to trade execution speed." Its competitors are no longer just Ethereum, but also traditional financial market platforms like Nasdaq.

2026 Outlook: On-Chain Price Discovery Becomes Mainstream

This "on-chain shift" in trading volume marks a structural change: price discovery is moving from centralized exchanges to on-chain. Solana in 2026 will no longer be a "high-risk beta network" but the main venue for high-frequency, stablecoin-denominated trading.

4. Ethereum Layer-2 Base

If Solana's advantage is "speed," then Base, the Ethereum Layer-2 network from Coinbase, wins with "user reach."

By leveraging the massive existing user base of this US exchange, Base has become the "default choice for consumer applications and stablecoin experiments," with extremely high user stickiness.

Base's success proves that in the 2025 cryptocurrency industry, "user reach" is more important than "novel crypto technology." It has become an incubator for "mass crypto applications"—consumer fintech apps that use crypto infrastructure on the backend but are completely imperceptible to users. Arguably, Base is the bridge connecting the chaotic on-chain world with Coinbase's compliant and secure system.

2026 Outlook: Rise of "Wallet-Native Commerce"

Base is expected to be the "core engine" for Coinbase's entry into merchant payments next year; "wallet-native commerce" (commerce based on crypto wallets) could become a new industry trend.

5. Ripple and XRP

After years of legal troubles, 2025 finally became the year Ripple and XRP "regained their freedom."

Ripple's long-running legal battle with the SEC ended with a final judgment, removing obstacles to institutional adoption of XRP.

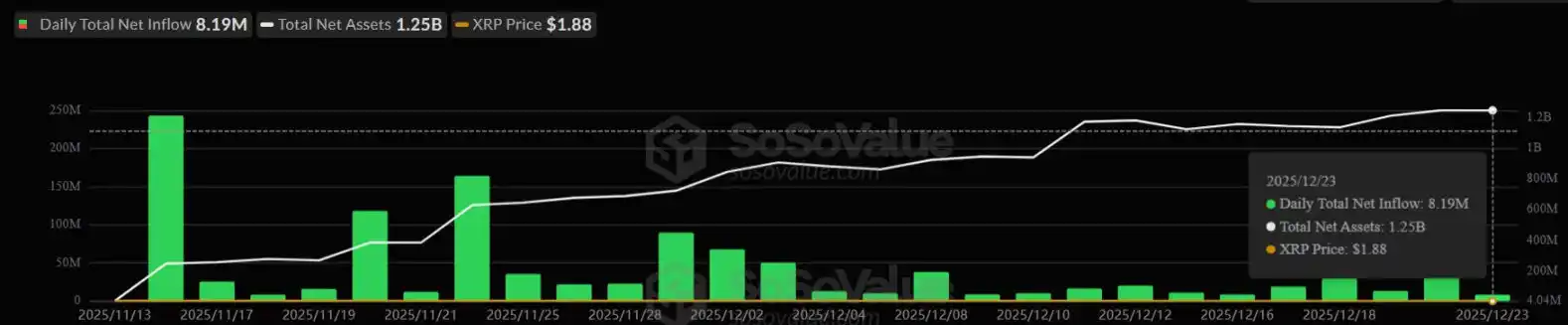

The result was that XRP's narrative overnight shifted from an "asset with litigation risk" to a "liquidity engine," driving its price up and paving the way for the launch of the first XRP spot ETFs in November.

XRP Exchange-Traded Fund Daily Flows (Source: SoSo Value)

Meanwhile, Ripple the company aggressively acquired traditional financial infrastructure this year: in 2025 alone, Ripple invested over $4 billion in strategic acquisitions, most notably including the acquisition of prime broker Hidden Road, treasury management company GTreasury, and stablecoin infrastructure provider Rail.

These moves彻底 transformed Ripple from a "payment company" into a "full-stack institutional-grade giant."

2026 Outlook: Integrating TradFi and Crypto Ecosystems

The "ETF-ization" of XRP is just the beginning. With legal risks消散 and Wall Street products落地, 2026 will be the "year of integration": Ripple's newly acquired treasury management and brokerage divisions are expected to begin cross-promoting the RLUSD stablecoin to Fortune 500 companies, ultimately breaking down the barriers between the Ripple ledger and corporate balance sheets.

6. Zcash and the Privacy Coin Sector

The recovery of Zcash and the entire privacy coin sector is the most surprising "comeback story" in the 2025 cryptocurrency industry.

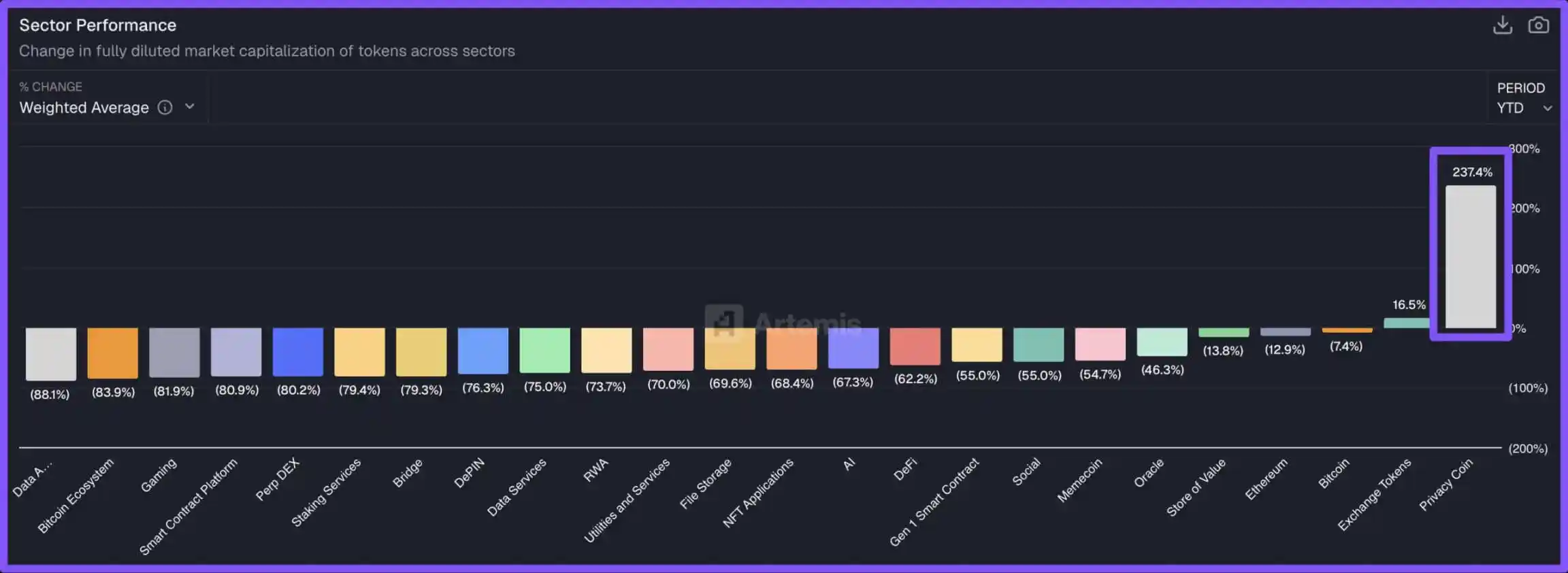

As the best-performing sector in 2025, privacy coins shed the stigma of "illegal use" and became the darlings of the "post-surveillance economy."

Outstanding Performance of Privacy Coins in 2025 (Source: Artemis)

Although Zcash led this recovery, the momentum covered the entire privacy coin space: Ethereum developers accelerated privacy-related plans, and other privacy solutions finally saw real-world use on mainnets.

Furthermore, a "thaw" in the regulatory environment was evident—the SEC held its first formal meeting with privacy protocol leaders to discuss compliance architecture. This was unthinkable a year ago.

2026 Outlook: Birth of "Privacy DeFi"

The privacy coin sector is expected to see "differentiation" in 2026: privacy will become a "premium feature" for compliant institutions. Wall Street will actively adopt these "selective disclosure tools" to prevent MEV (Maximal Extractable Value) front-running and protect the confidentiality of proprietary trading strategies.

7. Asset Tokenization (RWAs)

With strong support from a friendly SEC, Real World Assets (RWAs) transitioned from "pilot projects" to "core infrastructure" in the cryptocurrency industry.

The SEC's cessation of hostile enforcement actions allowed large institutions to confidently integrate these assets without fear of receiving a "Wells Notice" (a precursor to an SEC enforcement investigation).

BlackRock's BUIDL fund being accepted as "off-chain collateral" by Binance was a watershed event for this field—it blurred the lines between traditional finance (TradFi) and crypto market structures.

By December, the Assets Under Management (AUM) for tokenized money market funds and US Treasuries exceeded $8 billion, while the entire RWA market size was approximately $20 billion.

RWA Assets (Source: RWA.xyz)

Furthermore, TradFi giants like BlackRock, JPMorgan, Fidelity, Nasdaq, and the Depository Trust & Clearing Corporation (DTCC) have high hopes for the RWA space, expecting it to bring greater transparency and efficiency to the traditional financial industry.

As SEC Chairman Paul Atkins stated: "On-chain markets will bring higher predictability, transparency, and efficiency to investors."

2026 Outlook: "Repo-Like" Efficiency Gains

As large banks like JPMorgan and Bank of New York Mellon continue to integrate RWA assets, a 24/7 collateral market is expected to gradually form, pushing the sector's AUM towards $18 billion.

8. Stablecoins

The debate over the "killer app of cryptocurrency" is settled: stablecoins are the core infrastructure. In October 2025, the total stablecoin market cap surpassed $300 billion; in September, the Ethereum ecosystem's stablecoin supply also hit a record high of $166 billion.

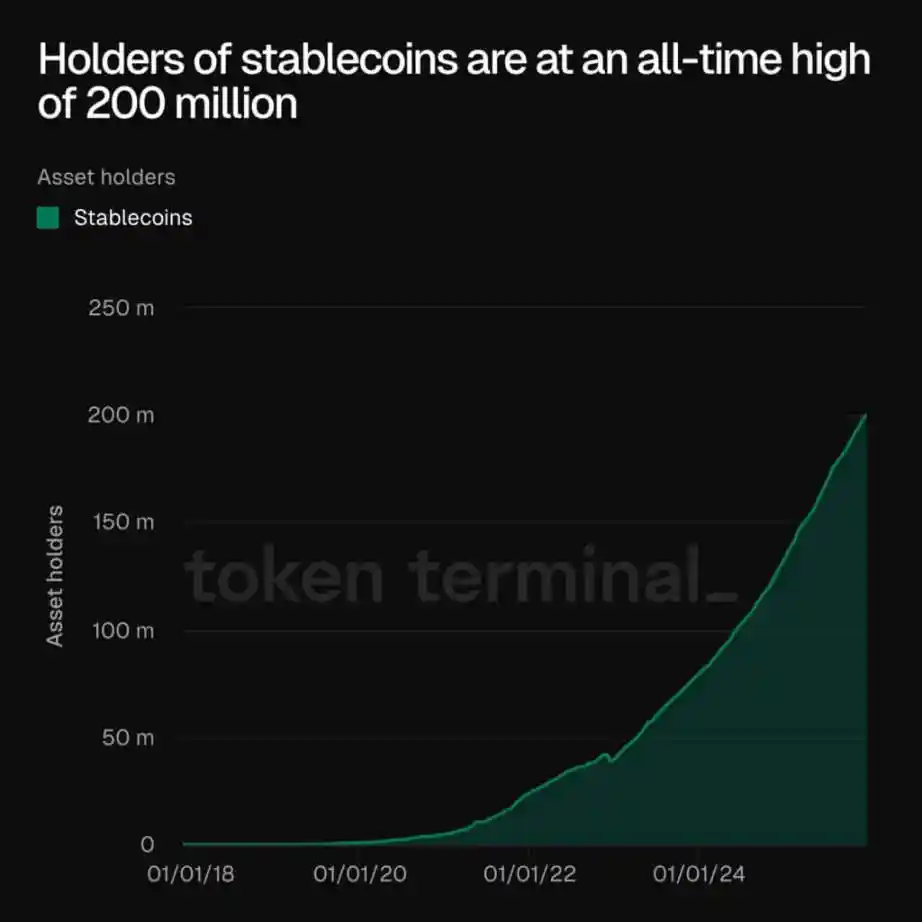

In fact, Token Terminal data shows the total number of stablecoin holders has reached a historical peak of approximately 200 million.

Stablecoin Holders (Source: Token Terminal)

This data indicates that the growth in the stablecoin sector stems from its core capabilities: "cross-border, 24/7, instant settlement."

Meanwhile, US legislative progress (especially the passage of the GENIUS Act) provided legal certainty for banks to enter the stablecoin space.

In essence, stablecoins are no longer just "gambling chips"; they are becoming the "settlement layer" for global fintech. As Jeremy NG, founder of Open Eden, stated: "Stablecoins have crossed over from being 'infrastructure accessories' for crypto to being the 'core of financial infrastructure.'"

2026 Outlook: Yield-Driven Growth

"Programmatic treasury investment" and "foreign exchange trading use cases" are expected to be the core drivers of stablecoin growth, with the total stablecoin market cap有望 reaching a benchmark of $380 billion in 2026.

9. Perp DEXs

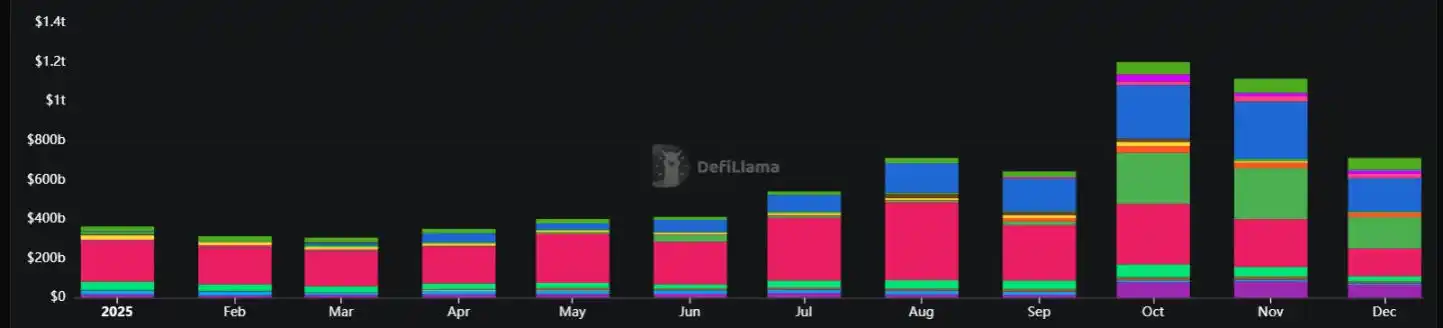

On-chain derivatives彻底 broke through the "credibility bottleneck" in 2025—October saw a record monthly trading volume of $1.2 trillion.

This sector became a winner because it successfully attracted significant volume from centralized exchanges (CEXs): by offering "self-custody" features and more attractive incentive mechanisms, on-chain perpetual contract platforms won over traders.

Rising Volume on Perpetual Decentralized Exchanges (Source: DeFiLlama)

The rise of perpetual decentralized exchanges (Perp DEXs) like Hyperliquid and Aster marks the maturation of DeFi market structure. Today, traders are willing to take on billions in smart contract risk to avoid counterparty risk.

2026 Outlook: Intensifying Fee Competition

On-chain open interest (OI) is becoming a legitimate macro risk indicator. However, 2026 is likely to see fierce "fee wars" in this sector—protocols will compete intensely for this $1.2 trillion monthly trading volume.

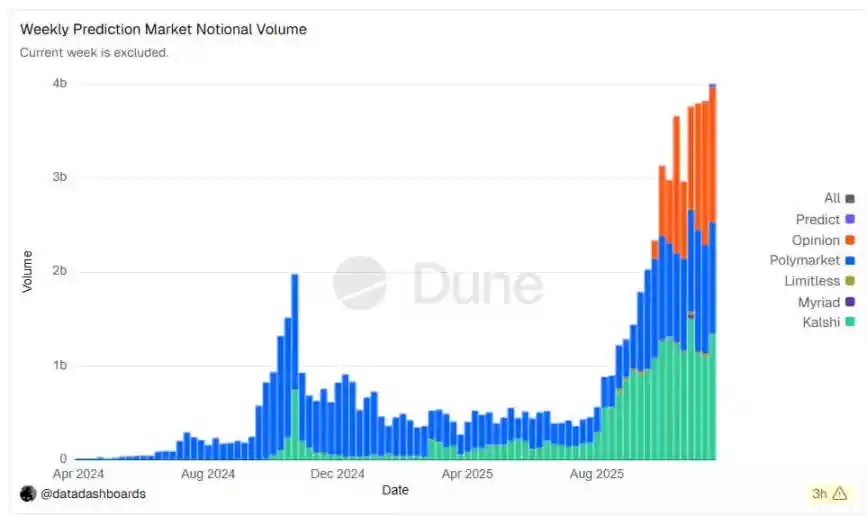

10. Prediction Markets

2025 was the year "event contracts" (the core product of prediction markets) entered the US mainstream: the two leading platforms in this field, Kalshi and Polymarket, both recorded record trading volumes.

But the more iconic victory was the entry of traditional financial institutions and crypto-native companies like Gemini and Coinbase into this emerging field.

Prediction Market Weekly Volume (Source: Dune Analytics)

Prediction markets became winners because they bridged the gap between "gambling" and "finance." Furthermore, Polymarket gained a clear development path through the CFTC's (Commodity Futures Trading Commission) revised framework, transforming "event contracts" from "niche internet curiosities" into "compliant hedging tools."

2026 Outlook: Standardization and Scaling

Event contracts are becoming a standardized asset class. With the "outcome economy" (financial activity around event outcomes) expected to reach a nominal value of $60 billion, crypto wallet infrastructure and USDC flows are有望 to see significant growth as a result.

11. Hong Kong, China

While the US focused on legislation, Hong Kong, China, focused on "execution advantage"—the data proves it. In Q3 2025, Hong Kong's ETP (Exchange Traded Product) market, measured by turnover, officially surpassed South Korea and Japan to become the world's third-largest ETP market, with an average daily turnover of HK$37.8 billion, a 150% year-on-year increase.

Hong Kong's strategy of "attracting the industry through clear regulation" yielded tangible results in the exchange sector: the Virtual Asset Trading Platform (VATP) regime evolved from a state of "presumed licensing" ambiguity into a robust ecosystem.

By mid-2025, the Securities and Futures Commission (SFC) of Hong Kong had issued formal licenses to more global large exchanges, bringing the total number of licensed exchanges to 11. This move effectively channeled regional institutional liquidity into a "compliant, bank-connected" system while isolating unregulated participants.

Meanwhile, Hong Kong's Stablecoin Ordinance, effective August 1, created a "high-quality sandbox"—by the application deadline in September, the sandbox had attracted over 30 applications.

2026 Outlook: Becoming Asia's Settlement Hub

With the first stablecoin licenses expected to be issued in early 2026, Hong Kong is poised to become Asia's cryptocurrency settlement hub. By combining the "world's third-largest ETP market" with "licensed stablecoin infrastructure," Hong Kong has successfully positioned itself as the "key valve for institutional liquidity in the Asia-Pacific region."

12. Early Believers (Crypto Investors)

The final spot on this list belongs to "those of you who held on"—the early believers in cryptocurrency.

Over the past challenging years, early believers constantly heard that "cryptocurrency is a scam, a bubble, or a dead end." They endured the industry crash of 2022, the regulatory suppression of the "Gensler era," and the industry's quiet period in 2024. In 2025, their perseverance was finally vindicated. (Gensler era: Refers to the period when Gary Gensler chaired the US SEC)

The significance of this year is not just "rising asset prices," but also "validation of core beliefs."

The result is that these early believers successfully "stayed ahead of the world's most renowned institutions": when BlackRocks, Vanguards, and sovereign wealth funds entered the cryptocurrency market en masse this year, the assets they bought were the same assets these early believers held with conviction during the industry's darkest hours.

2026 Outlook: From Investors to "Ecosystem Bankers"

As this group achieves "intergenerational wealth accumulation," they are not exiting the crypto ecosystem but are becoming its "bankers." This group is expected to become the primary liquidity providers (LPs) for new decentralized capital markets, funding the next wave of innovation that banks still cannot comprehend.