Author: Gu Yu, ChainCatcher

After several months, the Layer1 public chain sector has recently seen another financing round at the billion-dollar valuation level. Pharos, which claims to be a high-performance parallel Layer 1 public chain, announced an upgrade in its capital cooperation with the Hong Kong Stock Exchange-listed company GCL New Energy. GCL New Energy completed an investment subscription in Pharos at a valuation of $950 million, with an amount of $24.73 million.

GCL New Energy is a well-known domestic private photovoltaic power generation enterprise, mainly engaged in the development, construction, operation, and management of solar power stations. This aligns very well with Pharos's key RWA development direction, making it seem like a transaction of positive strategic significance for both parties.

However, this transaction has also raised many questions in the market. Given the current dismal secondary market, can projects in the Layer1 and RWA sectors really achieve billion-dollar valuations in the primary market? Would a listed company easily invest in such high-risk assets?

A Mutually Binding Betting Transaction

Many details hidden in the complex announcements show that this is not a conventional direct financing transaction, but a bundled deal involving mutual investment, phased settlements, and market value betting. Moreover, all core settlement conditions are firmly in the hands of GCL New Energy. If any condition is not met, this transaction will be nothing more than an empty document without any substantive binding force.

Among them, Pharos's share subscription in GCL New Energy is a preconditioned investment. It will subscribe for a maximum of 183,480,000 new shares in the company at a price of HK$1.05, worth approximately HK$150 million. This price represents a 15% discount compared to GCL New Energy's current price (HK$1.23).

This transaction seems to favor Pharos, but GCL New Energy is clearly well-versed in financial operations and has set five stringent settlement thresholds for this share subscription. If any batch of settlement conditions is not met, all subsequent settlements will be terminated, and the entire agreement is valid for only 18 months. Specifically, this investment is divided into five batches of settlements, with unlocking conditions all tied to the listing performance of the Pharos Token:

The first batch, accounting for 50%, will only proceed if the Pharos Token is successfully approved for listing on relevant Web3 exchanges and the opening price is not lower than the company's agreed investment price (calculated based on a $950 million valuation). If the listing fails or the opening price falls below the issue price, the company has the right not to proceed with the settlement.

The second batch, accounting for 12.5%, will only proceed if the daily average FDV (Fully Diluted Valuation) of the Pharos Token in the first three months after listing is not less than $760 million.

The unlocking conditions for the subsequent three batches are roughly similar, with the main difference being the calculation periods for the average FDV: the fourth to sixth months, the seventh to ninth months, and the ninth to twelfth months, respectively.

Once the Pharos Token meets the settlement conditions, Pharos's share subscription in GCL New Energy will take effect accordingly, and GCL New Energy's subscription for the Pharos Token will also take effect simultaneously, with the same unlocking ratio.

In other words, after the successful listing of the Pharos Token, Pharos will immediately settle a HK$75 million share subscription with GCL New Energy, while GCL New Energy will acquire Pharos Tokens worth approximately HK$96.73 million at a valuation of $950 million.

For GCL New Energy, this is an almost risk-free transaction. On one hand, it can obtain HK$75 million in share subscription funds, and on the other hand, if the Pharos Token performs well, it can acquire tokens worth nearly HK$100 million at the initial listing valuation, offering considerable profit margin.

The positive news has already been reflected in the stock price. Although GCL New Energy first disclosed its cooperation with Pharos on January 8, its stock price had already risen significantly a week earlier, climbing from HK$0.8 to HK$1.3 on the announcement day, and later reaching a peak of HK$1.8. Since then, it has been on a downward trend. In the trading market, this is a typical "rat trading" pattern.

Another potential issue is that Pharos has previously disclosed a cumulative financing of only $8 million, equivalent to HK$62.61 million. Therefore, even if the pre-investment conditions are met, this funding gap may pose a challenge for Pharos.

Source: RootData

How Was the $950 Million Valuation Derived?

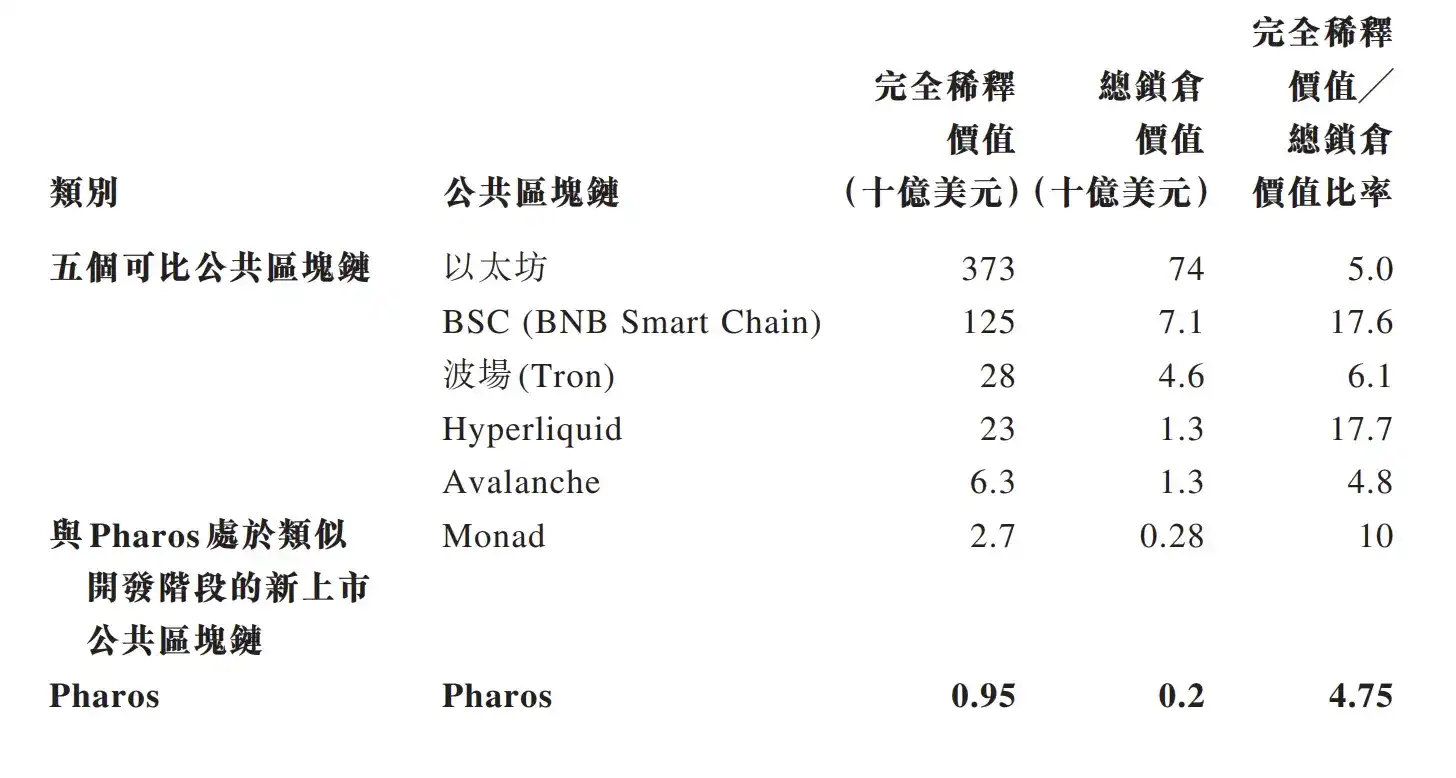

Another interesting piece of information is that GCL New Energy also detailed in the agreement why it valued Pharos at $950 million. According to the agreement, this investment valuation is primarily based on the on-chain total value locked (TVL). In the Layer1 sector, the average ratio of fully diluted valuation (FDV) to total value locked (TVL) for Ethereum, BSC, Hyperliquid, Tron, and Avalanche is 10x, with a median of 6x. Monad, which has a similar technical route, has a ratio of 10x.

Therefore, both parties decided to set the calculation coefficient for Pharos at 4.75x. Since Pharos's current total value locked is $250 million, and calculated with a 20% discount, the initial valuation should be $950 million.

Regarding the types of on-chain locked assets, the agreement disclosed that currently, among all locked assets in Pharos, 51% come from new energy assets of distributed photovoltaic operators and centralized power station operators, and 49% come from financial assets of fund management companies and credit asset issuers.

In other words, Pharos's total value locked includes physical assets in its calculation, specifically power station and photovoltaic assets closely related to the parties involved in this transaction. This calculation method sets a precedent in the Layer1 industry.

In fact, Pharos's mainnet has not yet been officially announced as launched. Professional on-chain data statistics platforms like DeFiLlama do not include Pharos's locked data, and the $250 million figure is entirely a unilateral disclosure from the project team.

The premature stock price movement, combined with the layers of betting conditions in the agreement and the inflated valuation calculation, makes it easy to see the true purpose of this transaction: For GCL New Energy, this may be a financial operation to hype the stock price and boost the company's market value by leveraging crypto concepts. For Pharos, it is an attempt to rely on the listed company's physical assets to create a high-valuation buzz and build momentum for the subsequent token listing. Both parties get what they need, but leave the risks to the market and subsequent investors.

When a实体产业 company injects physical assets into a Layer1 project and then calculates a valuation several times the value of those physical assets to easily create a $950 million valuation, isn't this capital game too outrageous? Does the crypto market really need such RWA?