On the evening of March 30th, Beijing time, the long-planned Aave V4 officially launched on the mainnet, bringing the first piece of good news since the Aave DAO governance debates began in 2024.

V4 can be described as a complete overhaul of Aave, with the most core change being the integration of previously independent lending markets into a unified liquidity pool architecture: the Hub and Spoke model.

In V4, each chain or L2 has a unified liquidity center (the Hub), where all assets deposited by users for lending are pooled into a single liquidity pool. The Hub is responsible for global coordination, credit limit control, system-level constraints (such as "Total Borrows ≤ Total Supply"), and emergency pauses. The Hub does not interface directly with users; it manages liquidity in the background.

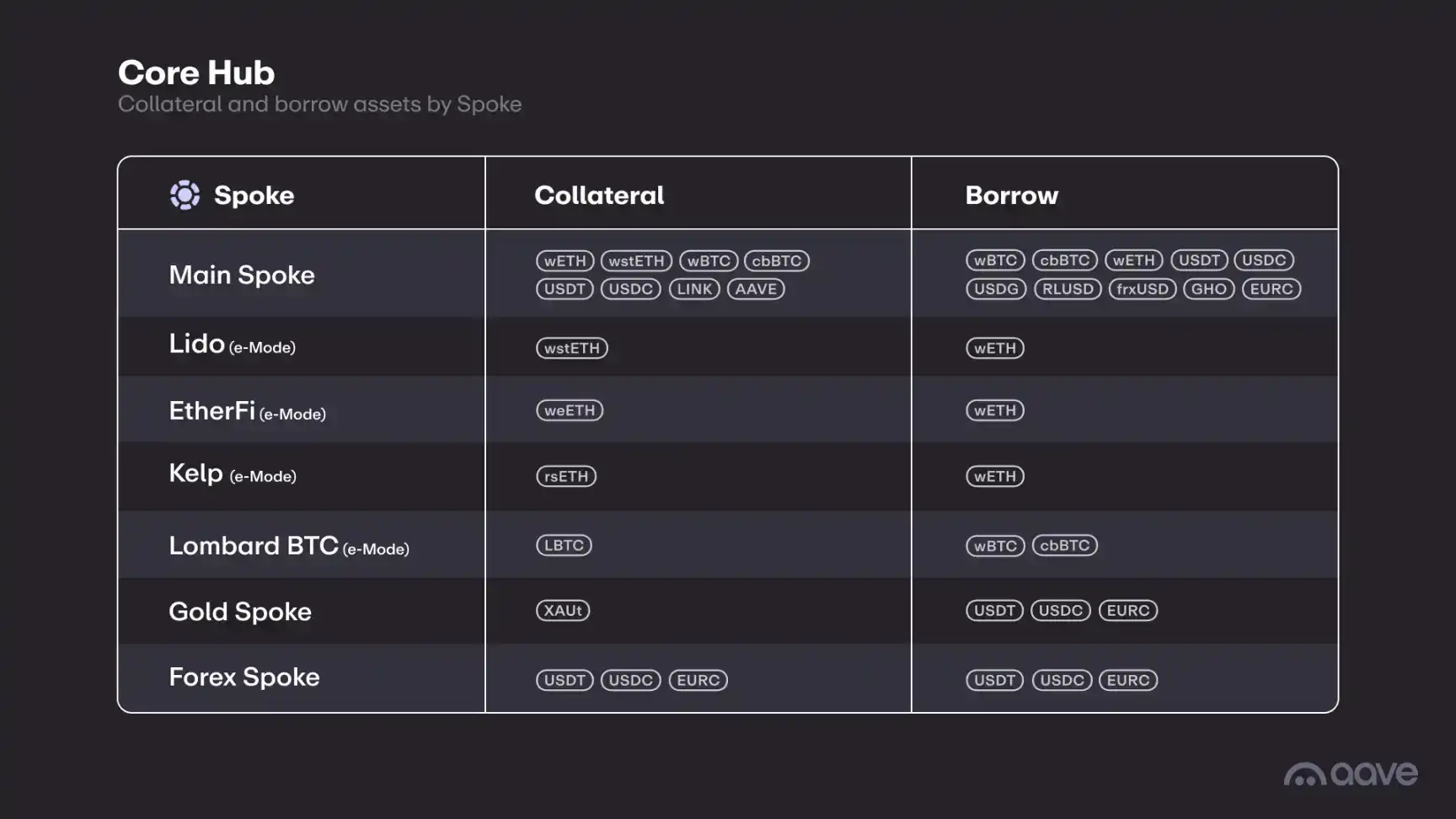

It is worth noting that there is not just one Hub per chain, but different Hubs are designed based on different needs, which is essentially a form of risk isolation. For example, V4 has currently launched the Core Hub, Prime Hub, and Plus Hub. The Core Hub contains mainstream assets and is open to all users, the Prime Hub is designed for suppliers seeking more "controllable" collateral, and the Plus Hub is designed for strategic stablecoins, with its parameters needing to consider the project's scale.

As for the Spoke, you can think of it as an independent market, each with its own lending functions, risk parameters, and collateral rules. Within a single Hub, user assets reside in the same liquidity pool, and borrowers choose different Spokes based on their needs. For example, as shown in the diagram above, a user can deposit WETH as a borrowable asset. Borrowers can borrow WETH from the first four Spokes, but only the EtherFi Spoke allows weETH to be used as collateral.

Although the official claim is that this integrates fragmented liquidity, in practice, the difference is not significant for users borrowing against high-quality collateral. For instance, if you want to抵押 ETH to borrow assets, the operation in V3 and V4 is not fundamentally different, as long as you ensure the health factor does not drop too low.

So, regarding the integration of liquidity, V4 indeed offers more精细 management than independent markets, but it's not a qualitative leap. The real differences come from the customizable parameters of the Spokes and the new liquidation engine.

In V4, a borrower's interest rate depends on the base rate and a risk premium. The base rate, like in V3, uses a utilization curve—rising slowly below optimal utilization and steeply above it. The risk premium depends on the nature of the collateral asset. If the collateral is more stable assets like USDT, ETH, or WBTC, the risk premium will be very low or even 0. However, high-risk altcoins will have a high risk premium, avoiding the situation where "good assets subsidize bad assets."

To give a simple example, in V3, the interest rate depended solely on supply and demand. When borrowing USDT, even though the loan-to-value (LTV) and liquidation threshold might differ, the interest rate for collateralizing ETH and LINK would be the same under the same supply and demand conditions, even though LINK's volatility is higher than ETH's. If the rates are the same, borrowers using LINK as collateral drive up the utilization rate, potentially causing borrowing costs for users collateralizing ETH to rise instead of fall.

V4 optimizes this flaw. Users borrowing against high-risk collateral need to pay a higher cost, while fund providers can earn higher yields. Simultaneously, the higher interest rate curbs borrowing demand, giving users borrowing against优质资产 a more明显的 cost advantage.

Regarding the liquidation mechanism, liquidators will only restore the health factor to the target value preset by the Spoke, and the lower the health factor, the higher the liquidation bonus. This design not only gives borrowers more room for maneuver but also reduces the platform's overall bad debt risk. Additionally, the new liquidation engine includes a "anti-dust mechanism," meaning if the remaining debt or collateral falls below a threshold (e.g., $1000), the liquidator must fully liquidate the position, preventing the accumulation of small残留 amounts that reduce capital efficiency.

Finally, idle liquidity in the Hub can be automatically deployed into low-risk yield strategies approved by governance (such as short-term government bonds, stablecoin LPs, money market instruments, etc.). This increases the income for fund suppliers while also boosting DAO revenue, which is perhaps one of the few advantages of "unified liquidity."

Overall, the advantages of Aave V4's unified liquidity for lending are not显著. The so-called composability—allowing borrowers to manage positions across different Spokes uniformly—is also not much more convenient than V3. But as the title suggests, V4 transforms Aave from a product into a financial infrastructure resembling a "bank."

Setting aside various complex operations, the core business of a bank is to accept deposits, retain a portion as reserves for daily user payments, transfers, etc., and earn the spread between deposits and loans through lending. As for idle funds, the bank can also allocate them to different investments within its risk tolerance.

The Bank of Saint George, established in 1407 in Genoa, Italy, is often considered the world's first bank. It not only provided deposit and loan services but also handled government debt management, currency exchange, and fund transfers, meeting the commercial needs of Genoa as a major European trade center at the time.

From the launch of ETHLend in 2017 to the mainnet release of Aave V4 in 2026, in less than 10 years, Aave has built what the earliest banks looked like. Of course, there are significant differences between Aave and a bank; this is just an analogy. Compared to P2P, the bank model, tempered by centuries of black swan events, is naturally a better choice, just as V4 is an improvement over V3.

If you look closely, you'll find that a vast amount of "innovation" in the DeFi sector has almost become历史尘埃, such as the hot DeFi 2.0 trend in the second half of 2021. Instead, projects like Aave, with simple business logic that has been成熟 in traditional finance for centuries, have survived and thrived. After years of exploration, many DeFi projects have likely discovered this truth: the ceiling for DeFi is high, but not a single step of the path taken by traditional finance can be skipped.

Aave V4's centralized liquidity opens up numerous future possibilities. For example, assets idle for a certain period (e.g., one year) could be allocated to relatively higher-risk investments, such as providing ETH/USDT liquidity on Uniswap. It could operate entirely in the mode of a commercial bank, gradually adding other commercial banking services, such as credit cards (referencing Ethfi's model of spending stablecoins borrowed against collateral), and so on.

Going a step further, Aave could expand into "investment banking." For instance, launching an ICO platform allowing users earning interest on deposited assets to borrow USDT or USDC to participate in investments, eliminating the need to withdraw and sell assets for stablecoins. This way, it could charge fees from projects on one side and collect interest on the other.

Although the Hub & Spoke mechanism doesn't bring massive innovation to lending itself, it paves the way for the next crucial steps.