Author: Fintax

Basic Positioning of CARF

CARF is a framework for the automatic exchange of tax-related information on crypto-assets, with crypto-asset service providers as the reporting entities, used to support tax authorities in various jurisdictions in obtaining information related to transactions involving their taxpayers.

Global Implementation Progress and Timeline

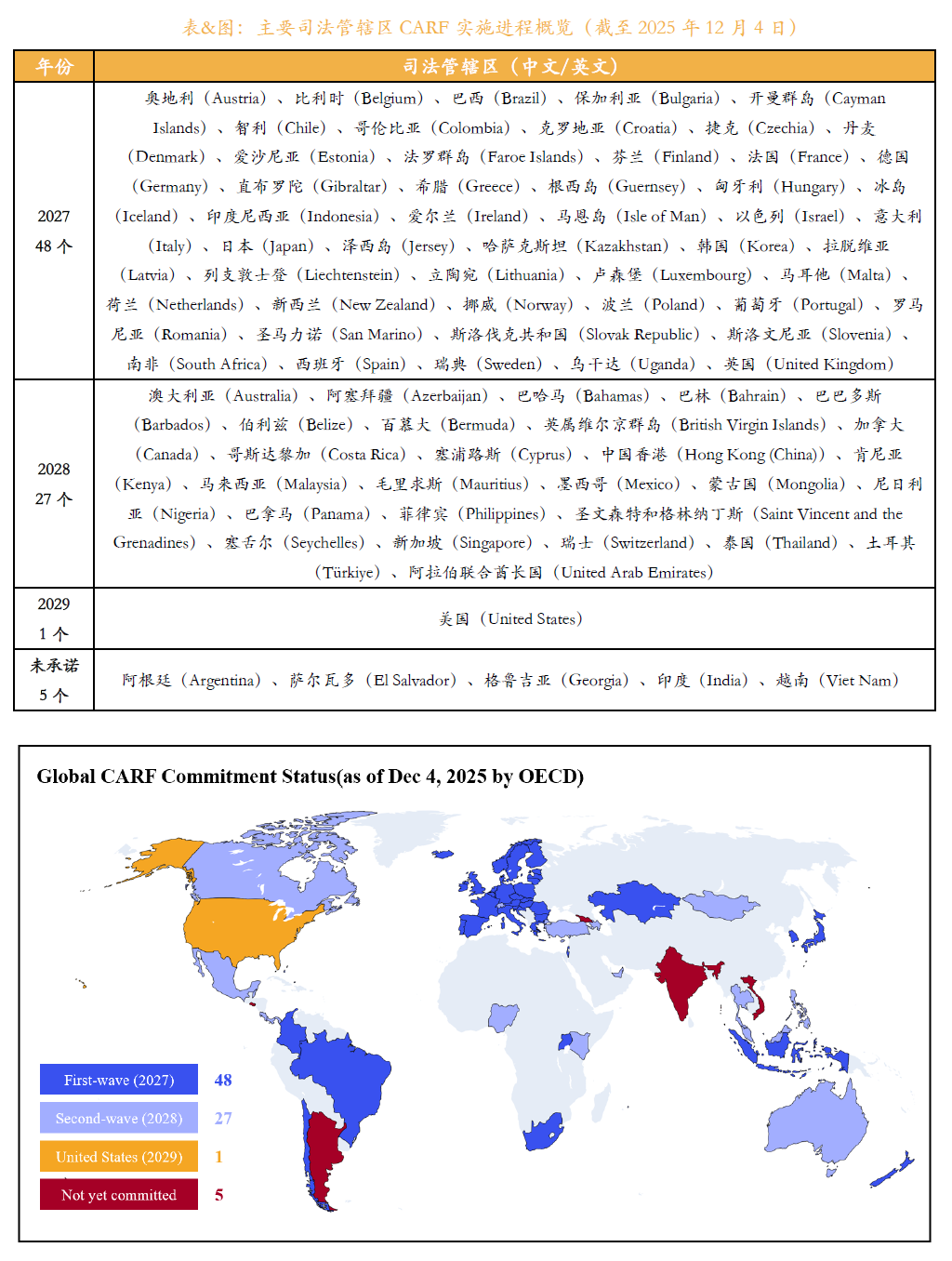

According to information released by the OECD Global Forum, as of the end of 2025, 76 countries and regions have committed to implementing CARF and will advance its implementation in batches.

The first group of jurisdictions plans to commence the first automatic information exchange in 2027, primarily including the UK and EU member states, etc.; the second group of jurisdictions plans to fully implement in 2028, including Singapore, the United Arab Emirates, and China Hong Kong, etc.

According to the institutional arrangement, the collection of relevant transaction data will commence one year in advance, starting from 2026, crypto-asset service providers will need to systematically organize reportable transaction information.

Figure 1: Overview of CARF Implementation Progress in Major Jurisdictions

China Hong Kong: Clear Participation and Timetable Advancement

In the aforementioned arrangement, China Hong Kong has clearly committed to implementing CARF and will advance related work according to the international timetable.

Hong Kong plans to start collecting crypto-asset transaction data from 2027 and commence automatic tax information exchange with other cooperating jurisdictions in 2028.

Crypto-asset service providers operating under Hong Kong's regulatory framework need to establish corresponding data compliance and reporting mechanisms, and relevant reportable transactions will be included in the cross-border information exchange process.

Mainland China: Not Yet Committed and Outside the Implementation Scope

In comparison, Mainland China has not yet made an implementation commitment to CARF.

As of the current stage, Mainland China is not included in any implementation batch of CARF, nor has it been listed by the OECD as a jurisdiction that is relevant but has not yet committed to participation.

Under the current regulatory framework, the mainland adopts a strict restrictive attitude towards cryptocurrency trading activities, and there are no legal crypto-asset service providers within the country that can be纳入 the CARF reporting system; therefore, it does not currently meet the institutional conditions for participating in CARF's regularized information exchange.

Future Possibilities and Realistic Judgment

It should be pointed out that Mainland China has fully implemented CRS since 2018 and has mature experience in financial account information exchange.

If future crypto-asset regulatory policies are adjusted, the mainland has the institutional and technical conditions to对接 CARF.

However, given the current policy environment, the possibility of Mainland China joining this framework around the 2027 launch of CARF and in the following years remains relatively low.

Domande pertinenti

QWhat is the CARF and what is its primary purpose?![]()

AThe CARF (Crypto-Asset Reporting Framework) is an international framework for the automatic exchange of tax-related information on crypto-assets. It targets crypto-asset service providers as the reporting entities, aiming to support tax authorities in various jurisdictions in obtaining information related to transactions involving their taxpayers.

QHow many jurisdictions have committed to implementing the CARF as of the end of 2025, and what is the implementation timeline?![]()

AAs of the end of 2025, 76 countries and regions have committed to implementing the CARF. The first group of jurisdictions, including the UK and EU member states, plan to commence the first automatic information exchange in 2027. The second group, which includes Singapore, the United Arab Emirates, and Hong Kong, China, is scheduled to fully implement the framework in 2028.

QWhat is the commitment and implementation plan of Hong Kong, China regarding the CARF?![]()

AHong Kong, China has explicitly committed to implementing the CARF. It plans to start collecting crypto-asset transaction data from 2027 and begin automatic exchange of tax information with other cooperating jurisdictions in 2028. Crypto-asset service providers operating under Hong Kong's regulatory framework will need to establish corresponding data compliance and reporting mechanisms.

QWhat is the current status of Mainland China's commitment to the CARF?![]()

AMainland China has not yet made a commitment to implement the CARF. It is not included in any of the implementation batches listed by the OECD and is not currently classified as a relevant jurisdiction that has yet to commit. Under its current regulatory framework, which imposes strict restrictions on crypto-asset activities, there are no legitimate crypto-asset service providers that could be incorporated into the CARF reporting system, making short-term participation unlikely.

QDoes Mainland China have the foundational experience to potentially join the CARF in the future?![]()

AYes, Mainland China has comprehensive experience in financial account information exchange, having fully implemented the CRS (Common Reporting Standard) since 2018. This provides it with the technical and institutional foundation to potentially adapt to the CARF requirements if its crypto-asset regulatory policy were to change in the future. However, given the current policy environment, the possibility of joining the CARF around its 2027 launch or in the subsequent few years remains relatively low.