Cardano founder Charles Hoskinson is urging the crypto industry to take a harder look at H.R. 3633, arguing that the market structure bill could lock future US token projects into securities status rather than provide the regulatory clarity its backers promise. His criticism goes beyond process: Hoskinson says the bill, as written, could protect legacy networks while making it far harder for new crypto projects to launch and grow inside the United States.

Cardano Founder Issues A Stark Warning

In a video published March 2, the Cardano founder framed the dispute partly as a direct response to Ripple CEO Brad Garlinghouse’s view that a flawed bill is still preferable to no bill. Hoskinson rejected that outright. “A bad bill is not better than no bill,” he said. “You start from a principles-based approach. You don’t make everything a security by default, and you upgrade modernized securities laws so that’s not so bad.”

His core objection is that the Clarity Act would treat newly launched digital assets as securities first, then require them to convince the SEC they qualify to “graduate” into commodity status once their networks are sufficiently decentralized. In Hoskinson’s reading, that framework would have captured XRP, Cardano and Ethereum at launch. The difference, he argued, is that older networks may ultimately be grandfathered in, while future projects would face a regulatory maze from day one.

Hoskinson repeatedly returned to the same question: what, in practice, stops the SEC from keeping a token classified as a security indefinitely? “If it starts as a security, what stops them from keeping it as a security forever?” he asked. “And are we really sure that we can trust that to rulemaking that has yet to happen by people who have yet to be appointed by agencies that spent the last four [expletive] years suing everybody and throwing everybody in prison?”

From there, he laid out a series of what he called “attack vectors” that an adversarial SEC could use in rulemaking. One involved procedural delays around filing completeness, where the agency could keep resetting the clock with deficiency notices. Another focused on the bill’s undefined treatment of “common control,” which he said could let regulators interpret open-source coordination itself as evidence of centralized management.

He also argued that proving decentralization could become impossible if issuers were required to identify beneficial owners across pseudonymous wallet systems or rely on compliance categories the SEC has not even created.

The broad point was that the bill may look workable in statute but become punitive in implementation. “A bad bill enshrines into law every single thing Gary Gensler was trying to do to the industry,” Hoskinson said. “A bad bill through rulemaking allows the SEC to arbitrarily and capriciously kill every new project in the United States. A bad bill exposes all DeFi developers to personal liability.”

He also argued the current political fight in Washington is not really about the bill’s structure at all. According to Hoskinson, the real holdup is stablecoin yield, not developer protections, DeFi coverage or the SEC-CFTC split. In his telling, that leaves the industry in a strange place: a bill marketed as market structure reform, but one that “doesn’t cover the core of what’s going on in the industry right now.”

Hoskinson’s preferred alternative is a principles-based rewrite that modernizes securities law itself, builds blockchain-native disclosure rails, explicitly protects developers and DeFi, and limits how much discretion regulators can exercise in later rulemaking. Otherwise, he warned, the practical result may be simple: established networks survive, while the next generation of US crypto projects builds offshore first and only tries to enter the American market years later.

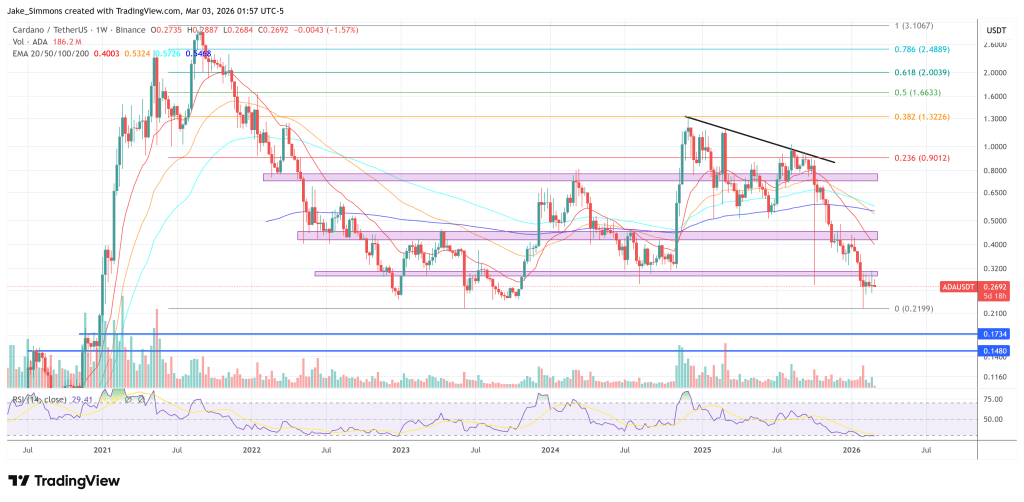

At press time, Cardano traded at $0.2692.