Author: FinTax

1 Introduction

Against the backdrop of the rapidly evolving global digital asset market, France, as a core member of the European Union, has initially established a crypto asset regulatory and taxation system that aligns with the EU's unified framework while retaining its own tax characteristics. From the enactment of the Action Plan for Business Growth and Transformation Law (PACTE Law) in 2019 to the full implementation of the EU's Markets in Crypto-Assets Regulation (MiCAR) in December 2024, France's institutional framework has evolved from pioneering national-level exploration to unified EU-wide standards. Concurrently, the advancement of the EU's Eighth Directive on Administrative Cooperation (DAC8) and the OECD's Crypto-Asset Reporting Framework (CARF) signals the dawn of the era of tax transparency for crypto assets. In this article, we梳理 (sort out) the existing French regulatory architecture, tax policies, and their convergence path with international standards.

2 Overview of France's Crypto Asset Regulatory and Tax Landscape

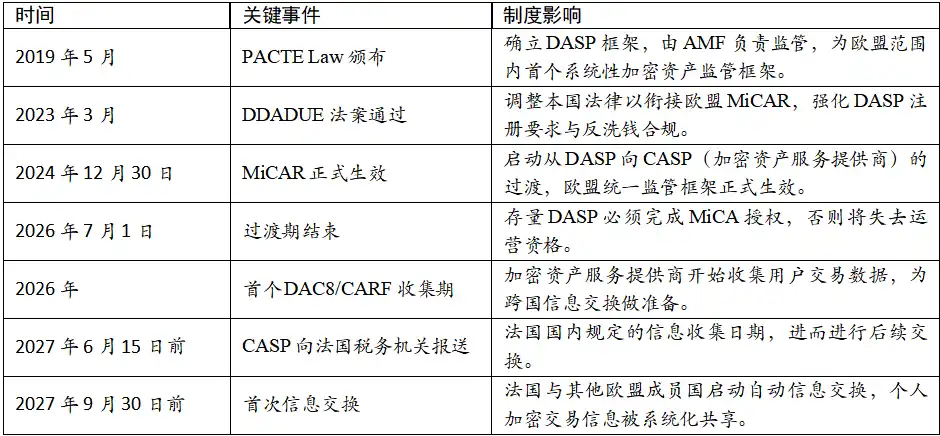

France's governance of crypto assets is characterized by regulation first and categorized taxation. On the regulatory front, France took the lead within the EU by establishing a registration system for Digital Asset Service Providers (DASPs), achieving compliant management of crypto service institutions. From December 30, 2024, the DASP framework officially transitions to the Crypto-Asset Service Provider (CASP) framework to comply with the EU's MiCAR requirements. This transition marks a shift in French crypto regulation from a voluntary registration system to a mandatory licensing system, imposing stricter capital, governance, and risk management requirements on service providers, custodians, and others.

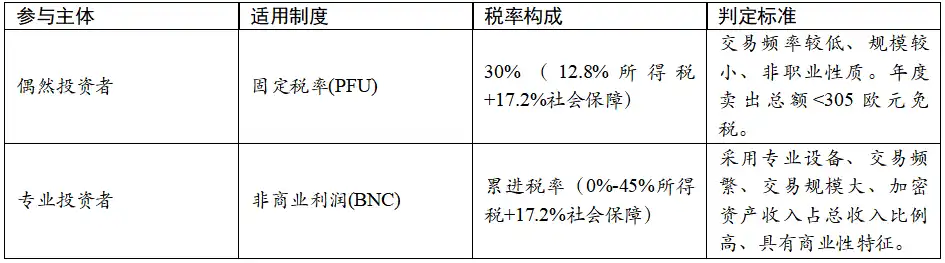

On the tax front, the French General Tax Directorate (DGFiP) categorizes participants based on the nature and frequency of their transactions, applying different tax calculation logics and rates. Occasional investors are subject to a flat tax rate of 30%, while professional investors are subject to a progressive tax rate of 0%-45%. Furthermore, different participants such as crypto mining enterprises, DeFi participants, NFT traders, and exchanges are subject to different tax regimes like Non-Commercial Profits (BNC) and Corporate Income Tax, reflecting their differing economic substance. This refined categorized taxation system acknowledges the diversity of crypto activities and provides relatively transparent tax expectations for different participants.

In the evolution of France's crypto tax system, the 2019 PACTE Law established the legal status of crypto assets. In 2023, the tax regime for professional investors was shifted from Industrial and Commercial Profits (BIC) to the Non-Commercial Profits framework. With the implementation of the DAC8/CARF framework, 2026 will be the first year for the automatic cross-border exchange of crypto transaction information, potentially ending the era of tax avoidance through the anonymity of crypto assets. A series of institutional changes reflect France's continuous adjustments in balancing innovation support and tax compliance. The table below outlines key timelines in French crypto asset regulation and taxation:

Table 1: Timeline of French Crypto Asset Regulation and Taxation

3 Current Regulatory System: The Institutional Leap from DASP to CASP

3.1 Core Regulatory Bodies and Division of Labor

Crypto asset regulation in France is carried out collaboratively by two main authorities: the Financial Markets Authority (AMF) and the Prudential Supervision and Resolution Authority (ACPR). The AMF is the core regulatory entity, responsible for the registration and authorization of digital asset service providers and the approval of Initial Coin Offerings (ICOs). Its regulatory focus is on market access, information disclosure, and investor protection. The ACPR, on the other hand, focuses on anti-money laundering (AML) and countering the financing of terrorism (CFT) compliance reviews, ensuring crypto asset transactions are not used for illegal purposes.

3.2 Legal Framework and Alignment with MiCAR

Before MiCAR came into effect, the French crypto market was primarily regulated under the PACTE Law. This law defined crypto assets as digital assets and required institutions providing services like custody and fiat currency exchange in France to register with the AMF. With the formal implementation of MiCAR on December 30, 2024, France is currently in a critical transition period from the DASP framework to the EU's unified CASP framework.

According to France's DDADUE law, DASP institutions registered with the AMF before December 30, 2024, can benefit from a transition period lasting until July 1, 2026, at the latest. During this period, these institutions can continue to operate within France, but if they need an EU passport to operate across the entire EU, they must apply for and obtain MiCA authorization in advance. CASPs under MiCAR must meet stricter capital requirements, governance standards, risk management, and customer protection measures.

3.3 International Cooperation Framework: DAC8/CARF and Tax Transparency

To further enhance the transparency of the crypto asset market, France is implementing the EU's DAC8 and the OECD's CARF. According to current plans, CASPs will need to start collecting user transaction data from 2026 and submit their first annual report to the French tax authorities by June 15, 2027.

This means that from 2027 onwards, an automatic information exchange mechanism will be activated between France and other EU member states, systematically sharing individuals' cross-border crypto transaction information with the respective tax authorities. This shift marks the end of anonymity for crypto asset transactions conducted through centralized platforms, moving tax compliance from reliance on taxpayer self-declaration to systematic reporting by CASPs and cross-border information sharing.

4 Crypto Asset Tax System: Categorized Taxation and Declaration Logic

4.1 Taxation Principles and Triggering Conditions

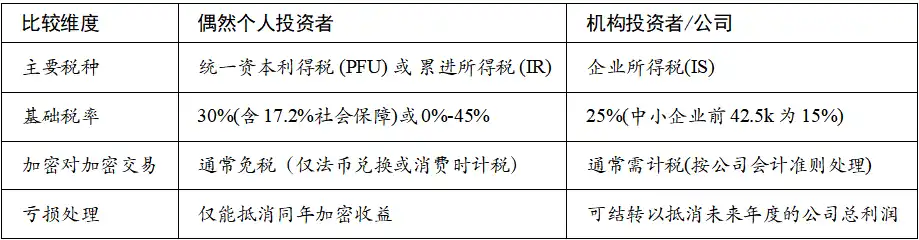

For individuals, France taxes crypto assets based on the principle that a taxable event is triggered only upon conversion into fiat currency or use for purchasing goods or services. That is, tax obligations arise only when crypto assets are sold for fiat currency or used to buy goods or services. Swaps between crypto assets (Crypto-to-Crypto) do not create an immediate tax obligation under the current system, a policy that greatly promotes the activity of the on-chain ecosystem.

For institutional investors and companies, France taxes crypto assets following the realization principle of corporate accounting standards. Crypto-to-Crypto transactions typically require recognizing profits and losses based on fair value changes, potentially creating immediate tax obligations even without conversion to fiat. This treatment is consistent with the accounting standards for traditional financial assets, requiring companies to value their held crypto assets at the end of each accounting period and include unrealized capital gains or losses in their current taxable income. Furthermore, capital losses for institutional investors can be carried forward to offset the company's total profits in future years, providing greater tax planning space for businesses.

4.2 Participant Classification and Tax Rate Structure

French tax law categorizes participants based on their nature and activity characteristics, with each category subject to different tax calculation rules. The following discusses occasional investors, professional investors and professional traders, crypto mining enterprises and pool operators, DeFi participants and liquidity providers, NFT traders, crypto exchanges and custodians, and institutional investors and fund managers.

4.2.1 Occasional Investors

Occasional investors are individual investors with low trading frequency, small scale, and non-professional nature. The French tax authorities use qualitative rather than quantitative criteria for determination, typically considering comprehensive factors such as: the complexity of transactions, tools used, transaction frequency, transaction scale, and its proportion in the taxpayer's total income.

Occasional investors are subject to the Flat-Rate Withholding Tax (PFU, Prélèvement Forfaitaire Unique). The rate is 30%, which includes 12.8% income tax and 17.2% social security contributions. Additionally, the portion of the annual sales total below €305 is exempt from tax. Losses generated from crypto trading within the same year can offset gains from the same year. Occasional investors calculate capital gains using the global cost proportion method (Portfolio Method). The specific formula is:

Net Capital Gain = Sale Price - (Total Acquisition Cost × Sale Price) / (Total Asset Market Value on Transaction Date)

This method allows taxpayers to consider the cost basis of the entire portfolio when calculating gains, rather than calculating transaction by transaction, which greatly simplifies the declaration process in practice. Meanwhile, occasional investors can choose to forgo the flat tax rate and instead be taxed according to the progressive income tax rate (0%-45%) plus 17.2% social security contributions. This option provides potential tax optimization space for low- and middle-income taxpayers.

4.2.2 Professional Investors and Professional Traders

Professional investors are individuals or entities with high trading frequency, large transaction size, crypto asset income constituting a high proportion of total income, use of professional equipment, and commercial characteristics. From January 1, 2023, the tax regime for professional investors has been shifted from Industrial and Commercial Profits (BIC) to the Non-Commercial Profits (BNC) framework.

Professional investors are subject to progressive income tax rates (0%-45%) plus 17.2% social security contributions. This means the tax burden increases with total income, reaching a maximum income tax rate of 45%. The taxable income for professional investors is the net capital gain, i.e., total gains minus total losses. Unlike occasional investors, professional investors can deduct losses within the same tax year, but losses cannot be carried forward to subsequent years.

Table 2: Comparison of Occasional and Professional Investors

The distinction between professional and occasional is based on qualitative criteria, not quantitative standards. The French tax authorities typically consider comprehensive factors such as the complexity of transactions, tools used, transaction frequency, transaction scale, and its proportion in the taxpayer's total income.

4.2.3 Crypto Mining Enterprises and Mining Pool Operators

Mining income for crypto mining enterprises is treated under Non-Commercial Profits (BNC) rules and must be included in annual total income at the market value at the time of receipt. According to DGFiP guidance issued in August 2019, mining income does not create Value Added Tax (VAT) obligations.

Mining income is recognized as income at the market price of the crypto asset on the day it is received by the miner. For example, if a miner receives 1 Bitcoin on a certain day, the market price of Bitcoin on that day should be used as taxable income. Mining enterprises can deduct costs directly related to mining activities, including but not limited to electricity costs, hardware equipment depreciation, maintenance costs, cooling system operating costs, etc. The deduction of these costs follows general business expense deduction principles.

According to DGFiP guidance, mining activity is not considered a VAT-taxable transaction in the absence of providing personalized services for a specific beneficiary. Therefore, miners are not required to pay VAT on the digital asset rewards received, nor can they claim VAT deduction rights. The tax treatment for individuals or entities participating in mining pools is the same as for independent miners, i.e., taxed under BNC rules. Mining pool operators, as intermediaries, need to provide participants with detailed records of profit distribution for accurate declaration.

Table 3: 2026 French BNC Net Income Progressive Tax Rate Table

4.2.4 Crypto Exchanges and Custodians

Crypto exchanges and custodians are subject to strict regulation in France. From December 30, 2024, these institutions need to transition from the DASP framework to the CASP framework to comply with the EU's MiCAR requirements.

As commercial entities, the income of crypto exchanges and custodians (including transaction fees, custody fees, interest, etc.) should be taxed according to French corporate income tax rules. The standard corporate income tax rate is 25% (since 2022). According to EU and French VAT rules, the exchange of crypto assets is generally considered a financial service and may be exempt from VAT. However, certain ancillary services (such as consulting, custody, etc.) may be subject to VAT.

CASPs need to meet stricter capital requirements, governance standards, risk management, and customer protection measures. However, we anticipate that these compliance costs may be deductible as business expenses.

4.2.5 Institutional Investors and Fund Managers

Capital gains from crypto asset transactions by institutional investors should be taxed according to French corporate income tax rules. Companies or funds registered in France must include gains generated from crypto asset transactions in their annual profits. Gains are treated as ordinary business income, with a standard tax rate of 25%. Depending on the specific structure of the fund (e.g., UCITS, AIF, etc.), the tax treatment may differ. Certain types of funds may enjoy special tax treatments; for institutions under specific accounting standards, a "Mark-to-Market" system may also apply, requiring the valuation and taxation of unrealized gains at the end of each accounting year.

Unlike the 30% flat tax (PFU) applicable to individual investors, France offers a preferential tax rate of 15% for the first €42,500 of profits for small and medium-sized enterprises (SMEs) with turnover below a certain threshold (usually €7,630,000) that meet the conditions, with the excess portion taxed at 25%.

Table 4: Comparison of Individual and Institutional Investors

Simultaneously, institutional investors engaging in cross-border crypto transactions need to consider the relevant countries' tax treaties and information exchange obligations under the CARF/DAC8 framework (see section 3.3 for details).

4.2.6 DeFi and NFT: Tax Categories Not Yet Clarified in French Tax Law

DeFi participants include all participants who earn returns by locking crypto assets in smart contracts, such as stakers, yield farming participants, and lending platform users. The legal characterization of Staking and Yield Farming is not yet clear in French tax law, lacking specific legal provisions or tax guidance. Based on existing tax guidance, since staking and yield farming contribute to the maintenance of the blockchain system, their returns might be taxed under BNC rules, requiring recognition at market value upon receipt, but this interpretation still needs further confirmation.

Until legally clarified, DeFi participants should keep detailed transaction records, including staking time, return amount, market price on the return date, etc., and consult professional tax advisors when filing.

There is significant uncertainty regarding the tax characterization of NFTs in France, lacking specific legal provisions or tax guidance. Depending on the specific legal characterization of the NFT, the tax rate could vary greatly: If characterized as a digital asset (like cryptocurrency), it would be subject to the 30% flat tax or progressive rates (0%-45%) depending on the participant category; If characterized as a work of art, it would be subject to a very favorable fixed rate of only 6.5% on the gross sales price. This simplified, very preferential rate in France is a special regime for specific movable property like artworks, aimed at encouraging art transactions.

Given the uncertainty of characterization, NFT traders should keep detailed transaction records, including purchase price, sale price, transaction date, specific characteristics of the NFT, etc., and consult professional tax advisors when filing tax returns to determine the most reasonable characterization scheme.

5 Summary and Outlook

France's institutional development in the crypto asset field reflects an approach that balances regulation and incentives. Through the implementation of MiCAR and the advancement of DAC8/CARF, France is transforming its pioneering regulatory advantage into a competitive edge within the EU. However, this process also marks the end of the era of anonymity in crypto asset trading, as the entire market gradually moves towards openness and transparency. To adapt to regulatory changes, individual investors and institutions have different response paths:

Individual investors should establish a well-maintained transaction ledger, using professional tax software to record each transaction. Beyond the €305 tax-free allowance, they should ensure accurate declaration to avoid compliance risks arising from undeclared foreign accounts. They should also monitor the progress of DAC8/CARF to understand the impact of automatic information exchange starting in 2027 in advance.

Crypto service institutions should accelerate the transition from DASP to CASP, focusing on strengthening internal AML/CFT audit processes to meet the stricter capital and operational requirements under MiCAR. Simultaneously, they should establish robust data collection and reporting systems in preparation for DAC8/CARF data collection starting in 2026. Furthermore, both institutions and individuals should consistently monitor policymakers' stance on the legal characterization of DeFi and NFTs, coordination with other EU member states, and the consistency and effectiveness of DAC8/CARF implementation.