Marvell delivered a seemingly brilliant report card with record revenue and a significant guidance raise.

After the U.S. market closed on May 27th, AI custom chip, optical communication, and data center interconnect leader Marvell released its Q1 FY2027 financial results and held an earnings call. The data center business continued its explosive growth, leading the company to once again significantly raise its full-year guidance. CEO Matt Murphy directly stated on the call, "Our data center business is on fire", and "orders are exceptionally strong."

Marvell's Q1 FY2027 revenue was $2.418 billion, up 28% year-over-year and 9% quarter-over-quarter, slightly exceeding analyst expectations of $2.41 billion. Non-GAAP earnings per share were $0.80, in line with analyst estimates. However, GAAP net profit was $34.5 million, a significant decline from $177.9 million in the same period last year, primarily due to one-time costs and non-cash amortization related to the acquisitions of Celestial AI and XConn.

The data center business contributed $1.83 billion in revenue, accounting for 76% of total revenue, up 27% year-over-year and 11% quarter-over-quarter.

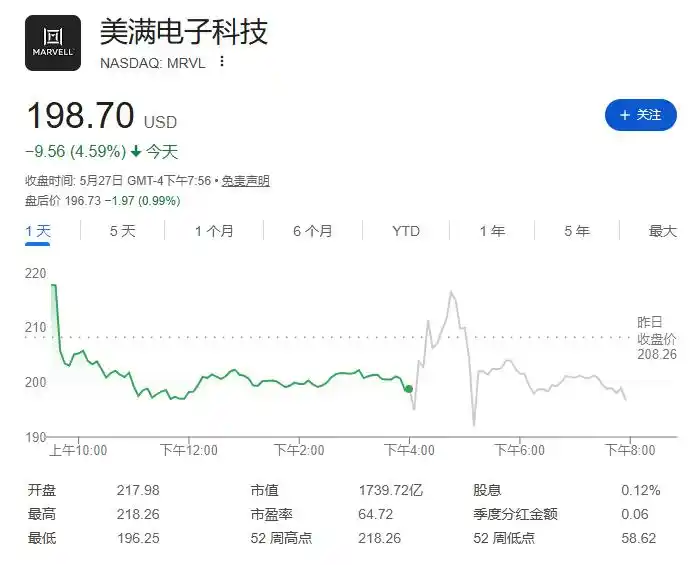

Following the earnings report and call, the company's stock price fell slightly by about 1%. Year-to-date, the stock had already more than doubled ahead of the earnings report. Against high expectations, merely "meeting expectations" may no longer be enough to impress the market.

01

"AI-Related Orders Are Exceptionally Strong," Marvell Raises Guidance Again

This marks Marvell raising its guidance for multiple consecutive quarters.

For the Q2 FY2027 guidance, the company expects revenue of approximately $2.7 billion (plus or minus 5%), representing year-over-year growth of about 35%, higher than the analyst consensus estimate of $2.6 billion. The non-GAAP EPS guidance range is $0.88 to $0.98, compared to the analyst consensus of $0.90.

For the full-year guidance, Marvell raised its FY2027 revenue expectation to approximately $11.5 billion, representing growth of about 40% year-over-year. Three months ago, the company's guidance was "approaching $11 billion."

More attention-grabbing is the outlook for FY2028. Marvell raised its FY2028 revenue target to approximately $16.5 billion, about $1.5 billion higher than the guidance provided last quarter, representing year-over-year growth of about 45%.

CEO Matt Murphy stated in the earnings release: "We are seeing exceptionally strong AI-related orders, and as a result, we are significantly raising our revenue expectations for Marvell's FY2027 and FY2028, showing substantial improvement compared to the guidance provided last quarter."

02

Data Center: Accounts for 76% of Revenue, Growth Still Accelerating

Q1 data center revenue was $1.83 billion, up 27% year-over-year and 11% quarter-over-quarter, accounting for 76% of total revenue.

Marvell's growth forecasts for this business are:

FY2026: +46% (already achieved)

FY2027: approximately +50%

FY2028: approximately +55%

Murphy stated:

The data center business is on fire, and we expect growth rates to accelerate this year and next, starting from an already high base.

03

Interconnect Business: Growth Rate from 30%→50%→70%, CEO Says "There's Room for Upside"

The AI Data Center Interconnect business is the largest segment within Marvell's data center portfolio, covering optical interconnect, DCI modules, coherent optics, and other product lines.

The expected annual growth rate for this business has been raised consecutively over the past few quarters: around 30% around September last year, later raised to 50%, and now raised again to over 70%.

When pressed by analysts, Murphy said directly:

I think there is a lot of potential for upside here. Our traditional DSP business will see a significant jump next year, the 1.6T product line has higher value content, DCI is accelerating, along with new businesses like retimers, AEC, and scale-up optics... This is the beginning of a major growth cycle for us.

Why has the interconnect business suddenly become so important? Murphy provided a clear logic:

Early generative AI primarily addressed compute and memory bottlenecks, with network interconnect being a secondary concern. However, with the deployment of more complex architectures like inference models and Mixture of Experts (MoE) models, the volume of data transmission within AI clusters has increased dramatically, significantly elevating the importance of network interconnect.

Some key numbers:

TIA and Driver Chips: Expected to surpass an annualized revenue run rate of $1 billion in the coming quarters.

DCI Module Business: Already shipping to all five major U.S. hyperscale cloud providers. Expected to surpass an annualized revenue run rate of $1 billion in FY2028, approximately double that of FY2026 (~$500 million).

Scale-up optics (NPO/CPO Optical Interconnect): Previously expected to be around $150 million; now raised, expected to exceed $300 million in FY2028.

04

Custom Chips (XPU): Doubling Next Year, Targeting Over $10 Billion by FY2029

Marvell's custom chip (Custom/XPU) business is another important growth line and a major focus for the market.

Current Progress:

FY2027 Custom Chip Revenue: Growth exceeding 20% year-over-year.

FY2028 Custom Chip Revenue: Expected to double year-over-year, higher than last quarter's expectation.

FY2029 Target: Exceed $10 billion (previous target was approximately $8 billion).

Analyst Vivek Arya (Bank of America Securities) pressed during the call: Does this mean FY2028 custom chip revenue will be over $4 billion, then jump to $10 billion in FY2029, implying a single-year incremental revenue of $5-6 billion?

Murphy's response was: Yes, you heard that correctly.

Three drivers for FY2028 custom chip growth:

Continued growth from existing flagship XPU projects.

More than ten XPU satellite projects (NIC, CXL, etc.) entering higher-volume production stages, with demand consistently exceeding expectations.

A new leading XPU project entering production — Murphy stated, "The project is progressing smoothly, and the full-year production plan is in place."

Murphy also revealed that while newly won design projects typically require about a two-year development cycle before contributing revenue, the significance of these projects lies in providing security for longer-term growth, which he referred to as "insurance policies."

05

Expanding Collaboration with NVIDIA, Three Key Directions Materializing

This quarter, Marvell announced an expanded strategic collaboration with NVIDIA. Murphy detailed three core directions on the call:

1. Optical Interconnect Collaboration: Marvell has long provided DSP, TIA, and drivers to NVIDIA. The two companies are now further collaborating on developing silicon photonics technology, considered a key enabling technology for scale-up networks.

2. NVLink Fusion Integration: Allows Marvell to build custom chips and network semiconductors that seamlessly interface with NVIDIA's infrastructure. Murphy stated this provides hyperscale cloud providers with greater flexibility to freely mix and match between custom chips and NVIDIA chips. "Marvell uniquely provides the bridge between these two architectures," creating new market opportunities for both companies.

3. AI-RAN: Marvell will enhance its Octeon base station processors to enable them to work directly in tandem with NVIDIA GPUs, running both 5G/6G wireless workloads and AI applications on the same hardware platform.

06

Supply Chain: Locking in Capacity Early, ~$1 Billion in Prepayments Planned This Year

Facing continuously climbing demand, supply chain management has become a critical variable.

CFO Willem Meintjes revealed on the call that the company plans to make approximately $1 billion in supplier prepayments during FY2027, with the first payments starting in Q2. These prepayments will be credited against future material purchases.

COO Chris Koopmans explained Marvell's supply chain strategy in response to analyst questions:

Everything related to AI has been supply-constrained from day one. Our approach is to build extremely close relationships with a small number of core suppliers, provide them with five-year demand forecasts, deliver on our promises every time, and back up our forecasts with action and prepayments.

Financially, Q1 operating cash flow reached a record $639 million. The company repurchased $200 million worth of stock in the quarter and paid $54 million in dividends. As of the end of Q1, total debt stood at $4.96 billion, with net debt/EBITDA at 0.32x.

This article is from the WeChat public account "Wall Street Insights Max," author: Long Yue