The markets, projects, currencies and other information, views and judgments mentioned in this report are for reference only and do not constitute any investment advice.

This week, BTC opened at $91,499.04 and closed at $90,872.01, a decrease of 0.68%, with an amplitude of 6.15%. Trading volume increased significantly compared to last week.

As mentioned in previous reports, BTC surged again towards $94,000 this week, driven by the continued improvement in Federal Reserve liquidity and the "soft landing" expectations fueled by US employment data meeting expectations.

However, with no hope of a rate cut in January, the risk appetite of on-market funds continues to deteriorate. After rising to the resistance level of $94,000, increased selling from BTC ETFs and long-term holders caused the rebound to fail, forcing a retreat back to the $90,000 line.

Currently, BTC and the crypto market remain in a dilemma where buying power supports but does not lift, while selling pressure intensifies on rallies. A renewal of buying sentiment, or an overall improvement in risk appetite, may be necessary for BTC to break through the $94,000 suppression and further expand the rebound space.

Technically, BTC is already in a favorable trend with rising retreat lows, and there are signs of stabilizing above the 60-day moving average. Barring negative external shocks, the price may break through $94,000 in the short term, challenging the 90-day moving average pointing to $95,000.

Policy, Macro Finance, and Economic Data

Considering the government shutdown, the monthly economic data released by the US this week was the first batch since data normalization, making it very important, but the final results did not exceed market expectations.

On January 8th, initial jobless claims data showed 208,000 applicants for the week, slightly below expectations and previous values. This is mildly positive for risk assets but aligns with "soft landing" expectations, indicating stronger economic resilience.

On January 9th, US seasonally adjusted non-farm payrolls for December were announced at 50,000, below the expected 60,000 and the previous value of 56,000, but the unemployment rate was only 4.4%, slightly below the expected 4.5%. Wage growth was 3.8%, higher than the 3.6% expected. These seemingly "conflicting" employment data suggest the crisis level in the job market is lower than expected, which caused the probability of a January rate cut shown by FedWatch to drop to single digits.

This week's data strengthened the consensus—the economy is achieving a soft landing, employment is cooling but not as bad. As the main battlefield for global capital, US stocks remained strong, with the S&P 500 and Dow Jones indices hitting new historical highs. The Nasdaq, questioned for excessive AI investment, also rose 1.88%, approaching its previous historical high. There are signs of capital shifting from tech stocks to consumer stocks, value stocks, and small to mid-cap stocks.

The 10-year US Treasury yield closed at 4.173%, with a real yield as high as 1.91%, which still puts enormous pressure on high-duration assets like tech stocks and BTC.

Crypto Market

Macro liquidity is improving but has not yet reached ample levels, and high-risk assets remain suppressed. If AI tech stocks are still under pressure, BTC is even more so.

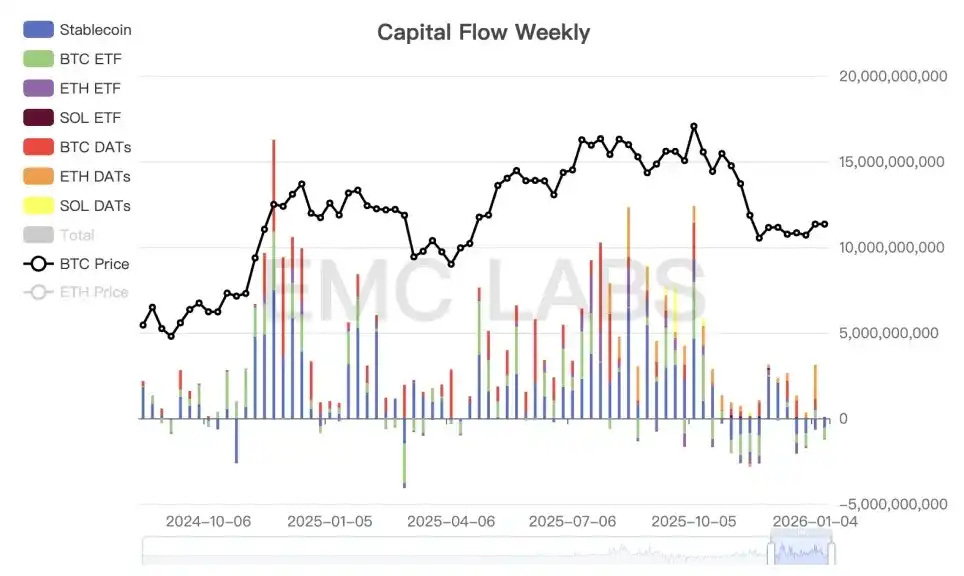

At the fund level, it can be seen that cyclical and short-term funds are still exiting on rallies, while long-term allocation funds are buying at low levels, currently entering a fragile balance.

This week, as the price rebounded to previous highs, a wave of selling reappeared before the release of major economic and employment data.

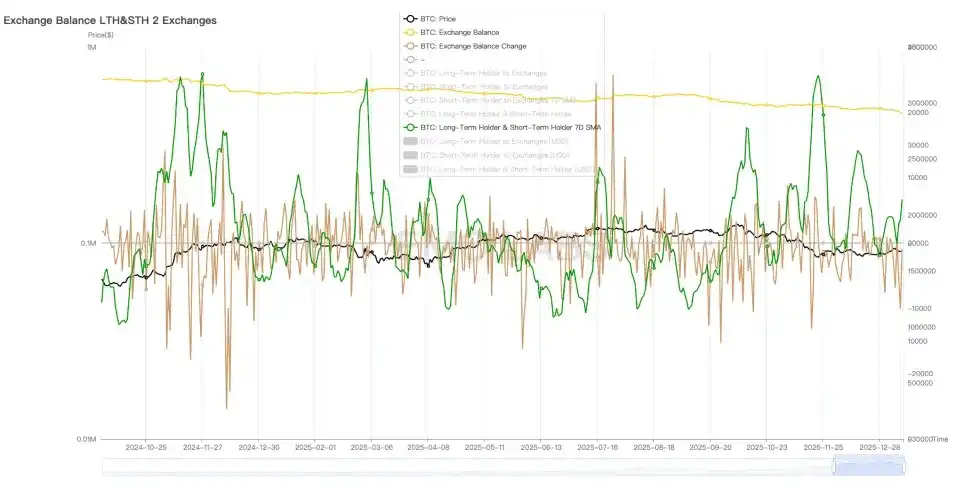

Centralized Exchange Long/Short Holder Selling Statistics (Daily)

This risk appetite-induced selling is not persistently destructive and is currently decreasing in scale. The continuous selling by long-term holders remains the biggest mid-term threat to the crypto market.

Long-term Holder Position Change Statistics (Daily)

The extent of continuous reduction by long-term holders weakened last week but is still ongoing, which also caused BTC to turn down after rebounding to $94,000.

The fund level also confirms this. The largest inflow occurred on January 5th, followed by continuous outflows, resulting in a net outflow for the week, with BTC ETF outflows at $647 million and stablecoin outflows at $539 million.

Crypto Market Fund Inflow/Outflow Statistics (Weekly)

Last week, centralized exchanges saw a net outflow of nearly 25,000 coins. The force supporting the market still comes from the "whale and shark group," whose holdings have been continuously increasing over the past week. However, this group currently adopts a "support but not lift" strategy, only accumulating at low levels and never creating upward buying pressure.

Cycle Metrics

According to eMerge Engine, the EMC BTC Cycle Metrics indicator is 0, entering the "downturn period" (bear market).

About Us

EMC Labs (Emergent Labs) was established in April 2023 by crypto asset investors and data scientists. Focused on blockchain industry research and Crypto secondary market investment, with core competencies in industry foresight, insight, and data mining, it is committed to participating in the booming blockchain industry through research and investment, promoting the well-being that blockchain and crypto assets bring to humanity.

For more information, please visit: https://www.emc.fund