Author:Connor Dempsey

Translation:Jiahuan, ChainCatcher

The crypto revolution did happen. It just unfolded nothing like what was originally expected.

When I first entered the space in 2017, the industry consensus was: this technology would change everything.

Government-issued fiat currency would be replaced by decentralized money. Blockchain would eliminate rent-seeking intermediaries standing in the middle of every transaction. Power would shift from corporations to users.

Almost none of that happened. But other things did.

To date, I've spent eight years across four crypto companies: @circle, @MessariCrypto, @coinbase, @crossmint.

I've watched this asset class balloon from under $10 billion to over $4 trillion, gone through several speculative bubbles, and weathered a near-systemic crash. What I've found is that what the industry actually ended up building is far more interesting than those early predictions.

Before starting my fifth job, I want to document these eight years. And talk about where I think it's headed next.

The False Prosperity (The 2017-18 Token Offering Frenzy)

Early 2017, I stumbled upon an explanation of Bitcoin in a book and got hooked. Soon after, I devoured every related book I could find and made a plan: go to Singapore and write a blog dedicated to documenting this new technology that fascinated me.

I didn't know it then, but this was right at the tail end of a massive speculative bubble around "Initial Coin Offerings." This model allowed anyone to raise funds online for an idea by selling digital tokens to investors.

Ethereum was the main stage for all of this.

In November 2017, I posted a layman's guide to Ethereum that blew up on Reddit. That was right at the peak of the bubble, which popped a month later.

Looking back now, that article feels more like a time capsule—capturing the optimism of the time and predicting a future that didn't arrive.

The Predictions Back Then

The core idea of the article: blockchains like Ethereum could be used to build a new type of consumer application.

Most consumer apps (Facebook, Uber, etc.) channel the value they create to large corporations and a handful of investors. These new apps would distribute the value they create among early participants (and early token investors).

The article imagined building a "decentralized Uber" on Ethereum. Early users and drivers would earn tokens for every completed ride, thus owning a piece of the network. This would more fairly reward the early believers who helped bootstrap the network.

On paper, it was a noble goal. But this decentralized revolution ended up taking a massive tumble.

What Actually Happened

A speculative frenzy reminiscent of the 2001 dot-com bubble.

Ethereum proved to be the most efficient crowdfunding platform ever. Over 3,000 token projects raised $22 billion from investors worldwide.

But just like 2001, the underlying technology was nowhere near ready for the outlandish valuations placed on it.

Worse, this model corrupted the normal incentive structure between investors and builders. Builders with just an idea could raise $10 million overnight.

Investors received tokens as their return, tokens that would only appreciate if the project succeeded. But the builders themselves also held tokens, which they could cash out to become wealthy from day one, removing their incentive to build a useful product.

Founders and early investors got rich. Inexperienced investors got rekt. While there were some genuine builders, the model unfortunately became a breeding ground for greed, fraud, and exploitation.

No different from every speculative bubble for the last few hundred years.

Building in the Rubble (Circle, 2018-19)

My wallet was thinning. Using the minor clout I'd built on Reddit, I landed an entry-level marketing role at Circle in early 2018.

Circle was four years old at the time. It had a suite of unprofitable consumer apps (investing, payments, trading) and a quiet over-the-counter (OTC) trading desk that quietly printed money and kept the lights on.

The next two years were the industry's hangover from the token craze. Most projects were abandoned. Most tokens went to zero. The vibe was terrible.

But it was during this time that the seeds for crypto's next renaissance were planted.

The focus this time wasn't consumer apps, but using the internet to reshape finance.

The Dollar and DeFi

Dollar-backed "stablecoins" started out to let traders easily switch between crypto positions. They peg their value to $1, backed by 1:1 reserves of cash and US Treasuries.

Tether's USDT took off first during the token craze, its dollar reserves swelling in bank accounts outside the US.

Although trading was the initial use case, the value of stablecoins for people who wanted access to dollars but couldn't access the traditional banking system was profound.

Like those evading capital controls. Chinese wealthy looking to diversify. Argentinians and Turks fleeing inflation.

In 2018, Circle, partnering with Coinbase, launched the compliant US version: USDC. Early use was still trading-heavy, but some began predicting that this new internet-native dollar could give dollar services, 24/7, to anyone with an internet connection.

Meanwhile, the few projects that survived the token era were almost exclusively financial.

If Ethereum could be used for fundraising, it could also be used to rebuild other foundational components of financial markets. Trading protocols (Uniswap), lending protocols (Aave, Compound). This later became known as "Decentralized Finance" or DeFi.

Stablecoins and DeFi were destined to merge. And what propelled them to the moon was a once-in-a-century pandemic.

The Wild West Reborn (Messari, 2019-2021)

At the end of 2019, I joined a 13-person data and research startup, Messari, as their first full-time marketer.

The company had a 4-person analyst team doing some of the most cutting-edge research on DeFi. Total Value Locked (TVL) in DeFi had grown to $665 million.

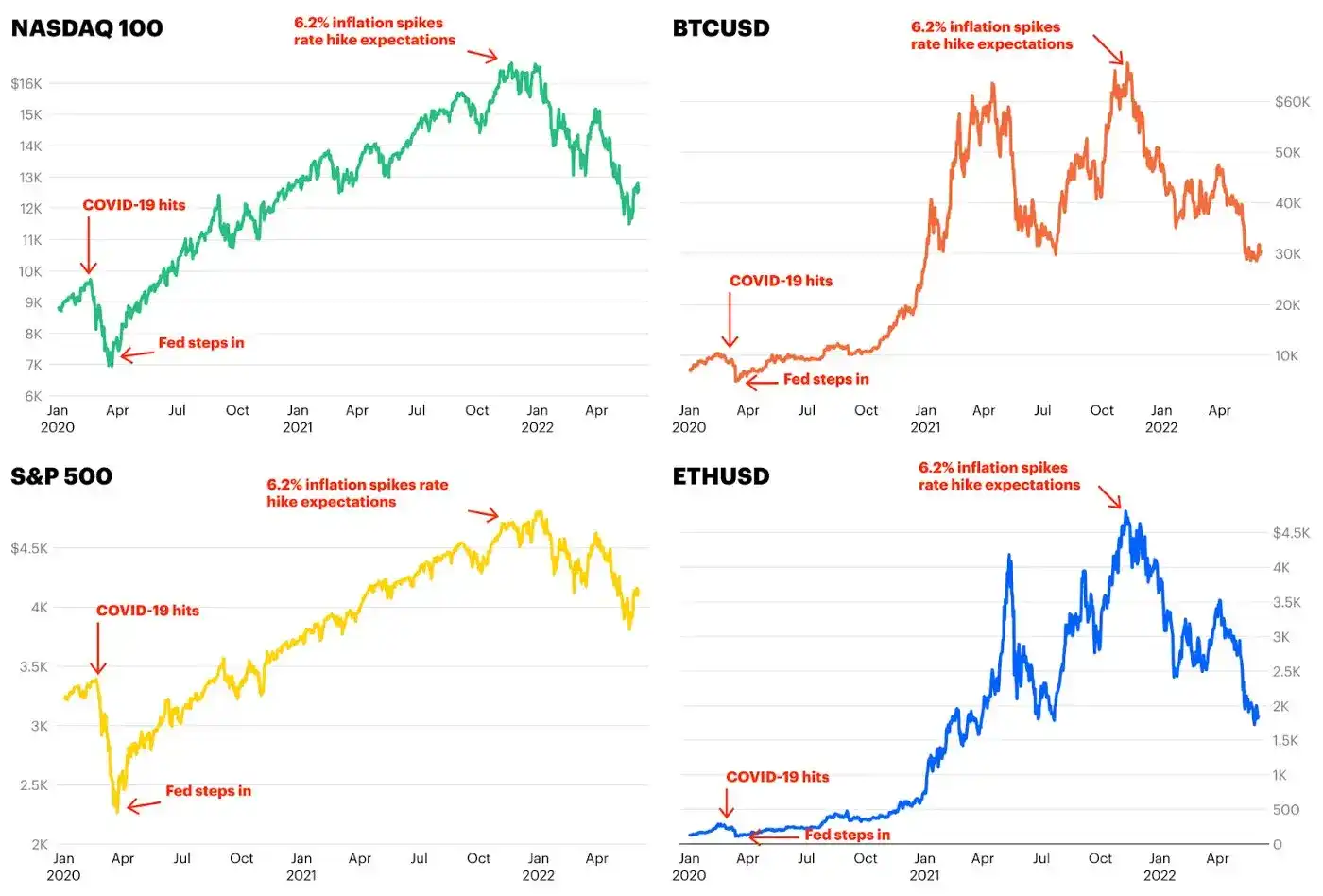

Then in early 2020, a mysterious virus emerged from China, threatening to shut down the global economy. All markets crashed.

The central banks' response: inject trillions of dollars into the global economy to prevent collapse. $9 trillion by the end of 2020 alone.

That money needed somewhere to go. Stuck at home, a tidal wave of capital flooded into Bitcoin, Ethereum, DeFi, and every speculative asset imaginable.

Bitcoin soared from under $4,000 to nearly $70,000, crossing a trillion dollars in market cap fueled by institutional investors, outperforming all other macro assets like gold.

Connor Dempsey Central banks continue printing, sending all markets to the moon, and simultaneously telling the world one thing: non-debaseable money has its place in this world.

#Bitcoin had the fastest leg, crossing $1T+ and outperforming all other macro assets.

These conditions also spawned the so-called "DeFi Summer," where the total value in DeFi protocols multiplied 250x, reaching $180 billion.

DeFi was supposed to rebuild traditional finance. But "DeFi Summer" felt more like a massive online game played by a group of mercenary traders, with tens of billions on the line.

The game was called yield farming. Anonymous developers launched new protocols, most for some reason themed around food.

YAM Finance, Spaghetti Money, SushiSwap. Traders deposited existing tokens (ETH, USDC, USDT) to earn newly minted tokens. $YAM, $SPAGHETTI, $SUSHI.

The whole process was both absurd and astonishing. A protocol would launch, and its newly minted token could hit a $1 billion market cap in days. Then early participants would sell, and the token would crash.

It was the true Wild West.

Like the token craze before it, DeFi Summer minted a generation of millionaires before imploding on itself.

It also minted a billionaire—Sam Bankman-Fried. A man who would become the epicenter of crypto's next disaster.

At the Peak (Coinbase, 2021)

In April 2021, Coinbase completed its $100 billion valuation IPO. Soon after, I was hired onto their corporate development and venture investing team.

My job was to sit alongside the people doing M&A and investing in early-stage crypto startups, write about industry themes, and work on the short-lived Coinbase podcast. It was one of the most interesting rooms I've ever been in, often making me feel like:

(Original image was the author at Coinbase HQ)

This was also the period when a second speculative bubble was forming—around digital artwork called NFTs.

If DeFi was for professional traders, NFTs were more accessible to regular people. They offered artists new ways to monetize online and showed promise for a native internet property rights standard.

But like early tokens and DeFi Summer, NFT speculation quickly went off the rails.

Digital pictures of cartoon monkeys, "punks," and penguins started selling for $1 million each. An artist named Beeple sold a collage for a ludicrous $69 million at Christie's.

Crypto culture was everywhere. Larry David mocked crypto skeptics in a Super Bowl ad. Sam Bankman-Fried's exchange, FTX, paid $135 million to put its name on the Miami Heat's arena.

Everyone was getting rich off tokens, NFTs, and stocks.

It was a re-run of the 2017 madness. Catalyzed by record money printing, the bubble was roughly four times the size of the previous one.

The Reckoning (2022)

But soon, the flywheel started coming apart.

The rate cuts, money printing, and stimulus that pushed all asset prices higher eventually leaked into consumer prices.

BTC, ETH, the Nasdaq, and the S&P 500 all peaked in late 2021. In that moment, everyone realized: inflation wasn't transitory, and central banks would have to reverse course, taking back every policy that sent stocks and crypto to all-time highs.

As interest rates rose and liquidity tightened, everyone holding overpriced assets started to get nervous.

Maybe monkey pictures aren't worth a million dollars. Maybe SUSHI shouldn't be worth $3 billion. Maybe Dogecoin isn't worth $90 billion.

Then, everything started to break.

If the token craze was most like the 2001 dot-com bust, what happened next was more like the 2008 financial crisis. A few toxic assets, combined with high leverage, nearly dragged down everything attached to them.

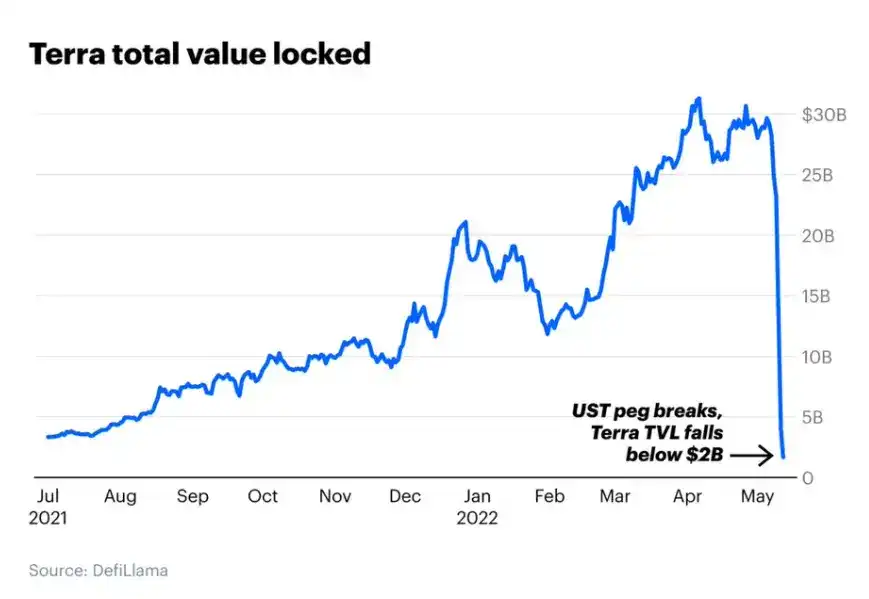

The first toxic asset was Terra's UST stablecoin.

Mainstream stablecoins (USDC, USDT) were simply backed by cash and Treasuries. UST used a complex algorithmic mechanism to maintain its peg. It worked in good markets. In a sell-off, it imploded.

$32 billion evaporated in days. People who thought they owned it woke up with nothing.

Next, a $10 billion hedge fund called Three Arrows Capital blew up—it was heavily invested in Terra and over-leveraged across the industry.

Three Arrows had borrowed heavily from crypto lending platforms Celsius and Voyager. These platforms took user deposits to lend out, chasing "safe" 8% yields. Three Arrows blew up, the platforms froze withdrawals and filed for bankruptcy, taking retail deposits down with them.

At Coinbase, we watched FTX and Sam Bankman-Fried step in, bailing out bankrupt lenders like BlockFi.

He was hailed as "the J.P. Morgan of crypto," the industry's white knight.

But the reality was, SBF and FTX were among the most exposed.

Remember FTX buying the Heat arena naming rights? That deal, and the entire SBF empire, was propped up by a token FTX printed out of thin air—FTT. SBF used FTT as collateral for huge loans. When FTT's price crashed, loans were called, and FTX went bankrupt.

Worst of all, FTX had been using customer deposits for investments and to plug holes. The once $32 billion-valued company collapsed in a week, with $8 billion of customer funds missing.

SBF violated the fundamental commandment of running an exchange: don't touch customer money.

This was crypto's Lehman moment.

Election and Casino (2023-25)

After the FTX collapse, SBF went to prison. Crypto markets fell from $3 trillion to under $1 trillion in 12 months.

Then, the Biden administration moved to kill the industry within the US.

The SEC, led by Gary Gensler, sued nearly every compliant company in the country for violating securities laws.

Coinbase, Kraken, Uniswap, Robinhood all received Wells notices. Companies that had spent years trying to operate legally became the SEC's primary targets.

Meanwhile, Elizabeth Warren quietly pressured banks to drop crypto clients, cutting off the industry's banking rails and pushing teams offshore.

This playbook had several unintended consequences.

First, launching anything in crypto with a business model (like DeFi) risked being labeled a security and sued into oblivion.

So the legally safest option became launching "memecoins," tokens with no stated utility.

On a platform called Pump.fun, millions of memecoins were launched. Iggy Azalea, Caitlyn Jenner, the Hawk Tuah girl—all launched their own memecoins. Without exception, all were disasters.

Crypto had a casino again, and it was bigger than the last. Over 6 million memecoins were launched. The sector peaked at $150 billion by the end of 2024, surpassing even the NFT bubble in dollar terms.

Second, the industry mobilized politically for the first time. Major companies poured tens of millions into pro-crypto PACs, launching organized lobbying efforts in Washington.

Third, Donald Trump saw an opportunity. He promised to fire Gensler, end banking hostility, and make the US the "crypto capital of the world," successfully turning the newly mobilized industry into a campaign asset. Many credit crypto voters with helping him win the election.

Then, three days before his inauguration, Trump launched a memecoin: $TRUMP. His wife did too: $MELANIA.

It was the most absurd thing I'd seen in eight years. Ironically, $TRUMP marked the top of the memecoin bubble—it sucked liquidity from everything else, followed by the entire memecoin market collapsing.

Going Institutional (Crossmint, 2025-26)

Aside from that awkward interlude, the industry's bet on Trump paid off.

The moment Trump looked poised to win, Bitcoin hit new highs. The market was pricing in the fact that the world's largest economy was shifting from hostility to friendliness.

Gensler resigned. The new SEC dropped its cases against US crypto companies. Banks were free to engage with the industry again.

Most importantly, the GENIUS Act passed in July 2025—the US's first major federal crypto legislation, establishing clear rules for stablecoins.

The signal from Washington to institutions was clear: crypto, especially stablecoins, was about to become big business.

Stablecoin companies like Bridge and BVNK were acquired by Stripe and Mastercard for valuations over $1 billion. Rain closed a ~$2 billion Series C. My former employer, Circle, the company behind USDC, IPO'd in June 2025, peaking at a $60 billion valuation.

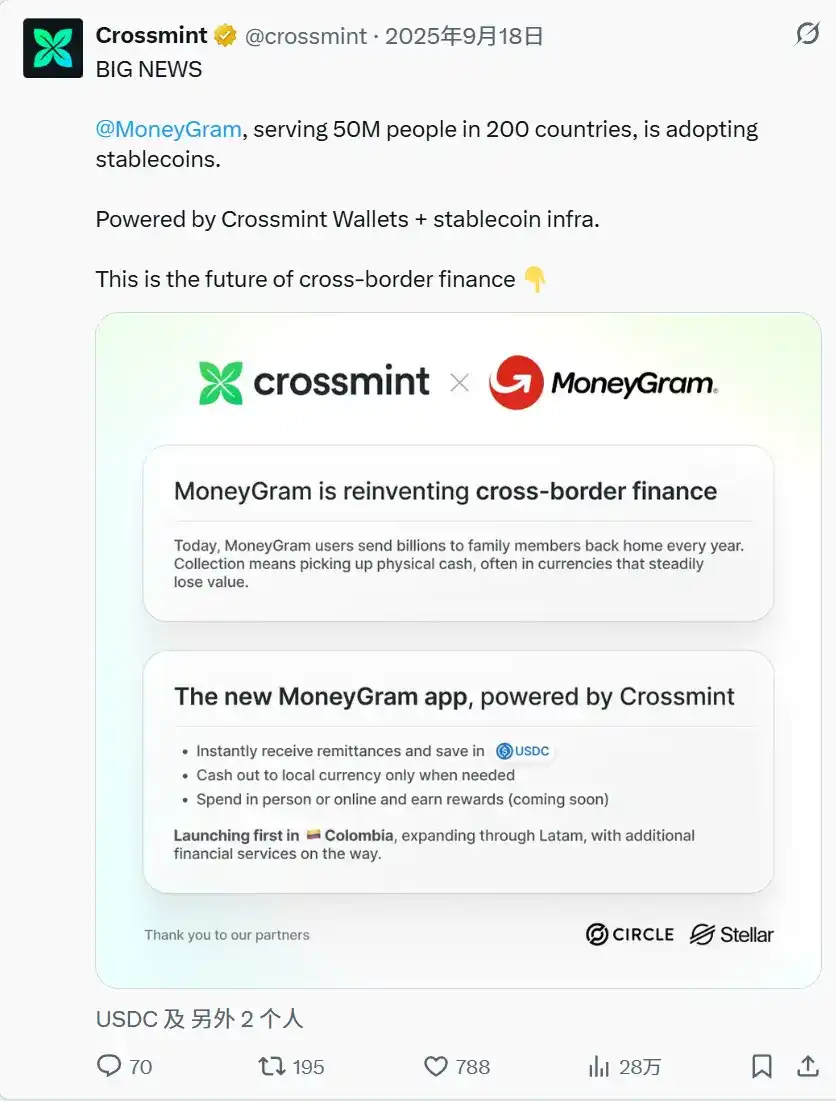

By this time, I was Head of Marketing at Crossmint. We had signed a deal with MoneyGram to help the century-old remittance giant move money across borders using stablecoins.

Crossmint@crossmint · 2025/9/18 Big news: @MoneyGram, serving 200 countries and 50 million users, is adopting stablecoins. Powered by Crossmint wallet + stablecoin infrastructure. This is the future of cross-border finance.

As the benefits of a "tokenized" dollar became clear, Wall Street began taking the tokenization of other assets seriously.

Even Larry Fink changed his tune. The man who once called Bitcoin an "index of money laundering" was now the BlackRock CEO managing $14 trillion, calling tokenization "the next generation for markets" and predicting all stocks, bonds, and asset classes would eventually run on a blockchain.

The Revolution We Didn't Predict (The Present)

Eight years after my Reddit post, we still don't have a decentralized Uber.

Blockchain hasn't eliminated all intermediaries, and fully decentralized money hasn't replaced government-issued fiat.

But I believe history will look back on this time as the messy, early days of a new internet-native financial system.

Each boom and bust polished the infrastructure. An infrastructure capable of reshaping global finance and delivering it to anyone with an internet connection.

Token offerings proved companies could raise money from anyone, anywhere in the world.

DeFi proved trading and lending could run purely on code (see @HyperliquidX and @pendle_fi).

NFTs laid the groundwork for native internet property rights.

Even the dumbest cycle—memecoins—proved the underlying networks could handle massive global transaction volume.

Swap those for non-fungible assets like stocks, bonds, real estate, add clear regulatory frameworks, and the migration of the entire financial system becomes inevitable.

Critics can still try to look away. But stablecoin data is the hardest piece to argue with.

With over $300 billion in stablecoin supply today, they settled $33 trillion in volume in 2025. Year-to-date, they've already settled over $40 trillion, on pace for $100 trillion.

Skeptics will say a lot of this is crypto trading and bot activity. They're not wrong. But the scale is undeniable, and the US government is now signaling where this is headed.

This is a critical, if slightly wonky, point: stablecoins are backed by US Treasuries, which are debt instruments the US government issues to finance itself.

Every stablecoin minted creates new demand for US debt, demand the US government desperately needs right now. For this reason, the Treasury Secretary has listed stablecoin growth as a US strategic priority:

Recent reports predict stablecoins could grow to a $3.7 trillion market by the end of the decade. With the GENIUS Act passed, that scenario is looking more likely. A thriving stablecoin ecosystem will drive private sector demand for US Treasuries...

Where to Next?

AI is changing everything, and crypto is no exception.

The marriage of crypto and AI has already begun. Millions of AI agents will soon be transacting in the real world. They'll use stablecoin-backed cards connected to merchants in 200+ countries. They'll also use crypto wallets and stablecoins to transact directly with each other.

Agents shopping for us, managing our finances, representing entire companies in transactions—this is all but guaranteed.

Looking further out, we'll see fully agent-driven business models with no humans in the loop. Imagine a hedge fund: it reads every SEC filing, builds its own models, trades on its own, with no analyst or portfolio manager in sight.

As this sci-fi future inches closer, crypto will go fully mainstream by integrating with the old system, not replacing it.

The backend will be crypto. The frontend will look exactly like what people already use. Most people won't even notice.

Institutions will replace decades-old legacy infrastructure. Startups will launch financial products globally at unprecedented speed and reach. The end result is a 24/7 financial system that works as well for someone in Nigeria as it does for someone in New York.

From there, a million more innovations will emerge.

Whether these predictions look as embarrassing in eight years as my old post does today, only time will tell.