Written by: Liam Akiba Wright

Compiled by: Chopper, Foresight News

TL;DR

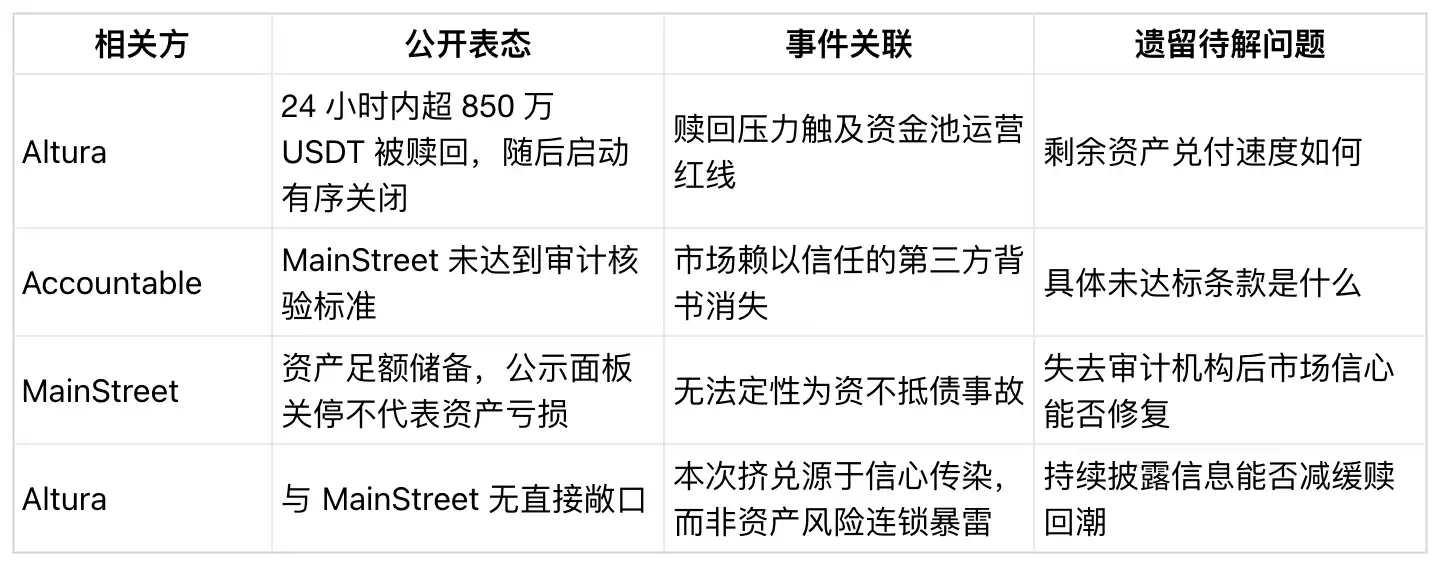

- Altura stated that users withdrew over 8.5 million USDT within 24 hours before it began an orderly vault shutdown.

- This run indicates that even if a stablecoin yield product has no direct asset link to disputes with other protocols, it can still face liquidity run pressure.

- The unresolved question is: Can the platform's remaining positions fulfill redemptions on time? Different investment strategies have significantly varying liquidation cycles.

The MainStreet reserve audit controversy has triggered a collapse in market confidence across the entire stablecoin yield sector, with Altura experiencing a single-day outflow exceeding 8.5 million USDT, leading the project team to decide to wind down its vaults in an orderly manner.

Altura CEO Ranveer Arora said the total user redemptions before the vault shutdown exceeded $8.5 million. Altura also stated it has no connection whatsoever to MainStreet or its underlying investment strategies. The core of this run is not asset risk contagion but a chain reaction triggered by collective loss of confidence in similar yield products.

The trigger was third-party audit firm Accountable terminating its cooperation with MainStreet, citing MainStreet's failure to meet audit verification standards. MainStreet publicly claimed its assets are fully reserved. However, the lack of third-party audit backing led to widespread skepticism among users holding similar yield products: If everyone redeems at once, can the fund pool fulfill redemptions quickly?

This is precisely the operational risk exposed by the Altura incident. From a user's perspective, the redemption action seems simple. However, the platform's assets are dispersed across different segments like exchange positions, private credit loans, and real-world asset (RWA) settlements, each with vastly different capital return cycles.

MainStreet later stated that shutting down the third-party reserve dashboard does not indicate asset losses or portfolio impairment.

Altura's own risk disclaimer is also crucial: the project explicitly stated it does not hold any MainStreet-related assets, and its HyperEVM lending pools, USDT/AVLT trading markets, and Ethereum lending positions were unaffected by this event.

But when users see an audit firm terminating cooperation with a stablecoin yield product, the focus shifts. It's no longer about whether a neighboring protocol has risk exposure, but whether all similar products can withstand a concentrated redemption wave.

Under a Concentrated Redemption Wave, Liquidity Becomes the Core Contradiction

Stablecoin users often focus only on the token itself; USDT in this event is also a core settlement medium in the crypto market. USDT's peg to $1 has remained stable, with a total market cap of approximately $186 billion and a 24-hour trading volume exceeding $51 billion.

This market scale has a dual impact: on one hand, the underlying liquidity for USDT is extremely ample, making it difficult for a single USDT-denominated fund pool to shake the overall stablecoin market; but on the other hand, the fund pool's own liquidity depends entirely on its capital allocation, asset placement channels, settlement rules, and whether counterparties can match users' expected redemption speed.

Altura's announcement also highlights this reality: funds held on exchanges can be liquidated more quickly compared to private credit or RWA investments; but exchange withdrawals are also subject to platform procedures, transfer channels, and market conditions. Private credit and RWA assets have fixed repayment cycles, where loan recovery, share redemption, and settlement windows cannot match DeFi users' demand for instant withdrawals.

The mismatch in capital return cycles across different assets means that even without actual asset losses, market sentiment can determine a product's survival. Users who redeem first can withdraw instantly, while those who redeem later must wait for asset maturity and liquidation. This expectation drives everyone to redeem early. The mere possibility of staged payouts is enough to accelerate a bank run.

The redemption scale in this event is significant. Altura's overall fund pool is valued at tens of millions of dollars, with the 8.5 million USDT single-day redemption representing a very high proportion. Large-scale concentrated withdrawals force an investment portfolio originally focused on yield generation to pivot towards liquidity-prioritized asset allocation.

Redemption Cycle: The Next Key Observation Metric

Looking at the entire stablecoin sector, this lesson cannot be ignored. The total stablecoin market cap is hundreds of billions, with daily trading volumes in the tens of billions. Various yield-generating stablecoin products promise principal stability plus yield, but most underlying investment strategies cannot be liquidated instantly.

Such products are operationally viable, but risks are concentrated at the operational level. Reserve proof disclosures, third-party audits, exchange holdings, private credit, RWA investments—the liquidity shortcomings of these links are only fully exposed when users abandon the pursuit of yield and simply want their cash back.

For Altura, the core observation point moving forward is the wind-down process: whether assets can be redeemed orderly, the frequency of platform disclosure updates, the scale of capital inflows at each stage, and whether it can prevent users from fire-selling long-term assets to exit hastily. Current information only suggests liquidity vulnerabilities; it cannot prove underlying asset losses at Altura.

For stablecoin yield products industry-wide, the test from this event is whether third-party audit backing can stabilize confidence during market volatility, rather than becoming a trigger for panic. Reserve dashboards and third-party verification are tools meant to reduce market uncertainty, but negative news about terminated audit cooperation spreads far faster than project clarifications.

This is the insight the Altura run offers the industry: in the DeFi fund pool sector, market confidence is by no means an irrelevant soft metric. It directly determines whether users are willing to deposit funds long-term, allowing sufficient liquidation cycles for the underlying investment strategies.