Written by: Taioo

Compiled by: Luffy, Foresight News

Currently, four major banks dominate the vast majority of institutional on-chain business with substantial operational scale, each following a significantly different strategic layout and development path.

JPMorgan Chase, Goldman Sachs, HSBC, and BNY Mellon have all made significant investments in tokenization infrastructure, yet they differ in their strengths, product philosophies, and market positioning. This article provides a horizontal comparison of these four institutions across four dimensions: transaction volume, breadth of product coverage, regulatory compliance framework, and underlying infrastructure model, aiming to clarify the real competitive landscape in the institutional tokenization race.

Evaluation Framework: Four Criteria

To assess institutional tokenization business, this article adopts a pragmatic evaluation standard: prioritizing practical implementation over conceptual promotion. The entire evaluation system consists of four core dimensions:

- Verifiable transaction volume processed by live production systems.

- Diversity of tokenized asset products across all categories.

- Completeness of regulatory licensing and compliance system construction.

- Underlying infrastructure model (self-built private network, participation in public blockchain networks, or a dual-track approach).

These dimensions correspond to different strategic advantages:

- Transaction Volume: Rewards institutions that commercialize their systems first and seize business opportunities.

- Product Breadth: Institutions capable of serving diverse institutional clients and covering the full spectrum of asset classes hold an advantage.

- Compliance Qualifications: Institutions that establish compliance frameworks ahead of the finalization of global regulatory details build first-mover barriers.

- Infrastructure Model: Directly reflects the institution's long-term strategic view on the future structure of the institutional blockchain market.

The following analysis breaks down each of the four banks according to this framework.

JPMorgan Chase's Kinexys: The Undisputed Leader in Transaction Volume

The most critical metric for evaluating institutional blockchain infrastructure is the scale of actual transactions processed, and JPMorgan Chase has left its peers far behind on this front.

Its Kinexys system has cumulatively cleared over $1 trillion in transactions, with core businesses focused on tokenized collateral management and intraday repo settlement.

$1 trillion is a key threshold. Exceeding this scale prompts regulators, counterparties, and institutional asset managers to view this financial infrastructure as a mature commercial tool rather than an experimental project.

JPMorgan's product strategy is deliberately refined. Kinexys focuses on three primary scenarios: JPM Coin cash settlement, collateral management, and repo clearing. The advantage of deepening a single vertical is extremely comprehensive functionality within that niche, rather than superficially covering a wide range of assets without depth.

JPMorgan's weakness lies in its closed, private network model. The Kinexys ecosystem is accessible only to JPMorgan's own institutional clients. Counterparties without an existing banking relationship with JPMorgan cannot access its clearing system. Although the transaction volume within the existing network is impressive, the overall addressable market space has a clear upper limit.

Goldman Sachs Digital Assets: Leader in Product Breadth

Among the four banks, Goldman Sachs' institutional blockchain business covers the widest array of product categories.

The Goldman Sachs Digital Asset Platform (GS DAP) has already completed tokenized bond issuances for multiple sovereign institutions and supranational organizations, including the European Investment Bank and the Hong Kong Monetary Authority. It has also launched tokenized money market funds for corporate treasury management and is a founding core member of the Canton Network, co-building a shared network with other major financial institutions.

This diversified product portfolio aligns with Goldman's client base: serving various capital market participants such as sovereign issuers, corporate treasury departments, and asset management firms. As an investment bank covering the broadest range of institutional capital clients, Goldman needs infrastructure that can support various types of tokenized asset businesses, rather than being limited to deepening a single application scenario.

The Canton Network builds a shared underlying layer for licensed financial institutions. As a founding member, Goldman Sachs can influence the network's development while benefiting from the liquidity pool brought by other institutional participants.

Compared to JPMorgan Chase, Goldman's shortcoming lies in publicly verified transaction volume. Although GS DAP has executed several real bond issuances, the overall clearing volume of its blockchain infrastructure has not been fully disclosed like JPMorgan's Kinexys.

HSBC's Orion: Frontrunner in Cross-Border Business and Sustainable Finance

Leveraging its Orion platform, HSBC has differentiated itself by focusing on cross-border tokenized securities issuance and sustainable financial products.

In November 2023, HSBC launched a tokenized gold product, "HSBC Gold Token," for institutional clients, backed by physical gold in London vaults. In March 2024, this product was extended to the Hong Kong retail market.

The Orion platform has repeatedly executed landmark tokenized bond projects. Representative deals include the Hong Kong Monetary Authority's digital green bonds issued in February 2024 and November 2025, with the latter being the world's largest digital bond issuance by size at the time.

HSBC's global geographical advantage is a natural barrier not possessed by New York or London-based domestic banks. Its long-established client resources in Asia, the Middle East, and emerging markets provide natural distribution channels for tokenized securities, precisely in regions where digital asset regulatory systems are rapidly maturing.

The HSBC Gold Token is a unique innovation, extending tokenized business from institutional clearing infrastructure to ordinary retail users.

Overall, HSBC's institutional blockchain business scale may not match JPMorgan's, and its product completeness may be less than Goldman's. However, its global network footprint creates a unique competitive moat in overseas markets where the other three banks have less penetration.

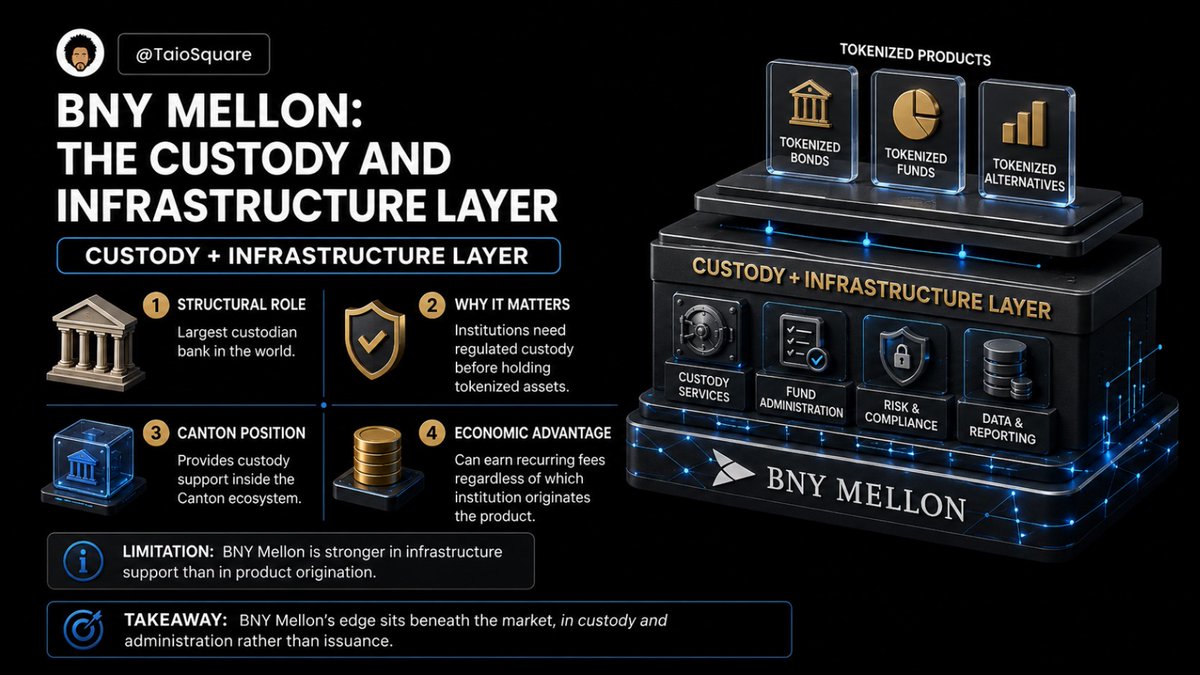

BNY Mellon: The Custodian and Underlying Infrastructure Provider

BNY Mellon's positioning in the institutional tokenization race is entirely different from the other three banks. The other three are primarily investment banks or large commercial banks with extensive institutional lending businesses, whereas BNY Mellon is primarily a custodian and asset servicer.

The world's largest custodian entering the digital asset custody space is highly significant for institutional RWA adoption. For institutional asset managers to hold tokenized assets in compliant accounts, robust underlying custody infrastructure is essential.

BNY Mellon participates in the Canton Network alongside Goldman Sachs, providing the underlying custody support for all transactions within the network. For example, when a Goldman client issues a tokenized bond via GS DAP and other Canton institutions participate in the subscription, BNY Mellon can provide custody services for the holdings. Regardless of which institution initiates a transaction, BNY Mellon can consistently earn stable custody fees.

BNY Mellon's weakness lies in its focus on underlying infrastructure support; it does not actively launch front-end products. It has not rolled out large-scale front-end businesses like tokenized bond issuances or tokenized money funds as Goldman has.

Its core competency resides in its custody and asset servicing foundation, a layer of service indispensable for all compliant institutional accounts holding tokenized products.

Conclusion

A horizontal comparison of the four banks yields the following results:

- Transaction Volume: JPMorgan Chase's Kinexys leads significantly, with verified total clearing volume exceeding $1 trillion. Goldman Sachs, HSBC, and BNY Mellon have not publicly disclosed complete transaction data on a similar scale.

- Product Breadth: Goldman Sachs leads by a wide margin, having executed sovereign tokenized bonds, tokenized money funds, and co-built the Canton Network. JPMorgan has fewer products but extreme depth in specific scenarios. HSBC uniquely offers a gold token, bridging the retail market. BNY Mellon focuses solely on underlying custody and does not issue front-end products.

- Regulatory Compliance: All four have proactively built compliance frameworks ahead of finalized global regulatory details. JPMorgan and Goldman Sachs have the deepest engagement with regulators across various jurisdictions. HSBC, rooted in Hong Kong, holds a geographical advantage in Asian digital asset regulation.

- Infrastructure Model: JPMorgan built a closed, private network. Goldman Sachs follows a dual-track approach: its own platform plus a shared network. HSBC and BNY Mellon primarily join shared networks and have not extensively built their own exclusive underlying networks. The shared network model reduces infrastructure investment costs but sacrifices the exclusive differentiation that a private network can offer.

The most crucial finding from this comparison is that the institutional tokenization market will not converge into a single infrastructure model. Instead, multiple development paths will coexist, each catering to different institutional client needs.

This parallel development harbors the risk of market fragmentation. If various institutional blockchain infrastructures operate as isolated islands with insufficient cross-network interoperability, rather than forming a unified, interconnected clearing system, the efficiency gains from blockchain technology will be confined within single-bank client ecosystems and fail to benefit the entire market.

The future level of industry fragmentation risk depends on two key variables: the progress in implementing interoperability standards between Canton and other institutional networks, and the speed at which unified regulatory frameworks for tokenized securities are perfected across countries.

My fundamental view is that over the next 5 to 10 years, major institutional networks will gradually enhance interoperability. There is a commercial incentive for institutions to interconnect liquidity pools, but the path toward comprehensive interoperability will be long and uncertain.

Each of the four institutions has forged a distinct strategic path: JPMorgan Chase holds the lead in transaction volume, Goldman Sachs boasts the most comprehensive product matrix, HSBC leverages its unique global positioning, and BNY Mellon dominates the underlying custody track. In the institutional tokenization race of the next decade, who will build the most enduring competitive moat? We shall wait and see.