Latin America's Payments Landscape Is Not What You Think It Is

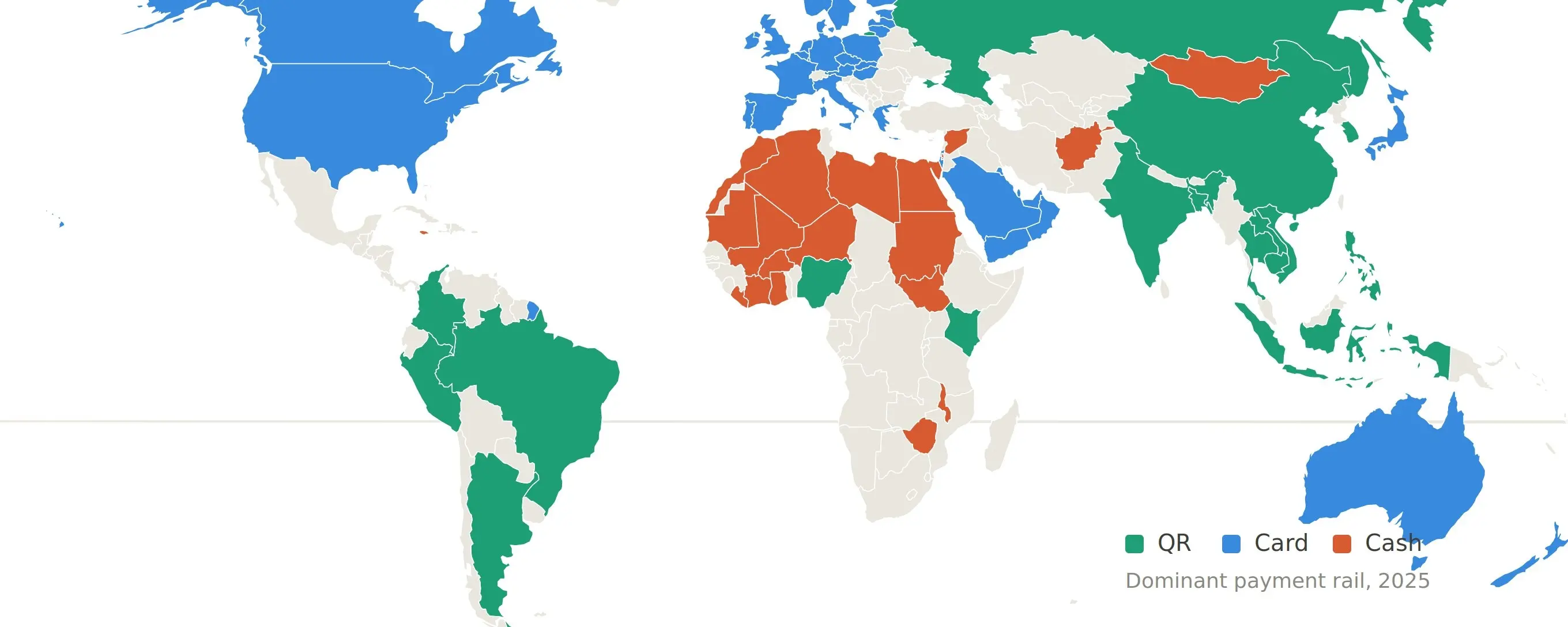

This report challenges common misconceptions about Latin America's payment landscape, based on over 500 hours of firsthand research. Key findings include: 1) Crypto card transaction volume primarily comes from high-net-worth individuals receiving USDT salaries, not retail spending. 2) QR code payments (e.g., Brazil's Pix, Argentina's Mercado Pago) are the dominant payment method across most emerging markets, not cards. 3) A major untapped opportunity lies in enabling cross-border interoperability between domestic instant payment systems. 4) Payment competition is shifting from customer acquisition to owning the settlement layer (e.g., acquiring banks). 5) Latin America is not a single market; Brazil, Mexico, Argentina, and smaller "forgotten five" countries (e.g., Guatemala, Honduras) have vastly different dynamics. 6) Stablecoin-to-fiat conversion margins are collapsing toward zero, pushing companies to build value-added services on top. 7) Future payment winners will be multi-country brands, not single-corridor specialists. 8) Marketing must target specific user segments (e.g., digital nomads, unbanked immigrants) with tailored messaging, not a generic "Brazilian" audience. 9) Contrary to perception, Latin American regulators are often ahead of the US in creating frameworks for digital assets and instant payments, with clear licensing deadlines. The core takeaway is that the region's payment rules are being rewritten, moving beyond cards and stablecoin arbitrage towards integrated, cross-border QR-based solutions.

链捕手13 min fa