The market is clearly shifting toward DeFi, and as a result, Layer 1s are rethinking how to stay ahead.

Consequently, it’s no surprise that most strategic partnerships are now centered around stablecoins. By acting as a bridge between TradFi and DeFi, they not only move capital on-chain more efficiently but also reduce friction and unlock access to key growth areas such as RWAs, AI, and NFTs.

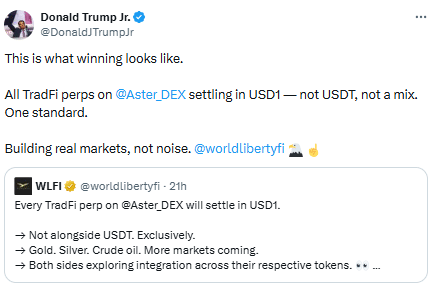

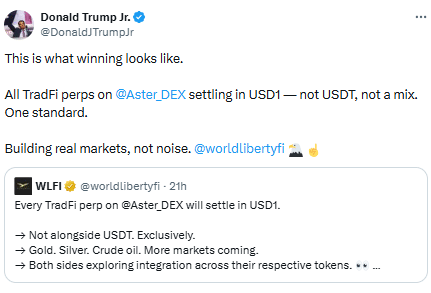

In this context, Aster’s [ASTER] partnership with WorldLibertyFinancial [WLFI] fits perfectly. Under this deal, WLFI’s native stablecoin, USD1, becomes the base layer for ASTER’s perpetual markets and RWA initiatives, further reinforcing the broader trend of connecting traditional finance more closely with DeFi via stablecoins.

Unsurprisingly, the market reacted quickly. The most buzzed-about response came from Donald Trump Jr. on X, calling the partnership a major “win” for both networks. That said, when we look at the technical positioning, it’s clear this move is about more than just strengthening fundamentals.

On the charts, both ASTER and WLFI have been impacted by ongoing macro FUD, closing near critical support levels that could soon be tested. At the same time, on the longer timeframe, these assets still have a significant way to go before reclaiming early-October price levels.

Naturally, the key question becomes, can this partnership actually drive meaningful price gains? That’s especially relevant when you consider that other DEX tokens like Hyperliquid [HYPE] have managed to stay relatively bullish despite the same macro headwinds.

ASTER bets on USD1 to reclaim ground

When you think of stablecoins, USDT usually comes to mind first.

That said, its technical setup doesn’t always tell the full story. So far this year, USDT’s market cap has only grown about 1.6%. Considering that this period overlaps with roughly a 20% correction across the broader crypto market, it’s clear that USDT flows still influence wider price action.

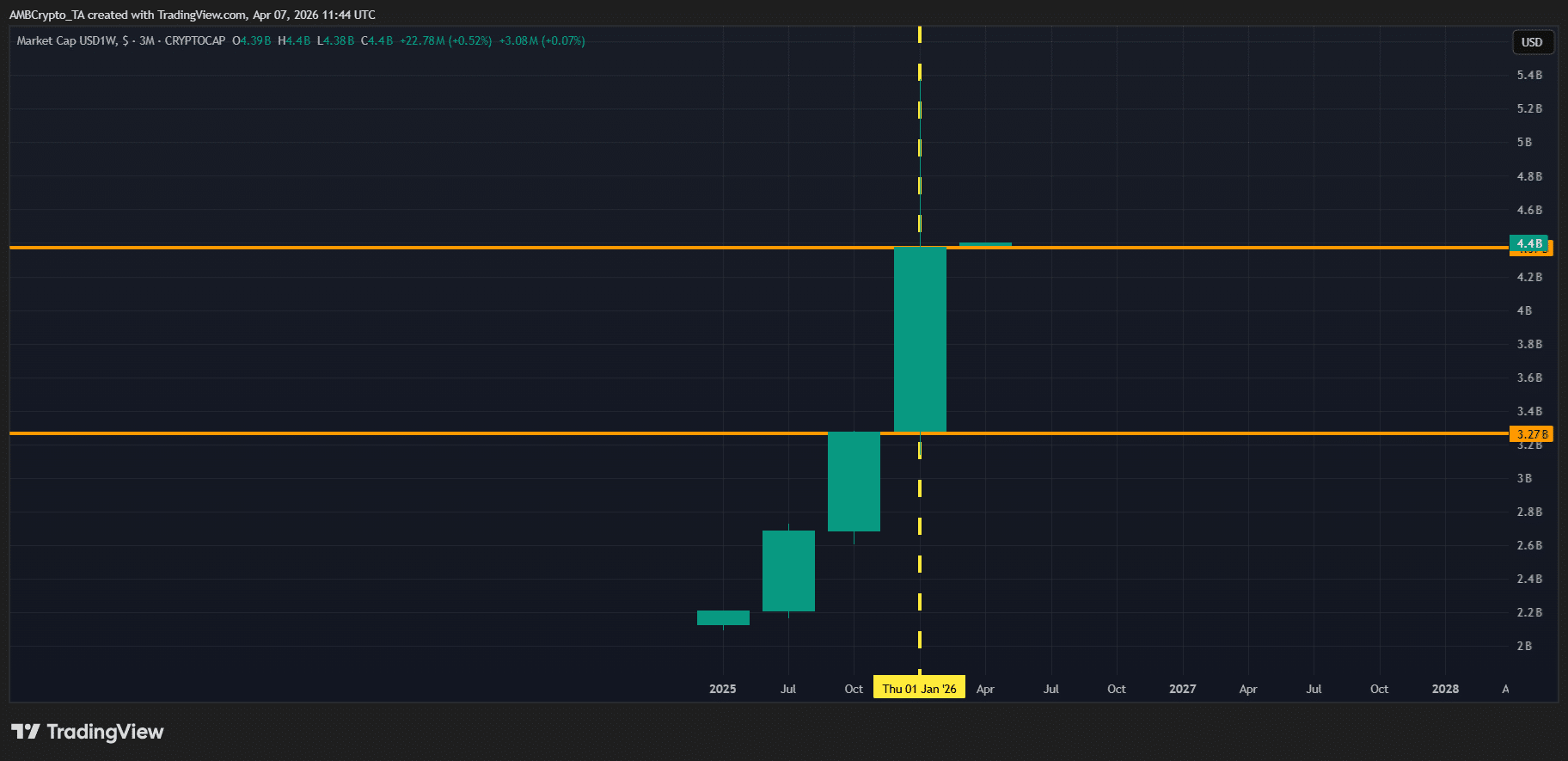

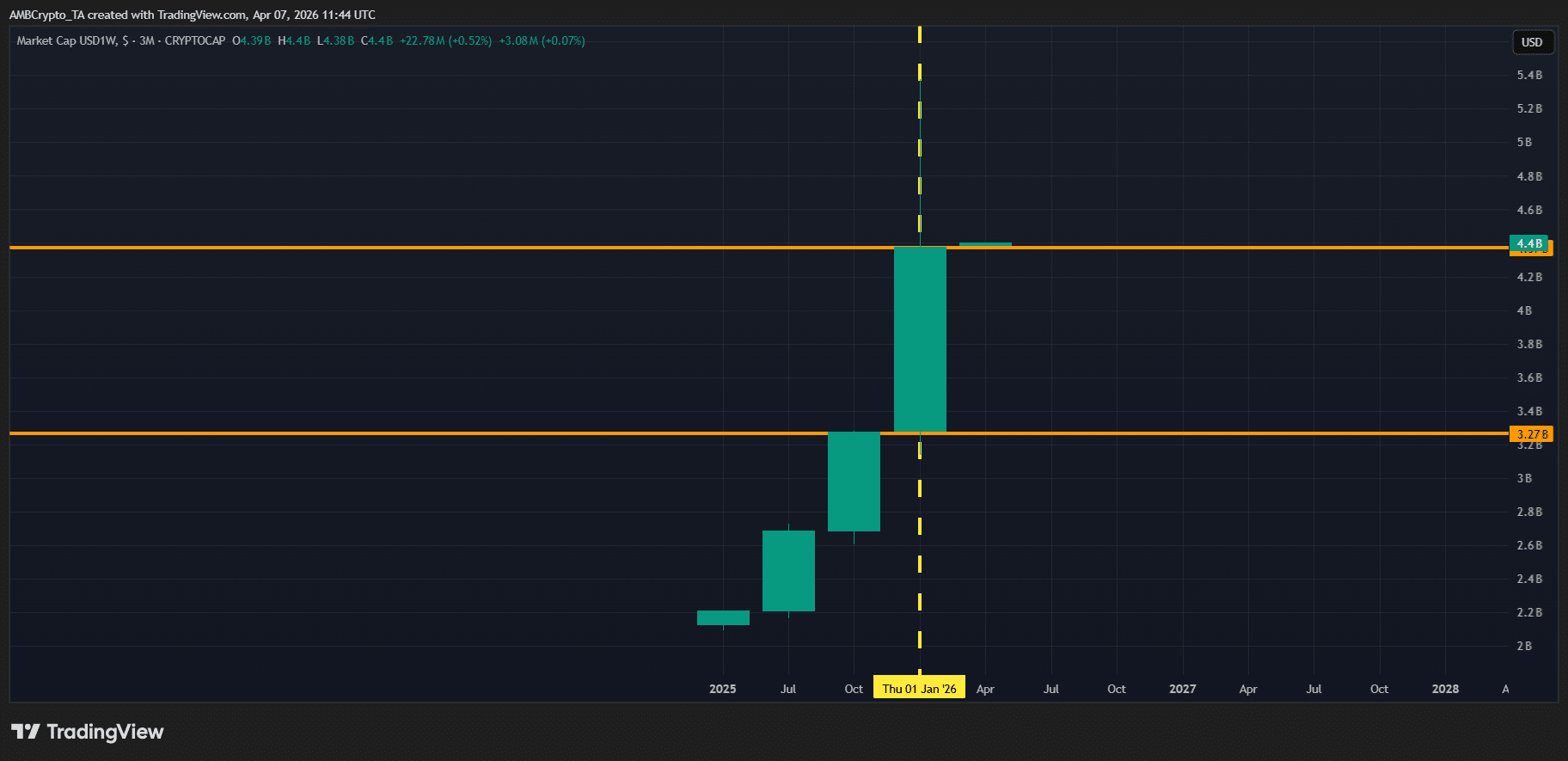

But capital isn’t just chasing speculation anymore. The RWA market, for example, has grown 35% this year, showing that money is moving into more structured, real-world assets. In this context, USD1’s 34.3% jump in market cap highlights how well-positioned stablecoins are driving real growth, making the ASTER-WLFI partnership a clearly strategic play.

Meanwhile, a similar divergence is visible in perpetual volume, which has cooled overall. Yet, on a chain-by-chain basis, Hyperliquid still dominates, reporting $620 billion in perp volume in Q1. Oil trading, in particular, has been a key driver, keeping Hyperliquid firmly in the lead even as broader market activity slows.

By comparison, ASTER posted $318 billion over the same period. Technically, that’s almost half of Hyperliquid’s volume. The impact shows in price action too, with HYPE ending Q1 up 43%, while ASTER slipped 3.32%. That said, the WLFI partnership puts ASTER in a position to strengthen its liquidity, potentially improving its competitiveness in the DEX perpetual market.

The main catalyst? USD1. Serving as the base layer for ASTER’s perpetual markets and RWA initiatives, it could be the lever that helps ASTER close the gap with Hyperliquid, creating a stronger presence across both trading and real-world asset markets.

Final Summary

- USD1 now serves as the base layer for ASTER’s perpetual markets and RWA initiatives, strengthening liquidity.

- While HYPE dominates perp volume, ASTER’s USD1 integration positions it to narrow the gap and expand its presence in both trading and real-world asset markets.