Крупнейший внешний акционер майнинговой компании Cipher Mining, связанный с генеральным директором Bitfury Валерием Вавиловым, продал 5% акций на фоне рекордного роста котировок. С июля по середину сентября компании V3 Holding и Bitfury Top HoldCo реализовали более 10 млн акций по ценам от $5 до $12,65 за штуку.

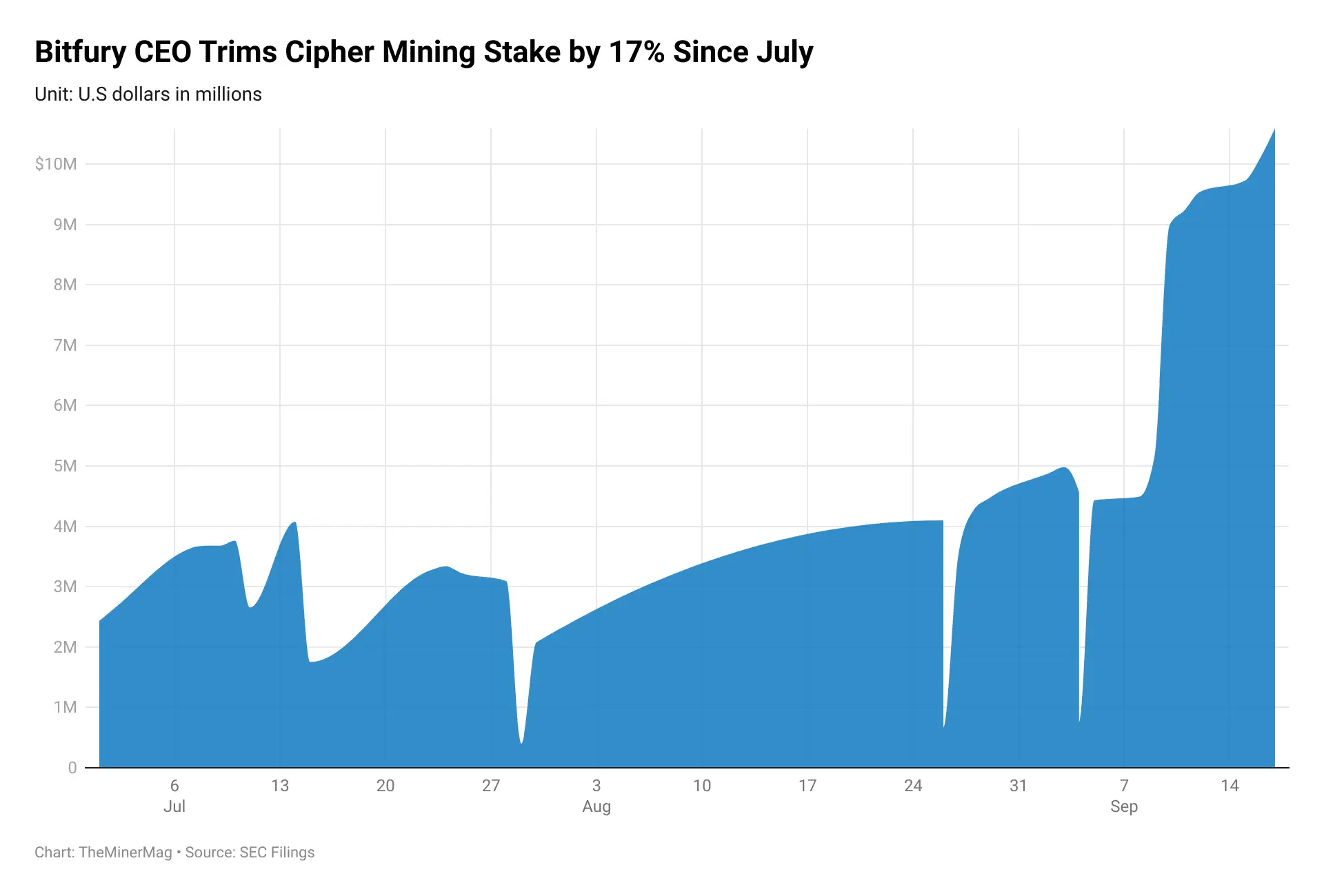

Согласно документам, поданным по Приложению 13D, компания V3 Holding, полностью контролируемая Вавиловым, начала сокращение своей доли в Cipher в начале июля. 8 и 9 июля было продано 1,2 млн акций по средней цене $6,13 за акцию, что составило 2,6% от прямого пакета на тот момент.

В заявлении продажи описываются как часть «дисциплинированной долгосрочной стратегии» по диверсификации личных инвестиций и финансированию благотворительных инициатив. Компания взяла обязательство не превышать 5% от среднего дневного объема торгов Cipher в любой день.

С конца июля до середины сентября V3 и Bitfury Top HoldCo ускорили продажи, реализуя ежедневные пакеты по 500-900 тыс. акций. За этот период стоимость акций Cipher выросла более чем вдвое.

Совокупная доля бенефициарного владения V3 в Cipher сократилась с 25,7% (95,4 млн акций) на 8 июля до 20,2% (79,4 млн акций) на 15 сентября. Bitfury Top HoldCo и ее дочерняя компания Bitfury Holding сохраняют владение более чем 48 млн акций Cipher.

Вавилов, занимающий пост генерального директора и председателя совета директоров Bitfury, остается крупнейшим внешним акционером Cipher. Bitfury, ранее один из ведущих производителей майнингового оборудования, в последние годы сфокусировалась на развитии центров обработки данных и блокчейн-сервисов, сохраняя стратегическую долю в Cipher после ее выхода на биржу через SPAC в 2021 году.

В документах подчеркивается, что продажи не отражают снижение доверия к компании, а Вавилов и V3 сохраняют позитивный взгляд на долгосрочные перспективы роста Cipher. Рост акций компании связан с быстрым расширением майнинговых мощностей и стабильным увеличением реализованной вычислительной мощности на новом объекте Black Pearl.