在币圈玩家们关注着川普的健康疑云风波,等待着可能的博弈机会时,一个叫 $CARDS 的币以从 9 月 2 日至今最高上涨近 10 倍,市值一度突破 4 亿美元的表现将玩家们的目光吸引。

$CARDS,是 Solana 上实体宝可梦卡片交易平台 Collector Crypt 的代币。Collector Crypt 在 2023 年 2 月宣布完成种子轮融资,具体金额未披露,由 GSR、Big Brain Holdings、FunFair Ventures、Genesis Block Ventures、Master Ventures Investment Management、StarLaunch 和 Telos 参投。

尽管完成种子轮融资的时间已经是 2 年半前,但 $CARDS 的预售在上周才开启。5% 的代币总量(1 亿枚 $CARDS)分配给了预售,最终共募集了 16500 枚 SOL(约 350 万美元),参与预售的人数为 718 人。

此外,分配给社区的占总量 20% 代币中,有 2.5% 和预售代币同时开放领取。而根据官方发布的代币经济学,如果项目方持有的代币不计入初始流通(项目方声称目前没有出售计划),目前 $CARDS 的流通量大约为 2.12 亿枚。

按市价计算,种子轮前、种子轮以及顾问在 TGE 时解锁的代币目前价值约 167 万美元

官方表示目前没有出售代币的计划

其实,如果从项目本身做的事情来看,Collector Crypt 所做的宝可梦卡牌链上交易并没有那么新颖。

Polygon 上的 Courtyard.io 也已经运行了 2 年多的时间。在上个月,Courtyard 的月销售额刚刚创下约 7843 万美元的新高。自今年 2 月以来,Courtyard 的月销售额均超过 4000 万美元。

在今年的快速发展可能是 Courtyard 收获大额融资的原因。7 月 28 日,据《财富》报道,Courtyard 完成 3000 万美元 A 轮融资,Forerunner Ventures 领投,NEA 和 Y Combinator 等现有投资者跟投。

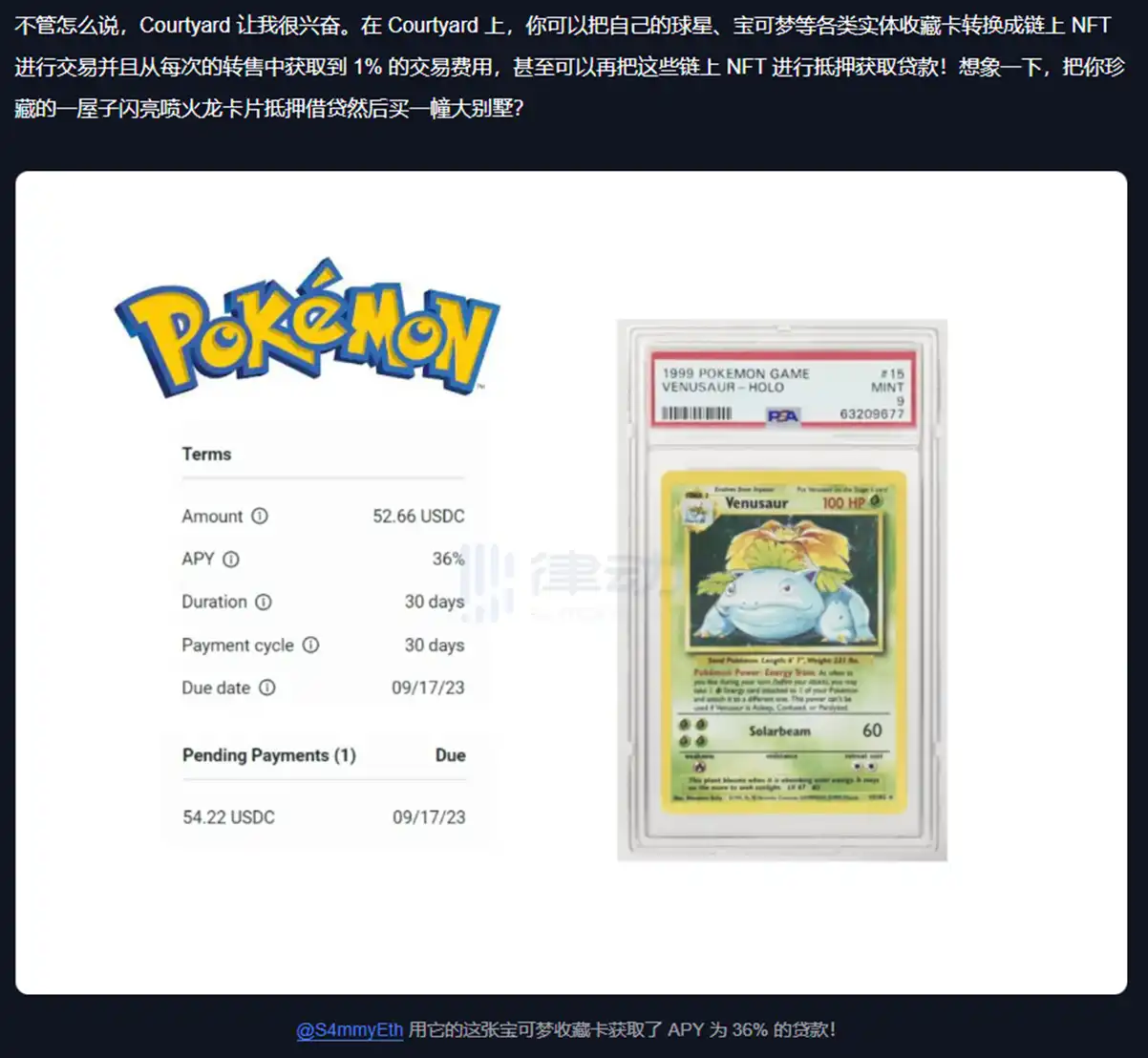

2023 年 8 月,Courtyard 刚刚引起少数 NFT 玩家关注时,我们曾对 Courtyard 进行了报导。在当时,已经有 NFT 玩家通过 Courtyard 获取宝可梦卡片并在链上进行抵押借贷。

在 Collector Crypt 和 Courtyard 之外,做类似业务的加密项目还有 Beezie、Drip、Emporium 以及 phygitals。

但是,Collector Crypt 在这些项目中是唯一一个发了币的,这使 $CARDS 占到了先机。当然了 Collector Crypt 自身也相当能打,上个月,其月交易量达到了约 4400 万美元,和 Courtyard 的差距并不算太大。

您可能会疑惑,在链上交易宝可梦卡片,真的有那么多真实的需求吗?

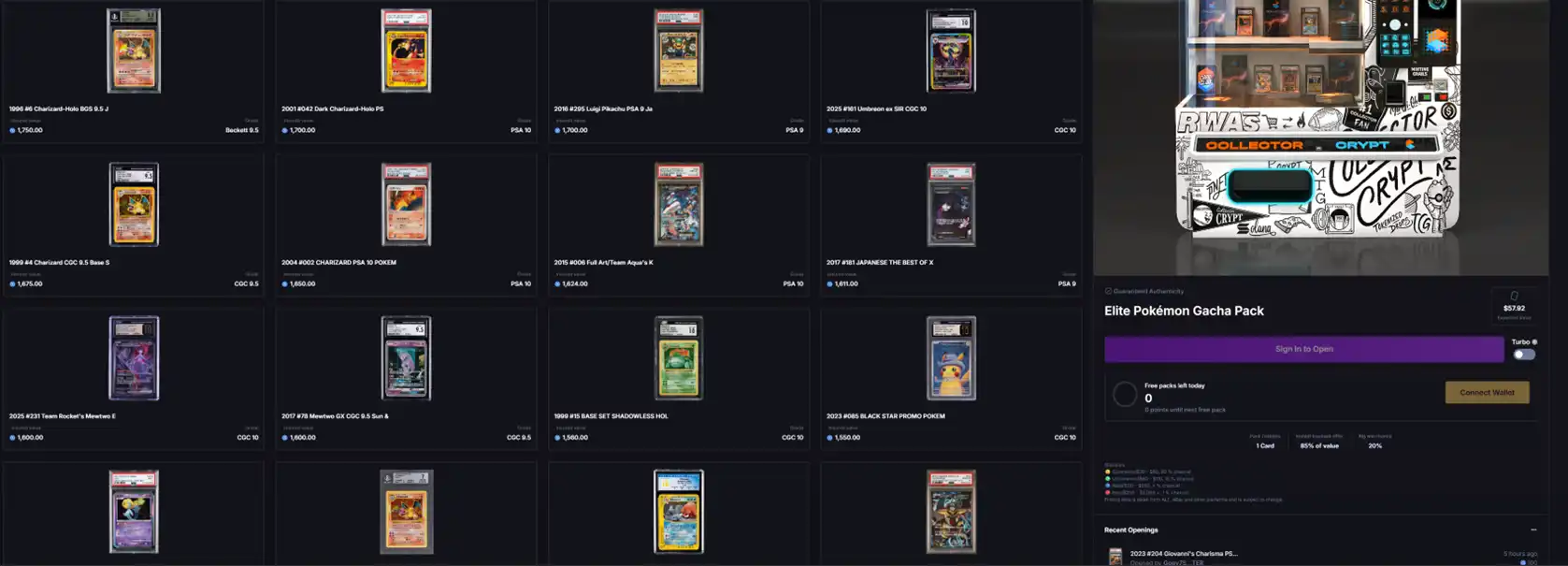

答案是没有。无论是 Collector Crypt 还是 Courtyard,他们实际赚钱的业务都是赌博式的「抽盲盒」。

上图就是 Collector Crypt 的宝可梦卡片扭蛋机系统。花大约 60 美元,有 80% 的概率抽到价值 30 至 60 美元的卡片,15% 的概率抽到价值 60 至 110 美元的卡片,4% 的概率抽到价值 110 至 250 美元的卡片,1% 的概率抽到价值 250 至 2000 美元的卡片。

抽到差的卡怎么办?没关系,可以以 85% 的折价直接卖回给 Collector Crypt,继续抽下去。

Collector Crypt 的这个抽奖系统在今年 1 月份正式推出,当月就实现了约 200 万美元的销售额,3 月份时成长到了月度 1255 万美元,5 月份时成长到了月度 2231 万美元,上个月更是达到了 4389 万美元。而在上个月,Collector Crypt 卡片交易市场的成交额只有约 12 万美元。

在 Collector Crypt 的月度总销售额柱状图上,来自卡片交易市场的份额几乎是完全看不到

虽然没有直接的抽奖收入数据,但我们可以从 Courtyard 此前的采访中侧面感受一下,抽奖业务究竟是有多赚钱。Courtyard 在上个月接受了 Fortune 的采访,采访中的数据提到,Courtyard 以 90% 的价值从客户手中回购抽奖卡片,然后将其以新的抽奖包形式转售给客户来赚钱,同一张卡片平均每月在平台上售出 8 次。

尽管如此,我们仍然很难说,$CARDS 的涨势是市场自驱动的「价格发现」。因为预售结束后到 2 天前,$CARDS 的价格都萎靡不振,参与了预售的玩家甚至觉得「又输了」。

但「车头」pow 与 gake 的加入极大改变了价格的走向。在他们都发推「奶」了 $CARDS 之后,大家开始相信了。

至此,我们可以对 $CARDS 做一个总结:

- 业务叙事并不新,但收入相当能打,是 Solana 上该赛道绝对的龙头。

- 需求是真实的,但不是宝可梦卡片交易本身的需求,而是「抽奖」的博彩式需求,同赛道的其它项目亦然。

- 同赛道的其它项目暂未发币,因此目前市面上没有与其竞争的相同概念标的。

- 代币持有者数量并不多,目前的上涨更多是「车头」喊单造成的。

有真东西,但在情绪驱动的上涨过后,$CARDS 能否继续保持势头,仍然需要时间检验。