OUSD's Impact on Circle, Tether, and Paxos: Not a Simple Negative, but a More Complex Competitive Reshuffle

This article analyzes the impact of the newly announced stablecoin OUSD, backed by a consortium including Stripe, on major incumbents like Circle (USDC), Tether (USDT), and Paxos (USDG).

For Circle, the announcement is not a simple negative. While the initial market reaction was rational, it's not a "death sentence." Circle retains deep liquidity, existing integrations, and first-mover advantage. A potential restructuring or termination of its exclusive revenue-sharing deal with Coinbase could even near-double its net income in the short term, providing more competitive flexibility. However, within the Stripe ecosystem, OUSD, with its strong engineering and product focus, could become the default choice, displacing USDC for new integrations. Circle must accelerate its own fintech product development and consider defensive M&A.

OUSD does not directly threaten Tether's core markets, which focus on different distribution channels. Tether's market share may decline over time but within a significantly growing overall market.

Paxos faces the greatest pressure. OUSD undermines the primary value proposition of its USDG stablecoin, and Paxos's regulatory advantages may erode as frameworks mature, posing a more existential challenge. This explains Paxos's recent strategic pivot towards brokerage-as-a-service.

A fundamental unresolved issue for enterprise adoption remains: if issued by a Bridge-related entity, OUSD, like USDC, still represents a credit exposure to a non-investment-grade issuer, unless a parent company guarantee is provided. Large banks and asset managers entering the space later could still compete for the most lucrative enterprise use cases.

链捕手1 h fa

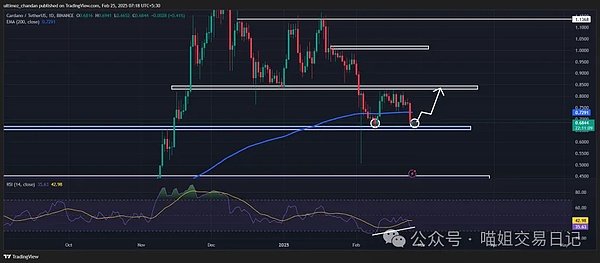

来源:Trading View

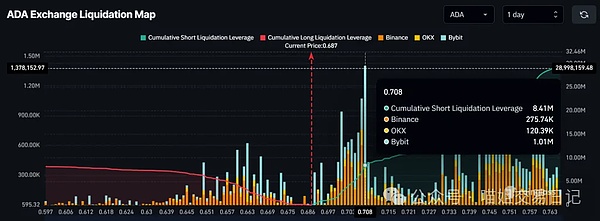

来源:Trading View 资料来源:Coinglass

资料来源:Coinglass 资料来源:Coinglass

资料来源:Coinglass