沉寂已久的SocialFi赛道再起波澜,一款名为Clout的应用正在改写「影响力变现」的规则。

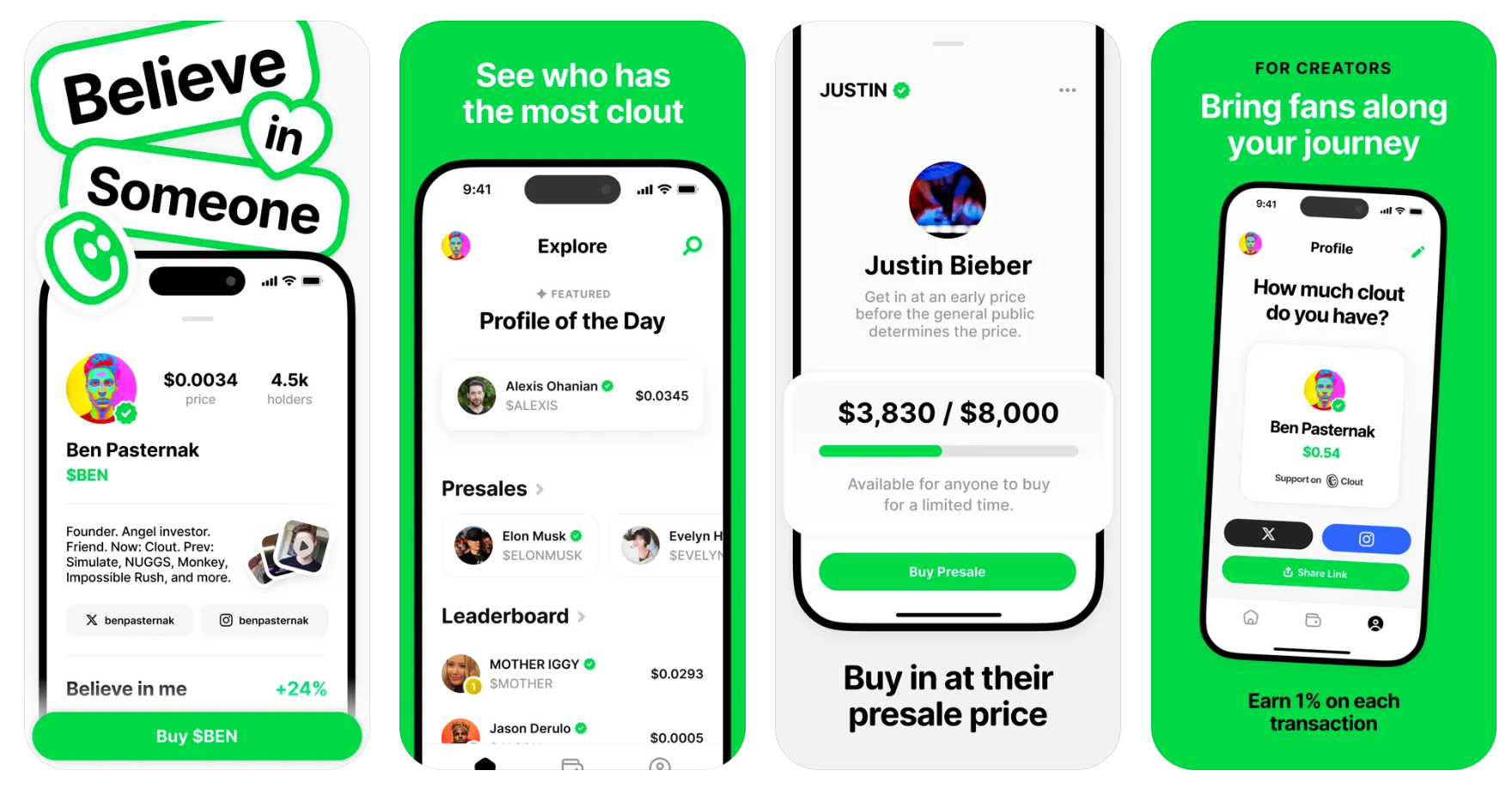

就在今天,这个允许用户发行个人代币的平台正式上线,其首枚代币$PASTERNAK在5小时内市值就火箭般冲破8000万美元,瞬间成为加密市场的焦点。深挖背后的操盘者——Ben Pasternak并非无名之辈,这位15岁辍学开发爆款社交应用、25岁入选《福布斯》30 Under 30的连续创业者,正试图用Clout为网红经济注入加密的基因。

值得注意的是,这场实验恰逢名人代币热潮的黄金窗口期。从特朗普家族的系列代币开始,社交媒体影响力正在被量化成可交易的数字资产。而Clout的特别之处在于,它将复杂的发币流程简化得像创建社交账号:绑定社交媒体认证、信用卡支付支持、自动分配内外盘交易机制——这套「Web2网红友好型」设计,或许正在为加密行业带来海量新鲜血液。

什么是Clout?

Clout的本质,是SocialFi领域一次大胆的基因重组实验——它巧妙缝合了FriendTech的社交资产化逻辑与Pump.fun的低门槛发币机制,最终孵化出一个“网红版纳斯达克”。

模式拆解:

- FriendTech的社交裂变基因

- 如同FriendTech将推特粉丝转化为私域流量,Clout进一步将影响力“上链”:创作者通过绑定X账号(需≥1万真实粉丝)发行个人代币,粉丝购买代币即可获得与偶像的“金融化关联”。

- Pump.fun的流动性增强术

- 借鉴Pump.fun的极简发币流程,Clout让创作者5分钟内完成代币创建,并通过内外盘机制控制流动性:内盘预售蓄势(仅限平台内交易),外盘开放后接入Raydium等DEX,形成价格发现闭环。

操作路径:

- STEP 1:创建用户名→绑定X账号→X发推验证(病毒式营销)

- STEP 2:输入代币名称/符号→设置发行总量

- STEP 3:系统自动审核粉丝数→通过后支付链上费用→生成代币

- STEP 4:粉丝通过信用卡/Apple Pay/加密货币钱包入金,参与内盘预售

这种混合模式既保留了FriendTech“社交资本证券化”的想象力,又通过Pump.fun式的技术普惠消解了加密门槛。当其他平台还在争论“社交与金融孰轻孰重”时,Clout已用一套标准化流水线,将网红经济推入了工业化量产时代。

创始人何许人也?

Ben Pasternak 是位25岁的澳大利亚小哥,15岁开发的游戏《Impossible Rush》冲入App Store美国区Top 20,17岁创立的青少年社交平台Monkey用户超2000万,20岁转身用植物基鸡块NUGGS攻占沃尔玛货架。如今这位创业天才又带着Clout闯入加密领域。

这种看似跳跃的创业轨迹,实则藏着一条隐秘的逻辑线:将抽象价值标准化。无论是将青少年社交需求封装成视频匹配算法,还是将大豆蛋白重构为“赛博鸡块”,Ben始终在解构复杂系统,并将其转化为可规模化的商品。而Clout,正是他给“个人影响力”装上的一台标准化计量仪——当社交媒体账号通过10万粉丝认证时,系统自动生成代币合约的行为,与NUGGS工厂将植物蛋白压制成鸡块的形状,本质上共享着同一种工业化思维。

这种思维的终极试验品,便是以他本人命名的代币PASTERNAK。作为Clout的首发案例,同时也收到了Solana官方的支持转发,该代币上线5小时市值突破8000万美元,却在白皮书中明确标注“创始人0持仓”。这种刻意剥离利益关联的操作,如同在实验室里设置对照组:当创始人与代币价值彻底解绑,市场的狂热究竟是对技术逻辑的认可,还是对名人IP的盲目崇拜?

Ben的野心显然不止于此。在最近的AMA中,他将Clout比作“Web3时代的华尔街+好莱坞”,试图将金融定价与明星造梦合二为一。然而历史总在重演:上世纪90年代,球星卡交易市场因过度投机崩盘;2023年,Friend.tech的代币化社交图谱经历暴涨暴跌。当Clout为每个网红配备一台迷你印钞机时,或许更该追问:当流量成为资产负债表上的固定资产,社交媒体会进化成更高效的价值网络,还是退化为一场全员参与的金融真人秀?

名人发币热潮与商业模式分析

当特朗普的MAGA代币以500亿美元市值力压其名下科技传媒集团(DJT)的估值时,加密市场彻底觉醒——名人的资本动员力,已远超传统实体资产的价值承载能力。而Clout的横空出世,恰似为这场“影响力IPO”浪潮装上了涡轮引擎:它不仅将名人发币标准化为流水线作业,更通过法币入口+流动性增强的双螺旋结构,将这场加密游戏升级为全民金融实验。

1. 天时:名人代币的“完美风暴”

2025年初的加密市场,正经历从“技术叙事”到“文化叙事”的范式转移。总统家族一个接一个的造富神话共同验证了一个底层逻辑:社交媒体影响力是可编程的资本。Clout敏锐捕捉这一趋势,将发币门槛降至“绑定推特账号+1万粉丝”的极简操作,其便捷性甚至让传统金融IPO显得笨重。

2. 基因重组:FriendTech+Pump.fun+Moonshot的混合进化

Clout的商业模式本质上是三股基因的合成生物:

- FriendTech的社交资本化:继承其将粉丝关系代币化的内核,但Clout通过标准化代币(而非碎片化Key)解决流动性割裂问题。FriendTech的Key仅能在封闭生态内交易,而Clout代币在内盘预售完成后自动接入Raydium等DEX,形成开放市场的价格发现机制。

- Pump.fun的工业化发币:吸收其5分钟创建代币的低门槛特性,但通过“身份验证+法币入口”实现合规升级。当Pump.fun用户还在为SOL链上Gas费头疼时,Clout的信用卡支付通道已吸引大批Web2网红入场。

- Moonshot的流动性迁移逻辑:值得一提的是,Ben是Moonshot的投资人,Moonshoot设计了“市值达标后迁移至DEX”机制,Clout将其改良为“内外盘双轨制”——内盘预售蓄积初始流动性,外盘开放后继续PVP,后续还有上CEX的预期,形成从封闭到开放的流动性阶梯,避免代币上市即崩盘的宿命。

3. 商业模式的优势

Clout的收益结构展现出与传统社交平台的差异化竞争力:

- 创作者端:通过链上费用和1%交易手续费获取收益。相较于FriendTech依赖单一Key交易抽成,Clout的多元收费模式(如内盘手续费、外盘流动性分成)更适应市场波动。

- 投资者端:法币入金通道降低参与门槛,吸引Web2用户涌入。这种设计类似于支付宝早期通过绑定银行卡简化支付流程,为Web3带来大量Web2的投机者。

4. SocialFi赛道的催化剂

Clout的崛起可能成为SocialFi生态的转折点。其创新机制直击行业三大痛点:

- 流动性困境:传统SocialFi平台(如Friend.tech)因代币流动性割裂导致用户流失,而Clout通过内外盘联动和CEX接入,构建了从预售到二级市场的完整交易链路。

- 用户门槛过高:加密原生平台依赖钱包操作,而Clout的邮箱注册和信用卡支付设计,将用户教育成本降至最低。这类似于微信支付通过扫码颠覆现金交易,让技术隐形于体验背后。

- 内容与金融的失衡:多数SocialFi项目过度依赖代币投机,而Clout通过绑定真实社交媒体影响力,将代币价值与创作者内容产出动态关联。这种“影响力即资产”的叙事,可能催生更多类似Substack的“订阅制内容+代币激励”混合模式。

若Clout能持续吸引顶级KOL入驻并完善生态工具(如数据分析面板、DeFi质押协议),它有望成为SocialFi领域的“基础设施级”应用。正如Uniswap通过自动化做市商重塑DEX格局,Clout或将以“个人代币发行协议”重新定义社交资产的流动性标准。

结语:Clout的未来图景

2007年,当YouTube推出首个创作者广告分成计划时,硅谷的批评者嘲讽这是“给业余爱好者发零花钱的幼稚实验”。没人料到,这一举措竟撬动了千亿美元规模的创作者经济——十七年后,头部YouTuber的单月收入足以比肩小型企业。

而Clout的实验,正以更激进的方式重演这场变革:它试图将YouTube的“广告分成按钮”升级为“个人IPO按钮”。健身博主不再需要等待平台算法施舍流量,他们可以直接将十万粉丝的期待封装成众筹代币;独立音乐人不必被唱片公司抽走七成收益,一段爆款视频带来的代币涨幅,可能抵得上一张白金唱片的版税。

这场实验的核心矛盾,实则是互联网演化史的复刻:如何在开放与管制、投机与创造、短期套利与长期价值之间找到平衡点。Clout给出的答案颇具启示性——通过“法币入口降低摩擦、内外盘机制过滤泡沫、真实社交关系锚定价值”,它试图在SocialFi的狂野西部中划出一块精耕细作的试验田。

回望历史,从PayPal解锁在线支付到TikTok重塑内容分发,每一次技术平权都伴随着旧秩序的裂变。而今,Clout正将裂变的矛头指向社交媒体最坚固的堡垒:注意力经济的定价权。若其能抵御短期投机的熵增,真正构建起“影响力-代币-实用场景”的价值飞轮,或许我们终将见证——

那个曾被视作妄想的Web3宣言,“You are the IPO”,正在从加密极客的呓语,变成每一块手机屏幕上的可触现实。