编译:深潮TechFlow

在加密货币领域,风险管理是最重要的技能。

如果你不主动管理风险,市场就会替你管理。

以下是 20 条聪明的规则,可以帮助你降低风险并增加利润:

1. 快速轮换

市场叙事和情绪变化非常快。新的协议可能在短短几周内取代市场领头羊。

时刻关注市场动态。尽早入场,并在大多数人之前退出。

把最后 20% 留给别人

当你获利时,很容易想要精准把握最高点,榨取每一个百分点的利润。

但这是不可能的,错误的时机可能会让你成为长期持币者。

不要贪心。

2. 尽早止损

我们都会犯错,但区别在于,有些人在亏损 15% 时就卖出,而有些人一直持有到亏损 80% 才卖。

在交易前就要制定好退出计划和规则。这样资金可以重新投入到更有潜力的投资中。

例如:如果亏损超过 15%,就卖出。

3. 获利的心理学

你可能会因为害怕错失“100 倍”的机会而不敢获利了结。

但即便你提早卖出,而它涨了 100 倍,你仍然获利。关键在于,你保护了自己免受可能的损失。

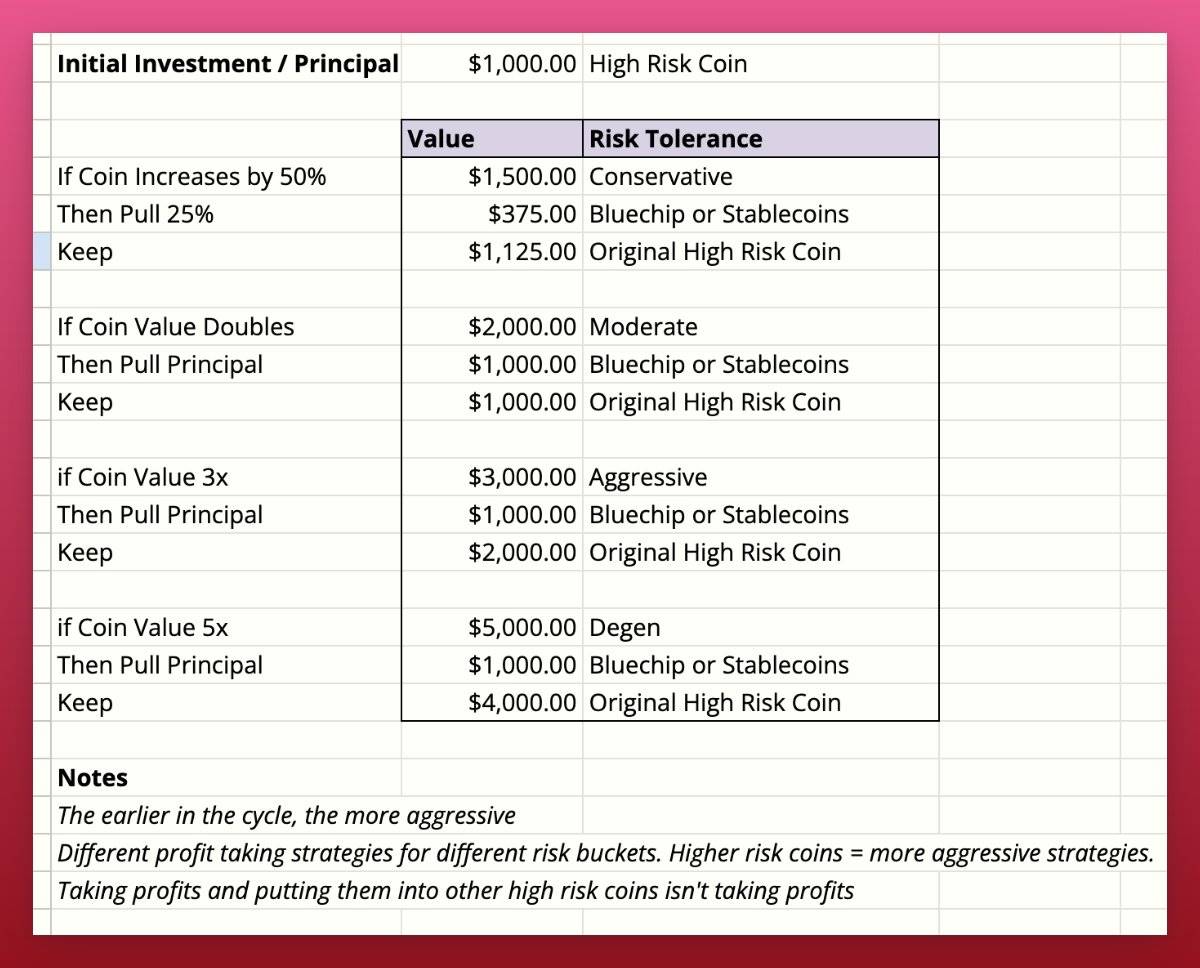

4. 获利了结

在你锁定利润之前,一切都只是屏幕上的数字。

当你收回初始投资时,会有一种心理上的满足感,而剩下的利润则可以继续增长。

用简单的公式来指导你的操作。

5. 等待市场稳定期

市场稳定期是指当流动性进入市场,整个行业呈现积极趋势。这种情况每年会发生几次。不要因为感到无聊或寻求刺激而参与波动市场。你不需要每天都进行交易。(如图所示的 Solana)

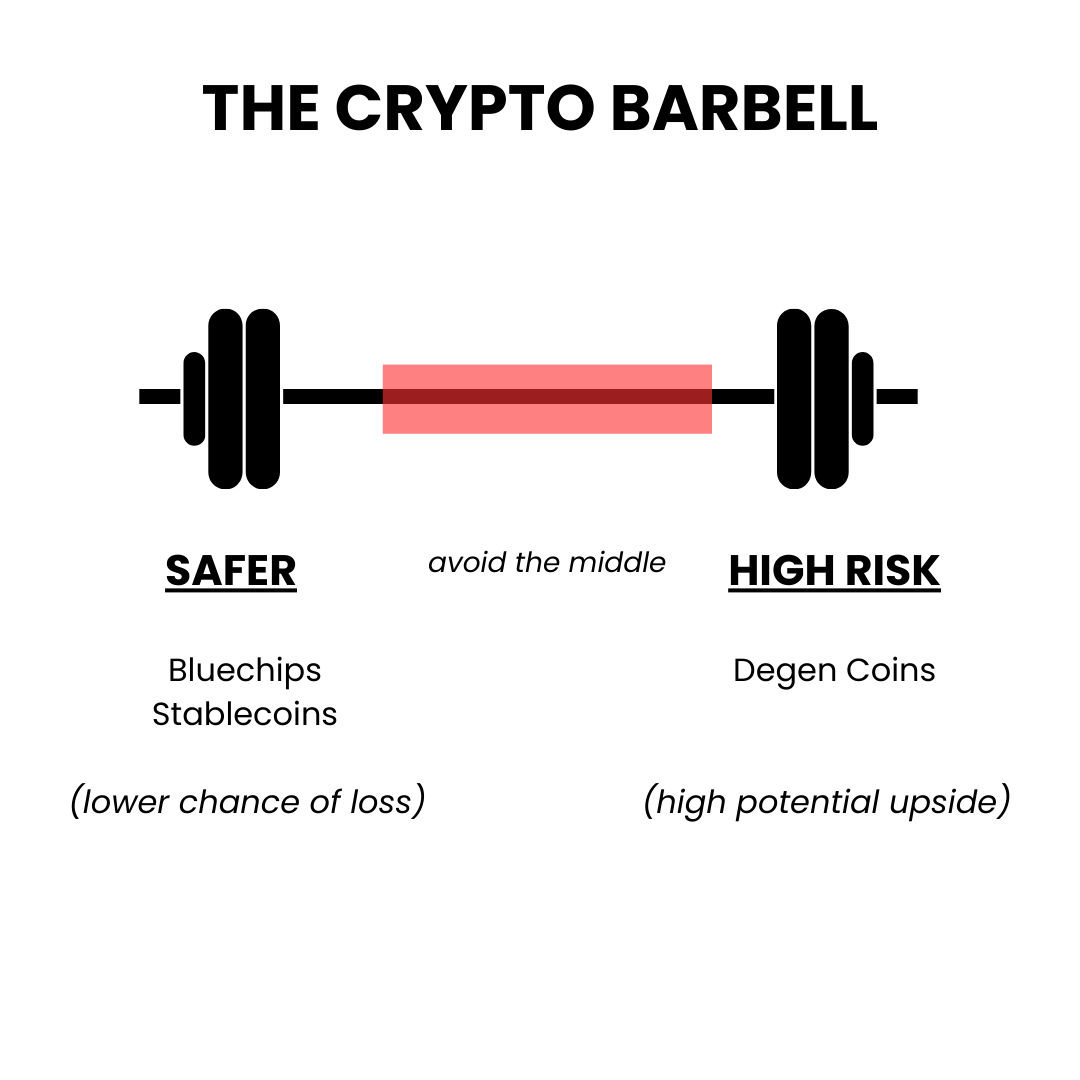

6. 创建一个平衡的投资组合

我的长期投资组合主要包括 ETH,并保留了一些稳定币。这些安全资产让我能够更从容地承担较大风险。我喜欢以杠铃策略来构建投资组合——一边是安全资产,另一边是高风险投资。

7. 追求 Alpha 投资

许多人因不断追逐高风险的贝塔投资而亏损。一个替代策略是选择市场领导者:

-

Pendle 用于真实世界资产 (RWA)

-

Bananagun 用于 Telegram 机器人 (TG Bots)

-

选择 ETH 而不是 ETH 的贝塔投资

潜在的强劲回报和较低风险。

8. 不要随意改变目标

2021年,我的朋友实现了他的目标:将15万美元变成了100万美元。但随后他又设立了新的目标,“再过几个月,我就可以一劳永逸了。”他错误地判断了市场顶点,最终资产回落到15万美元。要知道什么时候是“足够”。

9. 切勿将资产锁定

我见过太多人为了额外收益或积分将 Token 锁定,结果被协议“收割”。重视可选择性——你不希望在市场变化比预期更快时,Token 被锁定而无法使用。

10. 避免单点故障

1)将你的稳定币分散在 USDC、USDT 和 Dai 之间

2)使用多个中心化交易所进行入金,以防其中一个被锁定

3)将你的加密货币分散在多个钱包中

11. 将利润投入 Degen 币并不算是真正的获利

获利意味着你要从市场中撤出资金,将利润转入稳定币、长期持有或兑现。将利润投入 Degen 币更像是在进行复式押注。

12. 不要将超过 15% 的资金投入非蓝筹或非稳定币资产中

在加密货币领域,没有任何保证,也没有什么是大而不倒的。

-

Terra 和 FTX 都曾失败。

-

Euler 和 Curve 也曾遭黑客攻击。 黑天鹅事件比你想象中更常见——要保护好你的下行风险,以免一切归零。

13. 坚持在你的能力圈内行动

选择 2-3 个领域进行深入研究。每周在一个领域专注研究 10 小时将使你位列前 1%。许多风险源于投资你不熟悉的领域,仅仅因为害怕错过机会而盲目投资。

14. 定期调整投资组合

你应该为投资组合设定一个目标分配比例,这会因市场周期阶段的不同而有所变化。市场火热时,高风险 Token 表现优异,容易导致投资组合失衡,因此要养成定期调整的习惯。

15. 在加密货币领域之外进行多元化投资

我常常将获利资金投入加密货币以外的领域,包括最大化退休基金、建立充足的应急基金以及再投资于业务。这让我更能从容应对加密货币的波动性。

16. 尽量避免在现实生活中谈论加密货币

在发展中国家旅行时,佩戴金饰的人比低调的人更容易成为抢劫目标。同样,在现实生活中谈论加密货币越多,就越可能成为目标。

如果有人问我是否从事加密货币,我会说我在 FTX 崩盘时失去了一切,现在从事电子商务供应链工作。富有的人往往高调,而真正的财富则是低调的。不要给自己或家人招来不必要的注意。避免参与地位竞争。

17. 使用合适的安全工具

你应该使用 Rabby Wallet、Brave 浏览器、DeFiLlama 扩展、Wallet Guard 等。通过 DeFiLlama 扩展的绿色 Llama,我能确认自己在正确的协议网站上。

18. 使用临时钱包

我常常尝试新的协议,因此配备了一个临时钱包。这样即便协议是恶意的,我最多也只会损失 100 美元。把临时钱包视作在 Tinder 约会时使用的安全措施。

19. 不要试图在一个周期内实现成功。

• 大量使用杠杆。

• 借钱投资加密货币。

• 过度投资于高风险币种。

这些行为都是因为急于在一个周期内成功而承担过多风险。

20. 最终,整个行业都在鼓励你更加乐观并承担更多风险。为什么?

因为如果你进行风险管理,他们就赚不到钱。他们希望你购买他们手中的资产。

你必须对自己的财富负责。

学会防守才能赢得胜利。