2026 Investment Framework: The End of Globalization, AI Supply-Demand Mismatch, and the Silver Frenzy

marsbitPubblicato 2026-01-09Pubblicato ultima volta 2026-01-09

Introduzione

Investment Framework 2026: End of Globalization, AI Supply-Demand Mismatch, and Silver’s Surge

The author outlines a macro investment framework centered on three key themes: the end of globalization, accelerating resource nationalism, and the rise of AI-driven structural shifts. The portfolio returned 131%, largely due to significant long positions in gold and silver.

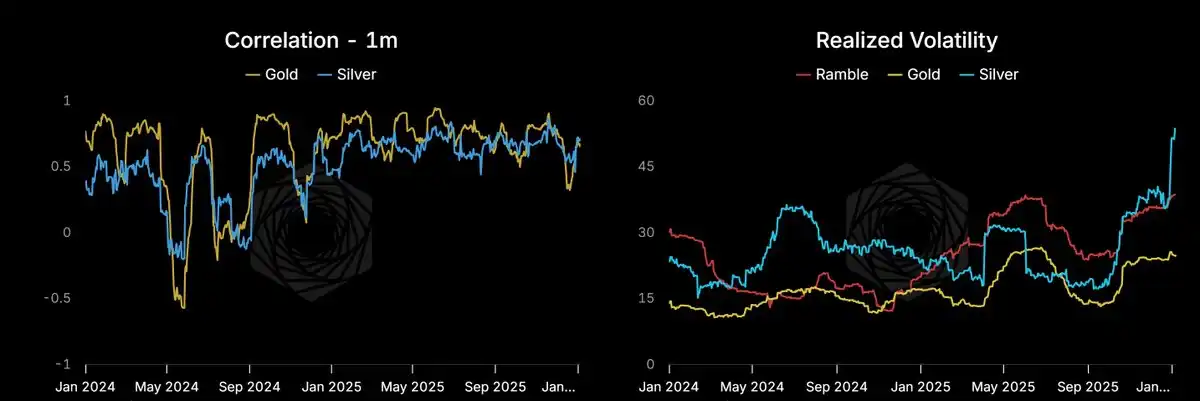

Silver markets are experiencing extreme volatility and a potential supply squeeze, with prices influenced by COMEX contango, LBMA backwardation, and Asian export restrictions. Investment strategies include calendar spreads and butterfly options on silver.

Other positions include shortening duration, adding crash protection via SPY, shorting student loan servicers, and going long on tin miners and Japanese banks.

Key thematic drivers:

- Globalization’s end: Resource nationalism rises; Monroe Doctrine 2.0 emerges; metal inflation continues while oil may face oversupply.

- China’s challenges: Banking system fragility, hidden real estate losses, and rising religious dissent.

- AI acceleration: Compute demand will vastly outstrip supply by 2035. Two phases: near-term oversupply (2025–2027) followed by demand explosion (2028–2030+) as agentic AI matures.

- Domestic US issues: Government shutdown risks, student debt crises, and the societal impact of AI and GLP-1 drugs.

Investment opportunities include copper, tin, photonics, nuclear energy, natural gas, and compute infrastructure. Markets face pressure from Japan...

Author:Campbell

Compiled by: Deep Tide TechFlow

Yes, we're updating a bit late. New Year's Eve was spent trading—adjusting the portfolio for 2026, cleaning up the books. Thought there would still be time for more analysis before hitting the publish button.

"What major events could possibly happen in the first week of the new year?"

The first misjudgment of 2026.

Silver skyrocketed. Maduro (President of Venezuela) was taken away like a thief in the night. Iran, in turmoil? Greenland back on the negotiating table? Ships from Russia, Iran, Venezuela seized by special forces? Today, Trump also banned defense contractors from paying dividends or conducting stock buybacks while working with the government, and prohibited institutional investors from entering the single-family home business.

Although our blog update is late, the world seems to be gradually accepting the framework we've been harping on: the end of globalization, resource nationalism, the remonetization of silver, China's gold reserves, the "Horseshoe Theory" of the political spectrum becoming reality, and the urgent need for a "New New Deal" against the backdrop of machines exacerbating inequality.

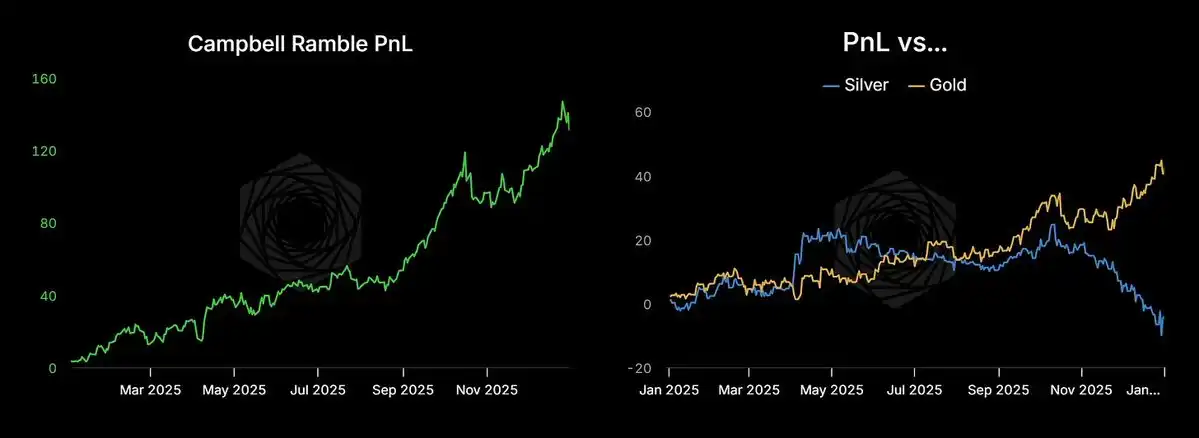

Clearly, the market agrees with these views—we ended the year with a 131% return. This was mainly thanks to our oversized positions in silver and gold.

Please remember: we are just small players, not on the same level as the big shots. Part of the reason we benefit is that we operate a relatively small portfolio, while the trading, liquidity, and institutional costs for those managing pensions and endowment funds could be 10 or even 1000 times ours. It's a completely different game—they are professionals, and I'm just an amateur. This portfolio was designed more to hedge my illiquid startup equity while capturing returns consistent with our overall Stoic macro investment framework.

Read in detail: Stoic Macro Investment Framework

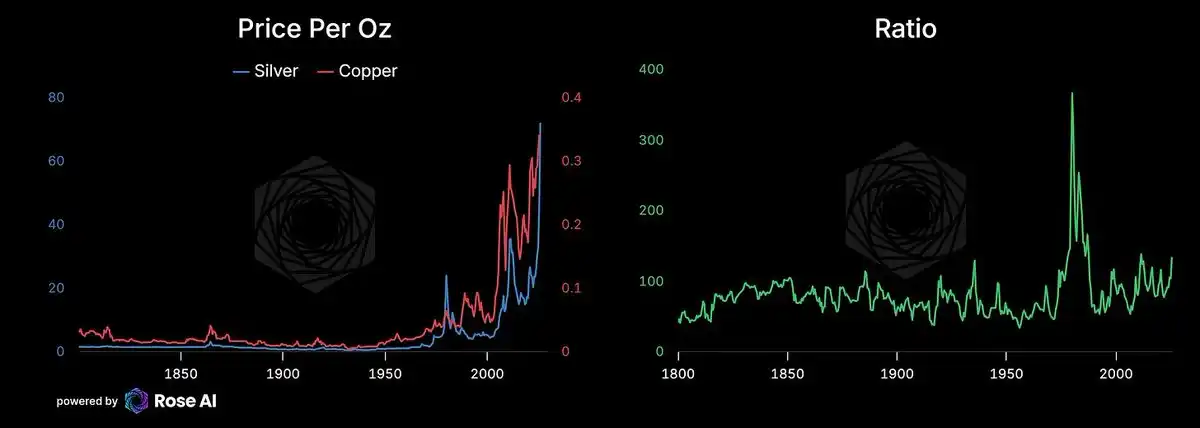

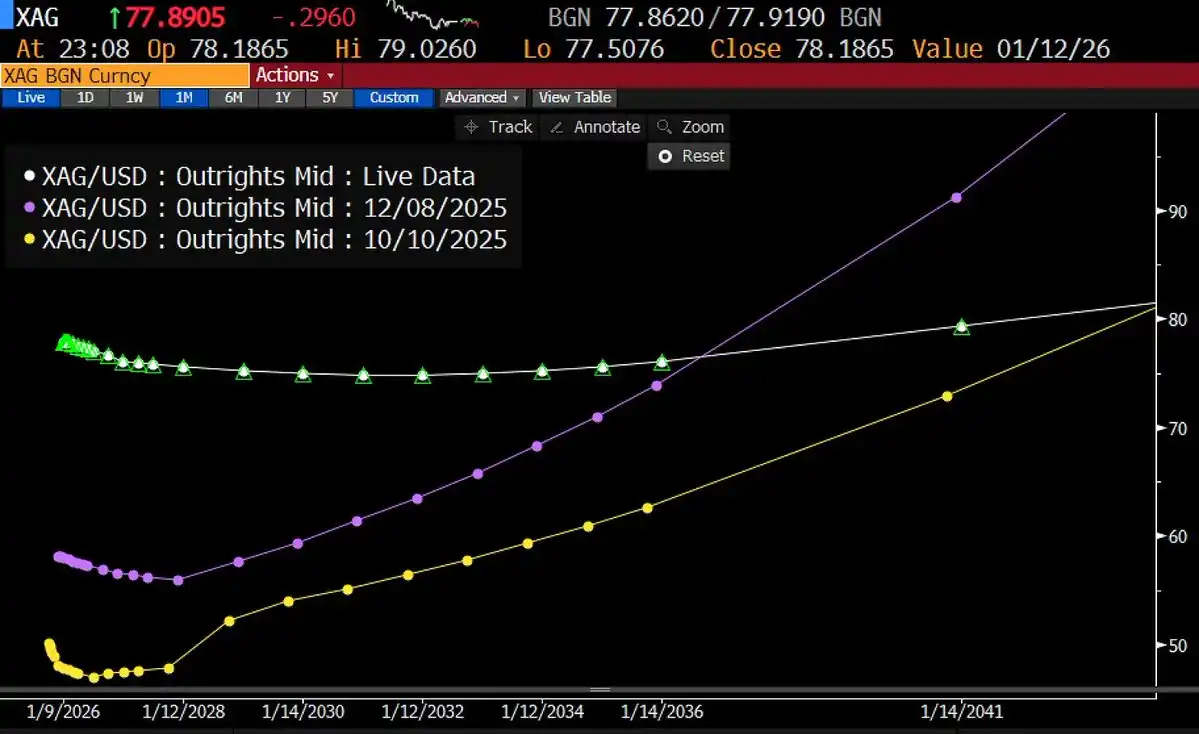

The State of Silver

Instead of focusing on the return rate, let's look at the actual composition of the portfolio. You can see that our portfolio's correlation with silver has increased, and our volatility target remains around 30.

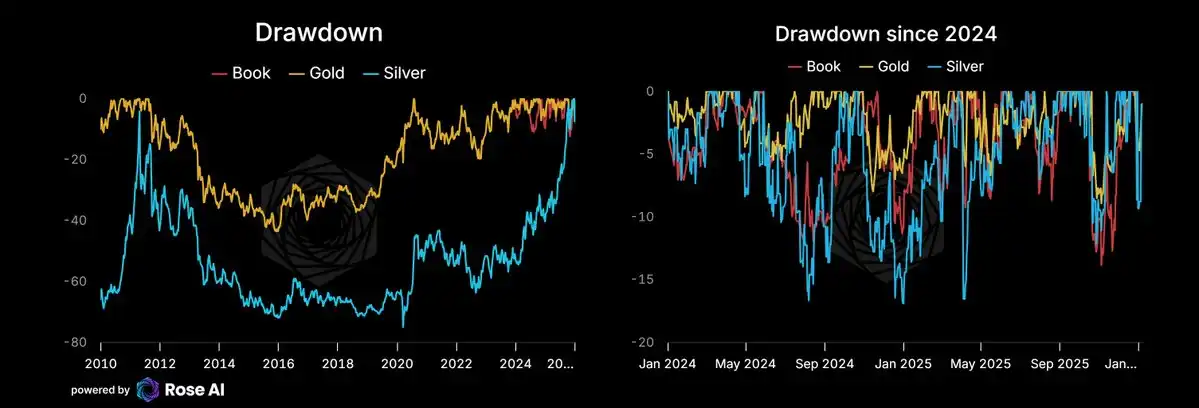

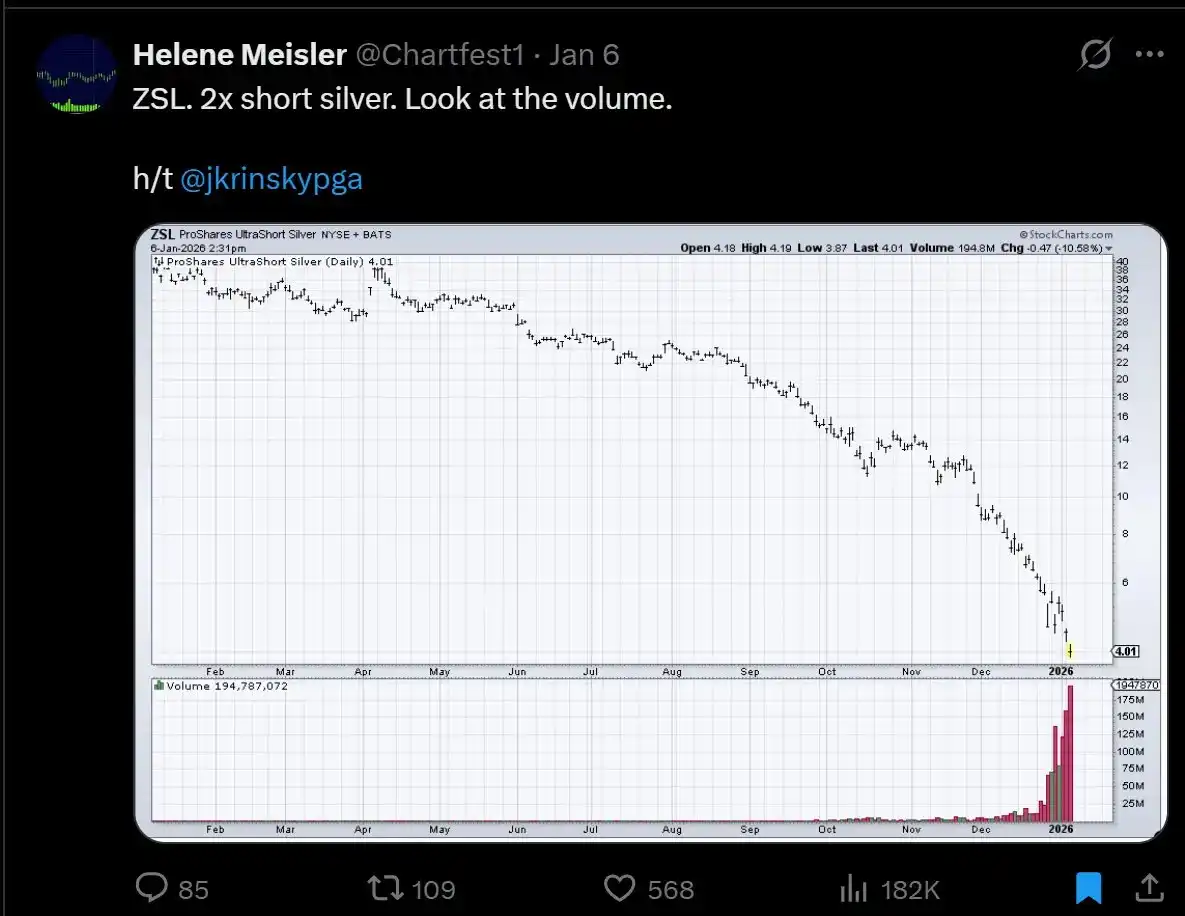

It's important to note that silver experienced sharp pullbacks after previous squeezes—these fluctuations are still clearly visible in data decades later. We know this wave will eventually end in a similar fashion. The question is, will it end at $85, $200, or $1000? And how long will it take to get there?

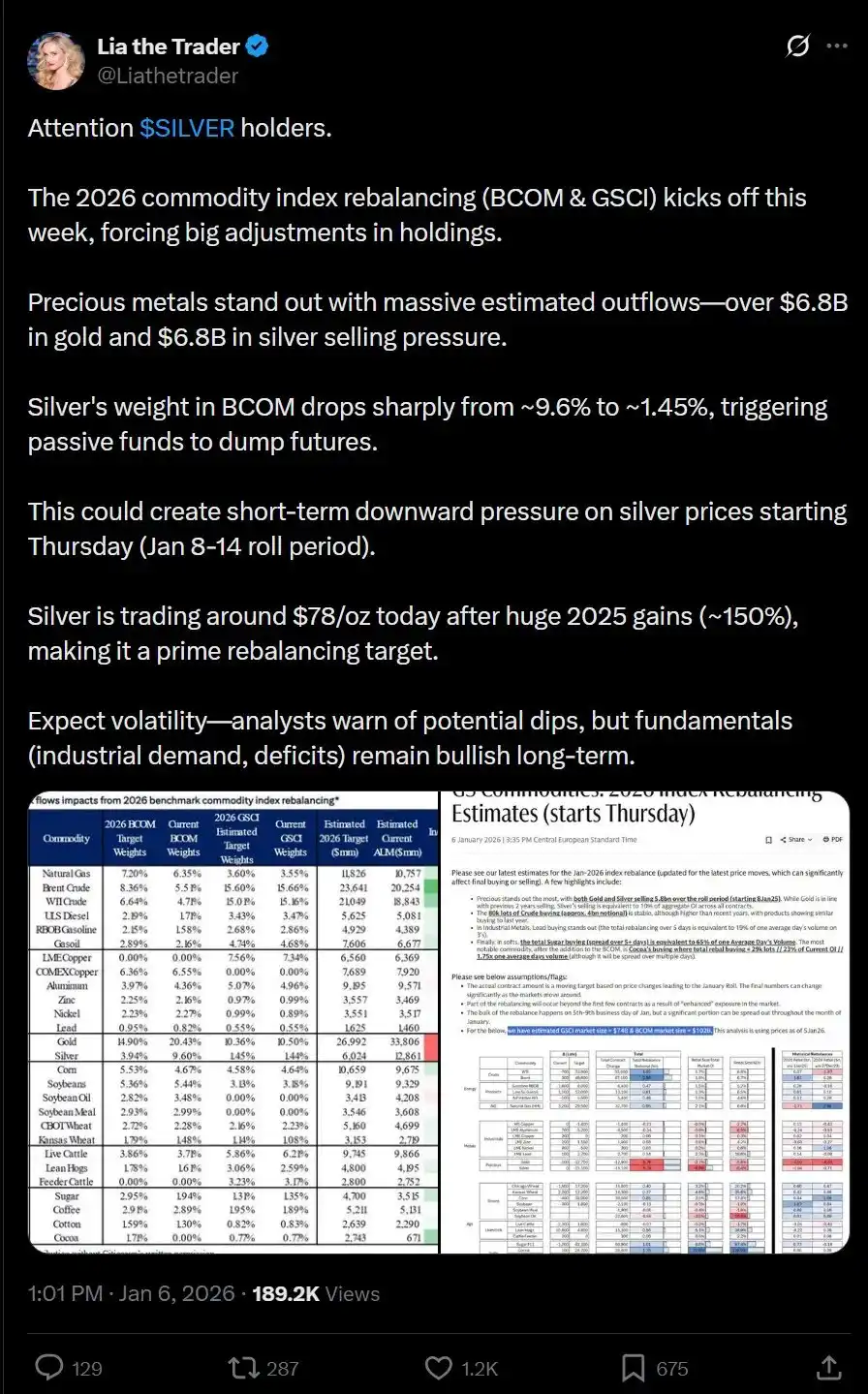

The shorts are waging war. A noteworthy observation is that index rebalancing is imminent—silver's weight in some commodity baskets will drop from nearly 10% back to its historical average of 2%. I believe the final outcome will be a structural increase in silver's weight, but the shorts are also correct: this will indeed bring selling pressure in Western markets.

What we're seeing in the silver market reminds me of trading crude oil back in the day.

When I train interns, I always start with a question: "What is the price of crude oil?" See what answer they give. The problem is, crude oil doesn't have a single price. When people say "the price of oil," they are using an abstract concept to refer to the prices of a series of markets. These markets each have different prices, which are then integrated into a complex basket or linked to the dollar-denominated futures market through some strange formula.

So, the question "What is the price of crude oil?" actually leads to more questions:

- Where is the price difference between US WTI and European Brent crude?—Different geographical locations.

- Is it the price for today, or tomorrow? Or five years from now?

- What about the type of oil? Like Dubai crude?

- What about the product type? Gasoline, naphtha, or fuel oil?

- What about the currency? Like crude traded in Shanghai?

This brings us to the silver market.

The shorts are correct: the index needs adjustment, the current rate of increase is unsustainable; and if the silver price breaks through $100, producers will accelerate plans to replace silver with base metals.

But in the medium term, these short pressures will gradually ease and turn into buying. Index rebalancing will eventually end, and record short positions will eventually be closed out—and this liquidity will actually benefit the silver price.

Part of the impact is reflected in market positions, and part is directly reflected in prices.

But when we zoom out, all this seems to become less important. Why?

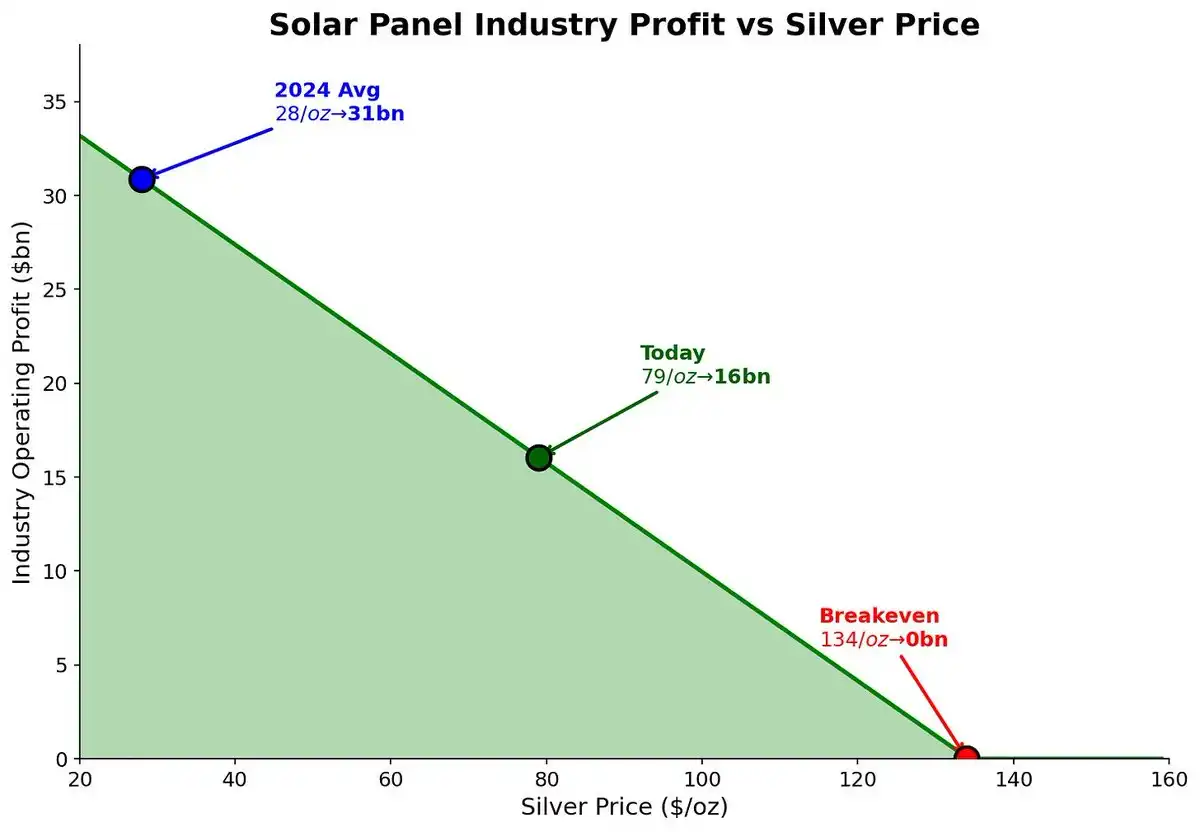

First, copper substitution takes time.

Based on my rough estimate: it would take more than 4 years and about $16 billion in capital expenditure to achieve. Welcome to provide other models for discussion.

<极速>

This means we have time before the "short squeeze" mentioned by the shorts truly evolves to the point where solar producers are forced to choose alternatives—and before that, the silver price could still have 50% upside.

At the same time, it's entirely possible for another scenario to occur: efficient frontier solar developers研发 panels that极大提升 energy capture efficiency, and these panels恰恰需要more silver. In fact, this has been the recent trend (although names like TopCon and HJT sound easy to forget).

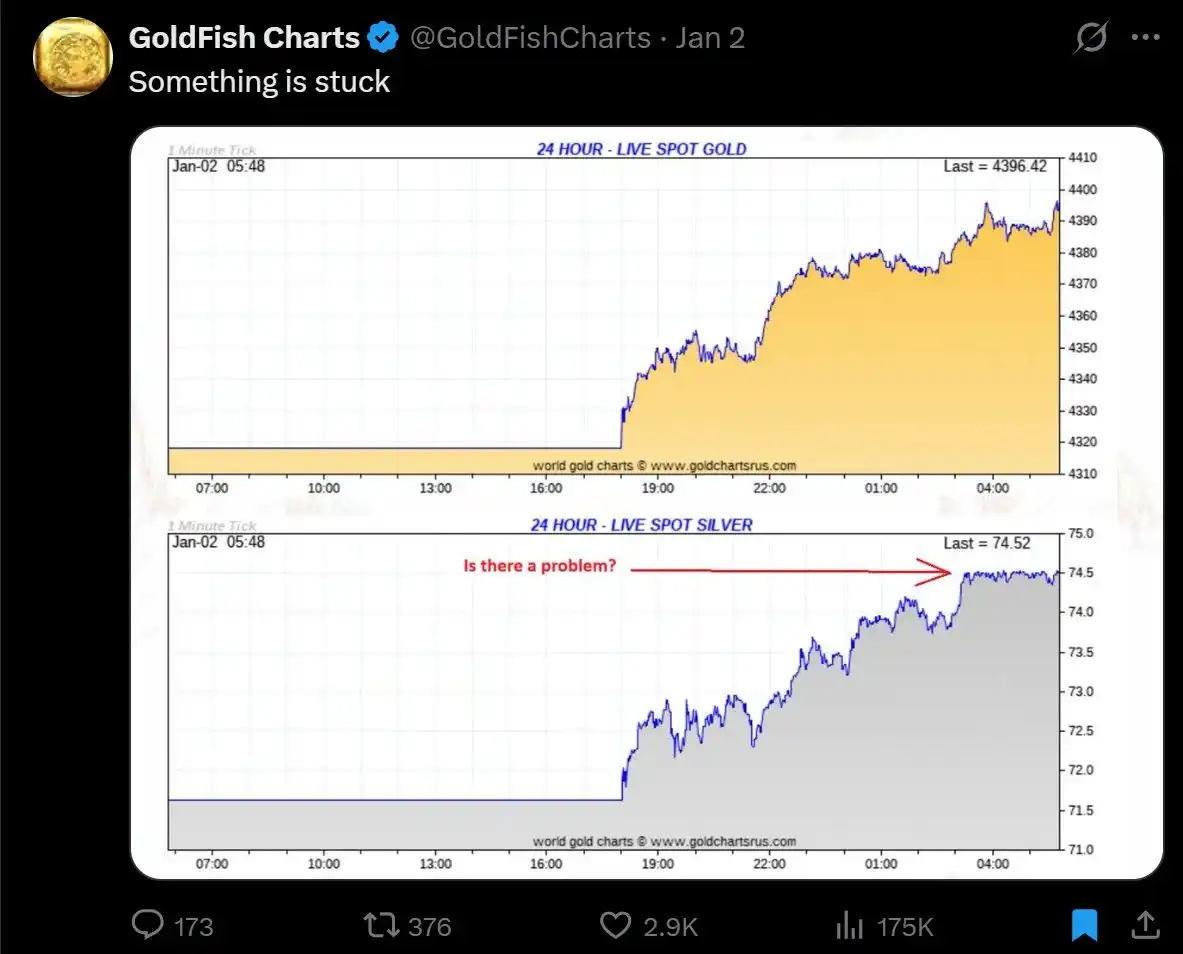

Second, when considering the question "What is the price of silver?", we need to look at it in the context of the actual market:

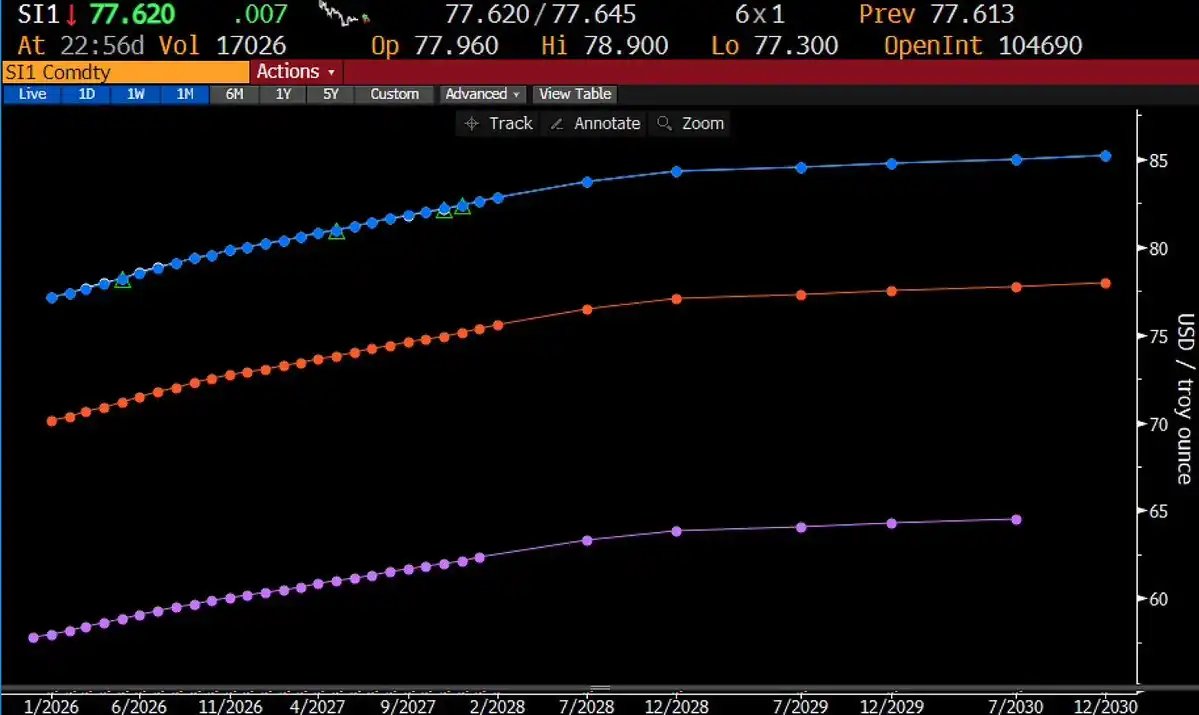

New York (COMEX) market: The current price is $76.93, market inventory is relatively ample, and the futures curve shows a typical Contango shape—near-term prices are lower than forward prices because holders need a premium to cover carrying costs.

London (LBMA): As the "old world home" of silver, inventory is scarce, and near-term prices are higher than long-term prices—a market characteristic known as Backwardation.

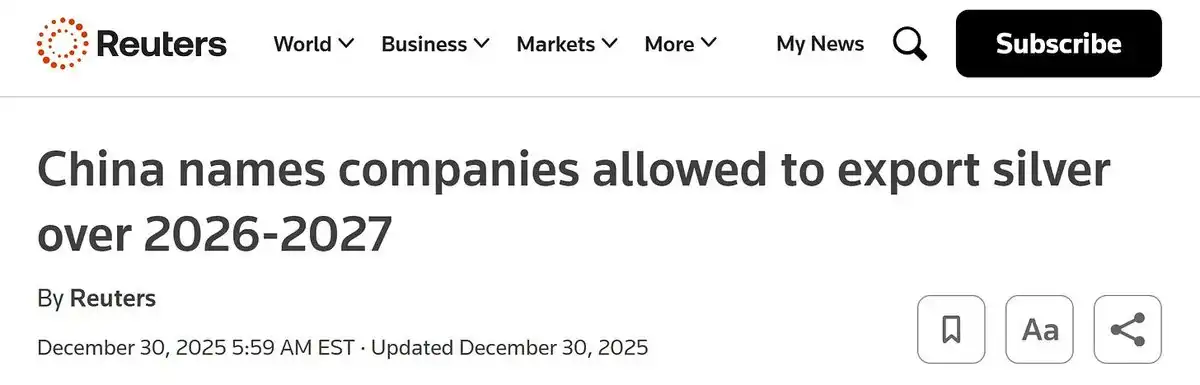

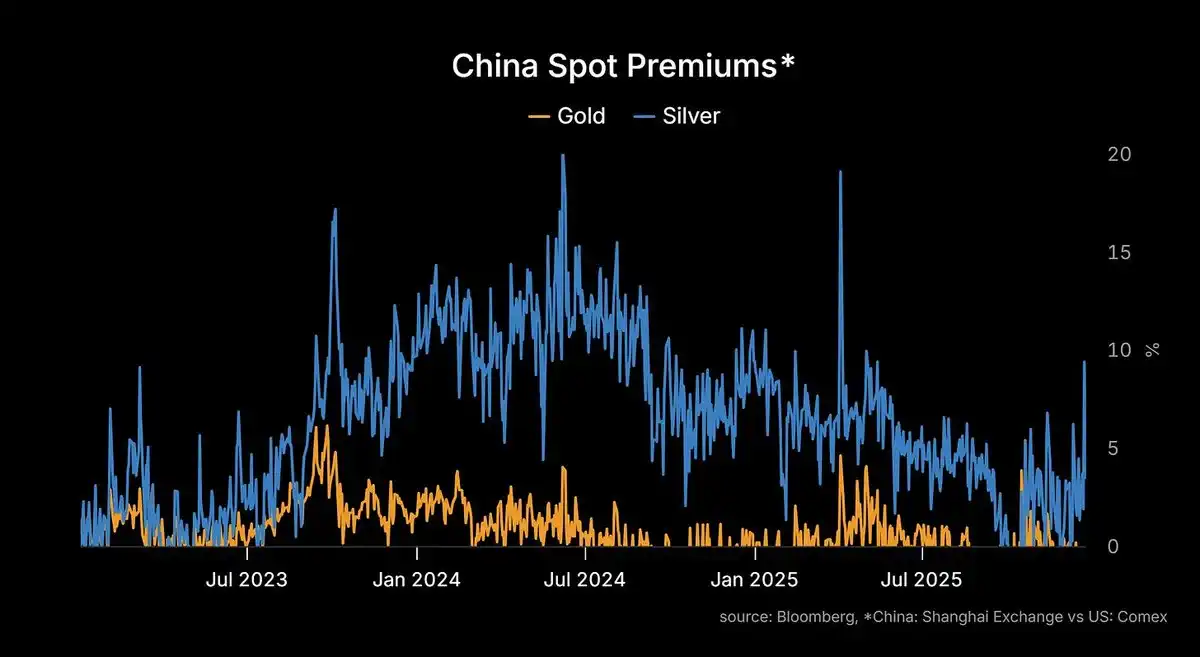

Shanghai/Mumbai/Dubai: These are now the "ultimate destination" for physical silver. Trading prices in these markets generally carry a premium. Moreover, governments have just banned (or severely restricted through administrative means) silver exports. Now, your silver in Asia needs a "passport" to leave the country.

This is why we love this market.

The long-term story of the silver market is so vibrant that you can enjoy tracking its daily dynamics. That feeling of deeply understanding a market—not predicting where it's going (even the best predictors only achieve 55%-60% accuracy), but understanding its behavioral patterns: the shape of the curve, the characteristics of volatility.

Investment Strategy:

We have adjusted our silver position from 30%+ direct long and 15% derivatives exposure to the following strategy:

- Calendar Spread:

- Capture the opportunity for the COMEX market to shift from Contango to Backwardation.

- Long March contract, short June contract.

- COMEX inventory has decreased by 81 million ounces since September.

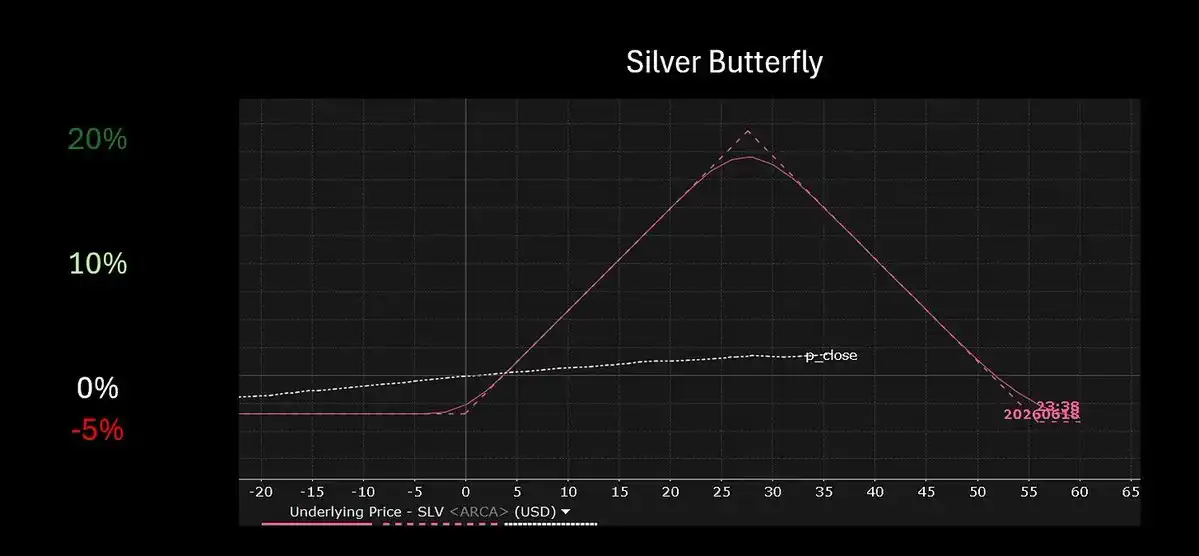

- Butterfly Options Strategy:

- For markets with expensive upside skew that we acknowledge the downside risk, use at-the-money butterfly strategies.

- Allocate 5% capital to a SLV (iShares Silver Trust ETF) 70-90-110 June butterfly, costing about $2.50.

- Target profit about $10, max profit about $20, potential return about 7x.

We will choose to roll or close the position when approaching the middle strike price (around $100/oz futures price) or 1-2 months before expiration.

Other Adjustment Actions:

Shortened Duration, Increased Crash Protection:

- Swapped medium-term Treasuries for SPY (S&P 500 ETF) put options, improving margin efficiency while gaining higher convexity returns in downside risk.

Short Student Loan Servicers:

- Total US student loan debt is $1.7 trillion, the SAVE plan (government loan forgiveness plan)前景不明, default rates are rising. When the system crashes, loan servicers will be the first to feel the impact.

Long Tin Mining Companies:

- Allocated a small amount of capital, based on a "lottery ticket" investment logic. Every chip needs solder, solder needs tin, and the tin supply chain is currently in chaos.

Long Japanese Banks:

- The Bank of Japan (BOJ) is finally beginning policy normalization, the 30-year Zero Interest Rate Policy (ZIRP) is ending, and bank Net Interest Margins (NIM) will see real recovery.

Final result: A cleaner portfolio, higher margin efficiency, and position layout consistent with the following investment framework.

Three forces drove 2025, and there are three decisive forces for 2026 as well.

The End of Globalization:

Both sides of Cold War 2.0 realize the old balance is unsustainable. Resource nationalism, gray zone conflict, and the division of spheres of influence become the new normal.

Acceleration is Real:

Both public and private sectors are racing to secure supply chains for critical minerals, energy, and talent to feed growing demand.

"Horseshoe Theory" Becomes Reality:

The disintegration of the neoliberal consensus is underway. Zero-sum thinking between generations and genders further exacerbates this trend, and a new political reality is emerging.

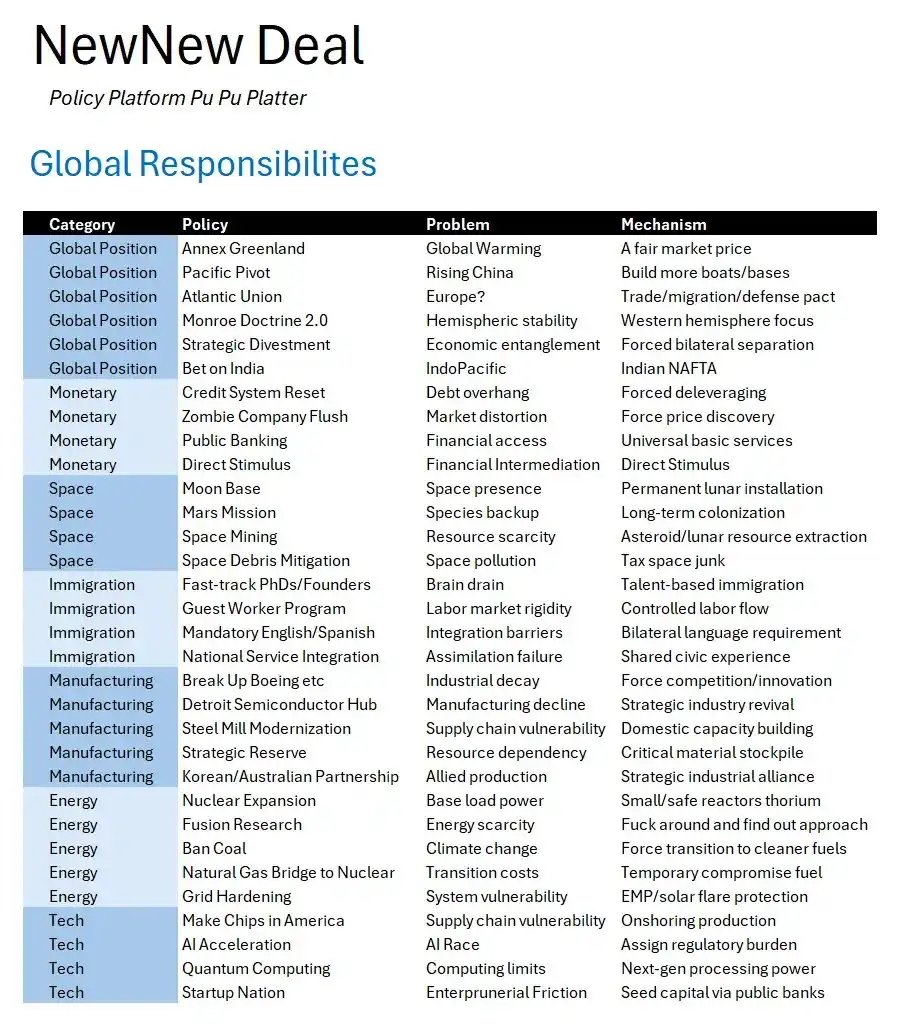

Many of the seemingly crazy ideas proposed on our "New New Deal" platform—especially regarding global portfolios—have now完全 entered the "Overton Window" of discussion.

Greenland, Monroe Doctrine 2.0, betting on India, moon bases, strategic reserves, US-South Korea cooperation, nuclear power expansion, nuclear fusion, natural gas, US chip manufacturing, AI acceleration—these have all become mainstream trends.

Related ideas about the US domestic scene may take another year or two to fully materialize:

More detailed analysis coming soon.

But you're not here for philosophical discussion.

Long-time readers want to see if we can maintain an ~80% hit rate, and new readers want to know the latest on silver (just mentioned).

Let's get straight to the views section.

Views

The End of Globalization

Resource Nationalism Accelerates:

Countries are starting to hoard resources. Indonesia restricts tin exports, Chile tightens control over lithium resources, China controls the export of Gallium and Germanium.

The end of globalization isn't just about finished goods tariffs, but a struggle for control over key raw materials.

Monroe Doctrine 2.0:

Greenland, Panama, Venezuela become focal points.

Maduro (Venezuelan President) may step down, Trump revisits the idea of "buying Greenland." Western Hemisphere countries are striving to secure strategic resources. This seemed absurd last November, but has now become a policy issue.

Conflict benefits metal inflation, but not necessarily oil:

The old rules of the game are失效.

Venezuelan and Iranian oil re-entering the market leads to a crude oil surplus, OPEC's pricing power may disappear in the next decade.

However, metals used for building energy infrastructure (like copper, silver, tin) are rising in price. Supply chains are disrupted, export bans are spreading, demand is soaring.

- WTI (West Texas Intermediate) price curve collapsed from $75 backwardation to $60 flat. The mid-term price curve for 2027-28 still has a hump, but may smooth out.

- Investment advice: Long metals, neutral or bearish on oil.

China's Challenges

Banking "Zombification":

China's banking system has not undergone substantial restructuring, losses are hidden, "extend and pretend" is the norm.

The real estate industry has $5-10 trillion in losses on the books, but still recorded at face value. Facing a "Sophie's Choice": structural reform or currency devaluation? Hasn't chosen yet,只能默默承受 long-term "slow bleeding."

Local Government Financing Vehicle (LGFV) Defaults Go Public:

The first public LGFV default was quickly covered up.

This type of debt now exceeds $9 trillion, and its implicit guarantee has never been truly tested publicly. If the system collapses, the government will try to contain it, but面对数万亿的债务规模, there is no precedent.

Religious Revival:

The proliferation of underground churches has triggered more control.

As economic performance falls short of expectations, more people are seeking spiritual solace outside the Party, and religious belief is gradually rising.

III. The Arrival of Acceleration

The Compute Gap (The Air Gap):

During the holidays, I consumed more compute power than in the past six months. Using desktop Claude Code, operating five different AI agents that talk to each other on Slack, and constantly creating, storing, and updating context from the perspectives of developers, quants, or data analysts. I saw the future, and the future has arrived. The age of acceleration is upon us.

The demand is real, I experienced it firsthand. When the infrastructure, permissions management, models, and local compute in the tech stack combine seamlessly, everyone can operate like me. And now, many developers (including myself) are埋头敲击键盘, trying to create their own "orchestration environment" to integrate all this. The first to achieve this might trigger an operating system-level revolution in personal computer interaction.

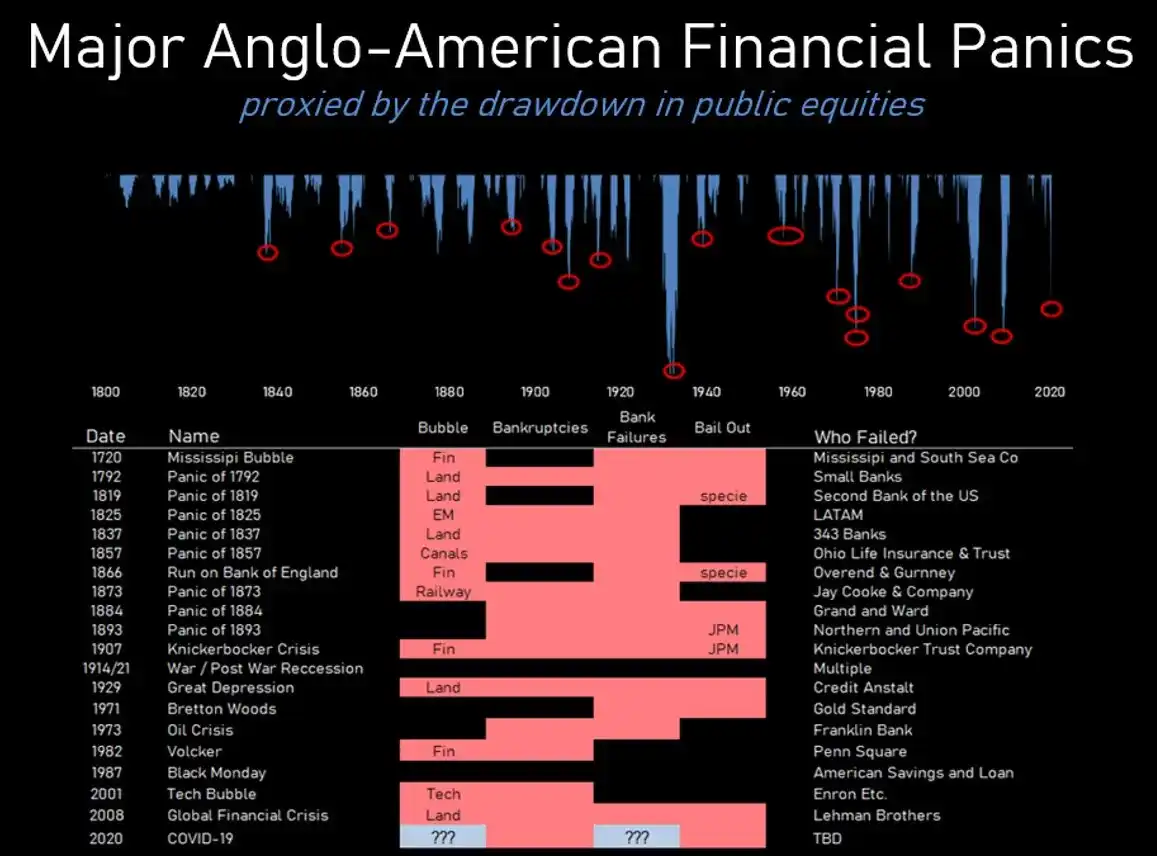

The problem is: infrastructure always arrives before demand. This has happened repeatedly in history, whether it's fiber optics, or highways, infrastructure construction always comes first. Although society will benefit in the long run, companies that invest in infrastructure often become victims of financial panic due to over-leverage—consistent with our 2018 framework on the origins of financial panic.

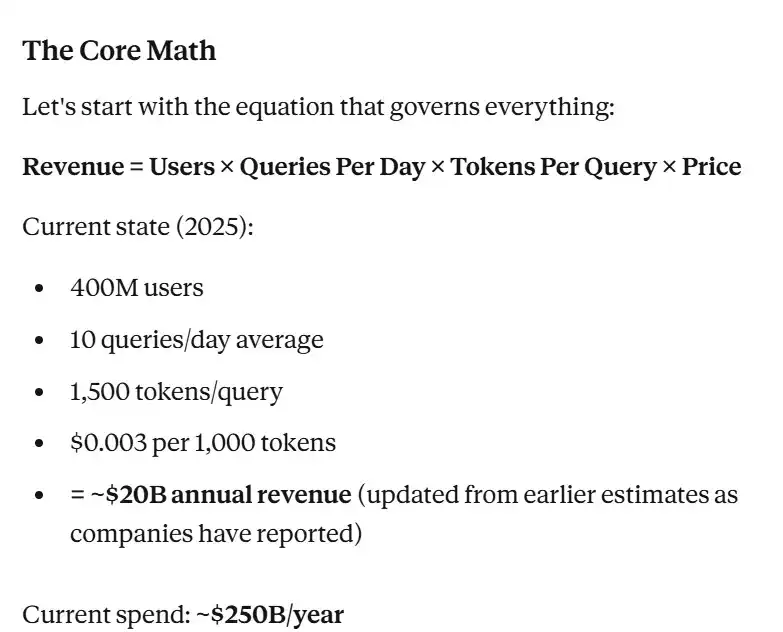

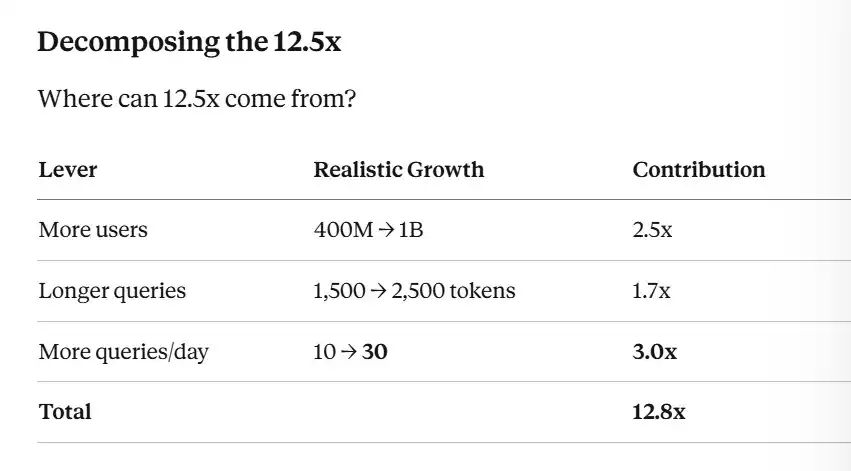

By 2035, we will have a compute power shortage of 8 to 50 times. By then, tokens will become the "kWh" (kilowatt-hour) of knowledge work. Current capital expenditure will prove to be prescient in the future.

However, the shorts may be correct about the current market. According to our preliminary estimates, current investment is about 12 times the earnings of related companies.

This can only be弥补 in one of three ways:

- More users;

- More queries per day;

- More tokens per query (i.e., compute power).

If we limit the increase in tokens required per query to 2x (although this estimate could be off by an order of magnitude, we believe it roughly matches the trend of token/compute efficiency improvement), then the average user's daily queries need to increase from 10 to 30.

For a user manually entering queries, this growth might be unrealistic. But for an AI agent operating on your behalf, it's completely reasonable—because they might trigger an order of magnitude more sub-queries per task than now.

Therefore, we expect the compute gap to reach its most severe point in 2027, and the market will begin to reflect this by mid-year. At that time, equity and credit markets will reprice.

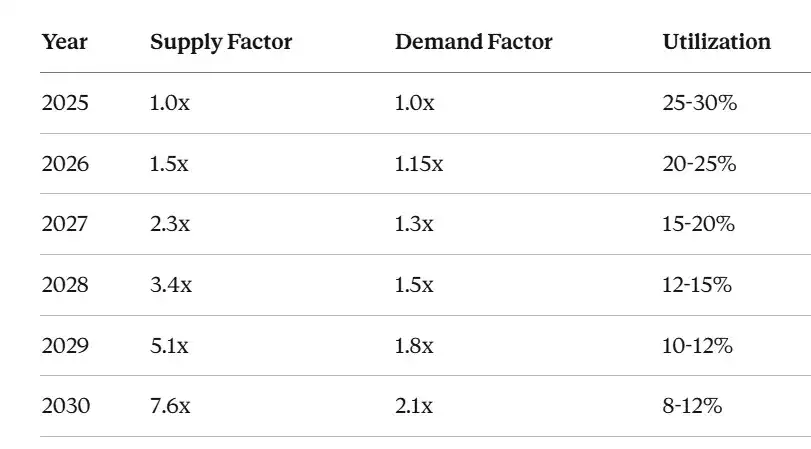

Supply-demand analysis and market forecast:

- Supply: Growing at a compound rate of ~50% per year (hyperscale data centers are expanding疯狂).

- Demand: Growing slowly at ~15% per year until the capability threshold is breached.

- Utilization: Based on current trends, utilization will drop from 25-30% today to 10-15% in 2027-2029.

Google's "1000x expansion in 5 years" goal is a planning scenario, not a demand forecast. Increasing supply alone cannot create demand. Without widespread adoption of "Agentic AI," compute power will lie fallow until technological capabilities cross the critical threshold.

Two Phases:

Phase 1 (2025-2027): Supply Overhang

- Infrastructure construction outpaces demand growth.

- Compute resource utilization drops significantly, economic losses gradually increase.

- This is exactly the stage we are in now.

Phase 2 (2028-2030+): Demand Explosion

- Technological capabilities cross the critical threshold, demand explodes.

- Compute capacity reaches its limits.

- This is the phase the bulls predict.

Both are correct, but they occur sequentially, not simultaneously. The question is: Can investors survive Phase 1 to reap the rewards of Phase 2?

- Short-term: The supply-demand gap weighs on stock performance.

- Long-term: The investment thesis is validated, market returns may increase significantly.

Agentic AI Starts Coming Online

Large Language Models (LLMs) embedded in environments, connected to local data, able to do real work.

This marks the arrival of Phase 2, where token demand per user will grow 10x to 100x, and the market will not only become broader but also deeper.

However, AI adoption is not equivalent to technological maturity; adoption = capability × tools × organizational readiness.

Even if models can perform 4-hour autonomous tasks, they still need to cross the following thresholds:

- Legal industry: Requires integration with document management systems (estimated 2029-2030).

- Finance industry: Requires ERP system integration and regulatory approval (estimated 2031-2032).

- Robotics industry: Requires safety verification and physical infrastructure support (estimated 2030-2035).

Technological capability is necessary, but not sufficient. This is why demand often lags supply by 3-5 years, which is the core logic of the "demand lag" three-threshold model.

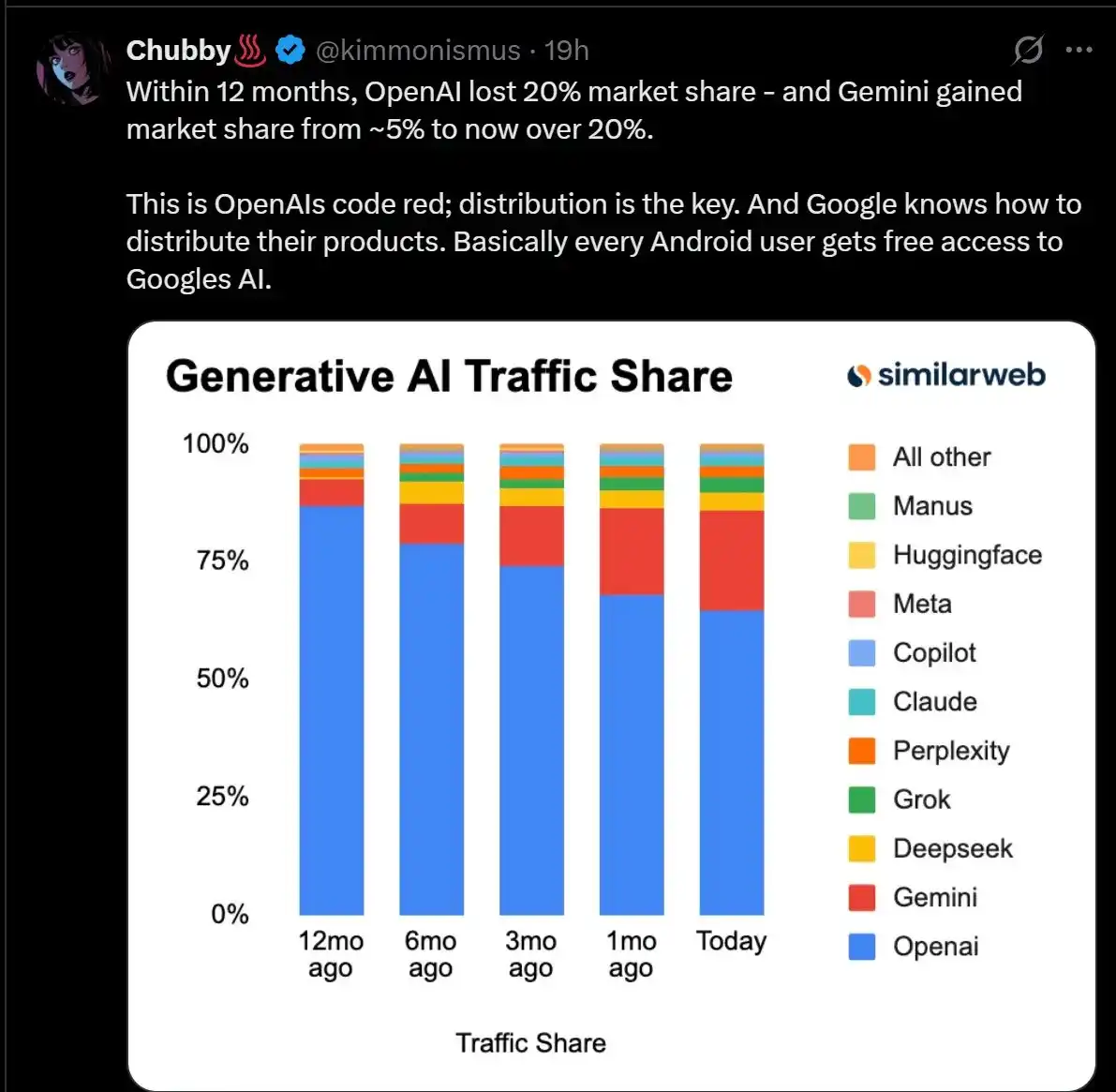

Claude's Market Share Growth

Currently, Claude Code is the best tool for building a single persistent chat. It eliminates the hassle of managing multiple chats and context windows before work restarts.

Hackers (including myself) have started integrating it into products. For example, many charts in this article were assisted by Claude during the holidays: I spent 100 hours building an environment that allows bots to create, store, index, retrieve, and share data within a network—developers, front-end, architects, quants, and data analysts can all collaborate in one channel.

Nonetheless, whether Claude's market valuation can grow further from $350 billion remains to be seen and will depend on various other factors.

While other labs may catch up, Claude demonstrates a leading culture in pushing the frontiers of "Agentic AI." We believe it will begin to have a greater impact, potentially even allowing Anthropic to surpass Perplexity (which is essentially a wrapper tool based on Claude).

The Rise of Local AI

As people gradually integrate AI into their work, they will also integrate it into their own devices. When you actually host and own the model, integration is simpler and more intuitive:

You can adjust the model according to needs; you can深入研究 the model's operation; you don't have to worry about others' servers going down or being hacked.

Although the cloud remains the main hosting ground for frontier models (due to their huge memory requirements), medium-sized models are already smart enough to do real work on consumer-grade hardware.

For example, the NVIDIA 5090 graphics card has 32GB of VRAM, while the SGX desktop device is equipped with 100GB of VRAM (although its CPU and memory performance are reportedly insufficient, and inference speed is average).

A Western Open Source Renaissance? The so-called "Doomer" and China's alignment strategies have indeed had some impact on Western open source development. But we are more certain that these "Doomers" will not admit their mistakes, rather than lacking confidence in future open source development.

LLMs in Games

NPCs in games will no longer be preset scripts, but characters with real "theory of mind."

AI will shape dialogue, characters, and environments,带来更沉浸式的游戏体验.

As long-time players (and investors) of the Grand Theft Auto (GTA) series, we hope TakeTwo delayed the release by a year to achieve this vision. Regardless, we believe it is very likely that this year an indie developer or mod team will have a hit integrating LLMs into a game engine.

Peak Data Center Construction

Even to execute current plans, data center construction requires a lot of work. From planning to legal approval to funding, data center construction takes two years. However, whether the exponential growth in compute power, energy, and data can be achieved to support these data centers remains to be seen.

IV. Long Resources

COMEX vs LBMA Spread Arbitrage

Refer to previous content: If only we had an ISDA agreement and a ship that could transport silver to London and melt it into form.

Long Backwardation in New York, short in London.

Long Copper

- Data centers each need 20-40 tons of copper.

- Electric vehicles, power grids, solar demand are soaring.

- Demand is expected to grow 35%-40% by 2030, but supply only grows 3% per year, with a 5-7 year supply-demand lag.

Long Tin

- Every chip needs solder, and solder is 50% tin.

- The AI explosion means more semiconductor demand, thus driving tin demand growth.

- The civil war in Myanmar has thrown 10% of global tin supply into chaos, Indonesia is also restricting exports, and the West has no aligned production base.

Long Laser/Photonics Technology

Holy photonics, Batman! These stocks have performed very well recently, I wish we had bought more last year!

- Optical interconnect technology is shifting from copper to fiber, co-packaged optics in data centers are developing rapidly.

- Defense sector: Drone economics have become problematic. A $50,000 Shahed drone is shot down by a $10 million Patriot missile, this asymmetric cost-effectiveness needs to be solved. And laser weapons can solve this—each shot costs only pennies, and ammunition is unlimited.

IV. Energy & Compute Infrastructure Investment Opportunities

Long Nuclear Power

AI needs stable baseload power,不受天气影响. The current bottleneck is labor, not technology. Over the past 30 years, the nuclear workforce has been almost decimated and desperately needs replenishment.

Long Natural Gas

Natural gas, as a transition fuel, is helping Europe gradually replace Russian energy supply.

At the same time, AI's demand for dispatchable power (for peak load handling) also makes natural gas a key energy source.

Long Compute Stack

We need more compute resources, including Korean memory chips, US chips, hard drives, networking equipment, and gaming hardware, etc.

Even without more large data center projects, just meeting the demand from existing data centers and local AI is already putting enormous pressure on the supply chains of memory, CPUs, and various components.

V. US Domestic Dynamics

Government Shutdown Risk

Polymarket predicts a 20%-30% chance of government shutdown. The standoff between the MAGA faction and Congress continues. The political deadlock in December did not disappear, the Continuing Resolution (CR) only delayed the problem.

Zero-sum game in US politics is evolving into a negative-sum game, although hopefully this won't last long.

Student Loan Pressure Intensifies

Total US student loan debt has reached $1.7 trillion, the SAVE (loan forgiveness plan) is facing lawsuits.

The government's accounting "fiction" is becoming harder to sustain, default rates are rising. Loan servicers will be the first to feel the most direct pressure.

GLP-1 Drugs Go Mainstream

Peptide drugs (like GLP-1) will achieve universal普及, and may even be covered by insurance.

These drugs are not only for weight loss but may also show potential in heart, kidney diseases, addiction treatment, and even Alzheimer's. If clinical trial results are positive, this will become the most prescribed drug in history.

Horseshoe Theory and Robots

The普及 of AI technology will bring major changes to the labor market, triggering rare consensus between left and right on inequality issues.

$150,000/year programming jobs are disappearing. $45,000/year nursing assistant positions are increasing. This may催生 "New New Deal"-style social policies to address emerging economic and social challenges.

VI. Markets

Japanese Policy Normalization

The Bank of Japan (BOJ) exits Yield Curve Control (YCC), 10-year Japanese Government Bonds (JGBs) trade freely. Japanese investors hold over $1 trillion in US Treasuries. If domestic yields rise, these funds could flow back to Japan. The market moves in August 2024 might have been a preview.

Private Credit Under Pressure

Private credit规模已超过 $2 trillion. Pension funds, chasing yield, invest in illiquid loans that are not marked-to-market.

The Commercial Real Estate (CRE) market is precarious. 2021 Leveraged Buyouts (LBOs) are facing rolling pressure from higher interest rates. If the stock market starts pricing in cash flow gaps, the credit market will not be able to avoid a similar reaction.

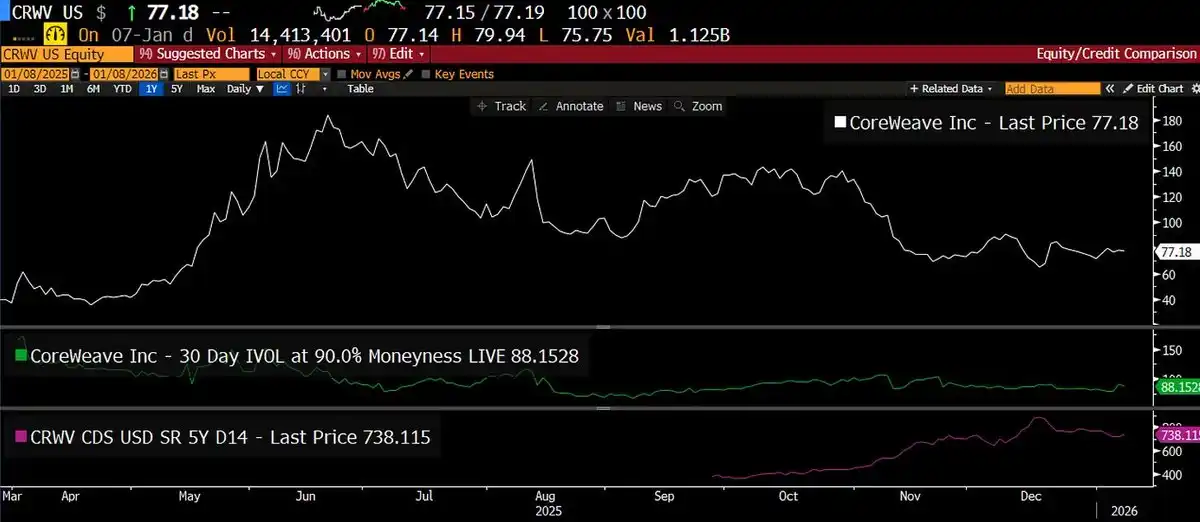

Market Arbitrage Opportunity on GPU-as-a-Service Companies:

Credit spreads are as high as 700+ basis points, while stock volatility is only 80. If analyzing Coreweave's credit spread (700bp) and leverage level using the Merton model, what should the actual volatility of 5-year debt be? This might provide a new market perspective.

A certain company expects Capital Expenditure (Capex) to reach $26 billion, while revenue is only $12 billion, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is $8 billion, resulting in cash flow of -$18 billion, while the company only has $2 billion cash on hand.

In this situation, no wonder someone chose a "straddle" strategy. We can't predict the direction, but we can be sure the status quo is unsustainable.

Oil Price Curve Flattens

Although we have no position in oil, the charts say it all:

WTI (West Texas Intermediate) price collapsed from $75 backwardation to $60 flat.

The return of Venezuelan and Iranian oil supply to the market validates previous assumptions. The "hump" in the mid-term price curve may have been arbitraged away.

The Core Logic Throughout

AI demand is real: Infrastructure is being built out. When agentic AI (agents) can truly do work, usage will grow exponentially.

Energy supply landscape shifts: Metal prices rise, oil prices fall. Nationalism over key resources rises, while crude supply becomes surplus.

Policy environment changes: Greenland has become a policy focus. The Monroe Doctrine is back.

Short-term impact of cash flow gaps: In the short term, cash flow issues will pressure the market. But in the long run, the investment thesis will be validated.

Investment strategy: Adjust positions according to the above logic.