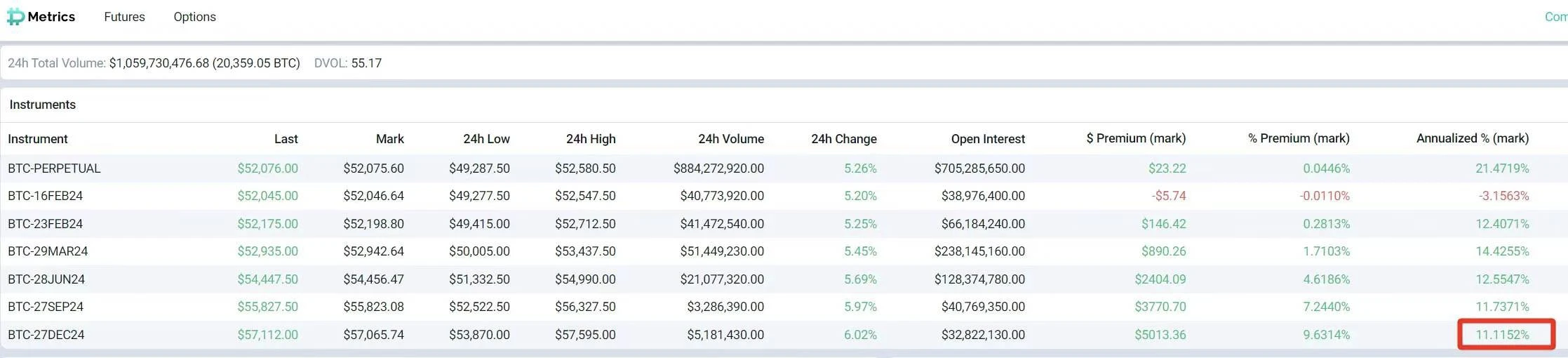

年底的 BTC 和 ETH 的期货升水/溢价纷纷冲回 11% + 。

卖 6 月底 8 万的 BTC 的看涨期权,现在年化收入(币本位)是 13.6% , 但是看这个涨势,我都不敢卖……

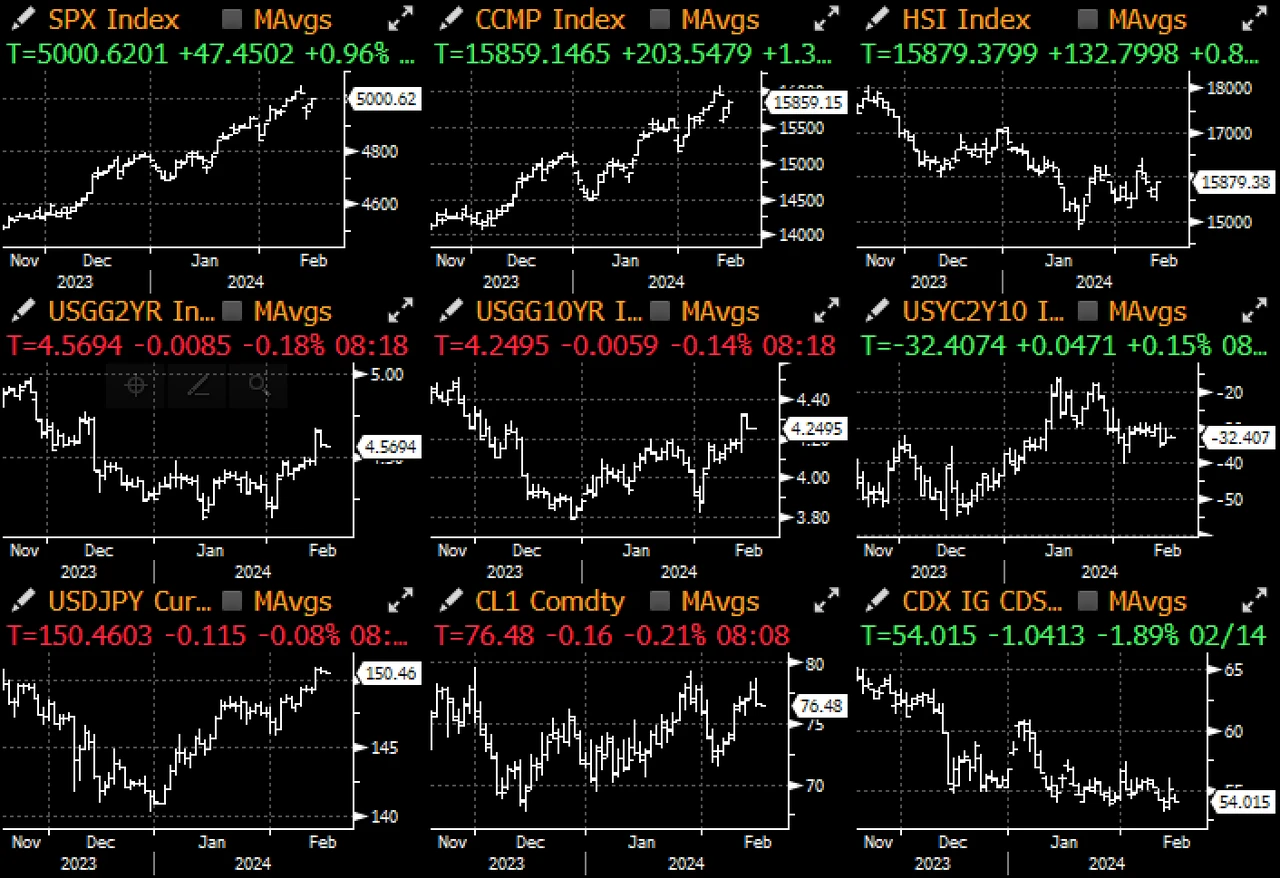

昨天的市场反弹最初由固定收益市场所引领,在地缘政治风险事件(俄罗斯新的太空核武能力)和温和经济数据的推动下,周二 CPI 熊平走势的回撤进一步扩大为大幅反弹。美国 PPI 修正值整体下修至 -0.2% ,核心 PPI 下修至 -0.1% ,使得整体年化率分别降至 1% 和 1.8% ,在昨天令市场失望的 CPI 数据后,这个数据结果令人松了口气。此外,英国 CPI 也大幅低于预期(环比 -0.6% vs 预期的 -0.3% ),英国央行 Bailey 评论称,“通胀放缓将进一步影响薪资谈判”,CPI 结果也使得市场对固定收益的需求异常强劲(30 年期德国公债发行的投标倍数为 2.27 x;Bristol Myers 规模 130 亿的债券供应吸引了 850 亿的资金),为债券反弹增添了动力。

此外,美联储 Goolsbee 意外发表了相当直接和鸽派的评论,称市场“不应因一个月的 CPI 数据而激动”,且“只是一个月的数据,不是几个月”,他还表示,美联储的通胀目标是基于 PCE 而非 CPI,并且“通胀率已经连续 6 到 7 个月往目标接近”,这种明确的鸽派态度与周二 Powell 与立法机构的闭门会议形成了鲜明对比,Powell 在会议上表示,低收入工作者的工资增长一直高于通胀,“而现在对于大多数工作者来说来说越来越是如此”,针对超出预期的 CPI,Powell 重申通胀数据“符合他们先前的预期”,美联储将依赖即将发布的 PCE 报告来提供“更多情报”,同时他拒绝给出任何关于美联储何时降息的线索。

股市也收复了前一日跌幅的 60-70% ,主要受企业股票回购计划的激励,最近宣布回购的公司包括 Las Vegas Sands、Ford、GM、RTX、Airbnb,当然还有 Uber 和 Meta;Uber 在首度实现全年盈利后,宣布 70 亿美元的股票回购计划,而 Meta 早些时候宣布增加 500 亿美元股票回购,并将首度发放股息。

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com