Written by: Cointelegraph

Compiled by: AididiaoJP, Foresight News

Original title: Why Only Dollar-Cost Averaging Can Capture Bitcoin's Long-Term Dividends?

Both backtest data and forward-looking models indicate that using a dollar-cost averaging (DCA) strategy to buy Bitcoin is the best way to invest in BTC. Will this method still work in the next bull market?

Bitcoin has experienced a 50% plunge over the past 5 months, and savvy investors adjust their strategies during such bear markets and correction periods. This strategy is called dollar-cost averaging (DCA), which involves investing a fixed amount regularly, regardless of market conditions.

By examining historical market cycle data and BTC price forward simulations, we can more clearly see how this steady investment approach performs across different entry times and investment horizons.

Five Years of DCA in Bitcoin Yields Substantial Net Gains

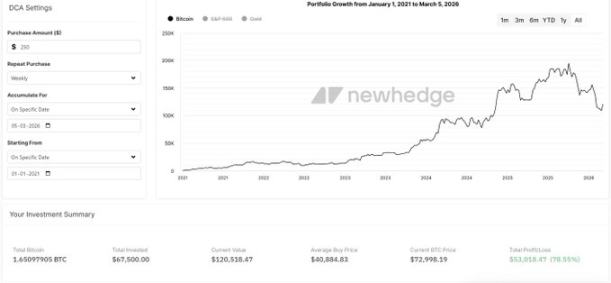

Starting from January 2021, investing $250 weekly in Bitcoin via DCA, the total investment over five years would be $67,500. According to DCA simulation data, this strategy would have accumulated 1.65097905 BTC, with an average purchase price of $40,884.

At Bitcoin's current price of nearly $71,000, this 1.65097905 BTC is worth approximately $120,500, resulting in a profit of $53,000 (a 76% increase). If Bitcoin rises to $100,000, the holdings would be worth about $165,000; and at the cycle peak of nearly $126,000 in October 2025, the holdings would reach a value of $208,000.

Bitcoin DCA Cycle 2021-2026 Source: Newhedge

Now consider a shorter investment period to see the impact of entry timing on early returns. Starting weekly $250 DCA from January 2024, the total investment is $28,500, accumulating 0.36863166 BTC with an average purchase price of $77,312.

At the current price of $71,000, this Bitcoin is worth approximately $26,909, representing a 6% paper loss. At a price of $100,000, the holdings would be worth $36,863; at the cycle peak of $126,000, the holdings would be worth $46,448.

In February this year, Swan Bitcoin analyst Adam Livingston compared on platform X the returns of DCA into BTC versus the S&P 500 index over the past five years. Investing $100 weekly resulted in $42,508 for BTC and $37,470 for the S&P 500, with returns of 62.9% and 43.6% respectively.

Livingston noted that although Bitcoin is highly volatile, historical data shows that persisting with DCA during downturns leads to higher long-term gains.

Weekly $100 DCA: BTC vs. S&P 500 Source: Adam Livingston/X

Long-Term Models: Time is the Key

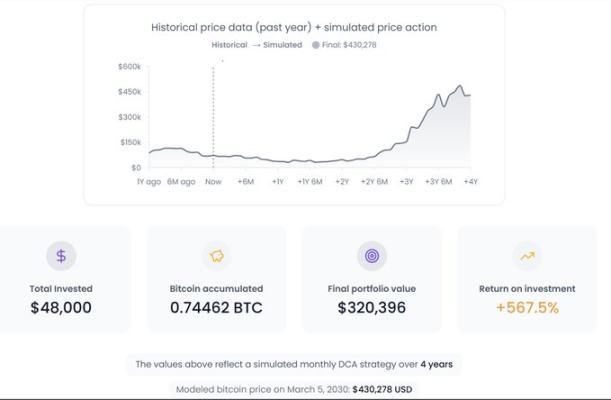

Forward-looking simulation studies have also tested the effectiveness of DCA starting in 2026. Starting a weekly $250 DCA from January 2026 until March 2030 would mean a total investment of approximately $54,250.

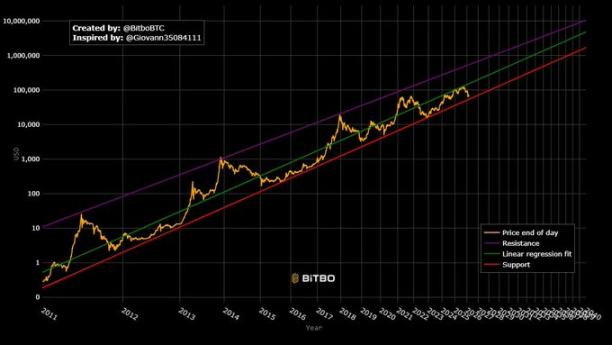

The price prediction is based on Bitcoin's long-term power law growth curve (which tracks the historical relationship between Bitcoin's price and time on a logarithmic scale). This model generates a rising support band and a median trendline, largely consistent with previous market cycles.

Bitcoin Power Law Growth Curve Source: Bitbo.io

Based on this model, analysts estimate the long-term trend support could break above $100,000 by 2028, which also serves as the foundational assumption for future DCA modeling. Bitcoin Well's simulation shows that by March 2030, the median price projection is approximately $430,000.

Accounting for potential price deviations, the model also considers the upper and lower bounds of the power law channel, providing a lower estimate (approx. $274,000) and a higher estimate (approx. $900,000).

Based on these assumptions, four years of DCA would accumulate roughly 0.30 BTC:

-

If BTC price is $274,000, holdings value ~$82,200.

-

If BTC price is $430,000 (median projection), holdings value ~$129,000.

-

If BTC price is $900,000, holdings value ~$270,000.

DCA Investment Results as of March 2030 Source: Bitcoin Well

In November 2025, Bitcoin researcher Sminston With conducted a study using a similar predictive model to test the impact of entry time on long-term returns. The findings revealed that even buying at a price 20% higher than the then price of $94,000 and selling at a price 20% lower than the projected 2035 median price, the remaining holdings after ten years would still yield a profit of nearly 300%.

In this simulation, the final total assets were 7.7 times the initial investment.

The study concluded: Entry timing affects the level of returns, but the duration of holding is the key determinant of the magnitude of gains.