Written by: Thejaswini M A

Compiled by: Luffy, Foresight News

Optimism's story could have had a version of great victory.

In that version, the OP Stack becomes the default infrastructure for Ethereum scaling, dozens of well-funded chains join the Superchain, revenue flows back to the Collective, interoperability features launch smoothly, and the entire ecosystem compounds, looking from afar like a new form of the internet: it belongs to no one, is governed by all, and is self-sustaining.

This version was not a fantasy. For a time, it really looked like it was about to happen. The problem is: everything Optimism did to achieve this vision also made it impossible to protect it.

The OP Stack was released under the MIT open-source license. The importance of this decision almost surpasses any other choice made by Optimism, so it's necessary to clarify its meaning: MIT is currently the most permissive general open-source license. Anyone can take the code, develop it further, modify it, commercialize it, or even do a full fork. No royalties, no revenue sharing, no obligations whatsoever—you don't even have to say thank you.

Optimism made this choice deliberately. The logic is simple: if you want to become the default framework, you must every reason not to adopt you. Reduce the onboarding cost to zero, make the protocol uncontroversial, and allow any team, company, or exchange with a development budget to launch an OP Stack chain permissionlessly, without signing any documents, with just one click.

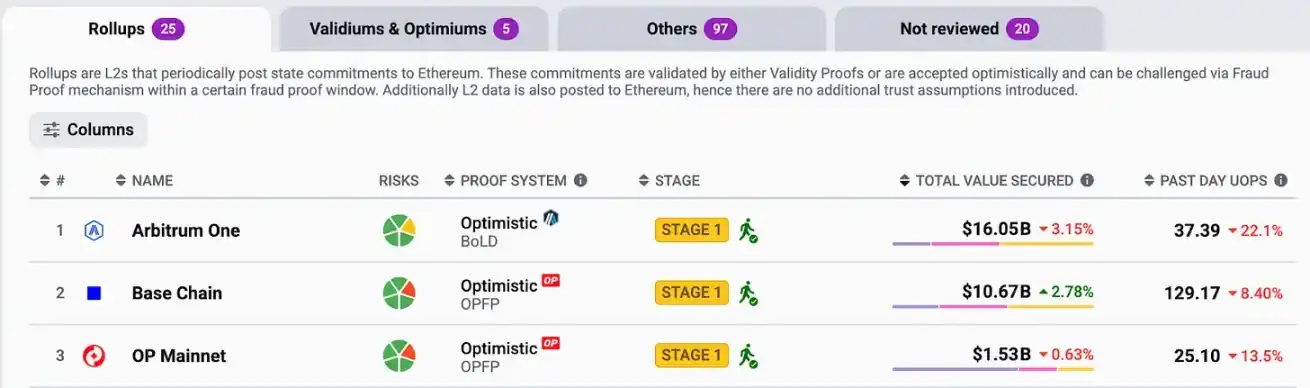

It succeeded. By mid-2025, the OP Stack processed 69.9% of L2 transaction fees, with 34 chains live on mainnet. Coinbase, Uniswap, Kraken, Sony, and Worldcoin were all using it. When people talked about Ethereum scaling, they were usually talking about something built on Optimism's code.

Optimism won the standards war.

Then, the largest chain it helped build announced it no longer needed this relationship.

On February 18, 2026, Coinbase published a blog post with a carefully worded, affectionate title—a typical writing style for companies announcing major events without wanting to sound harsh. The Base chain would integrate its codebase, accelerate its development cycle, and reduce coordination costs. The post expressed gratitude and praised the cooperation.

Upon the news, the OP token plummeted 28% within 48 hours, with selling volume surging 157%. In just a few days, the token was down 89.8% from a year ago, standing at just $0.12 at the time of writing, compared to a high of $4.85 in March 2024. OP Labs CEO Jing Wang wrote on X: "This is a blow to short-term on-chain revenue."

To understand why, you must understand what the Superchain was truly selling.

The OP Stack is free. The license makes this permanent and irrevocable. So why would any chain be willing to share revenue with the Optimism Collective? Optimism's answer was: interoperability. Join the Superchain, and your chain isn't just a chain, but part of a unified network—liquidity and users can flow freely between all member chains, developing on one chain is equivalent to developing on all, achieving a 1+1>2 effect.

This was its value proposition: pay 2.5% of total revenue or 15% of net profit, and in return, you get something no single chain could build alone.

But interoperability never launched.

Optimism was originally scheduled to launch native interoperability on mainnet in early 2025, but it didn't arrive. A long-time governance delegate stated: "Despite years of technical development, unfortunately, this was not achieved."

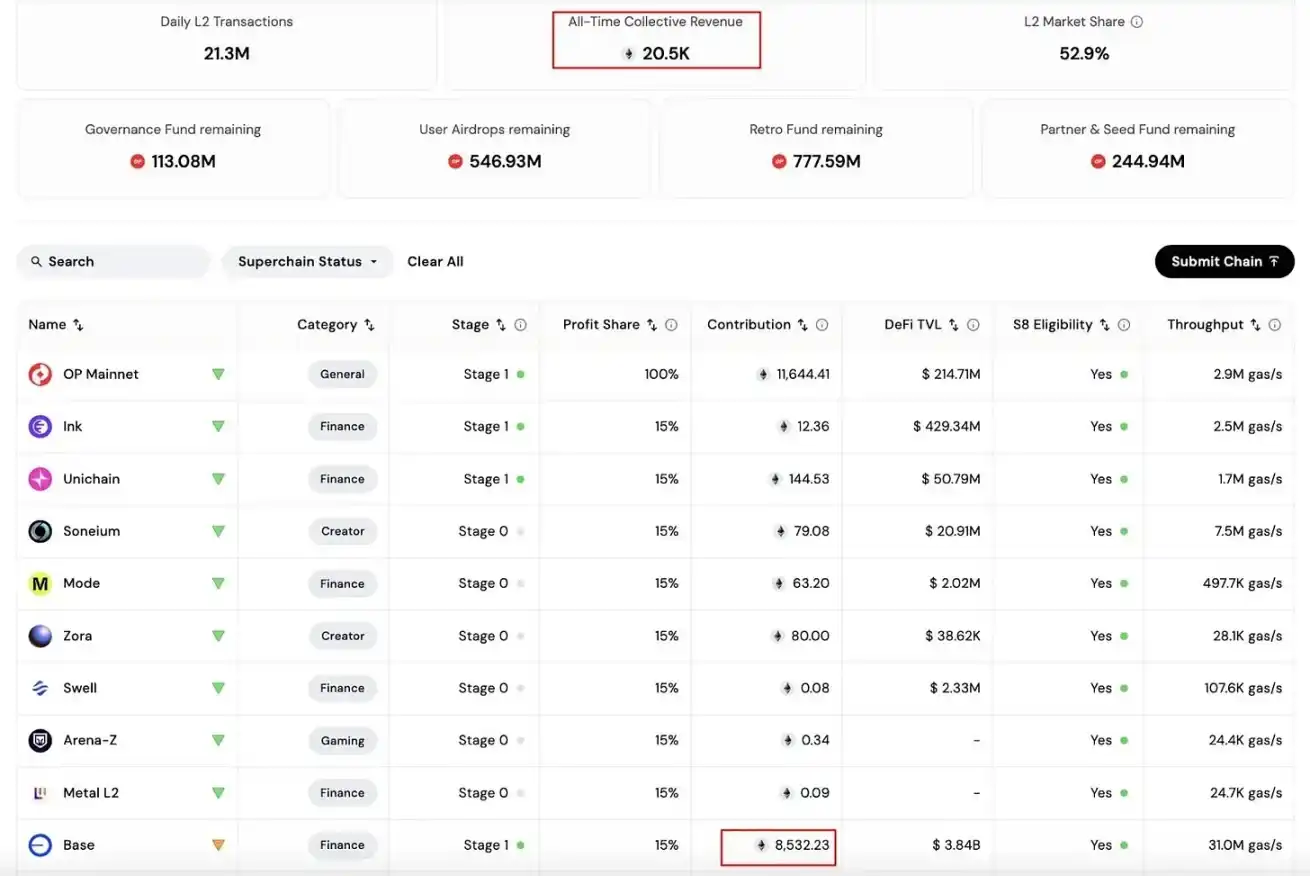

Members were paying "taxes," but the product this money was supposed to support remained theoretical. What the Superchain actually provided was only a shared brand, shared governance costs, and a revenue obligation. The thing that was supposed to make this obligation worthwhile was always "just around the corner." Meanwhile, Base continued to grow.

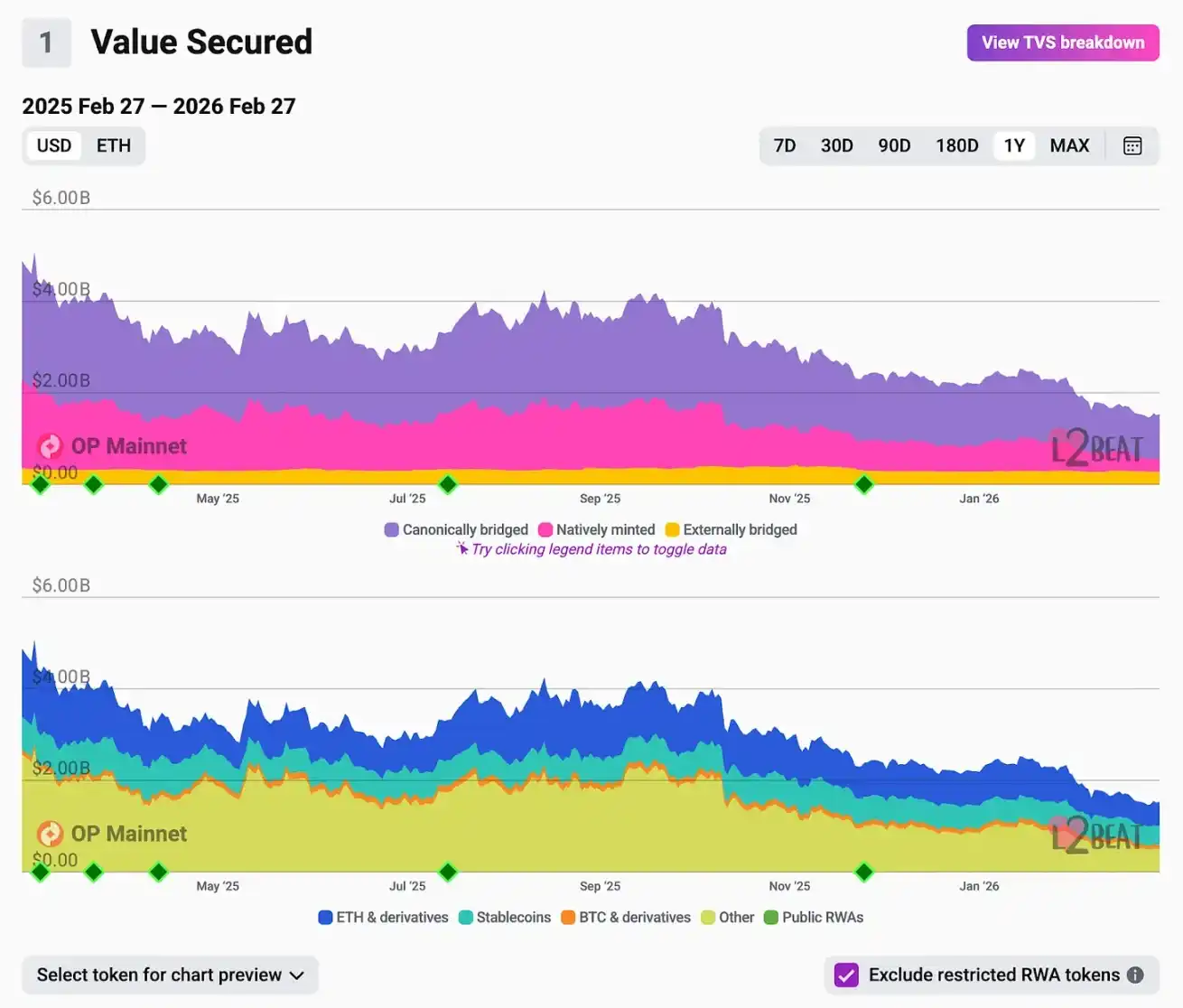

By January 2026, Base contributed 96.5% of all gas fees flowing into the Optimism Collective—almost all of it. Base's transaction volume was about 4 times that of OP Mainnet, DEX volume about 144 times, and gas fee generation 80 times. During their partnership, the Collective received a total of about 14,000 ETH in its lifetime, with Base contributing 8,387 ETH, and its monthly revenue share approached 100%.

The other 33 Superchain members were on the list but economically insignificant. In the first half of 2025, the second most active member, World Chain, accounted for only 11.5% of Superchain computation, OP Mainnet itself for 11.4%, and Ink, Soneium, and Unichain together for less than 13%.

Beyond its name, the Superchain had effectively become a one-chain ecosystem. The alliance was real on paper, but economically it was entirely Base.

In any alliance, there comes a point where the strongest participant asks the obvious question: What am I actually getting out of this?

Almost every successful open-source story follows this same logic. MongoDB built a widely used database, released it open source, and then watched as AWS built a profitable托管 service on top of it without paying a dime. AWS controlled traffic distribution, MongoDB set the standard. Value flowed to the entity that controlled the users, not the one that wrote the code. MongoDB eventually changed its license, and AWS forked it into OpenSearch.

Elastic and Redis went through the same cycle. The details differ, but the structure is identical: the infrastructure maker establishes the standard, a giant with distribution adopts it, the giant harvests the value, and eventually the giant internalizes the tech stack and leaves.

Optimism is the crypto version of this story.

Arbitrum saw this logic clearly and made a different choice. Its Orbit chains, the counterpart to the Superchain, use the Business Source license, with revenue sharing based on contractual obligations, not voluntarism. When your largest partner can leave without legal consequences, the alliance's survival depends entirely on its willingness to stay. Arbitrum did not want to build an ecosystem based on that assumption.

The official reason Base gave for leaving was technical: unifying the codebase meant faster development, aiming for 6 major upgrades per year instead of 3; independent control of the security council meant no external body could delay or block network decisions; reducing dependencies meant Base could keep pace with Ethereum's own upgrades without waiting for governance processes it didn't control.

Coordinating across multiple codebases is indeed slower than controlling your own tech stack.

But there was another reason, left unstated. Morgan Stanley estimated that a Base token could bring Coinbase about $34 billion in equity value and raised its price target to $404. As long as Base was paying 15% of its net profit to the Collective of an external protocol, designing a Base token with reliable value capture mechanisms was structurally very difficult. Leaving the Superchain was a prerequisite, not a side effect. Both motives pointed in the same direction, and Base did just that.

What remains for Optimism is not nothing, but one must be honest about the change that has occurred.

OP Mainnet still holds $1.5 billion in TVL. On the same day Base announced its departure, ether.fi stated it would migrate its on-chain credit card product to OP Mainnet, bringing 70,000 active cards, 300,000 accounts, and over $160 million in TVL. A few weeks earlier, the Collective had just passed a buyback plan, using 50% of sequencer revenue for monthly OP buybacks.

The ether.fi partnership gives OP Mainnet a clearer use case in consumer payments. But ether.fi's annualized fee contribution is only about $13 million, while Base's profit in 2025 alone was $55 million. The revenue base underpinning the buyback plan no longer exists. Token unlocks for investors and contributors continue at a rate of about $32 million per month.

Pivoting to enterprise services might be the right move. OP Labs has raised over $175 million, possesses top engineering talent, and there is genuine demand from institutions for hosted OP Stack deployments—entities that want to launch a chain but don't want to build their own maintenance capabilities. Jing Wang positioned it as "the Databricks of blockchain infrastructure," a reasonable analogy. It's a services business, and it could work.

But a services business is completely different from a network generating compound protocol revenue through an alliance. The OP token's valuation was priced for the latter. The market understood this less than 12 hours after the blog post was published.

Zooming out. What happened on February 18th is essentially not just about Optimism.

For most of 2024, over 50 L2 networks competed for users and liquidity. By the end of 2025, Base, Arbitrum, and Optimism together handled nearly 90% of L2 transactions, with Base alone exceeding 60%. Small Rollups saw activity drop 61% since June. The Dencun upgrade brought a 90% fee reduction, compressing profit margins across the industry. Base was the only L2 to be profitable in 2025.

The chains that survived, and those that will define this layer in the coming years, are not necessarily the most technically proficient. They are the chains with structural reasons for user retention. Exchange-backed chains (Base, Ink, Mantle) leverage the existing user base of their parent company for built-in distribution; every Coinbase user wanting to get on-chain is just one click away from Base. DeFi-native chains like Arbitrum and Hyperliquid hold their ground based on liquidity depth that is difficult to rebuild elsewhere.

Technology can be forked. The OP Stack proved this perfectly. What cannot be forked is Coinbase's relationship with its 100 million users, or Arbitrum's tens of billions in open interest. Lasting value lies here, almost regardless of which license you choose for your codebase.

Optimism's decision to release the OP Stack under a permissive open-source license was the right choice. It led to the broadest adoption among L2 frameworks, making Optimism the infrastructure standard for an entire generation of Ethereum scaling. Without this decision, Base might have been built on other technology, or might not have appeared at all.

But the decision that made it all possible also made exit costless. When Base grew large enough, with its own users, its own token roadmap, and its own reasons for pursuing full infrastructure sovereignty, there was nothing in the license to constrain it, and the promise of interoperability wasn't enough to give it a reason to stay.

Optimism won the standards war. It's just that this standard didn't come with a mechanism to capture the value it created. A token price of $0.12 is the market's final pricing of all this value.