• The depreciation of the US dollar is the result of a combination of factors: declining real purchasing power, the gradual intensification of fiscal dominance, and long-term changes in real interest rates and holding costs.

• The traditional banking system, constrained by regulation, capital requirements, and risk weights, creates a spillover demand for dollars, which stablecoins are filling precisely in this gap.

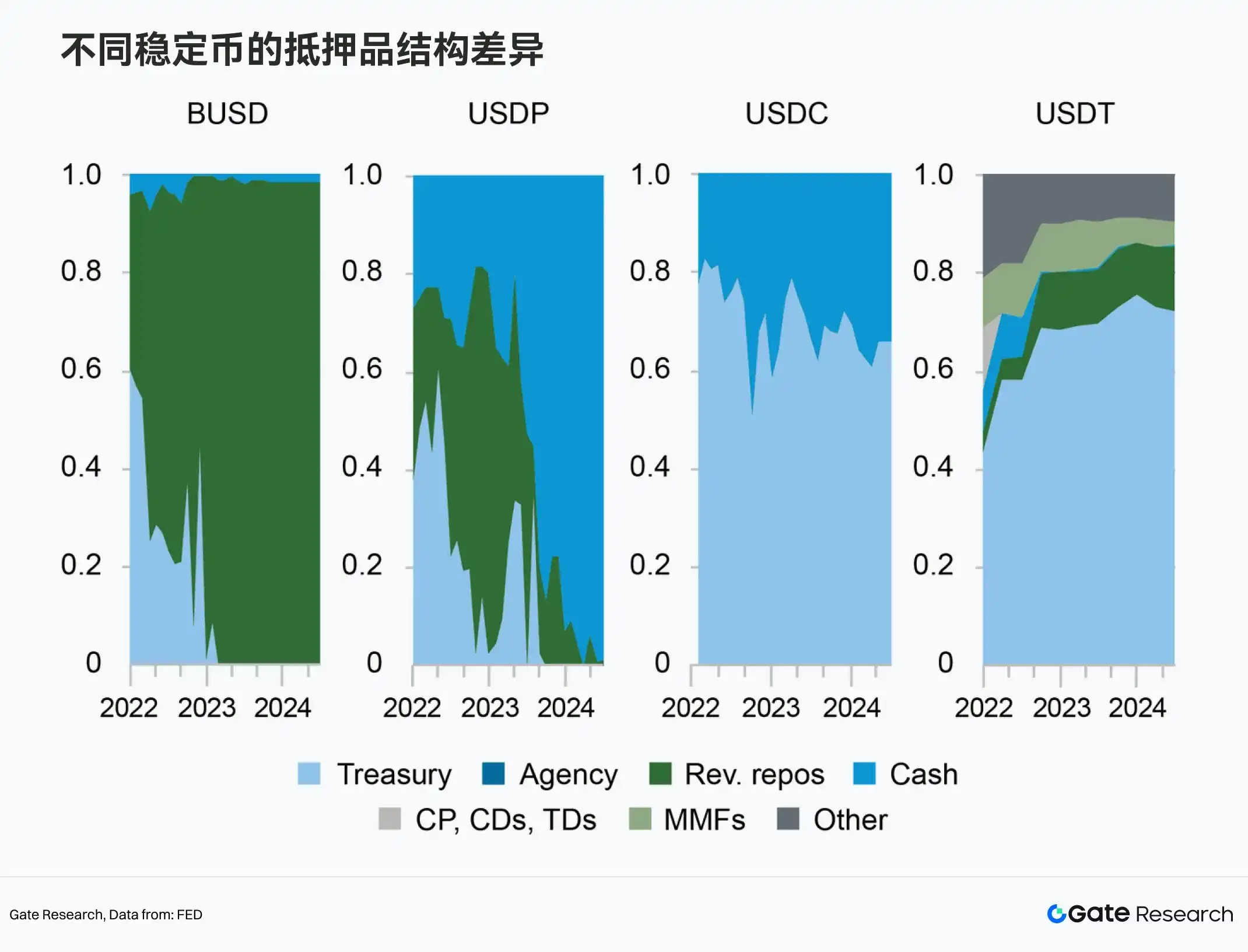

• Due to regulatory and business positioning differences, the collateral structures of different stablecoins vary, forming an implicit credit hierarchy among them.

• The quality of stablecoin collateral, transparency, and issuer credibility are becoming core variables determining their price stability, liquidity priority, and long-term capital preference.

• After reaching a certain scale, stablecoins have begun to become a significant structural force influencing short-term US dollar interest rates.

• Looking ahead to 2026, stablecoins are more likely to play the role of a US dollar "reservoir" and distribution layer; their reserve assets are forming a stable bid for short-term US Treasuries, which in turn is affecting the dollar's own pricing structure.

1. Introduction: The Dollar is Depreciating, But It's Not Exiting

Discussions surrounding the US dollar have become noticeably more complex recently. On one hand, the Fed's gradual shift towards interest rate cut expectations starting in 2024 has led to a peak and subsequent decline in real interest rates. On the other hand, persistent large national fiscal deficits, high pressure from Treasury supply, and long-term fiscal sustainability are repeatedly placed under the spotlight. Against this backdrop, narratives such as "dollar weakness," "dilution of dollar credit," and "accelerating de-dollarization" frequently emerge, seemingly forming a market consensus: the dollar is at a significant structural inflection point.

Superficially, this judgment is not entirely unfounded. Inflation continues to erode the dollar's real purchasing power, fiscal deficits and debt expansion undermine its certainty as a long-term store of value, and frequent geopolitical friction and financial sanctions have prompted some countries and institutions to consciously reduce their direct reliance on the traditional dollar system. Whether from macroeconomic indicators or the political and institutional environment, the dollar appears to be weakening.

However, shifting the perspective away from macro narratives to observe actual behavior and usage structure of funds reveals a counterintuitive yet crucial phenomenon: the dollar is not being abandoned. On the contrary, globally, the dollar still firmly occupies the core position for pricing, settlement, and safe-haven assets. Particularly noteworthy is that on-chain dollars, represented by stablecoins, have not only failed to shrink in recent years but have shown a trend of continuous expansion.

Whether in crypto asset trading, DeFi collateral and liquidation, cross-border transfers, or daily payments in emerging markets, the frequency of dollar usage has not declined alongside discussions of dollar depreciation; it has simply increasingly bypassed the traditional banking system. This constitutes a core contradiction worth exploring in depth: if the dollar is depreciating, why is the world still chasing it? If dollar credit is under pressure, why is its usage spreading, albeit in a different form?

Starting from this contradiction, this article attempts to move beyond simplistic binary judgments of "strong or weak" or "leaving or staying" to re-examine the real flow of dollar demand against the backdrop of dollar depreciation in 2026, with a focus on analyzing how stablecoins, as an extra-systemic form of dollar, are meeting the marginal dollar demand squeezed out by traditional financial structures.

1.1 Dollar Depreciation is More Than Just a Concept

When discussing dollar depreciation, the most intuitive understanding is often the dollar weakening against other currencies or a decline in its exchange rate. In reality, however, this understanding is too narrow. Dollar depreciation is more like an ongoing structural process, not necessarily manifesting as an immediate sharp decline, but slowly and continuously changing the real cost of holding dollars through the influence of multiple factors.

The first layer is the decline in real purchasing power. Even if the dollar remains stable nominally, or even appreciates against other currencies in certain phases, as long as inflation persists, the real wealth of dollar holders is constantly eroded. From an economic perspective, nominal price stability is not equivalent to purchasing power stability. For example, the same 1 dollar can buy one apple in one country but a full dinner in another.

The second layer is the gradual intensification of fiscal dominance. When a country runs persistent fiscal deficits and its government debt scale continues to expand, the independence of monetary policy becomes structurally constrained. In such an environment, the objectives of monetary policy will increasingly serve the sustainability of debt—meaning that lowering interest rates becomes a choice to artificially suppress financing costs and create operational space for fiscal policy. When monetary policy begins to shoulder the function of supporting fiscal policy, the long-term value anchor of the dollar naturally comes under pressure.

The third layer is the long-term change in real interest rates and holding costs. When nominal interest rates are suppressed and inflation is high, real interest rates tend to be low or even negative. This implies an implicit cost to holding dollars itself, where savers are无形中 subsidizing debtors. At this point, the dollar remains the world's most important currency, but "whether holding dollars is worthwhile" becomes the key question.

1.2 Fed Monetary Policy and Dollar Trends: The Policy Cycle Provides Space for Stablecoin Development

Monetary policy determines the pace and channels through which the aforementioned dollar depreciation mechanism transmits to the real world. Policy choices at different stages directly affect the strength and usage cost of the dollar.

• 2008–2014: The QE Era, Passive Dollar Weakness

○ Following the global financial crisis, the Fed launched multiple rounds of quantitative easing, massively expanding its balance sheet and压低 interest rates to repair the damaged financial system. Dollar supply expanded rapidly during this phase, with real interest rates remaining low for an extended period, significantly reducing the dollar's scarcity. At this time, there were more dollars, but they weren't necessarily "easy to use"; liquidity was largely trapped within the banking system and financial assets.

• 2015–2018: Gradual Hiking Cycle, Structural Dollar Strength

○ As the economy recovered率先, the Fed began raising rates and shrinking its balance sheet, leading to global capital flowing back into dollar assets and putting pressure on emerging markets. In this phase, the dollar re-established itself as the global monetary anchor, its availability decreased, its usage cost increased, and its financial attributes were significantly reinforced.

• 2019: Policy Shift Towards Easing, the Dollar's Peak Begins to Crumble

○ Against the backdrop of a global economic slowdown, the Fed conducted preventive rate cuts. The dollar index oscillated at high levels, its strength somewhat loosened but not fundamentally reversed yet.

• 2020–2022: Post-Pandemic Aggressive Hiking, the Dollar's Super-Cycle

○ During the pandemic, the Fed implemented unlimited QE and zero-interest-rate policy (ZIRP), leading to unprecedentedly宽松 dollar liquidity; subsequently, high inflation quickly backlash, forcing the Fed to undertake the fastest rate hike cycle in history. During this phase, the dollar index hit a 20-year high, simultaneously undermining confidence in the dollar's long-term value.

• 2023–2025: Rising Rate Cut Expectations, the Dollar Enters a Structural Decline Phase

○ As inflation subsided, markets have persistently anticipated a path of rate cuts since 2023. Although the dollar remains at high levels, marginal tightening has ended, with fiscal deficits, debt规模, and the long-term interest rate level beginning to dominate the dollar narrative. It is precisely in this phase that a key change occurred: the dollar is still needed, but dollars within the traditional system have become slower, more expensive, and more constrained.

2. Traditional Dollar Deceleration: How Stablecoins Meet Spillover Demand

As monetary policy adjusts and fiscal constraints加重, the traditional banking system, constrained by regulation, capital requirements, and risk weights, is actively收缩 its dollar balance sheet. Simultaneously, strict AML, cross-border compliance, and account access thresholds exclude a large number of non-core users and marginal funds from the traditional dollar system, creating structural spillover demand for dollars. Stablecoins are恰恰 filling this gap, providing quasi-dollar liquidity with lower friction, becoming an important container for extra-systemic dollar circulation.

2.1 Dollar Depreciation ≠ Decline in Dollar Usage, The Counter-trend Expansion of On-Chain Dollars

When discussing dollar depreciation, a common intuition is: if the dollar's purchasing power is declining and its credit is being questioned, its usage scope and demand should contract simultaneously. But the reality is恰恰 the opposite. Over the past few years, especially after experiencing interest rate hike shocks, bank risk events, and剧烈 volatility in risk assets, stablecoins—this on-chain dollar form—have not shrunk accordingly but have instead shown signs of recovery or even expansion across multiple dimensions.

First, in terms of total value, the overall market capitalization of stablecoins has gradually stabilized and rebounded after periodic pullbacks. By early 2026, the total stablecoin market cap had突破 $3.09 trillion, hitting a new historical high. Although the market structure has changed and the market share among different stablecoins has adjusted, dollar stablecoins as a whole have not been marginalized. This phenomenon itself indicates that the market has not abandoned dollar-denominated tools due to concerns about the dollar's long-term prospects.

Second, in terms of usage, the activity level of stablecoins has significantly increased. Throughout 2025, the total on-chain transaction volume of stablecoins was approximately $33 trillion, a year-on-year increase of about 70%. During the same period, USDT and USDC dominated all stablecoin transactions, with USDC processing about $18.3 trillion in on-chain transactions and USDT about $13.3 trillion, together accounting for the vast majority of the flow.

Looking at monthly transaction volume, the monthly transfer volume of stablecoins on main chains like Ethereum once reached levels around $850 billion, demonstrating their core role in trading, cross-chain流动, and pricing.

In other words, even as risk preferences towards the dollar change at the macro level, stablecoins in crypto trading have not retreated to the margins but continue to play a crucial role in liquidity and settlement.

2.2 Stablecoins as "Shadow Dollars," Meeting Demand Squeezed Out of the Banking System

In recent years, the friction in cross-border dollar settlement has continuously increased. Dollar transfers within the traditional banking system often involve multiple intermediaries, complex compliance checks, and high time and monetary costs. Against the backdrop of rising geopolitical risks, issues like account freezes, payment channel disruptions, and sanction compliance have also made using the dollar itself non-neutral.

In such an environment, stablecoins have begun to assume a function similar to shadow dollars. They do not challenge the dollar's计价 status but, without changing the dollar standard, reduce institutional friction and meet marginal demand. For example, for many cross-border merchants, the core appeal of stablecoins lies not in yield but in accessibility, transferability, and settlement certainty, specifically: not relying on local bank accounts,不受 business hours限制, and near-instant cross-border transfers.

It is worth emphasizing that the essence of stablecoins is US dollar liabilities issued by private entities. This means the value of stablecoins in investors' hands does not come from sovereign credit directly but is built on trust in the issuer's balance sheet. To support this trust, mainstream stablecoin issuers typically heavily allocate their assets to short-term US Treasuries and repo assets collateralized by Treasuries.

In 2024, these stablecoins purchased $40 billion in US Treasuries, a规模 comparable to the largest local government money market funds and exceeding the purchase volumes of most foreign investors.

This structure not only maintains the peg between stablecoins and the US dollar but also allows stablecoins to functionally延续 the dollar's settlement attributes while游离于 the public financial system in terms of credit hierarchy. For issuers, they are an off-balance-sheet liability; for users, they are a form of dollar that can be held and transferred without a bank account. This is not the disappearance of dollar credit but its migration.

It must be stressed that stablecoins are not necessarily safer than traditional dollars, nor are they necessarily superior in risk control. They lack central bank lender-of-last-resort support and deposit insurance mechanisms; under a confidence shock, they can still experience volatility or even de-pegging.但从 a usage perspective, stablecoins are often more convenient—lower barriers to access, faster transfer speeds, and fewer usage restrictions.

2.2.1 Differences in Collateral Structure Among Stablecoins Due to Regulation and Business Positioning

On the surface, there are huge gaps in the choices different stablecoins make regarding "where assets are held": some are almost entirely composed of cash and short-term Treasuries, while others still include loans, crypto assets, and other non-standard assets. In fact, this divergence is the result of the long-term interplay of the regulatory environment, business objectives, and risk preferences of the issuers.

Differences in regulatory constraints are the core watershed. Stablecoins like USDC, BUSD, and USDP have their issuing entities primarily located in heavily regulated jurisdictions. This means the issuers have extremely limited freedom in asset allocation,几乎只能 choosing the "cleanest," most监管-acceptable asset types.

Specifically, cash, reverse repos collateralized by US Treasuries, and ultra-short-term Treasuries become the mainstay of these stablecoins' reserves. These assets are not yield the highest, but they are structurally clear, risk-explainable, and highly liquid, making it easier to demonstrate solvency to regulators and the market under any stress scenario.

In contrast, USDT operates in a more offshore regulatory environment. Its historical disclosure transparency has been lower, and it faces relatively looser direct regulatory constraints. This gives USDT greater leeway in asset allocation. Furthermore, USDT has long played a market-oriented role rather than being a strictly compliant financial product, hence its reserves have historically included commercial paper, loans, and even non-stablecoin crypto assets.

Differences in business positioning further amplify this structural divergence. The core goal of USDC and USDP is very clear: avoid de-pegging at all costs. To achieve this, they are willing to sacrifice some yield to prioritize liquidity and transparency. In this model, stablecoins act more like passive monetary instruments. USDT's goals, however, are more偏向 scale, usability, and global coverage. At certain stages, USDT's reserves were not only used to passively support stablecoin redemption but also for lending, supporting exchanges and market makers, and even allocating non-stablecoin crypto assets. This makes USDT functionally closer to a shadow bank with financial intermediary attributes, rather than just a simple payment medium.

2.2.2 Stablecoins Are Not Homogeneous; "Safety Tiering" Begins to Dominate Pricing

In the early stages of the crypto market, stablecoins were largely seen as a functional tool—as long as they were pegged to the dollar and priced near $1, they were默认 considered equivalent. This "homogeneity assumption" was rarely challenged during平稳 market periods, but past rounds of systemic shocks have gradually broken this perception.

The Terra event was the first real watershed. The collapse of UST in 2022 was not due to an external financial shock but the rapid failure of its own structure under reversed confidence. This event made the market clearly realize for the first time: even if nominally stable, if缺乏 real, realizable dollar asset backing, a stablecoin will almost inevitably de-peg or even go to zero under stress. From that moment on, "whether it has real, liquid US dollar asset backing" became the first threshold for distinguishing stablecoin safety.

The FTX collapse, also in 2022, further reinforced the second layer of judgment: having assets alone is not enough; transparency and issuer credit are equally important. Although FTX itself was not a stablecoin issuer, its commingling of funds and information opacity quickly evolved into a liquidity crisis, severely impacting market trust in centralized financial intermediaries. This event indirectly changed the risk pricing logic for stablecoins, pointing to the fact that stablecoins are no longer just about "whether there are assets" but "whether the assets are credible."

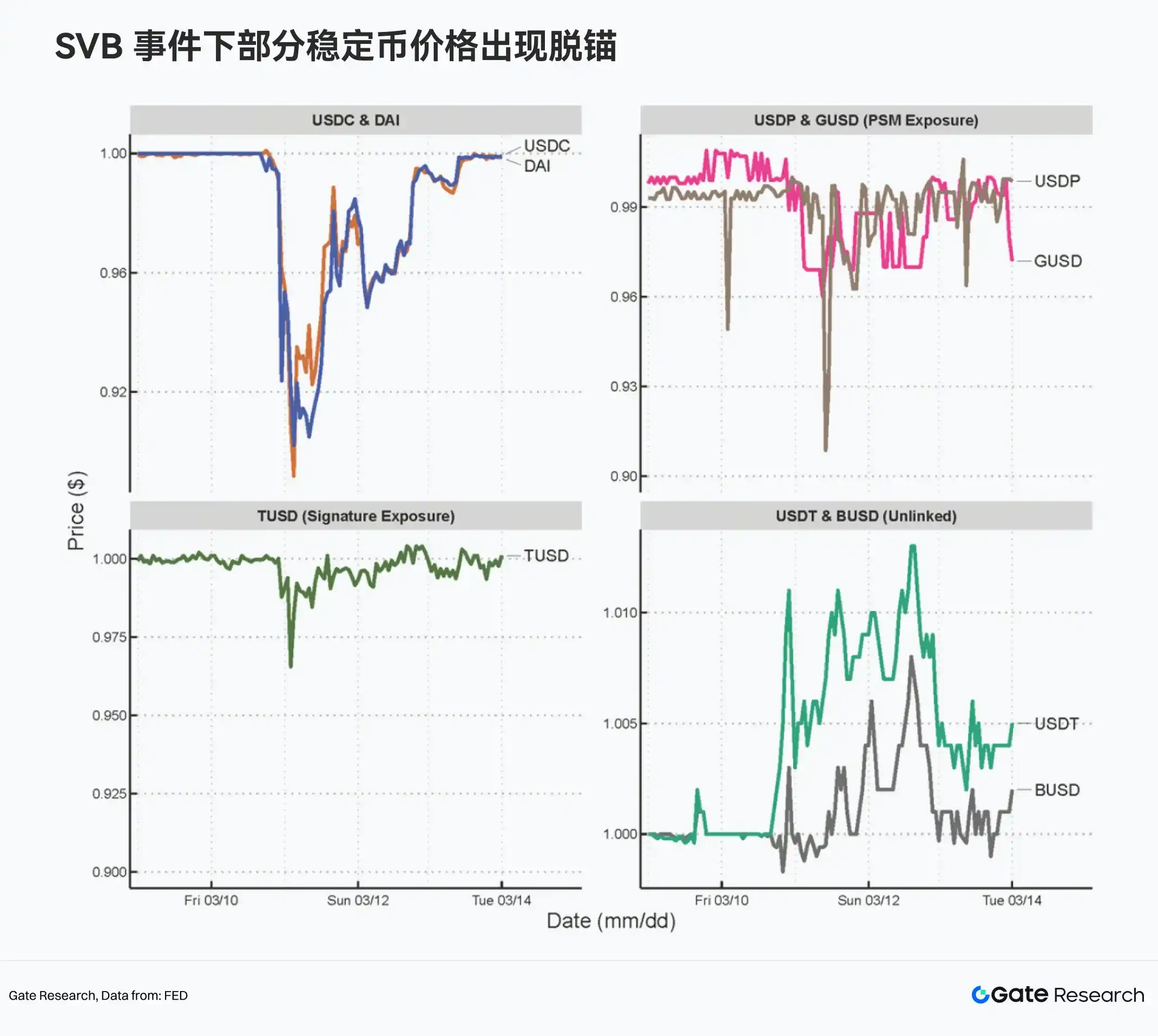

What truly brought safety tiering clearly to the forefront was the Silicon Valley Bank (SVB) incident in 2023. During this shock, USDC briefly lost its peg as part of its reserves were held at SVB, with its secondary market price一度 falling to around $0.86. Meanwhile, USDT, which the market perceived as having no direct risk exposure to the event, traded at a premium in some scenarios. This contrast was highly symbolic: for the first time, stablecoins were explicitly differentiated by the market into "relatively safe" and "relatively unsafe" dollars within the same time window, expressed directly through price.

Simultaneously, this tiering did not only occur in centralized exchange markets. In the DeFi system, automated mechanisms反而 amplified risk transmission. Taking MakerDAO's "Peg Stability Module" (PSM) as an example, other stablecoins like DAI maintain a 1:1 exchange rate with USDC through the PSM. When USDC de-pegged, arbitrage行为 quickly drained the PSM's liquidity, causing stablecoins that were not directly exposed to SVB risk (e.g., DAI, USDP) to also experience price fluctuations. The technical module originally designed as a connector became an accelerator of risk under stress scenarios.

This series of events collectively points to one conclusion: the market no longer views stablecoins as a single, homogeneous dollar substitute but has formed an implicit credit hierarchy within them. Furthermore, collateral quality, transparency, and issuer credibility are becoming core variables determining their price stability, liquidity priority, and long-term capital preference.

3. Stablecoins Are Beginning to Influence Short-Term Dollar Funding Prices in Reverse

Some academic research, starting from monetary system theory, has proposed a so-called "hybrid monetary ecosystem model." In this framework, stablecoins are not shadow assets游离于 the dollar system but are digitally native dollars issued by private entities, which, together with central bank money and commercial bank deposits, constitute a layered operating dollar system. In this system, stablecoins are not passively embedded but, through interaction with regulatory rules, central bank policies, and traditional financial markets, substantively participate in the operation of liquidity distribution and payment systems.

3.1 From Data to Conclusion: The Inverse Relationship Between Stablecoin Scale Expansion and Short-End Treasury Yields

Against this backdrop, the function of stablecoins naturally does not stop at payment or settlement. As their scale and usage depth continuously expand, stablecoins have begun to exert feedback effects on the dollar system itself, particularly showing influence in the short-term funding market. They are no longer just recipients of dollar liquidity but have evolved in recent years into an important marginal force capable of inversely influencing short-term dollar funding prices.

Factually, the reserve assets of mainstream stablecoins like USDT and USDC are highly concentrated in highly liquid instruments such as short-term Treasuries, reverse repos, and cash. This is not accidental but an inherent requirement of the stablecoin issuance mechanism:既要 ensuring随时 redemption,又要 obtaining some yield under compliance and risk control premises. As stablecoin issuance scale continues to expand, this配置 structure naturally意味着—stablecoin issuers are becoming long-term, stable buyers of short-end dollar assets.

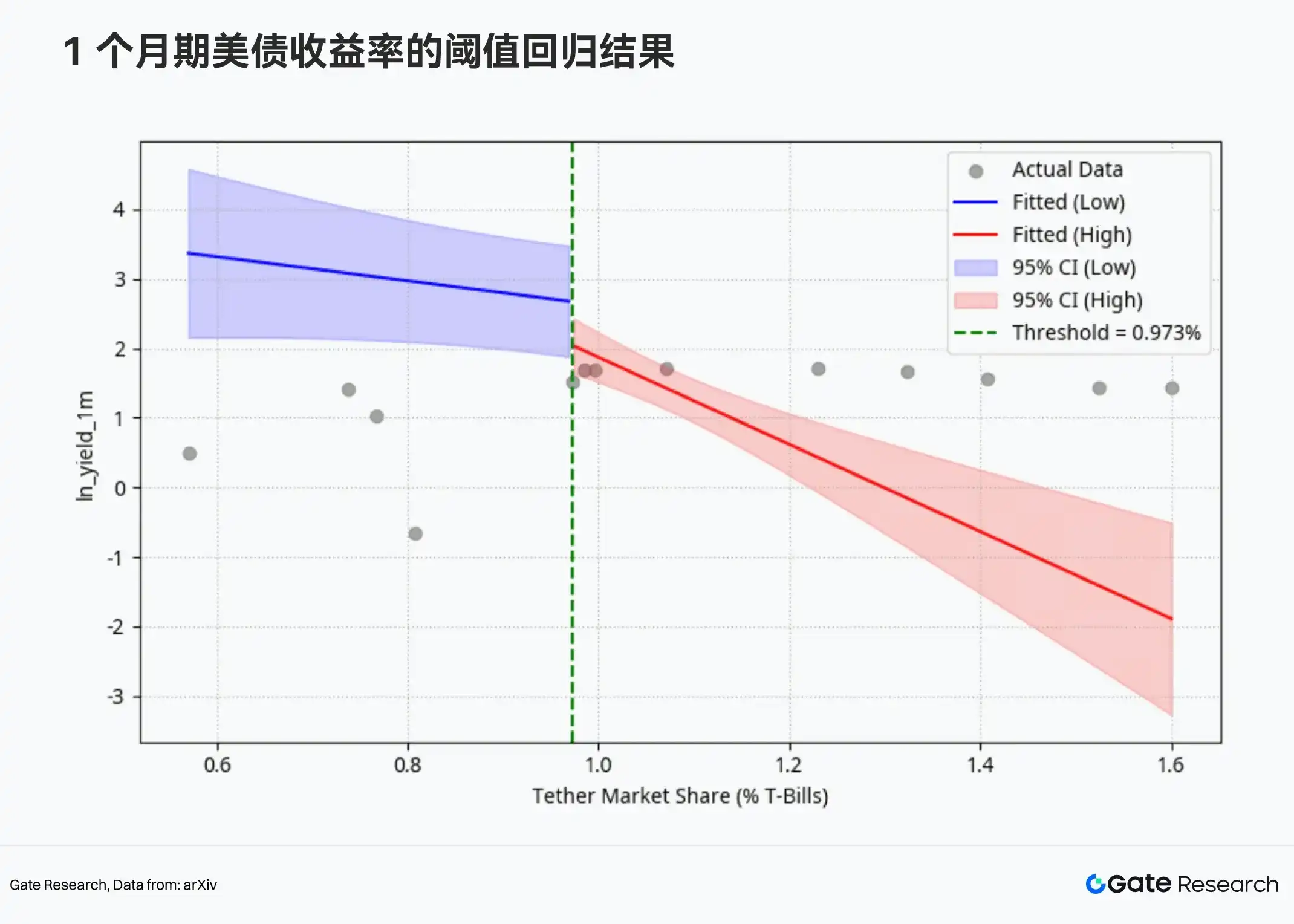

This phenomenon has been systematically verified by recent academic research. Recent studies on arXiv show that stablecoin issuers, represented by USDT, have跻身 among the world's largest non-sovereign holders of short-term US Treasuries. More importantly, the research found that changes in stablecoins' share of the Treasury market have a significant impact on short-end interest rates: for every 1 percentage point increase in stablecoins' share of the Treasury market, the 1-month Treasury yield is significantly suppressed by approximately 14–16 basis points. By early 2025, the cumulative effect of this structural influence had reached over 20bp.

The figure above shows the results based on a threshold regression model, used to characterize the nonlinear impact of changes in USDT's share of the short-term Treasury market on the 1-month Treasury yield. The horizontal axis represents USDT's share of the Treasury market, and the vertical axis represents the logarithm of the 1-month Treasury yield. The model identifies an optimal threshold of approximately 0.97% (green dashed line) through grid search and divides the sample into low-share and high-share intervals. The results show that when USDT's market share is below the threshold, its expansion has a relatively limited impact on short-term interest rates; however, when the share exceeds the threshold, a further increase in USDT holdings is significantly negatively correlated with the 1-month Treasury yield, with the magnitude of the interest rate decline明显加大, indicating that stablecoins' influence on short-term funding prices has significant scale effects and nonlinear characteristics. The blue and red solid lines represent the fitted results on either side of the threshold, respectively, with the shaded areas representing the corresponding 95% confidence intervals, and the gray scatter points representing the actual observations. These results indicate that after reaching a certain scale, stablecoins have begun to become an important structural force influencing short-term US dollar interest rates.

3.2 Fed Top-Down vs. Stablecoin Bottom-Up Interest Rate Influence Mechanisms

The aforementioned research indicates that stablecoins are no longer just "using dollars" but are changing the supply and demand structure of short-term dollar funds. When stablecoin scale expands, they continuously absorb short-term Treasury supply, forming a marginal demand that is weakly correlated with the macro cycle but highly stable, thereby exerting downward pressure on short-end yields.

This logic stands in stark contrast to the traditional Fed monetary policy path. Generally, the central bank influences interest rates in a top-down manner: policy rate adjustment → financial market repricing → transmission to the real economy. The influence path of stablecoins, however, is bottom-up: on-chain dollar demand expansion → change in stablecoin reserve配置 → rebalancing of money market supply and demand → change in short-term interest rates.

Precisely because of this, stablecoins are difficult to simply understand as a policy tool. They are not a variable the central bank can directly adjust but a structural force originating outside the banking system: not driven by interest rate directives, yet genuinely participating in the flow and pricing of short-term dollar funds. It is also on this point that stablecoins begin to become a key interface connecting on-chain dollars with the traditional dollar system.

3.3 Mechanism Closed Loop: Rate Cuts → Stablecoins → Short-Term Rates → Dollar Redistribution

Viewed within a larger macro framework, stablecoins are participating in a complete dollar redistribution mechanism. The logical starting point is the coexistence of rate cuts and fiscal constraints. When the central bank enters a rate-cutting cycle, nominal financing costs decline, but at this time, fiscal deficits and debt规模 continue to expand, while regulatory constraints on bank balance sheets反而 tighten. Therefore, in such an environment, the banking system will not expand dollar supply indefinitely but is more inclined to收缩 risk exposure and compress dollar service capacity for cross-border and marginal clients.

The result is that dollars do not disappear, but the supply channels change. Part of the dollar demand that originally relied on the banking system—including cross-border payments, crypto trading, market maker margin, on-chain settlement—is squeezed out of the system, forming a spillover of marginal dollar demand.

Stablecoins, because they can bypass bank accounts,地域, and business hour restrictions, quickly absorb this extra-systemic dollar demand. When stablecoin scale expands, the corresponding reserve funds do not remain idle in accounts but systematically flow into short-term Treasury and repo markets.

This behavior has a direct impact at the money market level: stablecoin issuers continuously and stably buying short-end Treasuries equates to providing a new, structural bid for short-term dollar funds, thereby exerting a yield-suppressing effect. The decline in short-term rates further reinforces the low-risk asset allocation logic for stablecoins.

Ultimately, a closed loop is formed: Rate cuts and fiscal pressure → Banking system contracts dollar supply → Stablecoins absorb spillover demand → Reserves buy short-end Treasuries → Suppress short-term yields → The role of stablecoins as a dollar reservoir is continuously strengthened.

4. 2026 Outlook: Stablecoins Amid Rate Cuts, Dollar Depreciation, and De-Dollarization Narratives

From a longer-cycle perspective, what the dollar is experiencing is not a simple exchange rate fluctuation but a structural change gradually emerging against the backdrop of rising rate cut expectations, heightened geopolitical uncertainty, and other factors. Persistently high long-term debt levels, a偏低 real interest rate level, and a monetary policy tilt towards easing are causing the market to re-evaluate the "unconditional safety" that the dollar, as a traditional store of value, relies upon.

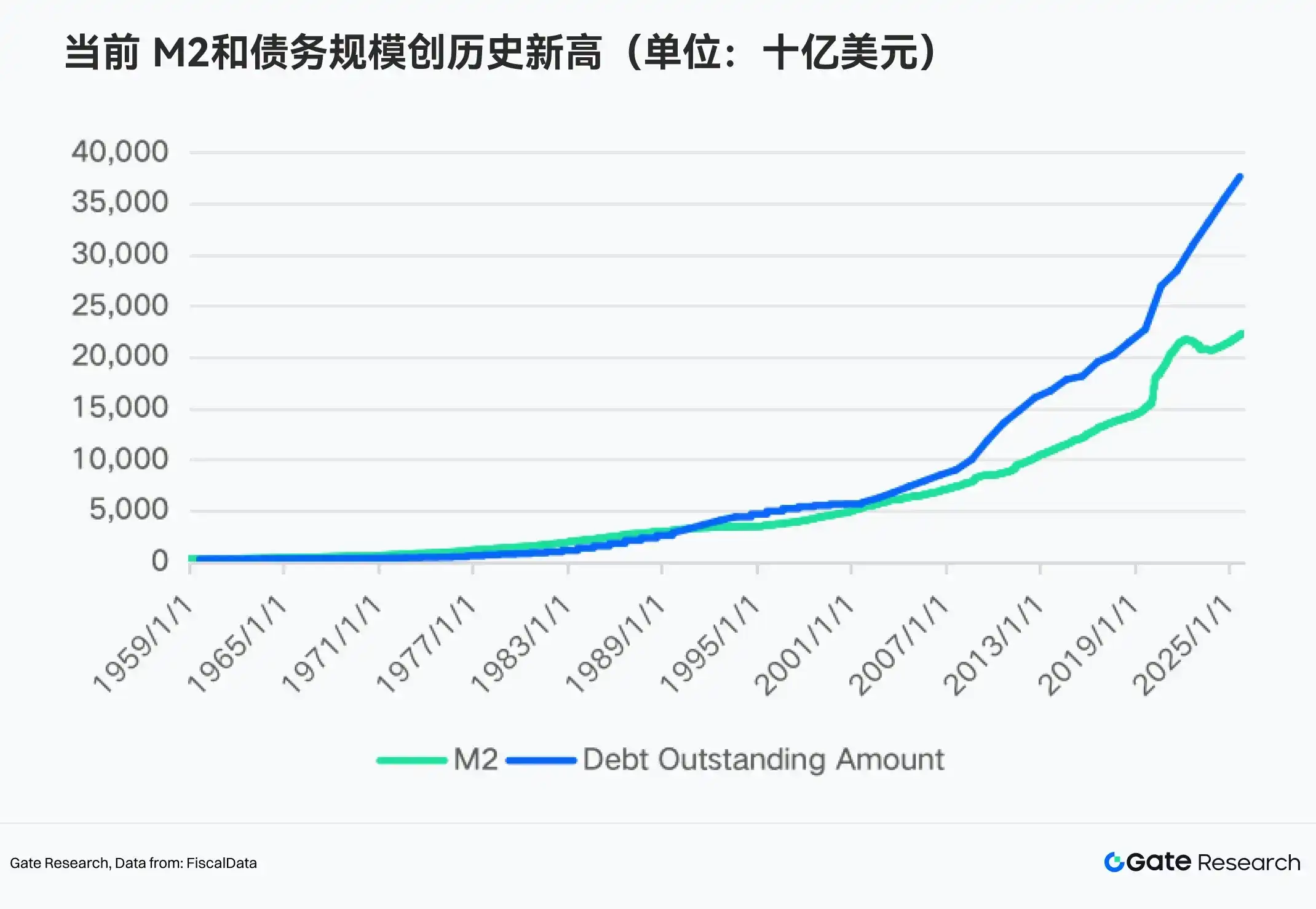

In 2025, total US debt突破 $38 trillion, and the M2 money supply expanded to approximately $22.4 trillion, both hitting historical highs, indicating that while fiscal elasticity is constantly being depleted, the dollar system is expanding liquidity to hedge against financing pressures. These collectively point to a fact—dollar credit is shifting from "taken for granted" to needing verification. It is precisely against this backdrop that stablecoins are meeting the marginal dollar demand that the traditional system难以覆盖. They are not creating new dollar credit but are reshaping the accessibility of dollars.

In terms of scale, stablecoins are still微不足道; but in terms of direction, change has already occurred. Stablecoins account for only about 1.3% of M2, which恰恰 means they have not entered the stage of replacing the dollar but are still in the stage of absorbing spillover demand. Furthermore, relative to the庞大的 global money supply and total dollar demand, the penetration rate of stablecoins is extremely low,蕴含 enormous marginal growth potential. The current USDC market accounts for only about 0.35% of total M2 (calculated based on USDC's $72.4 billion market cap), indicating that stablecoins are still in a very early stage of expansion. If stablecoins further penetrate into payments, cross-border settlement, and store-of-value demand in the future, marginal dollar demand may continue to migrate to this on-chain channel.

Looking ahead to 2026, the role stablecoins are more likely to play is not that of an eroder of dollar credit, nor a leader of de-dollarization, but rather part of its extended structure: in an environment where traditional financial system constraints intensify, stablecoins provide a new "reservoir" and distribution layer for the dollar, allowing part of the dollar demand originally constrained by the banking system to continue to exist and be effectively met. As the stablecoin scale continues to expand, the stable bid for short-term Treasuries formed by their reserve assets has already begun to marginally压低 short-term dollar funding prices, in turn affecting the dollar's own pricing structure.

Therefore, the strength of the dollar remains the core of macro discussions in the medium to long term; but how the dollar is used, through which channels it is held and circulated, is becoming a more important structural question. And stablecoins are at the center of this transformation, both extending the usage radius of the dollar and quietly reshaping the operating方式 of the dollar short-end funding market.

References:

• BIS, https://www.bis.org/publ/work1270.htm

• Federal Reserve Bank of New York, https://libertystreeteconomics.newyorkfed.org/2025/04/stablecoins-and-crypto-shocks-an-update

• arXiv, https://arxiv.org/abs/2505.12413

• FiscalData, https://fiscaldata.treasury.gov/datasets/historical-debt-outstanding/historical-debt-outstanding

• Federal Reserve, https://www.federalreserve.gov/econres/notes/feds-notes/in-the-shadow-of-bank-run-lessons-from-the-silicon-valley-bank-failure-and-its-impact-on-stablecoins-20251217.html

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform, providing readers with in-depth content including technical analysis, hot topic insights, market reviews, industry research, trend predictions, and macroeconomic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks. It is recommended that users conduct independent research and fully understand the nature of the assets and products they purchase before making any investment decisions. Gate is not responsible for any losses or damages caused by such investment decisions.