Abstract

The possible Ethereum merger date has been set for September 19, 2022. The Ethereum merge is entering the countdown phase. The impact of the merge has also been the topic heated discussion recently, one of which is the hard fork. Here, we analyze the possibility of the Ethereum hard fork from three aspects: First, the realization of the hard fork; Secondly, the value exploration of the forked chain; Lastly, the interests of all parties. We then draw the following conclusions:

(1) Judging from the current attitudes of all parties, there lies the possibility of success although fork chain supporters may be few. The ETH Proof of Work (PoW) fork chain needs to meet the following conditions in order to achieve success: 1. In the short term, get the support of the necessary parties, including a certain proportion of miners, third-tier or above of central exchanges and early ecological developers; 2. In the medium-term, there needs to be a stable market for forked chain tokens, in addition to funds and users retained on the forked chain’s ecosystem; 3. In the long run, if the forked chain can achieve the development of Layer 2, which will solve the problem of Ethereum On-chain congestion, it would be possible to achieve the status of a competitive public chain.

(2) The risk brought by this hard fork is higher than that of ETC. Since smart contracts have been deployed on Ethereum, many forked coins will become worthless. The ETH forked token carries certain functions on the smart contracts, making its price more difficult to predict. Moreover, other infrastructures, such cross-chain bridges and oracles, barely support forked chains at the start. The ecosystem on the forked chain may be difficult to operate normally in the short term.

(3) All parties seem to benefit from the hard fork. The hard fork of Ethereum is not difficult, and can attract high-quality users from Ethereum. The hard fork is very beneficial for central exchanges, and is capable of obtaining traffic, new users and funds. The protocols can be run on the forked chain at a very low cost. It is also a great opportunity for developers. Also, Ethereum users will receive free airdrops. But no one is the winner forever, and new users who enter the market with real money still need to pay attention to risks.

Overview

The Merge project, backed by the Ethereum Foundation, has always laid claim to a strong community consensus, and hard fork supporters have been seen as an unpopular minority. Vitalik also re-emphasized his opposition to hard forks during the Korea Blockchain Week event, saying that people who push Ethereum hard forks to keep PoW are "outsiders" who "just want to make a quick buck". Even so, as the merge approaches, the more heated the discussions about the hard fork have grown. On July 29, 2022, Bao Erye, one of the largest participants in the Chinese mining ecosystem, said that he might conduct the hard fork and the test chain for it has been developed. Following that, many institutions also expressed their support for the forks.

In such a case, the Ethereum hard fork poses interesting questions. First, Ethereum today lays claims to many smart contracts and assets, and its forked chain will face many complex situations. Which direction will the forks take in the future? Second, since there is some consensus to support the forks, there will inevitably be new markets and opportunities that will arise. Which parties, then, will benefit, and which will lose?

1 Hard Fork Controversy and Implementation

Since its inception in 2015, Ethereum has experienced many hard forks:

ETC

ETC is the result of the first hard fork in Ethereum history as a result of an incident that happened in 2016. The contract bugs of The DAO led to funds being stolen by hackers. Groups that disagreed with the hard fork continued to support the old blockchain, i.e., admitting to the loss of funds. ETC is the most controversial fork, with the market cap currently ranking 19th in CoinMarketCap.

ETZ

ETZ was launched by a group of technology enthusiasts in 2018 to create a better decentralized application platform. But it has few supporters —the Dapps have not been developed, and its token price is almost zero.

Hard forks to reset Ethereum difficulty bomb

The difficulty bomb aims to encourage Ethereum’s smooth transition from a PoW chain to a Proof of Stake (PoS) chain. Artificially increasing block difficulty, so miners cannot continue to produce blocks and obtain rewards, would serve to discourage the coexistence of the new chain and old chain. However, due to the technical progress of ETH2.0, the difficulty bomb has been repeatedly delayed and reset six times, resulting in six hard forks. These hard forks brought no controversy or any new forks.

ETC, backed by big miners, is a successful example of an Ethereum hard fork. Unlike current times, people in the industry at that point in time had very distinct understandings of what decentralization meant. The technical implementation for the hard fork was relatively easier, and there was no need to consider the smart contracts or their tokens. For ETH 2.0, a hard fork would need to retain the function for executing smart contracts on Ethereum, completing historical data and current user status. That is to say, the new PoW chain has to record all accounts, their respective balances, and all smart contracts which were deployed and run in the EVM. At this point, the same applies to the forks. Both the original chain and the forked chain before the fork time point have the same blocks. But after the fork, miners who support the PoW forked chain will continue to generate blocks and ledgers while following the new rules. It is possible that this rule removes the difficulty bomb or EIP-1559, making block rewards higher and resulting in more profitability for miners. The setting of the new rules means that the PoW fork chain needs to develop new node clients, browsers and wallets. The fork also needs to be supported by exchanges and custodians.

1.1 Conditions for a successful hard fork

It would not be easy for a hard fork to perform as well as ETC today. At present, competition among public chains remains strong. High performance and PoS consensus have become the general trend. Meanwhile, the fork has not received high levels of funding like Aptos, nor does it have a team of technical experts. Conditions are challenging for a hard fork to be conducted. Interestingly, the growing number of supporters for the hard fork may result in a higher likelihood for success. Moreover, since the specific time for the Ethereum merger to take place remains uncertain, this lends more time to the team desiring to create a forked chain project in terms of development, operation and risk control, which would improve the probability of success.

In the short term, gaining the support of more industry players is the primary condition required for the birth of a fork, and this would include miners, exchanges, and early developers. Currently, there is no suitable chain for Ethereum miners to transition to except the ETC chain. They will take the lead in supporting the hard fork to reduce their losses. The new market has also provided some traders and speculators with opportunities, which is a positive signal for exchanges. At the same time, in order to obtain forked tokens, some people will buy ETH, which will increase the demand for ETH in the short run.

In the long run, the fundamental reason for the Ethereum upgrade is that current performance is insufficient for supporting on-chain activities. PoW forked chains will inevitably face the same situation. And with the continuous increase of state data, the requirements for miners will get higher. Whether miners would be willing to cultivate a fork for a long time is an issue that needs to be considered.

The competitor of the ETH PoW fork is not ETH 2.0. We can see that the old PoW public chains have not done well performance and ecosystem-wise. Therefore, we think that the competitors of the ETH PoW fork will be the old PoW chains and the PoS chains with immature ecosystems and insufficient users. Other factors aside, the PoW+Rollup mechanism has been able to alleviate the congestion on Ethereum. It is attractive enough for the fork to be regarded as a new public chain. On the other hand, ETH 2.0, which turned to PoS consensus, will likely not witness much improvement in performance (block time will be increased to 12s, while gas fee will be reduced by 12%), and it can only rely on Rollup and subsequent sharding technology. If the PoW fork can cooperate with the Layer 2 teams, a competitive public chain will result. Of course, the team that leads the fork will be required to provide long-term technical support for it to achieve long-term success.

1.2 Risk assessment

The forked chain and Ethereum use the same mining machine, and the computing power can be easily rented on some platforms. Should only a small number of Ethereum miners support the forked chain, the computing power and block time will be unstable at the beginning. Therefore, the remaining miners can easily start a 51% majority attack on the forked chain. Such an occurrence has also happened many times on ETC. Because of vulnerability, small forked chains simply cannot succeed.

In addition to the 51% attack, there is also the possibility of a replay attack. This usually occurs within a short period after a hard fork. Attackers steal account funds by monitoring the transactions. In order to prevent replay attacks, the forked chain needs to make changes in the transaction structure, and the implementation method is relatively simple. This is used to distinguish the original chain from the forked chain by upgrading the node client or identifying the transaction, using technologies such as chainID.

Another risk lies with smart contracts. At present, most of the smart contracts’ authority lies with the project teams. These teams can change the contracts at any time to affect the fork tokens. These forked tokens may be worthless, but are inextricably related to ETH forked token in smart contracts. Once the ETH forked token gains value, there will be arbitrage space. Some can also use this method to carry out risk-free arbitrage through flash loans.

2 ETH PoW fork prediction

2.1 The value of forked token

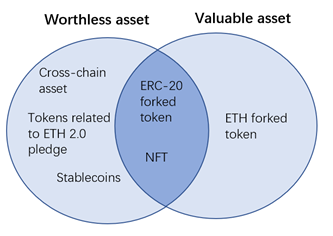

The PoW fork replicates the Ethereum ledger before the merge. Apart from the ETH forked token, a large number of forked assets are also generated, including stablecoins, cross-chain assets, smart contract tokens, NFTs, etc. In this section, we analyze the potential changes that may exist for these assets.

Stablecoins

Stablecoins are directly related to the DeFi ecosystem and affect most protocols. According to Etherscan, the issuance of USDT on Ethereum exceeds 32 billion, while the issuance of USDC exceeds 45 billion. If the stablecoins on the forked chain are to have value, two conditions must be met: 1. The issuer recognizes these assets; 2. The issuer has a 1:1 USD asset reserve. These two conditions are not being met right now, and are impossible to achieve. Any stablecoins on the new network would start out worthless. If Tether or Circle support the fork, the only viable way would be to issue new stablecoins. However, because Tether and Circle are the centralized issuers, aspects such as shareholders, users and regulatory aspects need to be considered, which is very complex process.

Cross-chain assets

The largest cross-chain asset on Ethereum is WBTC, with a market cap of over US$5 billion. Similar to stablecoins, the issuer of WBTC is a centralized custodian. Behind all cross-chain assets is a 1:1 mapping of the original chain assets, and this mapping has been completed on ETH 2.0. Therefore, the value of all cross-chain assets on the forked chain will also return to zero.

The tokens of smart contacts

Most of the permissions of Dapps and smart contracts are in the hands of the project teams. At present, no project team has expressed support for the fork, especially well-known projects such as Uniswap and Curve. Although the technical support aspect is simple, the potential risks and reputation losses are difficult to predict. Some small teams may support the fork driven due to interest. These projects, like dex or lending protocols, may become the first to receive support from the forked chains.

NFT

The value of NFT assets is reflected in community recognition and IP attributes. For the benefit of the community, it would be unlikely for the community to recognize the value of NFT on the forked chain. Even with high gas fees, the issuance of NFTs on Ethereum has not decreased, and well-known artists and creators recognize Ethereum over other public chains. This is also called "orthodoxy". If the fork is to develop NFT projects, it can choose "net celebrity" or "sports" type NFT projects. Such projects have the willingness to expand and experiment on the new chain; and they are not as focused on uniqueness as BAYC.

ETH PoW forked token

The first condition for the success of the forked chain is that its public chain token has value. Unlike previous hard forks, users have strong expectations for the merge due to the profound influence of the Ethereum Foundation. Once a fork occurs, users who receive airdrops will become the biggest sellers, the price of the ETH forked token may plummet, and it may become a meme token. There is also a special ETH forked token, which is pledged on ETH 2.0. Due to the particularity of the pledge, it is impossible to return these tokens to the user's address. This leads to unfairness, and these users will not receive staking benefits, and there is no need for protocols like Lido to exist on a fork. The total amount of ETH forked token will be reduced by more than 10%. In our previous report "Will there be a Surge after the Merge", we quantitatively studied the impact of ETH supply and demand from a market perspective, and also predicted the price of ETH PoW forked token. Assuming that the unit computing power income of the ETH forked token in the future is equivalent to that of ETC, if the forked chain can undertake 20% of the computing power of Ethereum, the price of the ETH forked token is expected to reach US$138 or higher.

Fig.1 Analysis of asset value on ETH PoW fork (From: Huobi Research)

2.2 Ecosystem on-chain

After the hard fork, the smart contracts on chain will still run unless the project team makes changes to the code. But this operation will no longer have any value. For example, the loan agreement is no longer liquidated. DeFi projects without oracles’ support simply cannot function properly, and all token prices fall into a state of confusion. The only thing that may work properly is the protocols of the AMM mechanism, but in the short term, all tokens may be exchanged by arbitrageurs into valuable ETH forked token. And these ETH forked tokens will likely perform poorly on centralized exchanges. For ordinary users, the realization of this path is very difficult. First, the swap protocol is still running, but without the UI interface, it needs to be operated entirely by code. Second, there are not many miners on the forked chain. Once the chain is congested, users will need to bear high gas fees. Third, even if many arbitrageurs use automatic execution robots, the transaction will be submitted to the miners, and whether the transaction is executed or not is still controlled by the miners.

In terms of oracles, although Chainlink has said that it will not support the hard fork, if the forked chain proves successful, there is little technical difficulty in providing the oracle service, and other oracles may support the forked chain. However, even an oracle supports the fork, the price of tokens will be in disarray without enough liquidity. This will result in a negative effect on the oracle.

In terms of cross-chain bridges, all cross-chain bridges that rely on wrapped assets cannot function properly on the forked chains. But without cross-chain infrastructure support, it is difficult for the forked chain to survive in a multi-chain network ecosystem. In order to avoid risks, the cross-chain bridge project needs to be redeployed on the forked chain, and the cross-chain assets also need to be redefined.

On the Layer 2 side, all forked assets related to it will be worthless, and the ETH that crosses Layer 2 will qualify for the ETH forked token airdrop. At present, the TVL on Layer 2 is relatively small, so this would have little impact.

3 The interests and opportunities of all parties

A hard fork would have the greatest impact on the miner group. The Ethereum PoS chain completely eliminates the possibility of miners. Miners, who had previously expressed dissatisfaction with the EIP-1559 scheme, made up for their losses as the price of ETH increased. In order to maximize value, miners will definitely support a PoW fork. However, if the price of the forked token is very low, it may be difficult to attract miners, especially the token economic model suffers from inflation after the changing of rules, which may further lower the price.

For the protocols on Ethereum, the advantage of recognizing their forked assets is that they can take the lead in accumulating a group of users on the new chain. However, most of these users may become sellers. To avoid this, the project team may need to redesign the product and increase the token pledge function to prevent selling. There seems to be no need for well-known projects to risk their reputations by taking part in a forked chain. However, it is an excellent opportunity for small teams. The project deployment cost and difficulty are low, and there are mature user groups on the forked chain who are familiar with the rules of the game. During the vacuum period when the forked chain goes online, DeFi projects starting liquidity mining may attract user participation.

For the exchanges, a forked chain poses great benefit. If the forked chain itself has viable resources and operations, it can attract a large number of users and funds. Most users' assets are stored in exchanges, so forked tokens can only be provided through exchanges. If the exchange provides more convenient channels and interesting derivatives, it will further attract traders and speculators. This is the case with BCH. So long as there are second- and third-tier exchanges that support the forked tokens, top exchanges will be prompted to do likewise.

For ordinary users on Ethereum, forking would typically mean receiving an airdrop. And from historical experience, the forked tokens must have a price. Although users may feel that the value of the forked token is not sufficiently high, airdrops and hot trends could attract new entrants to the market and further push up the price. General users will support the fork, but these are likely the biggest sellers. If the new users who enter the market cannot follow the dynamics of the forked chain in time, the forked tokens in their hands will likely dip quickly in value. If the user's ERC-20 tokens are on chain, they can receive airdrops directly. However, if the forked chain develops a new hot wallet, it runs the risk of being attacked. For the likes of MetaMask, it would be best to generate a new wallet to transfer the forked tokens to in order to isolate risks. Another safer way would be to transfer the ERC-20 tokens to an exchange that supports the fork.

Read more:

Huobi Research's research report on the Ethereum merger and impact can be found at:

1. All You Need to Know about the Merge of Ethereum

2. Will there be a Surge after the Merge - A Quantitative Analysis of Post-Merge Impact on the Market

About Huobi Research Institute

Huobi Blockchain Application Research Institute (referred to as "Huobi Research Institute") was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain. As the research object, the research goal is to accelerate the research and development of blockchain technology, promote the application of blockchain industry, and promote the ecological optimization of the blockchain industry. The main research content includes industry trends, technology paths, application innovations in the blockchain field, Model exploration, etc. Based on the principles of public welfare, rigor and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms to build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical basis and trend judgments to promote the healthy and sustainable development of the entire blockchain industry.

Official website:

https://research.huobi.com/

Consulting email:

research@huobi.com

Twitter: @Huobi_Research

https://twitter.com/Huobi_Research

Medium: Huobi Research

https://medium.com/huobi-research

Disclaimer

1. The author of this report and his organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report.

2. The information and data cited in this report are from compliance channels. The sources of the information and data are considered reliable by the author, and necessary verifications have been made for their authenticity, accuracy and completeness, but the author makes no guarantee for their authenticity, accuracy or completeness.

3. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment and other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report, unless clearly stipulated by laws and regulations. Readers should not only make business and investment decisions based on this report, nor should they lose their ability to make independent judgments based on this report.

4. The information, opinions and inferences contained in this report only reflect the judgments of the researchers on the date of finalizing this report. In the future, based on industry changes and data and information updates, there is the possibility of updates of opinions and judgments.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the source. If you need a large amount of reference, please inform in advance (see "About Huobi Blockchain Research Institute" for contact information) and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original inten