Author: Prathik Desai

Original Title: The Maturity Fingerprint

Compiled and Edited by: BitpushNews

Everyone believes stablecoins are growing. In just two years, their circulating supply has more than doubled, while adjusted transaction volume has more than tripled. Last month, the monthly adjusted transaction volume of stablecoins hit a record high. Some people scoff at these numbers, while Crypto Twitter (CT) celebrates.

But numbers alone are insufficient to explain the nature of this growth. Equally important is the context in which growth occurs—such as who is using stablecoins, for what purposes, and whether usage patterns are changing. Allium gave us a preview of their latest report on stablecoin infrastructure—'Stablecoins: The Rise of a New Payment Rail.' This is a very important report because the charts show that the use of stablecoins is shifting from enabling low-cost cross-border remittances to supporting general commerce and supplier payments between businesses.

Most current debates about stablecoins focus on whether they are financial products (like banks, Treasury wrappers, yield vehicles) or merely payment infrastructure. Policy-level debates about stablecoin interest assume that stablecoins primarily function as financial instruments. But the data in the report tells a different story: the recent composition of stablecoin activity increasingly resembles a payment rail rather than a savings product.

This mirrors the evolution pattern we saw with the Automated Clearing House (ACH) network: from initially replacing paper checks in payroll to becoming the backbone of general commerce, B2B payments, and consumer bill payments.

This article will combine data from Allium's stablecoin infrastructure report to explain why it changes our perspective on the direction of stablecoins.

The Differentiation of Velocity

Since January 2024, the circulating supply of stablecoins (total supply minus non-circulating supply) has grown by over 100%. During the same period, adjusted transaction volume (excluding wash trading, internal entity transfers, and round-tripping) increased by 317%.

In the accumulation phase of any new asset, supply growth typically outpaces usage growth. As the asset matures, usage growth outpaces supply growth. This is because asset holders are spending the asset more frequently. Here, since adjusted transaction volume is growing much faster than the circulating supply of stablecoins, it indicates that stablecoins are maturing from a store of value asset to a more popular medium of exchange or value transfer tool.

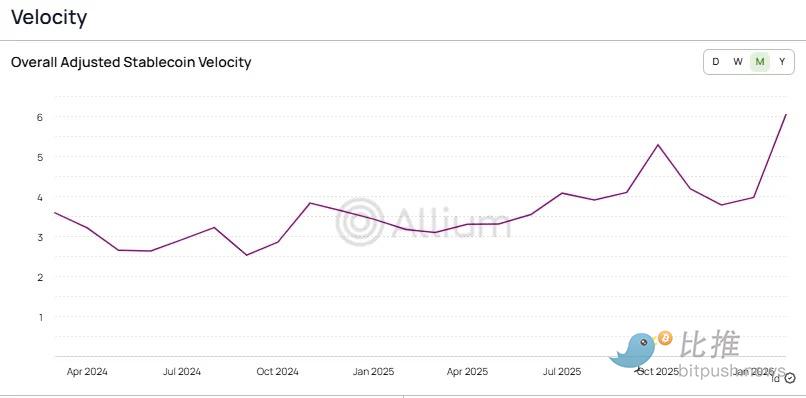

This shift is reflected in the velocity of stablecoins, calculated as adjusted transaction volume divided by circulating supply.

Allium

The velocity of stablecoins has increased from 2.6x to over 6x in the past two years, reflecting that each dollar of stablecoin supply is now turning over 2.3 times more actively than in January. Benchmarking this against traditional payment rails shows how mature stablecoin usage has become.

Another metric that establishes the maturity of stablecoin usage is the number of transactions. It is least affected by large-value noise. Therefore, when the growth in the number of payment transactions outpaces the growth in transaction value, it indicates that the average payment amount is decreasing. This behavior is typical of a payment rail gaining traction, rather than an experimental tool shuttling between exchanges.

This raises the question: who is making these payments, and what are they paying for?

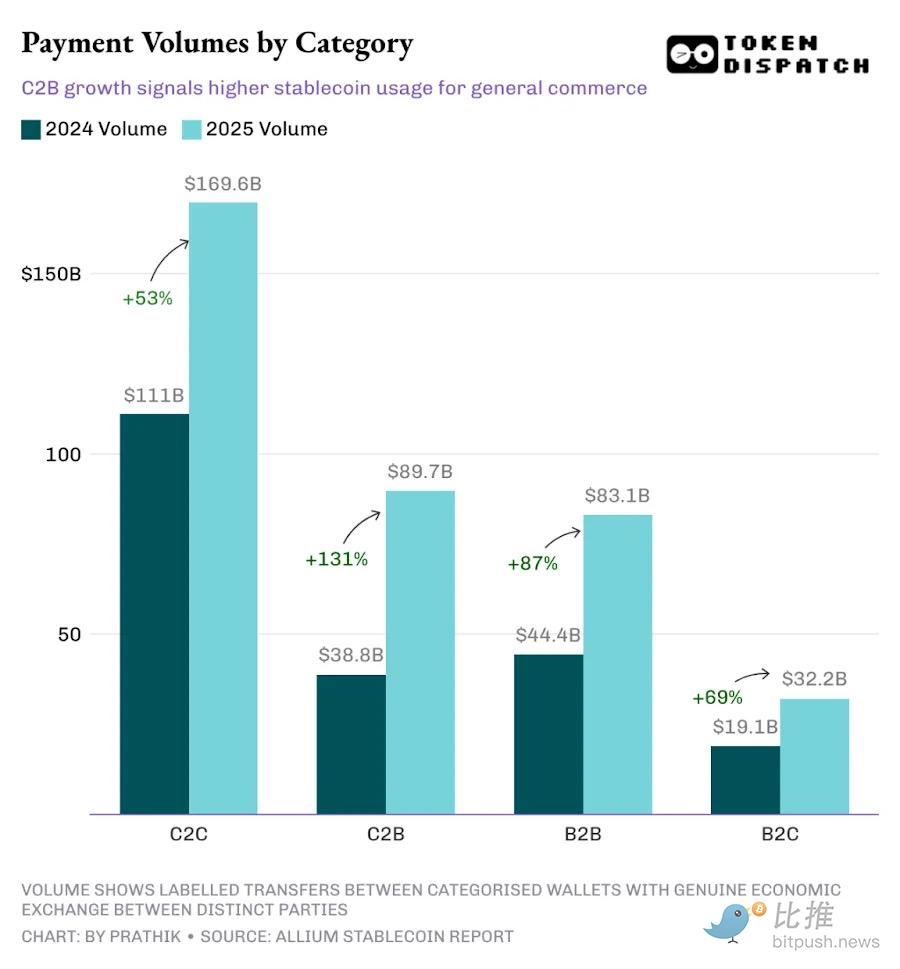

In 2025, the consumer-to-consumer (C2C) category remained the largest channel, ahead of consumer-to-business (C2B), business-to-business (B2B), and business-to-consumer (B2C). But its growth rate was the slowest among the four categories.

The slowdown in C2C growth further confirms the maturation of stablecoin usage, as person-to-person transfers are the simplest use case. They require no merchant integration, no invoicing tools, no APIs, and have minimal adoption barriers. This is the typical starting point for every new payment technology.

When India launched the Unified Payments Interface (UPI) a decade ago, retail users joined first, driven by cashback and other customer acquisition strategies. I remember using Google Pay (initially launched as Tez in India) to transfer money between my own accounts just because it gave me a one-dollar cashback. Only when commercial tools, reporting, and dedicated payment confirmation audio device systems (speakers) were introduced did stores and institutions join.

As infrastructure matures, commercial use cases begin to absorb market share. And this transformation seems to be happening.

The high growth in C2B indicates that more users are using stablecoins for general commerce, subscriptions, and merchant payments. Meanwhile, the growth in B2B indicates that commercial counterparts are beginning to adopt stablecoins in invoice processing, supply chain payments, and financial operations. Both growth rates (131% for C2B and 87% for B2B) exceed the overall payment growth rate of 76%, indicating that the share of commercial payment volume is expanding.

When you combine the growing C2B transaction volume with the decreasing average transaction value in C2B (from $456 to $256), it suggests a trend of people starting to use stablecoins for recurring purchases.

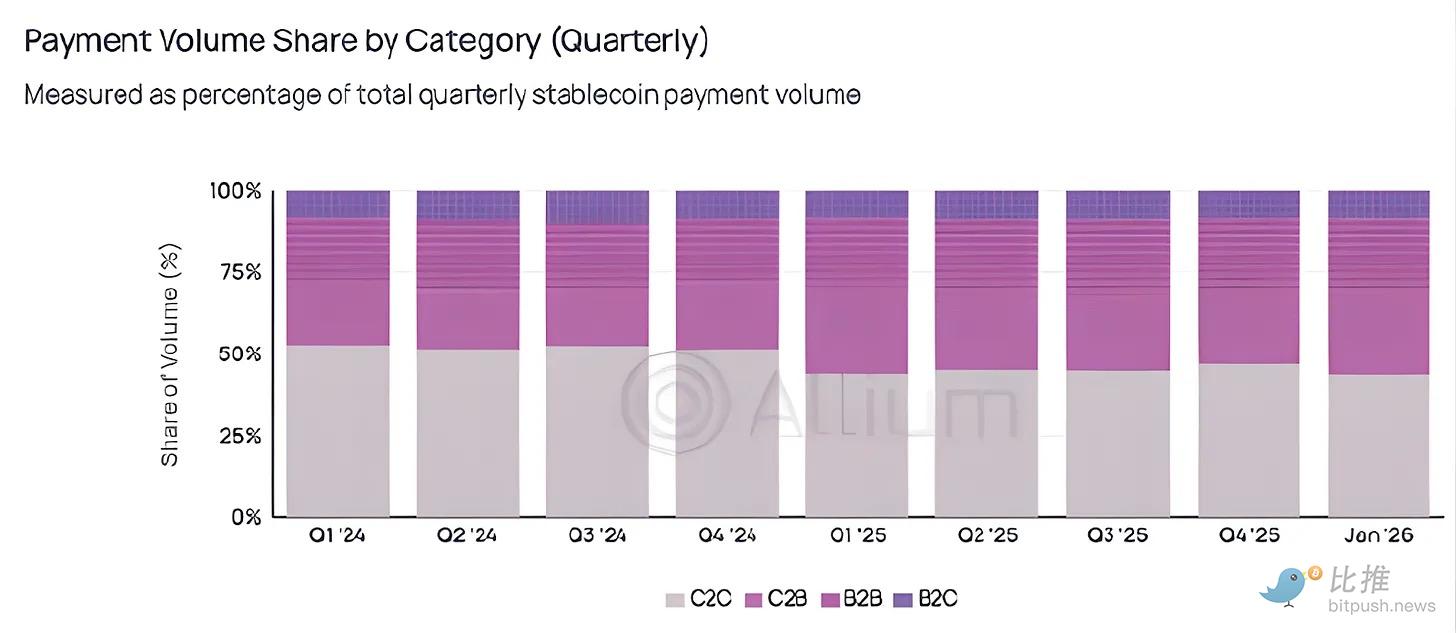

Although peer-to-peer (P2P) categories still dominate in absolute terms, they will soon cede ground. Quarterly share data makes this rotation even more undeniable.

Allium

After falling below the 50% mark in Q1 2025, C2C's share of total payment volume has never exceeded 50% again.

The world seems to be moving beyond the experimental phase of using stablecoins for low-risk, low-frequency peer-to-peer transfers, toward consistently using them for high-frequency payments.

When I first started tracking stablecoin adoption, a mainstream narrative supporting stablecoins was how they could enable cross-border remittances and potentially disrupt Western Union by allowing workers in developed economies to send money home. But the data tells a different story.

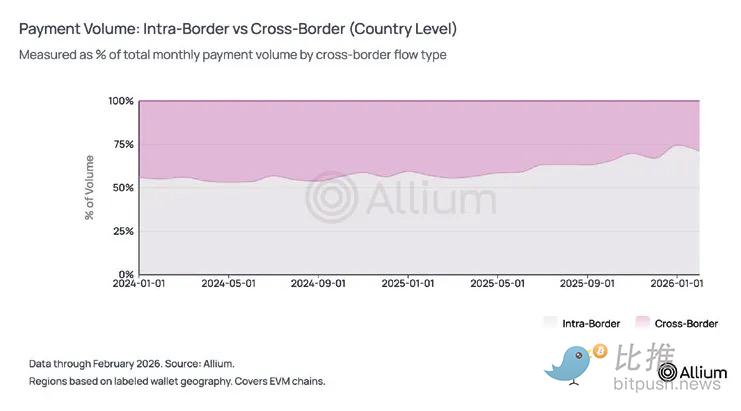

Currently, about three-quarters of stablecoin payments occur domestically. Over the past year, the share of cross-border payments at the country level has decreased from 44% to about 25-29%. At the regional level, 84% of payments remain within the same geographic region.

Allium

Based on all our previous charts, it is clear that stablecoins are not competing with SWIFT in the international settlement space. Instead, B2B metrics—including 74% domestic dominance, declining average transaction size, payroll, and growing invoice use cases—point to stablecoins competing with domestic payment rails like ACH.

For reference, ACH B2B payments grew about 10% in 2025, while stablecoin B2B payments grew 87% during the same period. I realize the absolute scales are not comparable, and we must consider the low base effect of stablecoins. However, this growth cannot be ignored.

Outlook

For a long time, I viewed cross-border remittances and peer-to-peer transfers as the main drivers of stablecoin adoption.

Imagine a son in India receiving dollars from his family in Dubai on a bank holiday without intermediaries taking 7% to 8% in fees—this narrative is indeed appealing. This story still holds today, but perhaps it is no longer the main storyline.

Interestingly, the narrative of domestic consumption scenarios has quietly and rapidly surpassed everything else. C2C's market share hasn't returned to 50% for over a year, a metric that never seemed to trend in crypto discussions. But it is this metric that marks stablecoins' transformation from a 'crypto product' to 'financial infrastructure'—enabling transactions between consumers and businesses, or between businesses themselves.

It's also worth noting that the payment transaction volume labeled by Allium is based on their analysis of wallets they can cover, identify, and tag. Although this data shows that payment transactions account for only 2% to 3% of the total adjusted stablecoin transaction volume, this should be considered a lower bound—as there are undoubtedly many wallets that Allium has not covered.

Moving forward, I will focus on two directions: whether the shares of C2B and B2B continue to rise, and whether the average transaction value can remain low in the coming quarters. If these trends persist even during a crypto market downturn, it will indicate that stablecoin payment infrastructure has truly begun to decouple from the speculative cycles of the crypto market.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush