Author: Citrini Research

Compiled by: Felix, PANews

The opportunity for retail investors to achieve high returns in the stock market is becoming increasingly slim, likely due to companies delaying their listings. Research firm Citrini published an article discussing the trend in modern capital markets where companies tend to remain private for extended periods, leading to growth value being primarily captured by venture capital (VC) firms. Public market may have been reduced to a liquidity exit tool. Details below.

Companies staying private for a long time is simply nonsense.

While one can understand the motivations and doesn't blame founders for doing so, this practice damages the system that initially built these companies. Fundamentally, it is a betrayal of the promise that keeps capitalism running.

The social contract in the United States has worked remarkably well for capital markets.

Sure, you might work for a boring small business or have a mediocre job; you might not become extremely wealthy or have transformative ideas, and sometimes you might feel the system isn't working for you at all.

But at least you had the chance to participate in the great achievements created by this system.

For much of the post-war period, the deal roughly went like this: the public bore the market's volatility, inefficiencies, and the dullness of holding broad indices. In return, they were occasionally given access to transformative growth opportunities.

It created upward mobility opportunities that didn't exist before. Especially for those who believed in the prospects of U.S. economic growth but weren't direct participants.

Two stories were shared before: a retired woman in her sixties invested two paychecks into Apple stock after its first Super Bowl ad and never sold. A childhood neighbor invested in AOL in 1993; by the time it merged with Time Warner, the proceeds from selling the stock paid for all three of his children's college tuition and cleared his mortgage.

Today, there are almost no companies going public at stages similar to Apple in the 70s or AOL in the early 90s.

Even if you were just a janitor, you had the opportunity to invest in companies that were writing chapters of American history. The meritocracy of the market meant that if you were sharp enough, you could buy AOL stock in 1993.

And that's just the tip of the iceberg: a few visionaries noticed certain changes.

The broader, more socially significant impact was on those who didn't pay special attention to societal trends. They clocked in and out day after day. As part of the machinery that kept the system running, they got the chance to participate in creating enormous wealth.

Even if you weren't the savviest individual investor, even if you never bought a stock in your life, your retirement funds would always, at some point, be invested in the companies building the future. As a small cog in the capitalist engine, you didn't need to rely on luck.

You were already fortunate, thanks to a portion of your salary being invested in your future. Sometimes, you'd find yourself a small part-owner of a company that eventually became a cornerstone of the future.

Thanks to the support of this system, some companies grew to generate billions in annual revenue. But the people keeping this system running today cannot benefit from it because, in the eyes of the capital markets, they are not equal.

Under this dynamic, capitalism simply regresses to feudalism. A small group controls the era's means of production (land), while others work for them, and social mobility becomes an illusion. If companies don't go public, they are just rebuilding the same structure with different assets. Equity in transformative companies is the new land.

You must have a net worth of $1 million (excluding primary residence) or an income of $200,000 for two consecutive years. The median U.S. household net worth is about $190,000. By legal definition, they are too poor to invest in the future. Yet it is these median households that, through their work and consumption using these companies' products, give these companies value.

Without hundreds of millions of people using ChatGPT, OpenAI couldn't reach a $500 billion valuation. Users create value. No matter how many B2B transactions occur in the middle, the end of the chain is always individual consumers. They should at least have a chance to get a piece of the pie.

In a way, it might even be worse than feudalism now: at least farmers knew they were farmers. Today, people "participate in capitalism" through 401(k) plans but are systematically excluded from the most transformative wealth markets.

The rich getting richer has always been how capitalism works. But until recently, America's strong capital markets at least that you had a stake in it. Winners would win, but you could participate in their victory.

You could have been one of AOL's first million users and said, "Cool, I'm going to invest in this company." Over the next six years, its stock rose 80-fold. Today, almost any good new product from any new company you use is not traded on the public markets.

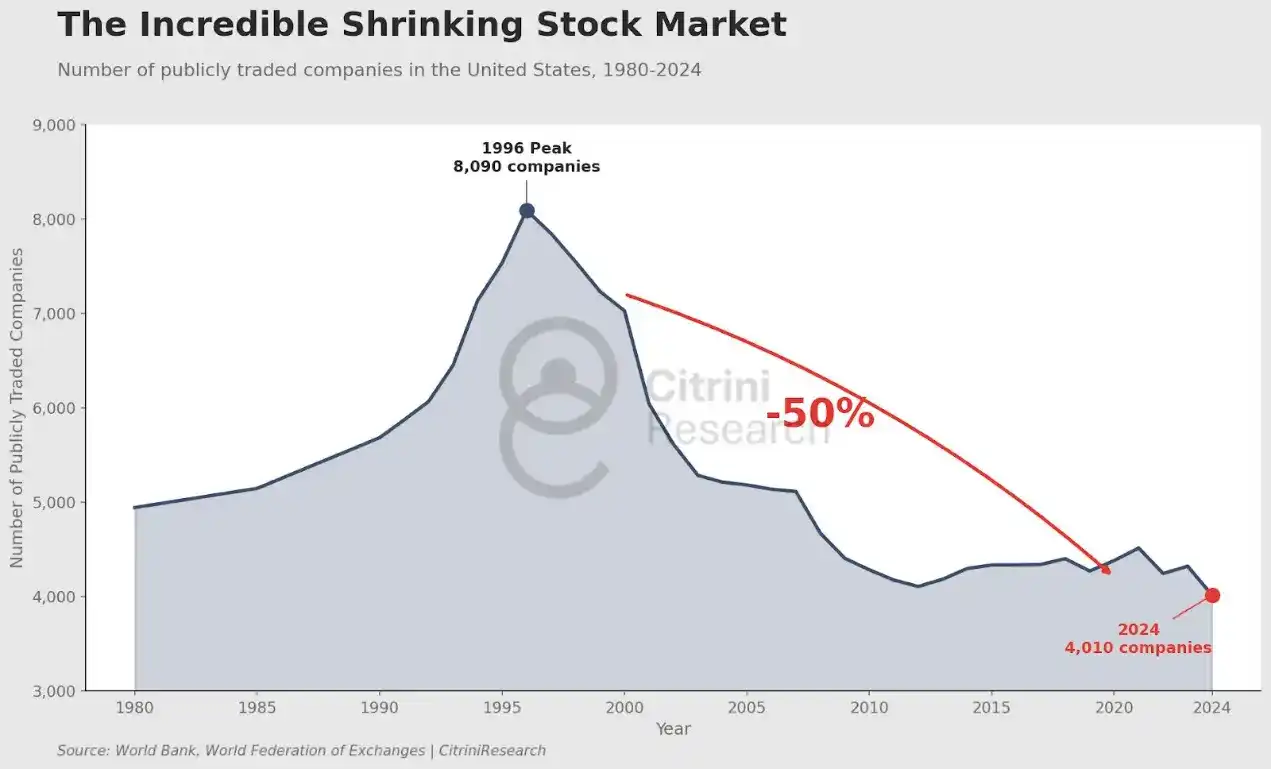

In 1996, there were over 8,000 publicly listed companies in the U.S. Despite the economy growing exponentially, today there are fewer than 4,000.

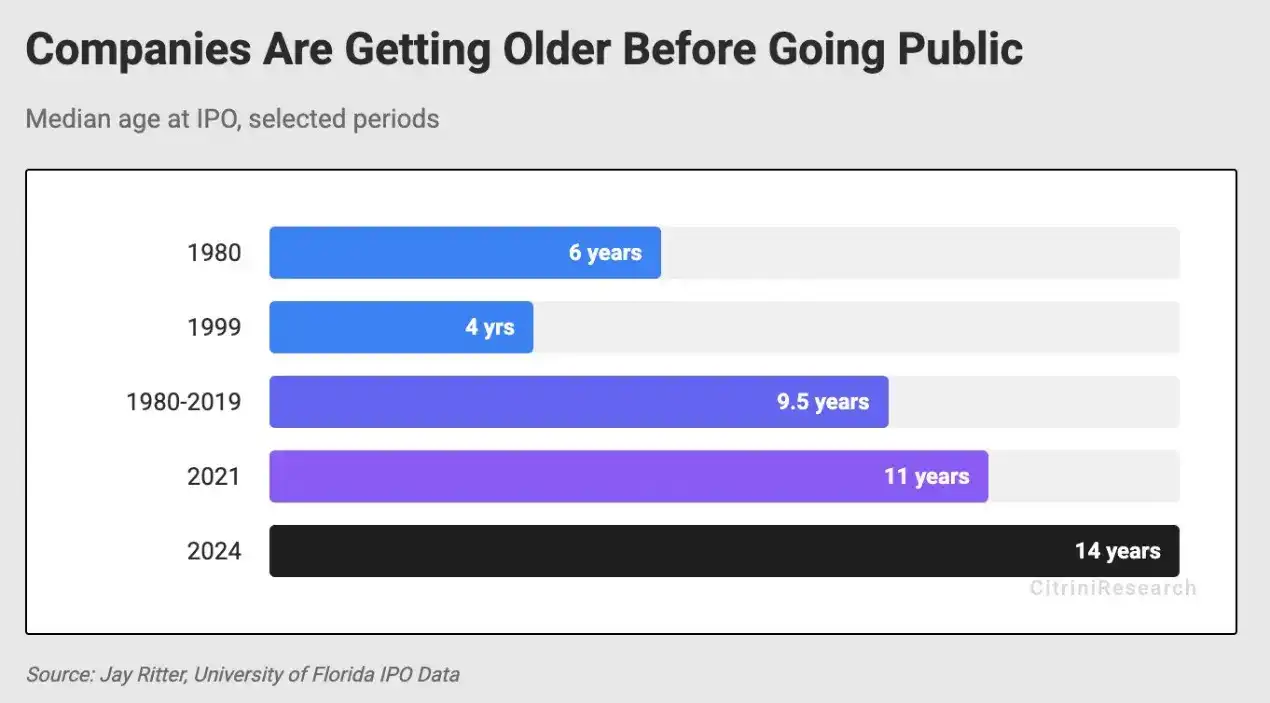

Adjusted for inflation to 2024 dollars, the median market cap of a company going public in 1980 was $105 million. In 2024, it is $1.33 billion.

The point here isn't about the median market cap. Nearly half of the market cap growth over the past century has come from the top 1% of companies.

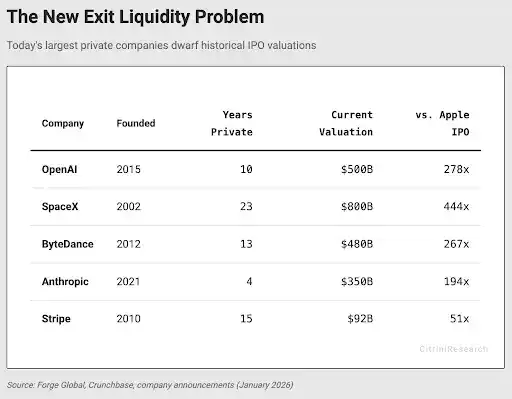

Anthropologie, SpaceX, OpenAI.

These companies should be among that 1%. Today, the only way for the public to participate in their growth is through an IPO after their growth rate has plateaued.

Amazon went public after just three years, with revenue of only $148 million and operating at a loss. Apple went public after four years.

When Microsoft went public in 1986, its market cap was about 0.011% of U.S. GDP. It created about 12,000 millionaire employees within a decade. Secretaries and teachers in Washington State also became millionaires by buying and holding stock in this software company.

SpaceX is arguably one of today's most inspirational and landmark American companies, valued at $800 billion. That's about 2.6% of GDP.

OpenAI recently closed a funding round at $500 billion and is reportedly trying to raise another $100 billion at an $830 billion valuation. In October 2024, its valuation was $157 billion. If OpenAI had gone public then, it would likely have been quickly included in the S&P 500, perhaps becoming the sixth or seventh largest holding in the index (or even higher, given how AI companies trade).

However, the bulk of this新增 value will not land in the hands of U.S. citizens but will flow to venture capital and sovereign wealth funds.

Adjusted to 2024 dollar values, Apple's market cap at IPO was $1.8 billion. It wouldn't even crack the top 100 companies by market cap.

In 1997, Amazon went public with a valuation of $438 million. The process was messy and volatile. Its stock fell 90% during the dot-com bust.

But because the public bore this volatility, they also reaped the subsequent 1700x gain.

They didn't need enough capital to invest in a VC fund or "network." The barrier to entry was simply the price of a share.

Look at Uber.

This is a company that would have captivated ordinary public investors in any era because Uber rides were everywhere. However, when Uber went public in 2019 at an $89 billion valuation, its value had already grown about 180x from early VC rounds.

If this were the 90s, individual investors might have had a chance to notice the world changing. Imagine an Uber driver noticing the company in 2014 when it hit 100 million cumulative rides (valued at $17 billion then) – that would still have been a 10x return, a 22% CAGR.

But the reality is, the public only got about a doubling of Uber's stock price in nearly seven years since IPO.

Let's be clear: this is not a call for all startups to go public. Those who invested in Uber's seed to C rounds clearly took significant risks and were richly rewarded.

But by the time Uber did its D round, one must ask if staying private was just to ensure a smoother path to market dominance, easier cashing out, with all gains ultimately flowing to the VC circle.

It must be reiterated: venture capital has been an indispensable part of technological progress. Many companies that would have been weeded out by the market likely survived because they could raise funds from a group of long-term investors.

But if VCs want the game to continue, they need to ensure the whole system doesn't collapse under its own weight.

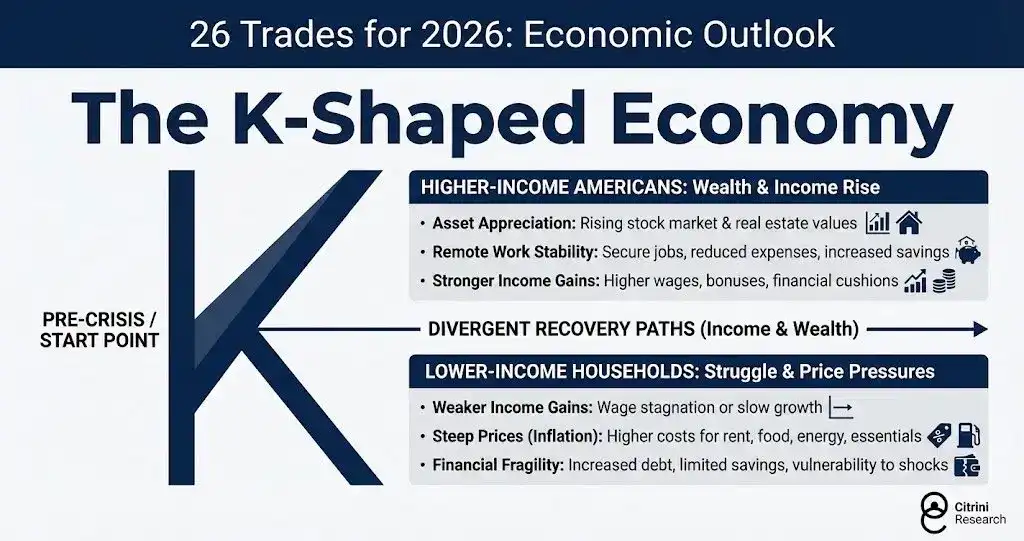

We are already seeing the emergence of a "K-shaped economy."

High-income Americans: Wealth & Income Growth:

- Asset Appreciation: Rising stock market and real estate values.

- Remote Work Stability: Job security, reduced spending, increased savings.

- Stronger Income Growth: Increased wages, bonuses, and financial buffers.

Lower-income Households: Struggling, facing cost pressures:

- Slowing Income Growth: Stagnant or slow wage increases.

- Soaring Prices (Inflation): Rising costs for rent, food, energy, and essentials.

- Financial Fragility: Mounting debt, limited savings, vulnerability to shocks.

There is more than one solution to this problem, but anything that increases asset ownership more broadly aligns incentives. The impact of AI will likely only exacerbate this dynamic. It will be much worse if the top part of the K becomes narrower because the beneficiaries are too concentrated. If public markets become merely liquidity exit tools for matured venture projects, this dynamic is inherently unsustainable.

Capitalism will give way to neo-feudalism. Social unrest will become more common.

In contrast, China might see more early and mid-stage AI companies go public this year than the U.S. The STAR Market looks strikingly similar to the Nasdaq of the early 90s, offering mass investors chances to create huge wealth. China seems to understand this helps build a strong middle class, while America seems to have forgotten.

Companies don't want to bear market volatility. They don't need to enter public markets until they are too big for VCs to fund them. VCs, knowing they can just mark up valuations in a higher round, don't push for IPOs either.

It's unclear if or how this changes, but it's clear the U.S. is heading towards a world where the S&P 500 is essentially a liquidity exit tool.

OpenAI and Anthropic will IPO as some of the world's largest companies, and the indices people rely on for retirement will be forced to buy their stock. By then, even if the stock performs well, the public will have been excluded from the wealth creation, damaging future returns.

The total value of companies on Crunchbase's unicorn list is $7.7 trillion, more than 10% of the S&P 500's market cap.

Given the list of some of the last century's most successful companies above, some might accuse this of survivorship bias. But that's precisely the point. Part of why investing in a passive index like the S&P 500 is so effective is that, over time, it tends to keep the good companies and weed out the bad. It benefits from companies' dominant periods, especially while they are actively on their way to dominance.

Apple was added to the S&P 500 just two years after its IPO, replacing Morton Norwich (a salt company that later merged with a pharma company, became responsible for the Challenger disaster, and was eventually broken up by private equity).

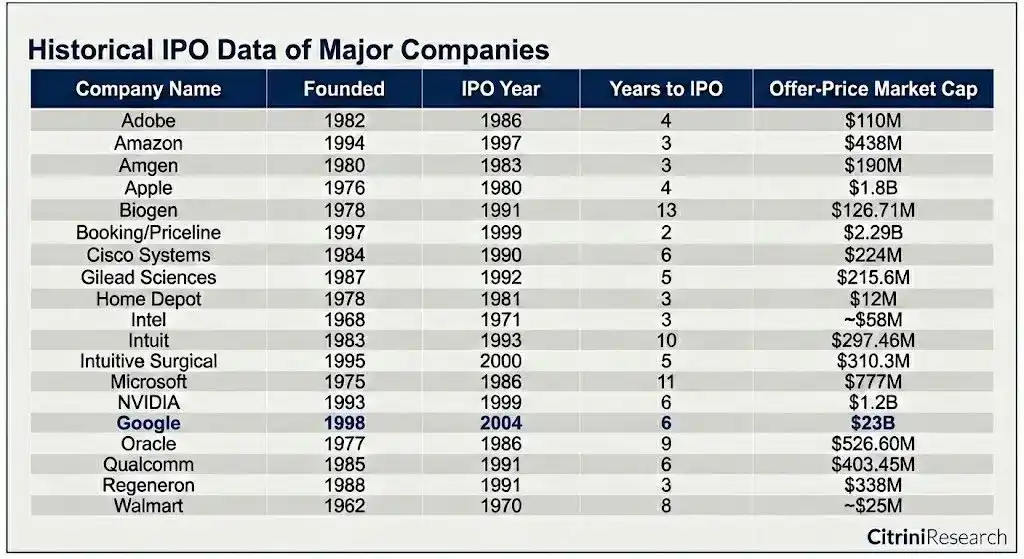

Look at the companies that truly created wealth over the past 50 years:

Even the largest IPO by market cap – Google ($23 billion) – was barely in the bottom of the top 100 companies then.

If we want the capitalist system to endure, we need to encourage people to invest. But if investing becomes merely a tool for a few to profit, the system is hard to sustain. Treating listing as an exit and restricting companies before they become national behemoths ignores the very system that created the conditions for their existence. If the returns from investing in era-defining companies are monopolized by a few, most people will gradually lose faith in the system.

It's unclear how this changes, or if the existing incentives are too entrenched to change, but if one has the power to change it, it should be improved.

Related reading: Robinhood vs Coinbase: Who is the next 10-bagger?