Author: @WazzCrypto, Legion

Compiled by: Frank, PANews

Observations on Prediction Markets in the Token World

Polymarket's Token Sale market has processed nearly $250 million in trading volume. The platform's advertised accuracy data is impressive: 100% accuracy in fundraising amount predictions and over 90% for FDV (Fully Diluted Valuation). However, a deeper analysis reveals that these numbers are misleading. The real signal is not what the crowd predicts, but how wrong they are.

By analyzing 231 prediction markets across 29 token sale events and cross-referencing Polymarket's historical probability data with actual token performance on CoinGecko, we found that "prediction markets are not reliable forecasting tools. Instead, they are actually sentiment indicators, and often a contrarian signal.

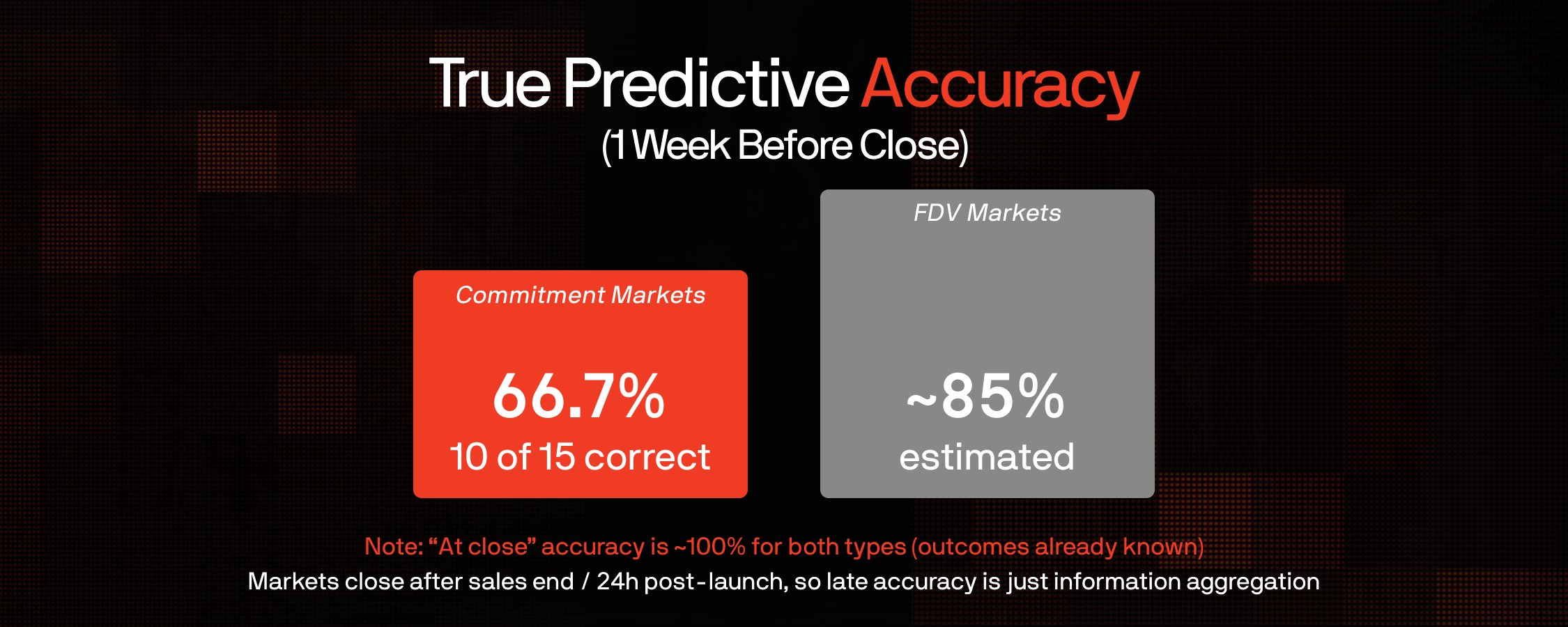

Key Finding: One week before market close, the real prediction accuracy was only 66.7%. At critical moments, the crowd is wrong one-third of the time, and incorrect predictions often show systematic over-optimism.

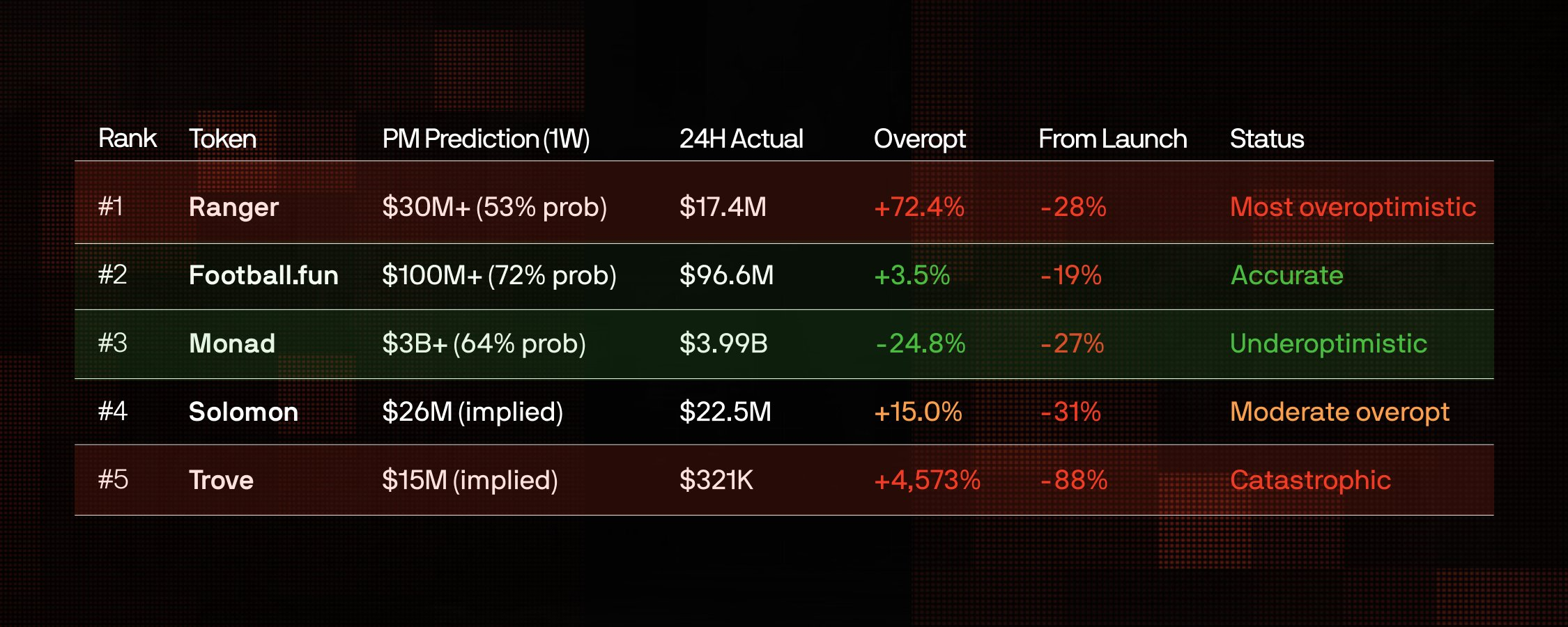

24-Hour Volatility Issue: Using CoinGecko's hourly data, we found that Polymarket's markets for "FDV above X 24 hours after launch" are essentially bets on extreme volatility. The average 24-hour price change was ±23% (e.g., Best performer: Monad +54.8%; Worst performer: Trove -38.7%). 75% of tokens faced selling pressure within 24 hours of launch. In this context, Polymarket's accuracy for 24-hour FDV predictions was only 62.5%.

The Fallacy of Accuracy: The Market is Wrong One-Third of the Time

When we track how market probabilities evolve over time, rather than just looking at static data at settlement, a completely different picture emerges. The fundraising amount prediction markets appear "100% accurate" because the final figures are inevitably leaked gradually as the sale progresses. Insiders and observers update prices accordingly; this is merely ex-post price discovery.

Key Insight: The reason fundraising and FDV markets tend towards 100% accuracy at close is because they settle *after* the outcome is largely certain. Fundraising markets close after the sale ends; FDV markets close 24 hours after launch. The only meaningful predictive metric is the accuracy one week before close, when genuine uncertainty exists. The 66.7% accuracy rate for fundraising predictions shows that, at the critical moment, the market is wrong 1/3 of the time.

Crowd Predictions Err on the Side of Excessive Optimism

We reviewed every prediction market where "crowd confidence exceeded 60% but ultimately failed to materialize." In every case, the error was consistent: over-optimism. The crowd consistently believed the raise would be higher and the valuation more expensive than reality.

This systematic bias suggests the participants in these markets are optimistic speculators, attracted to token sales precisely because they are bullish.

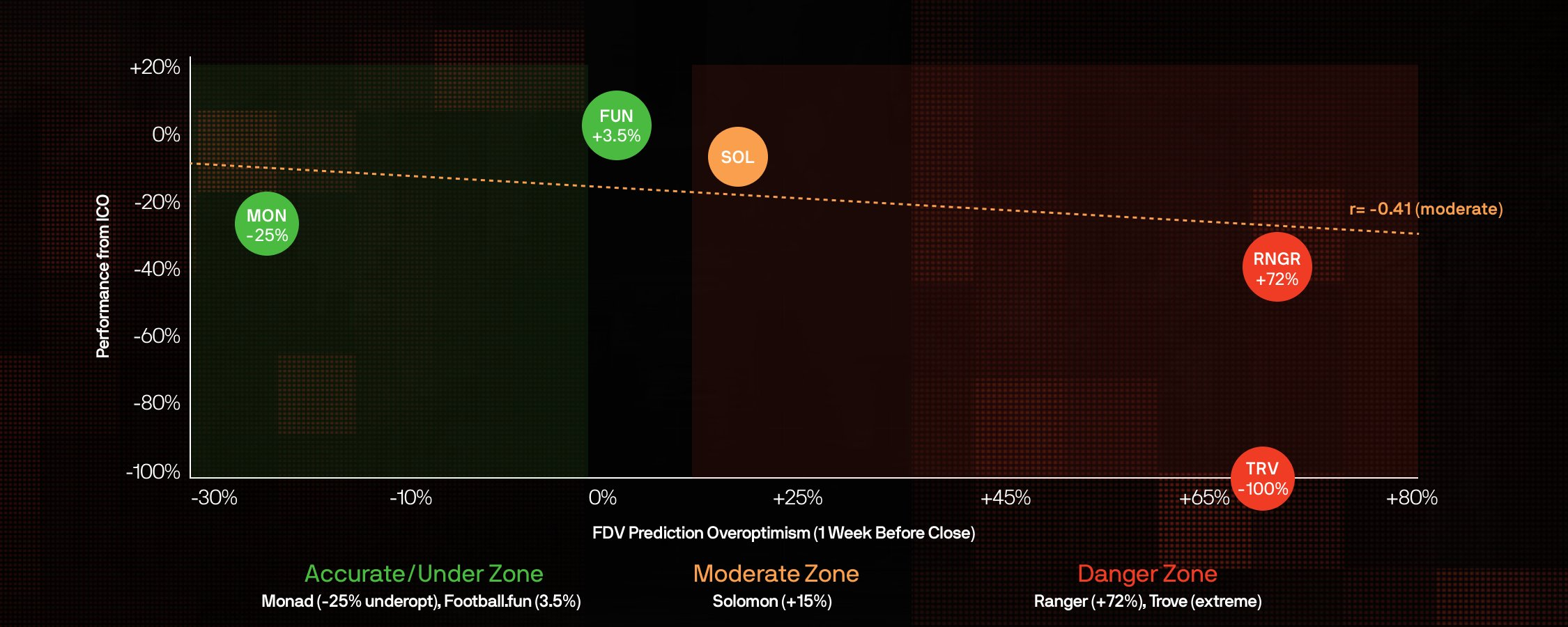

Over-Optimism vs. Token Performance (Based on ICO Data)

Methodology: This analysis only includes markets for projects that conducted a public ICO and have issued a token, using Polymarket odds from one week before market close.

Degree of Over-Optimism = (Polymarket Predicted FDV - Actual 24h FDV) / Actual 24h FDV.

The Y-axis shows price performance from ICO to current.

The data shows a moderate negative correlation (r=-0.41) between the degree of over-optimism and ICO returns. Monad was "underestimated/pessimistic" by the market (-25%), yet its price is still down 24% from ICO. Ranger was the most "over-optimistic" (+72%) and is currently down 32% from its ICO price. Only Football.fun remains above its ICO price (+1%).

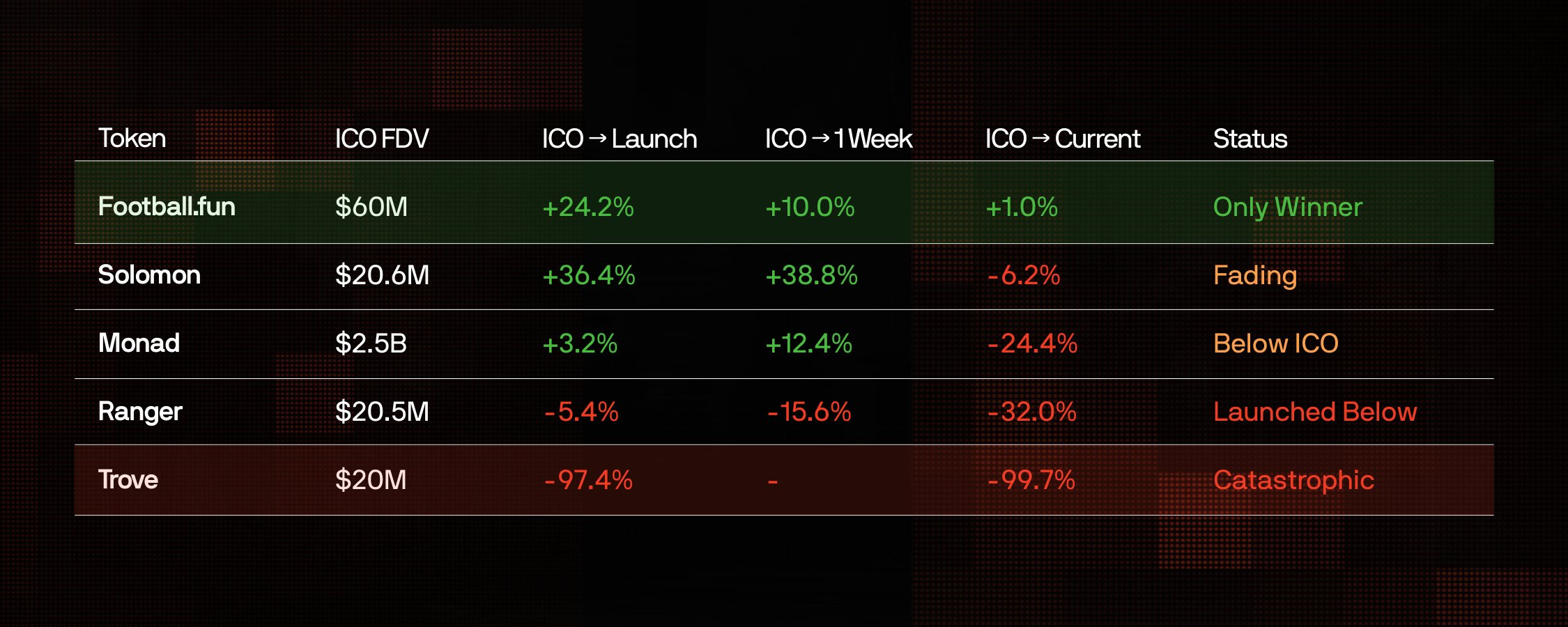

Token Performance Ranking: 40% Launch Below Valuation

The table below, using historical Polymarket odds from one week before close, reveals the true prediction accuracy. The pattern is clear: extreme over-optimism预示 disaster, and high trading volume on Polymarket, even when predictions are correct, is often a contrarian signal.

Key Finding: Among tokens with ICO data, 40% launched at a price below their ICO valuation. The average return from ICO to current is -32.2%. Only Football.fun is trading above its ICO price.

The pattern is brutal: Even tokens that launched above their ICO valuation (e.g., Monad, Solomon) eventually fell below the issue price. Football.fun is the only winner among the 5 ICO tokens in this dataset, currently just 1% above its ICO price.

Core Conclusions:

After analyzing 231 markets, $241.5 million in trading volume, and 8 tokens with verified 24-hour FDV data, several conclusions are clear:

-

"100% Accuracy" is meaningless. Markets close for settlement *after* the outcome is known (fundraising markets post-sale, FDV markets 24 hours later), so late-stage accuracy unsurprisingly nears 100%. But the real predictive accuracy one week before close is only 66.7%. At the critical moment, the crowd guesses wrong 1/3 of the time.

-

Systematic Over-Optimism. Among the top 15 markets, 5 markets showed over 60% confidence in thresholds that were never reached. FDV was overestimated by an average of +35%.

-

High prediction market volume is a contrarian signal. Monad ($89M) and MegaETH ($67M) had the highest degrees of over-optimism. The more money the crowd bets, the more confident they are, and the more wrong they tend to be.

-

Conservative Predictions = Better Outcomes. Tokens with relatively accurate predictions (Monad, Football.fun) fell less. Low hype and accurate predictions appear to be bullish signals.

Trading Signals:

Based on the analysis, we can distill actionable signals for evaluating future token sales. These are not absolute guarantees but represent patterns that held consistently within the dataset.

Bearish Signals:

-

Polymarket trading volume > $50 Million

-

FDV Over-Optimism degree > 50%

-

All FDV prediction thresholds are likely to fail

-

Fundraising amount Over-Optimism degree > 30%

Bullish Signals (Relatively)

-

Polymarket trading volume < $5 Million

-

FDV prediction偏差 within 20%

-

Multiple FDV prediction thresholds are met

-

Crowd expectations are relatively conservative

This asymmetry is important. Bearish signals are strong indicators of poor outcomes. Bullish signals are weaker, only suggesting the token might perform "less badly" than over-hyped alternatives. In a market where all tokens are down from their all-time highs (ATH), "losing less" is the best-case scenario.

Summary

Polymarket's token sale section is effectively a Hype Meter. The signal is not in the prediction itself, but in how much it deviates. When the crowd piles money into bets for higher valuations, caution is warranted. Historically, "extreme confidence" from the masses has often meant "maximum pain" for investors.