Article Compiled by: Block unicorn

Tokenization stitches together two very different worlds: the always-on, permissionless DeFi protocol, where prices fluctuate every few seconds, and the traditional fund, whose settlements follow the administrative timeframes of a group of permitted holders.

Merging the two requires masterful orchestration, but for those who can pull it off, there is immense value. In today's article, I explore who is behind the curtain, operating the bridges that connect these worlds, and who is capturing the value.

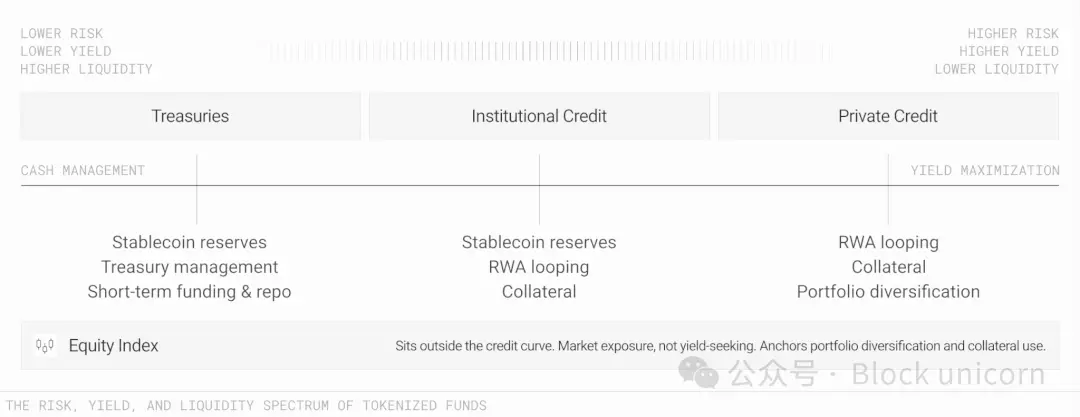

The size of tokenized real-world asset (RWA) pools exceeds $33 billion, with tokenized U.S. Treasuries accounting for about $15 billion. But notably, its share has slipped from 55% to less than 45% in just one year. Meanwhile, other tokenized funds have grown, including institutional credit funds (e.g., Apollo's ACRED) and private credit funds (e.g., Janus Henderson's JAAA).

The maturation of tokenization offers a range of choices for treasurers or CFOs managing corporate cash, across varying risk appetites. Those seeking low risk, low returns but high liquidity can opt for Treasury funds, while those pursuing higher yields and stronger programmability can choose riskier investment options. The safety of yields is no longer the concern it once was. These instruments backed by Treasury funds are audited by the same auditing institutions that audit traditional bonds.

This is the strongest argument that real-world asset tokenization is on the verge of a boom among institutional investors.

If someone asks me what the difference is between off-chain and on-chain money, I'd say it's composability. It is composability that allows one dollar to serve a greater purpose across multiple channels, achieving higher compound growth. The ability to cash out instantly and to put your money to more efficient work makes them seem like funds on steroids.

Traditional finance makes us choose between yield, liquidity, and transferability. Tokenized funds, if managed well, can give us all three at once.

But "managed well" is no simple task. The composability of funds involves an engineering problem.

Stitching Together Two Very Different Worlds

Blockchain brings speed, cost-effectiveness, and rapid settlement to tokenized risk-weighted assets (RWAs). But a tokenized money market fund is still a fund, not a stablecoin. It still needs its net asset value updated once every business day, following the fund manager's schedule. It still needs to maintain a KYC'd holder group. For example, BlackRock's BUIDL has a $5 million minimum investment threshold, while Circle's USYC is restricted to non-U.S. persons. It still needs to adhere to redemption cutoffs because its underlying Treasury settlement relies on off-chain infrastructure with a settlement cutoff at 5 p.m. ET.

This is the legal essence of the product. Remove daily NAV settlements, and it's no longer a money market fund. Remove the whitelist, and the SEC will come knocking.

So how can a fund maintain its set timeline, holder setup, and redemption window while also having the token representing its shares flow at internet speed? The fund needs specially built infrastructure to maintain NAV at period-end, support epoch-based settlement, and adhere to strict legal boundaries when moving assets across blockchains. It's a tricky co-existence puzzle.

A recent report jointly published by LayerZero and Centrifuge describes how they solved this.

Resolving the Conflict Points

Three conflict points determine whether this coexistence model can succeed. If the orchestration layer gets these right, the fund can run at internet speed without breaching legal boundaries.

The first is price.

What is the token worth between two NAV settlement cycles? Some issuers freeze the token price at yesterday's level and accept the stagnation. A frozen price is easily manipulated when rates move during the day. A continuously moving price is harder to manipulate, but also harder to reconcile with the fund's actual books.

The second is the compliance factor.

Where does the whitelist verification layer run? If it runs on every transfer, the token cannot touch open DeFi and can only move between approved wallets. If that layer is wrapped inside a vault, the vault holds the regulated shares and issues a freely transferable receipt token to holders who have passed KYC once. That receipt can be composed through DeFi, with compliance embedded in the vault, not checked on every transfer. Centrifuge's deRWA framework is a good example.

The third conflict arises when moving assets across chains.

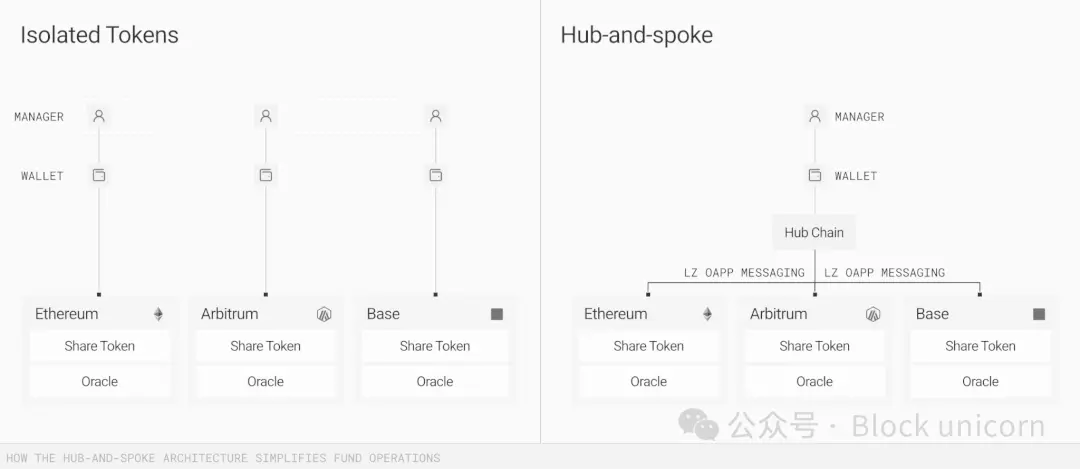

When a tokenized fund is deployed on nine chains, you need a single source of truth for ownership and value. While on-chain infrastructure can update in real time, discrepancies still need to be updated and reconciled across nine chains. The more failure points, the more chances for error.

LayerZero and Centrifuge solved this by building a hub-and-spoke model. In this model, one authoritative chain manages NAV, accounting, and compliance. A messaging layer (orchestrated by LayerZero in this case) pushes these updates to the spoke chains where tokens are actually used.

Centrifuge's V3 architecture is built exactly on this, where each pool chooses a hub chain as its source of truth, branch chains as distribution terminals for deposits, and enabling DeFi composability. LayerZero transmits operational data between the chains to keep NAV updates, compliance instructions, and cross-chain balance states in sync.

This is the coveted yet essential orchestration I mentioned earlier, which delivers value to those who can execute it. Whoever can maintain a fund's authoritative state consistently across chains becomes very hard to replace. While fund managers still own time, and blockchains still own composability, someone in the middle must enable both.

The most fragile part of asset movement is accounting for assets in transit.

When an asset is in transit between chains, it can temporarily disappear from the fund's visible balance sheet. Centrifuge V3 issues tokenized confirmations for assets in transit, so the fund's balance sheet remains continuous even while the underlying token is still moving. This is the on-chain equivalent of trade-date accounting. Tedious, but crucial.

Why should institutional investors consider tokenized funds despite these conflicts?

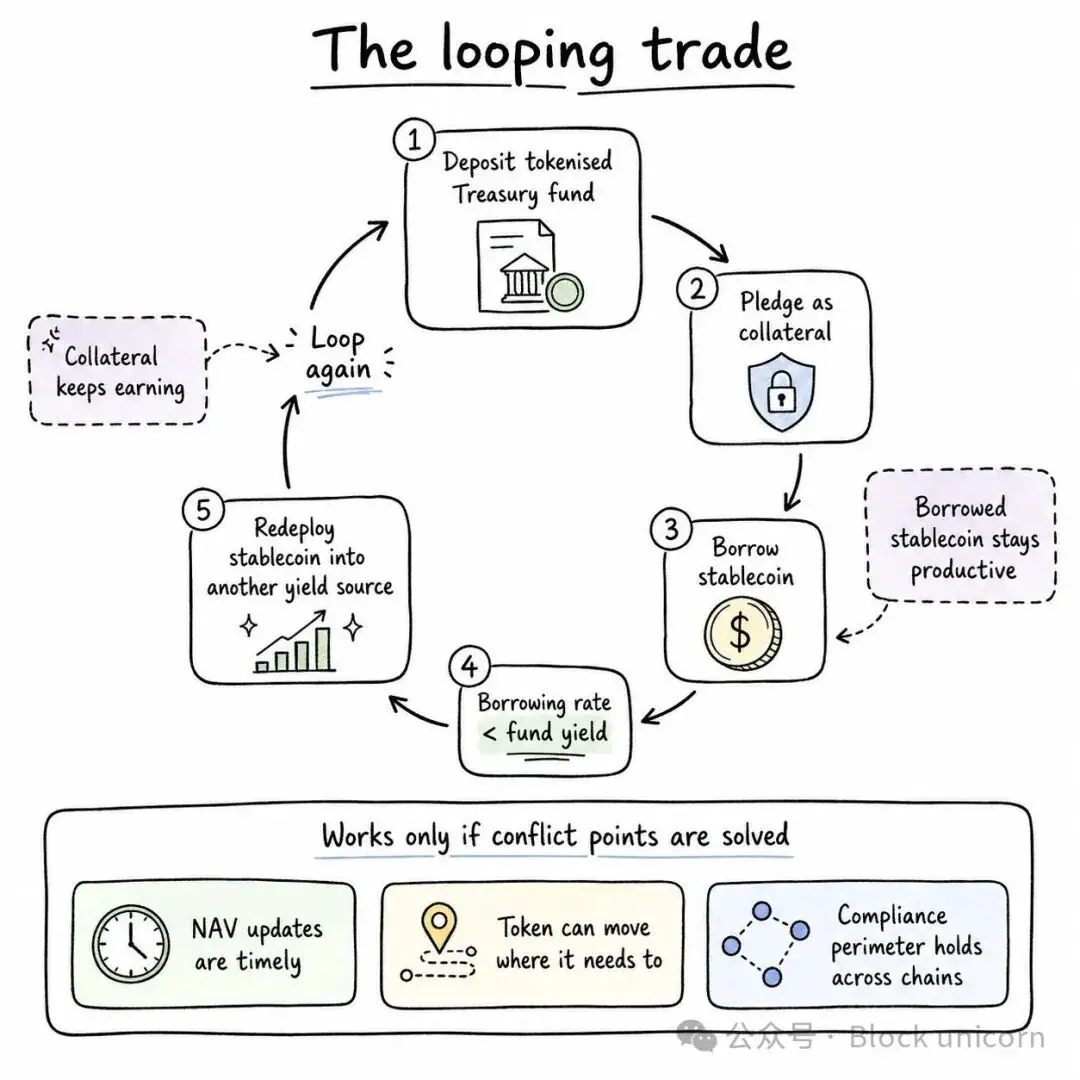

One of the best ways to optimize idle cash via tokenization is round-tripping. A treasurer can deposit tokenized Treasury funds and borrow stablecoins against them as collateral. If the borrowing rate is lower than the fund's yield, holding the fund earns a profit. The treasurer can then redeploy the stablecoin proceeds into other yield sources and repeat the cycle.

The entire round-trip only works if the above conflict points are resolved. This is the next challenge for those building tokenization infrastructure. These conflict points have been exploited in the past. For instance, if the on-chain NAV price for a smaller tokenized product stays constant for two to four hours and lags the underlying asset price, it creates an arbitrage opportunity until the next NAV price spikes.

A redemption gate conflict can occur when off-chain NAV triggers liquidity limits, if independent on-chain smart contracts try to process token redemptions instantly. This leads to smart contracts holding "orphaned" or unexecuted token transactions that keep trying to execute simultaneously against the off-chain caps.

Large private credit funds and business development companies (BDCs) are facing this right now. Three weeks ago, Apollo Global's $26 billion private credit fund, the Apollo Debt Solutions fund (ADS), had to cap redemptions at 5% after investors tried to redeem about 16.8% of the fund. If something similar happened to a fund that also trades a tokenized version, it would be hard to rule out a redemption gate conflict. In Q2, investors redeemed $15.6 billion from broadly held private credit funds, up from about $13.9 billion in the previous quarter.

Faults can occur in cross-chain message delivery, leaving positions not fully settled. Only by monitoring every failure mode, with credentialed people accountable, can institutional trust be won.

If tokenization is to live up to its apparent potential, it must navigate the following challenges. It is not just about putting U.S. Treasuries on-chain or creating a new asset class. Those building the infrastructure must break the old rules that force investors to choose between yield, liquidity, and transferability. If tokenization can make a dollar do multiple jobs at once without compromising the credibility brought by existing safeguards, institutions sitting on billions in cash will certainly take note.

I've written before that SWIFT, as the orchestration layer of today, has more value and influence than any party on either side of the network it serves. Visa is also worth more than all the banks it serves globally, except JPMorgan.

That is the incentive for being the orchestration layer in an evolving financial world. It can secure a seat at the table in capital markets for the next decade. Centrifuge is defining the role on the fund side, while LayerZero is building the bridges that connect the pieces.

That's all for today. See you in the next article.