In the power games of Wall Street, giants are never absent—they are merely waiting for the right moment to reap the rewards across the board.

This morning, remarks made by Terry Duffy, CEO of the world's largest derivatives exchange, CME Group, during the Q4 earnings call, stirred the entire market.

Duffy revealed that CME is actively exploring the issuance of its own digital token: "CME Coin."

This move is not merely a technical experiment. Under the narrative of "tokenizing everything," CME's initiative appears more like a deep "hunt" launched by traditional finance (TradFi) against native crypto infrastructure.

1. The Mystery of Its Role: A Chip or Ammunition?

Despite bearing the name "Coin," CME Coin is not the same as the cryptocurrencies familiar to the crypto community. From Duffy's brief response, the following key points can be distilled:

The token is designed to operate on a decentralized network.

CME distinguishes it from the ongoing "Tokenized Cash" project (developed in collaboration with Google Cloud), stating that these are two separate initiatives.

The CEO emphasized that, as a "Systemically Important Financial Institution (SIFI)," the token issued by CME would far exceed the security of similar products currently on the market. (Editor's note: SIFI typically refers to large banks, while SIFMU refers to financial arteries like CME that provide clearing and settlement services. CME's SIFMU status grants it access to Federal Reserve accounts.)

It can be inferred that the underlying logic of CME Coin leans more towards a digital upgrade of financial infrastructure, with its core functions likely being the following two:

Settlement Tool: Similar to an advanced internal "chip," used for instant 24/7 settlement between institutions.

Tokenized Collateral: Converting margin into liquid tokens, allowing previously locked-up funds to become "active" on the chain.

2. Why Now? CME's Triple Agenda

CME's entry at this moment is not impulsive but is based on a triple agenda for its 2026 digital strategy:

Solving "Weekend Liquidity Drought"

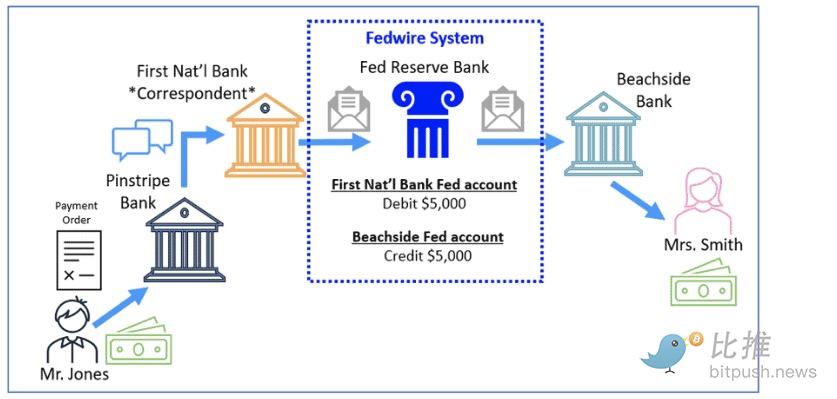

CME has already planned to fully launch 24/7 trading for crypto futures in 2026. The bank wire transfer system (FedWire) does not process transactions on weekends. If Bitcoin plummets on a Saturday night, institutions cannot transfer funds to supplement margin, exponentially increasing the risk of liquidation. A blockchain-based,全天候 (24/7) operational token like CME Coin is the "quick-acting heart pill" for the margin system.

Recapturing Lost "Interest Profits"

Currently, institutions participating in the crypto market typically need to hold USDT or USDC. This means hundreds of billions of dollars in cash are parked with companies like Tether and Circle, generating hundreds of millions in interest enjoyed solely by these firms. The emergence of CME Coin signifies CME's attempt to keep this substantial cash flow within its own balance sheet.

Building a "Compliance Moat"

With BlackRock issuing its BUIDL fund and J.P. Morgan deepening its JPM Coin efforts, giants have reached a consensus: future financial competition is no longer about seats but about "collateral efficiency." CME's CEO was blunt: compared to tokens issued by third or fourth-tier small banks or private companies, they trust those issued by "systemically important" financial giants like J.P. Morgan (SIFI) more. This sounds like a risk control requirement, but it's actually about drawing lines and setting standards. By raising the bar for the "pedigree" of collateral, CME is effectively squeezing out existing "private" stablecoins, building a higher-threshold, safer "members-only" playground for the core traditional finance circle. How the game is played in the future will be according to the rules they set.

Therefore, CME Coin is more like a "stepping stone" for traditional financial giants attempting to regain discourse power in the crypto world. This show has just begun.

3. Erosion of Existing Stablecoins?

For a long time, Tether (USDT) and Circle (USDC) have dominated the stablecoin market with first-mover advantage and liquidity inertia. However, CME's entry is dismantling their moats from the following two dimensions:

It's an Asset, But More Importantly, "Liquid Clearing Power"

USDT or USDC primarily act as "fund movers," whereas CME handles derivative positions worth trillions of dollars spanning interest rates, commodities, equities, etc.

Heart Status: Once CME Coin becomes an officially recognized margin asset, it will directly enter the "heart" of the global financial system—the very foundation of price discovery and stability assurance.

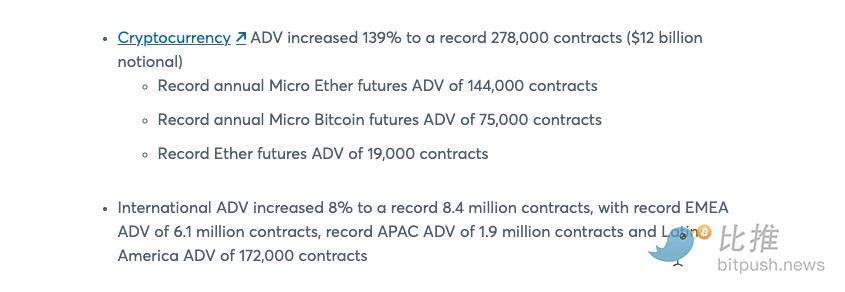

Forced Holding: CME Coin captures the "clearing flow." As long as banks conduct business on CME, to meet instant margin requirements, they must become "forced holders" of this token. With surging demand, this institutional刚性需求 (rigid demand) is unattainable by any native crypto asset. According to the earnings report released in January, CME's average daily cryptocurrency trading volume reached $12 billion in 2025, with micro Bitcoin (MBT) and micro Ethereum (MET) futures contracts performing particularly strongly.

Collateral as Sovereignty: Reshaping the Market's "Digital Throat"

In modern finance, collateral is the real throat. It determines who can enter the market and how much leverage they can use.

Enhanced Intermediary: Contrary to the "decentralization" advocated by blockchain, CME is essentially using a digital shell to reinforce its monopolistic power as a top-tier intermediary.

Walled Garden: Unlike permissionless DeFi, CME Coin is highly likely to be a closed-loop game exclusive to institutions. It has no open governance, only legally protected clearing rights.

Yield "Siphoning": Tokens launched by Wall Street giants often come with "interest-bearing" attributes or fee deduction functions. Faced with risk-free U.S. Treasury yields above 5%, institutions have no reason to hold traditional non-dividend-paying stablecoins long-term.

Summary

Looking at the bigger picture, CME's strategy is not alone. J.P. Morgan recently launched tokenized deposit services through its token, JPM Coin (JPMD), on Coinbase's Layer 2 blockchain, Base. Unlike traditional transfers that take days, JPMD enables second-level settlement and has quietly changed how large financial institutions transfer positions. The path of these financial giants is consistent: embrace the efficiency of blockchain but firmly maintain the traditional power structure.

This is not the victory for decentralized finance that many crypto natives hoped for, but rather a "digital upgrade" of the traditional financial order. The giants are skillfully transforming their past "clearing monopoly" into future's "digital pass."

Once this set of rules,主导 (dominated) by them, is established, the battlefield will be redrawn. Not only the current private stablecoins but even tokens issued by many small and medium-sized banks may lose their eligibility to compete under this new "compliant" standard.

Author: seed.eth

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush