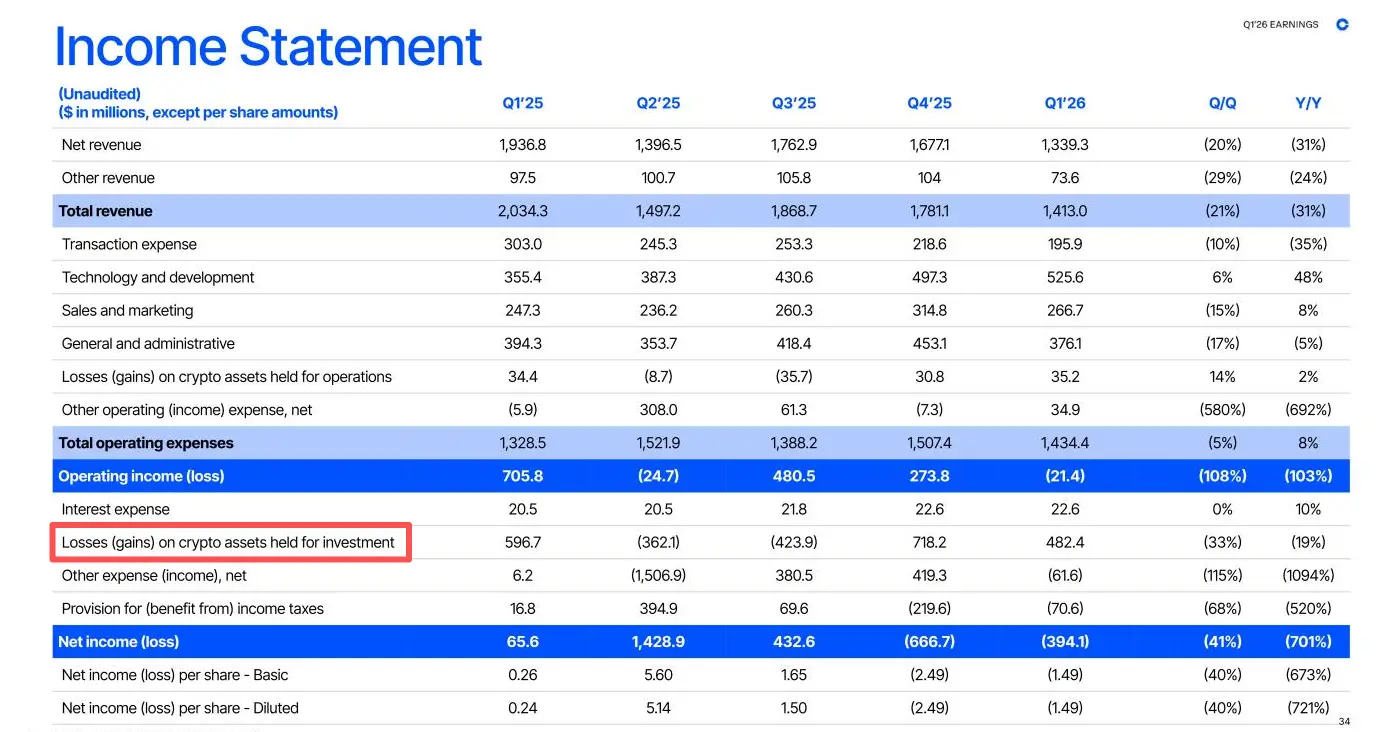

On May 7th, after the US stock market closed, Coinbase released its first-quarter financial report for 2026. The data showed the company's total revenue was $1.41 billion, a year-on-year decrease of 31%.

Dragged down by unrealized losses on held crypto assets, the company recorded a net loss of $394 million, with a loss per share of $1.47. In contrast, the company achieved a net profit of $66 million in the same period last year.

Following the earnings release, Coinbase's stock price fell approximately 4.7% in after-hours trading. The cumulative decline for the year-to-date has now exceeded 15%.

Transaction Revenue Down 40%, Institutional and Stablecoin Business as Bright Spots

Most of Coinbase's loss this quarter came from paper losses.

Behind the net loss of $394 million is an unrealized loss of $482 million from the company's investment crypto assets. This loss is accounted for with market price fluctuations and does not represent an actual cash outflow.

Excluding this portion, the company's adjusted net loss was only $45.6 million, and adjusted EBITDA remained positive at $303 million, with an operating loss of approximately $21.4 million.

The crypto market was generally weak in Q1. The price of Bitcoin fell from over $97,000 in early January to around $63,000 in early February, hovering below $70,000 by the end of the period. Market sentiment shifted rapidly, and retail trading activity contracted significantly. According to CoinGlass data, global crypto spot trading volume in Q1 was approximately $1.94 trillion, down about 44% year-on-year.

As a result, the company's total transaction revenue declined 40% to $756 million, with consumer transaction revenue at $567 million, a 48% year-on-year drop. Despite the halving of trading volume, Coinbase's global crypto spot market share rose to a record high of 8.6%, ranking fourth among global spot exchanges.

The institutional side, however, showed a completely different trend. The company's institutional transaction revenue reached $136 million, a 37% year-on-year increase. More notably, the derivatives business stood out, with derivatives trading volume growing 169% year-on-year, benefiting from the consolidation of Deribit acquired in August 2025. The collateral pledged by derivatives clients also surged from $27.4 million at the end of last year to $333 million at the end of this quarter, an increase of more than 10 times.

In terms of subscription and services revenue, the company recorded $584 million for the quarter, a 14% year-on-year decline, a significantly smaller drop than the transaction business. This segment's share of total net revenue increased to 44%. Notably, stablecoin revenue was $305 million, up 11% year-on-year, one of the few bright spots this quarter. Total assets on the platform stood at $294.4 billion at the end of the quarter.

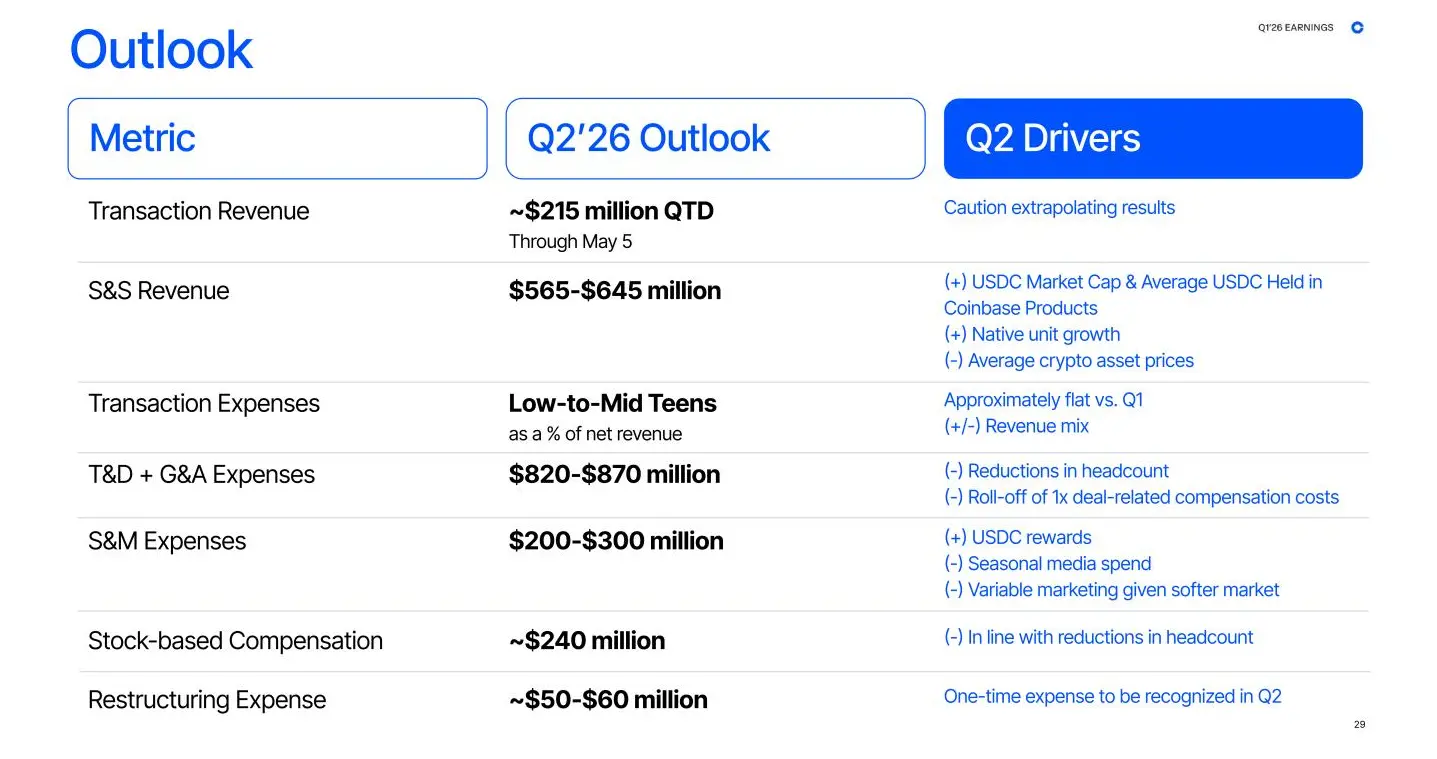

For Q2, management's outlook is generally cautious. The company disclosed that transaction revenue through May 5th was approximately $215 million, but management emphasized that current market volatility is high and this figure does not represent the trend for the entire quarter. The guidance range for subscription and services revenue is $565 million to $645 million, with the midpoint slightly above Q1's $584 million, indicating management's continued confidence in this revenue line. Restructuring expenses related to the recent layoffs, amounting to $50 to $60 million, will be recognized in Q2. Cost pressure is expected to ease significantly thereafter.

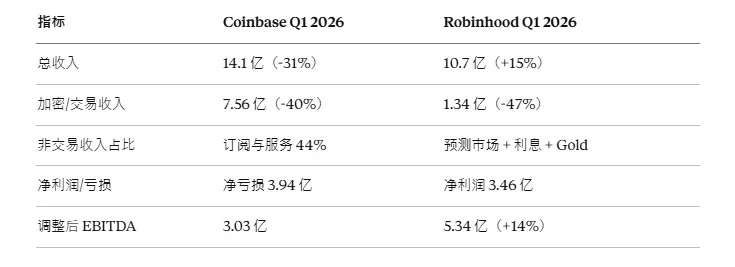

It is worth noting that Robinhood's Q1 earnings report presented a different picture. Its total revenue increased 15% year-on-year to $1.07 billion, with a net profit of $346 million and adjusted EBITDA reaching $534 million.

Examining the structure, the quality of this growth warrants scrutiny. Crypto-related revenue also declined 47% to $134 million. The company mainly filled the gap with three business segments: revenue from prediction market contracts skyrocketed 320%, becoming the largest incremental source; net interest income grew 24% to $359 million; and Gold subscription service revenue grew 32% to $50 million.

Additionally, Robinhood secured the role of sole initial trustee for the Trump account, investing approximately $100 million in related setup costs.

This quarter, Robinhood sustained growth through the policy tailwinds of prediction markets and the Trump account, while Coinbase bet on a longer-term transformation under the pressure of halved trading volumes.

Defensive Moves: Laying Off 700 Employees, What Is the Company Restructuring?

On May 5th, just two days before the earnings release, Coinbase announced cutting approximately 700 jobs, representing about 14% of its global workforce.

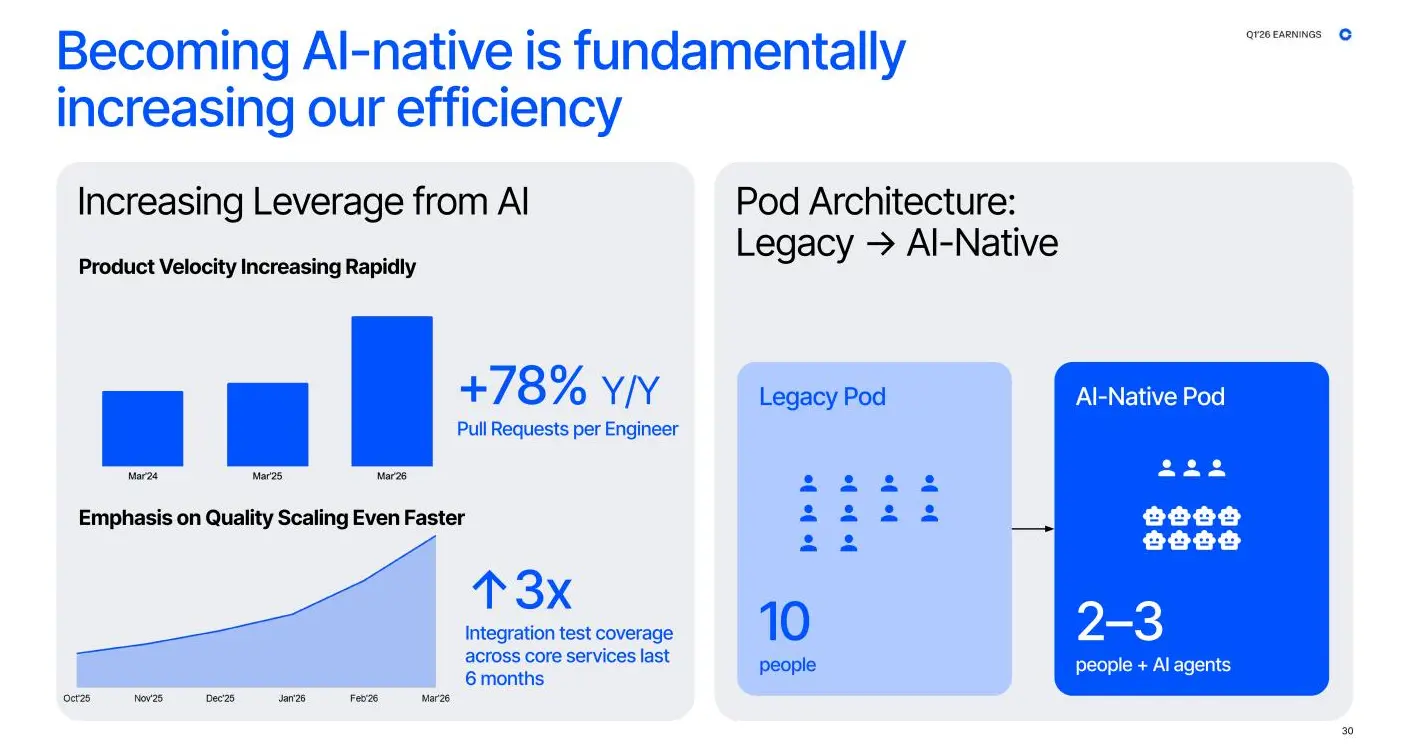

CEO Brian Armstrong stated that this restructuring aims to bring the company back to startup speed and accelerate the transition to an AI-native organization. The goal is to refactor Coinbase into an organization with intelligence at its core, augmented by humans at the edges.

Coinbase defines this approach as "AI-native"—not just introducing AI tools into the existing organization, but redesigning the company's operational model from the ground up. Company data shows a 78% year-on-year increase in engineer pull requests per capita. Team structures have been reorganized from traditional 10-person pods to AI-Native pods consisting of 2-3 people plus AI agents. Core service integration test coverage tripled within six months.

However, the financial implications need to be carefully considered. Omar, a partner at crypto venture capital firm Dragonfly, estimates that this layoff could save the company approximately $225 million in annual salary costs. But the full-year 2026 expense guidance indicates that, excluding the impact of increased USDC rewards, expenses will be roughly flat year-on-year. In other words, a significant portion of the cost savings from layoffs is offset by investments in user incentive programs.

It is also worth noting that over the past year or so, OpenAI has poached at least six senior marketing executives from Coinbase, including former CMO Kate Rouch, Sarah Russell, and others. Sarah Wolf, head of marketing for the Base chain, moved to Anthropic. Coinbase officially characterized these departures as normal personnel movement, but it is noteworthy that while the company is using AI to restructure its organization and reduce headcount, it is also supplying AI companies with marketing talent who best understand branding and growth.

When asked about potential future layoffs, CFO Alesia Haas stated, "We can't predict the future, but as a public company, we will always do what is best for the company."

Offensive Moves: Building On-Chain Financial Infrastructure

The "Everything Exchange" Blueprint

At the end of last year, Armstrong proposed the strategic goal of an "Everything Exchange"—transforming Coinbase from a primarily spot crypto platform into a comprehensive multi-asset platform encompassing derivatives, commodities, futures, and prediction market contracts, allowing users to avoid switching between different platforms.

Q1 data shows strong growth in derivatives, prediction markets, and decentralized exchanges. On the Base chain, stablecoin transactions initiated by AI agents already account for 90% of total chain transaction volume. Derivatives trading volume reached a record high, with contract business exceeding spot trading for the first time.

With initial results showing, the company has continued to double down recently, including: investing in Centrifuge to secure the tokenization infrastructure for RWA; taking a stake in Kemet to integrate institutional derivatives channels; launching the stablecoin credit fund CUSHY; obtaining the OCC national trust charter to clear the compliance hurdle for institutional custody; and partnering with AWS to integrate wallet infrastructure and the x402 protocol into Amazon Bedrock's AgentCore payment system, enabling AI agents to autonomously complete micropayments using USDC.

The Stablecoin Moat

Beyond expanding trading categories, the stablecoin business constitutes a deeper revenue moat for Coinbase.

According to Coinbase's revenue-sharing agreement with Circle, 100% of the earnings generated by USDC held on the Coinbase platform go to Coinbase, while off-platform USDC earnings are split approximately 50/50 between the two parties.

USDC's market capitalization has now reached a record high of approximately $80 billion, with over 25% held on the Coinbase platform. The balance on the platform has grown nearly 10-fold compared to three years ago. As USDC adoption continues to expand, Coinbase's share of the pie grows proportionally.

However, this revenue stream is not without risks. This quarter, the average interest rate declined by 67 basis points, negatively impacting stablecoin revenue by approximately $57.5 million. Changes in the interest rate environment may weaken the resilience of this revenue line.

CFO Alesia Haas emphasized during the earnings call, "Our USDC contract automatically renews every three years, and it renews in perpetuity. This contract cannot be terminated." CLO Paul Grewal added immediately, "We expect to continue our partnership with Circle on the same terms going forward."

These statements were clearly addressing market concerns about stablecoin regulation legislation. Regarding the CLARITY Act, Coinbase has engaged in a prolonged game of chess:

- In January, it withdrew support due to unfavorable earnings provisions, causing the Senate to delay the vote;

- In March, it rejected a new draft again, causing Circle's stock price to plummet 20% in a single day;

- In early May, a compromise text emerged, prohibiting "pay for hold" but retaining space for rewards tied to real activities. Armstrong replied "Mark it up" on X, and Grewal also publicly expressed being "very confident" about the bill passing this summer.

The true value of this game is that Coinbase is not just complying with rules but participating in shaping them. The legal teams, compliance processes, and regulatory communication capabilities required to repackage yield products constitute a resource barrier that smaller exchanges cannot replicate in the short term.

In other words, once the CLARITY Act is enacted, the advantages of leading platforms will be solidified by legislation. Regulatory clarity is beneficial for the entire industry, but the deepest beneficiaries will always be the few capable of sitting at the negotiation table.

However, it is noteworthy that after the bill passes, there will be a 12-month rule-making phase, and the final boundaries are yet to be defined, leaving uncertainties.

Conclusion

With trading volume halved and a net loss of $394 million, Coinbase's earnings report once again reminds the market that the company remains strongly tied to the crypto cycle. There is no shortage of skeptical voices questioning whether the AI narrative represents a genuine transformation or merely a wrapper for declining business performance.

Brian Armstrong has repeatedly emphasized, "All finance will eventually move on-chain." As crypto increasingly resembles traditional finance, Coinbase is also striving to make itself look more like a mature financial infrastructure company. This might be the answer it is offering in the current cycle.