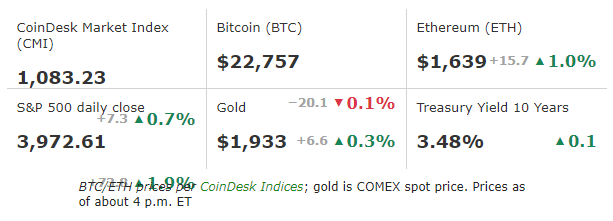

Bitcoin continued its 2023, jumping past $23,000 for the first time since August before retreating to trade at about $22,750.

⠀

⠀

Bitcoin continued its recent buoyancy over the weekend, rising over $23,000 at one point – BTC's first time above the threshold since early August – before retreating late Sunday.

⠀

The largest cryptocurrency by market capitalization was recently trading above $22,750, roughly flat for the last 24 hours but up more than 8% during the past week.

⠀

Bitcoin has risen roughly 37% this year as investors dismiss various crypto industry headwinds, most recently Genesis Global Holdco LLC filing for Chapter 11 bankruptcy protection, although in an email to CoinDesk, Joe DiPasquale, CEO of crypto fund manager BitBull Capital, said that the rise was typical for first quarters and noted "a long consolidation period that saw shorts accumlating."

⠀

"The market has risen, partially fueled the short squeeze," DiPasquale wrote, adding warily that "Bitcoin and several altcoins are overheated and due for a correction. "We wouldn’t be surprised to see Bitcoin testing $20,000 in the coming days."

⠀

"For the week ahead, market participants should be mindful of downside risks and potentially seek to take profits."

⠀

Ether followed a similar weekend path and was recently changing hands near $1,640, up about 1% from Saturday, same time.

⠀

The second largest crypto in market value is up approximately 4.5% for the past week and 35% since Dec. 31.

⠀

Most other major cryptos assumed a light green hue, although AXS, the token of the Axie Infinity Gaming platform Axie Infinity, and YGG, the native crypto of play-to-earn gaming guild, Yield Guild Games, were up more than 38% and 18%, respectively.

⠀

The CoinDesk Market Index (CMI), a measure of leading cryptos' market performance, was up slightly.

⠀

Cryptos' weekend rise followed a positive Friday for equity indexes as the tech-heavy Nasdaq and S&P 500, which has a strong technology component, jumped 2.6% and 1.8%, respectively.

⠀

Traditional asset markets have looked optimistically at mounting evidence that inflation is waning without casting the economy into a steep recession, and are hopeful that the U.S. central bank will be ratcheting back its next interest rate hike to 25 basis points (bps) from its more recent diet of 75 and 50 bps increases.

⠀

Meanwhile, Signature Bank will not handle crypto transactions larger than $100,000, according to a Bloomberg report that cited a statement from exchange giant Binance.

⠀

In a statement to Bloomberg, Binance said that Signature, which has been looking to reduce its exposure to crypto markets, would "no longer support any crypto exchange customers with buying and well amounts less than 100,000 USD as of February 1, 2023."

⠀

Binance said that this would be "the case for all Signature's crypto exchange clients" and noted that some users might "not be able to use SWIFT bank transfers to buy or sell crypto with/for USD" is smaller amounts.

⠀

In recent weeks, Signature, which has ranked among the most crypto friendly banks, and other financial services firms have been reducing their exposure to crypto, part of the widening fallout from crypto exchange FTX's implosion. In December, Signature's CEO said the bank would shrink its deposits tied to cryptocurrencies by $8 billion to $10 billion.

⠀

Nearly a quarter of the New York-based bank’s $103 billion in total deposits, or roughly 23.5%, came from the crypto industry as of September 2022. But given the recent “issues” in the space, Signature will reduce that amount to under 20% and potentially under 15% eventually, Signature's Joe DePaolo said at an investor conference hosted by investment bank Goldman Sachs.

⠀

Despite his cautious outlook for the week, BitBull's DiPasquale was more sanguine about the crypto "market's appetite for risk."

⠀

"This is a positive sign for an eventual recovery, but we believe that may need more time and could materialize by end of the year," he wrote.