Author: Changan I Biteye Content Team

Do you know why you can't beat the pros on Polymarket? Because they scrutinize the rules, parsing every word like lawyers reviewing a contract.

In April 2026, a controversy over Venezuela's leader erupted in the Polymarket community.

There was a market on Polymarket asking, "Who will be the leader of Venezuela by the end of 2026?" Many traders intuitively thought: Maduro is in a U.S. prison, Delcy is presiding over the cabinet in Caracas, so the de facto ruler is obviously Delcy. They placed their bets on Delcy.

But the rules and supplementary notes were clear: "officially holds" refers to the person formally appointed and sworn in. The UN-recognized Venezuelan government has not formally removed or replaced Maduro; official government information still identifies him as president. The rules specifically added: "Temporarily authorized to exercise presidential powers does not equate to a transfer of the presidential office."

According to these rules, even if Maduro remains in a U.S. prison, he is still the legitimate president of Venezuela.

Similar examples abound:

-

After Polymarket issued a stablecoin, controversy arose over "What is the FDV of the Polymarket token?": Is a stablecoin considered a token? A single word makes all the difference.

-

Iran Uranium: The standard for "agreement"—conditional statements vs. formally signed agreements.

Behind these cases lies the same logic: On Polymarket, the rules are paramount. But when disputes arise over the rules, Polymarket has a complete adjudication process to resolve them. This article will explain how this mechanism operates, and where it resembles and fundamentally differs from traditional courts.

I. Polymarket's Adjudication Mechanism

Ambiguity in the rule text doesn't just cause pricing discrepancies; it becomes a formal dispute at settlement.

Polymarket sees numerous market settlements daily, with markets involving political statements, diplomatic postures, and military actions being particularly prone to controversy.

Disputed events are actually the norm in prediction markets. Ambiguity creates pricing divergence during trading and turns into conflict at settlement—it's the same issue at two different points in time.

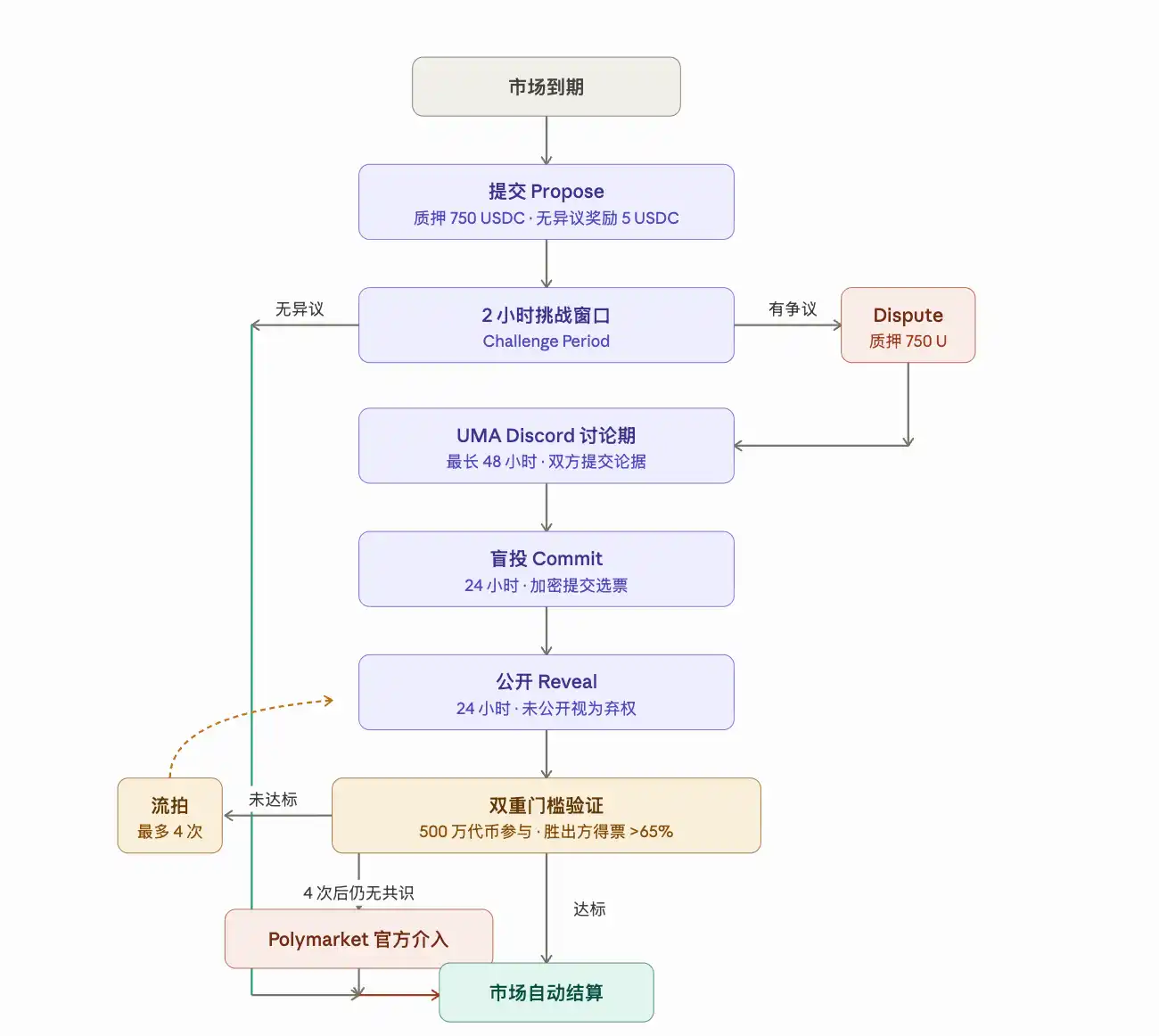

To resolve these disputes, Polymarket has established a complete adjudication process. The settlement process splits into two paths: normal settlement and dispute resolution.

Step 1: Submit a Proposal (Propose)

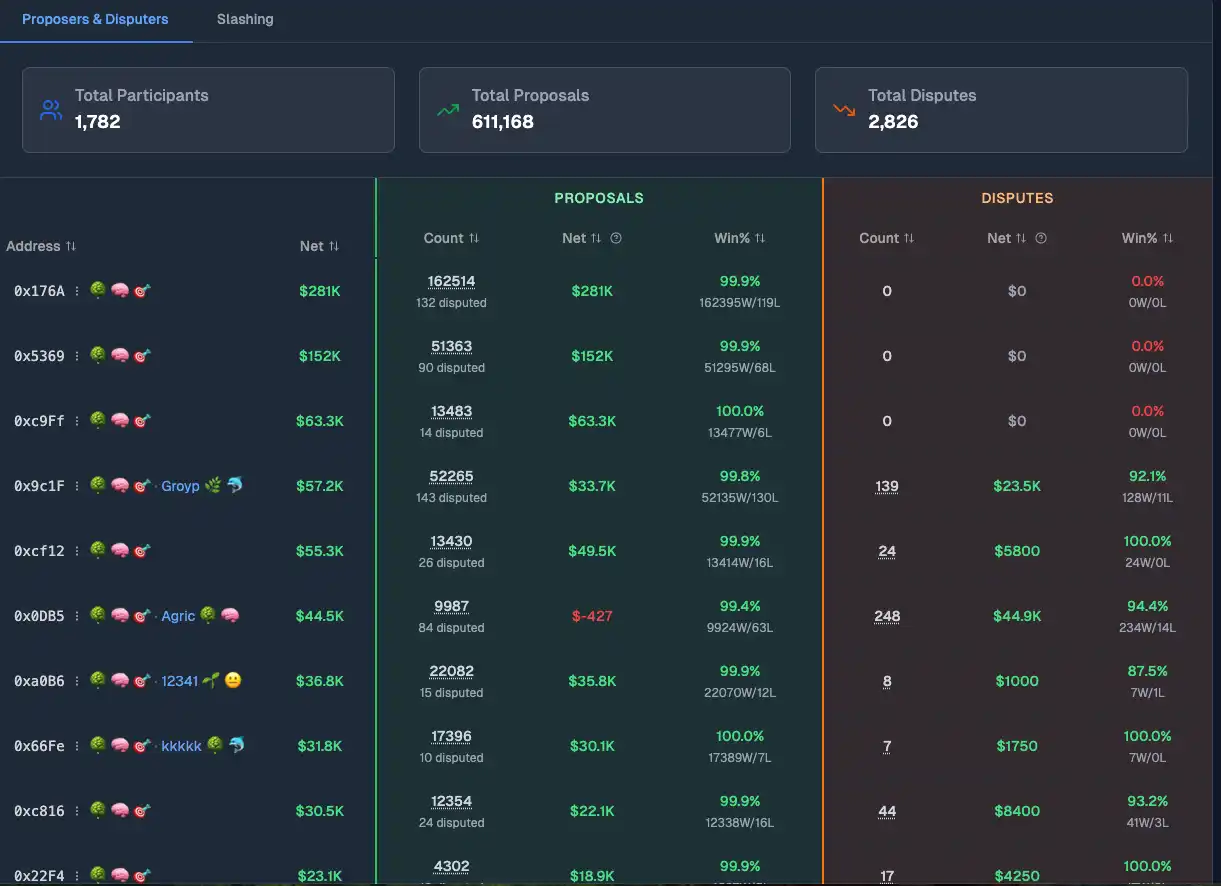

When a market meets the settlement conditions, anyone can submit a proposed resolution, declaring whether the market should be judged YES or NO. Submitting a proposal requires staking 750 USDC as a bond, which serves as the submitter's endorsement of their judgment. If the market has no objections, the user who submitted the proposal receives a 5 USDC reward.

Currently, only 1782 users have submitted Proposals. The top-earning user has accumulated $281K.

Step 2: 2-Hour Challenge Window (Dispute)

After a proposal is submitted, it enters a 2-hour challenge period. This is the first fork in the entire process.

If no objections are raised within 2 hours, the system defaults the proposal as correct, the market settles directly, and the process ends. The vast majority of markets follow this path.

If someone believes the proposal result is incorrect, they can challenge it within this 2-hour window, also requiring a stake of 750 USDC. A successful challenge earns a 250 USDC bonus.

Very few users specialize in Disputes. The user who has earned the most from the Dispute环节 is 0xB7A, with profits of $17,123.

Step 3: Up to 48-Hour Discussion Period

Once entering the dispute track, both parties proceed to the UMA Discord discussion phase. This stage allows各方 to present arguments and evidence: interpretations of the rule text, relevant news reports, historical precedents, official statements—any material supporting their position can be presented at this stage.

The discussion period lasts up to 48 hours and is the only phase where reasons can be fully stated. The quality of this stage很大程度上 determines the direction of the subsequent vote.

Step 4: 48-Hour Voting

After the discussion, it enters the UMA token holder voting phase, divided into two 24-hour stages.

-

The first stage is blind voting. It forces each voter to make an independent judgment based on their understanding of the rules, rather than following big players.

-

The second stage is public. Votes not made public in this stage are considered abstentions and are directly invalidated.

After voting, UMA sets two settlement thresholds that must be met simultaneously for the adjudication to complete:

-

Participation level: At least 5 million tokens must participate in the vote, ensuring the裁决 has sufficient representativeness.

-

Absolute consensus: The winning side must have a vote share exceeding 65%, not a simple 51% majority.

If both thresholds are not met, the vote fails and enters a new round of re-voting, up to a maximum of 4 times. If no consensus is reached after 4 rounds, Polymarket officials have the right to intervene directly in the adjudication.

Step 5: Automatic Settlement

Once the vote result is confirmed, the market settles automatically, and funds are distributed according to the result. There is no appeal, no retrial, no recourse.

The entire dispute process, from challenge submission to final settlement, is typically completed within a week.

II. Polymarket vs. Traditional Courts: The Same Logic, Different Design

On the surface, Polymarket's adjudication process is highly similar to traditional courts: there is a party making a claim, a party challenging the claim, a discussion phase for statements, and finally an adjudicator who gives the result.

But the two systems differ fundamentally in one key design: separation of powers.

-

Court power is isolated

In traditional courts, the plaintiff and defendant only have the right to state their case, not to adjudicate. The judge only has adjudication power, without a vested interest. Crucially, the judge must remain independent of the case. If the judge has any interest in the case, they must recuse themselves, and another judge takes over.

The adjudicator and the interested party are never the same person.

-

Polymarket lacks this isolation

UMA token holders are the adjudicators, but they can simultaneously hold positions in the disputed market. Which direction they adjudicate directly affects their own profits and losses. The裁判者 and the interested party being the same person is called a conflict of interest in traditional courts, requiring mandatory recusal, but in Polymarket, it is legal and normal.

This design flaw is the root cause of the following two problems.

1️⃣ Why the discussion环节 fails

In court, the positions of the plaintiff and defendant are fixed from the moment of filing. Lawyers don't switch sides mid-trial, nor do they withdraw their statements because the other side is more assertive. Positions are clear, roles are defined, and the entire debate is built on this stability.

The UMA Discord discussion faces two problems simultaneously.

-

Herd mentality: The discussion is public and real-name. Once influential KOLs state their position, it's easy for others to follow. Many participants just post "P1" or "P2" without giving any理由.

-

Position switching: Participants also hold positions in the disputed market. When their positions change, their stance naturally changes with it. This is why posts in the UMA Discord are often deleted after being made.

Both problems stem from the same root: the adjudicator and the interested party are not separated. Courts use a mandatory recusal system to separate these two roles, ensuring the stability of positions during discussion. Polymarket lacks this isolation.

2️⃣ Why the adjudication results are opaque

In court, the judge hears the full arguments from both sides before making a ruling. The ruling document states which arguments were adopted, the basis for the decision, and the reasoning behind it. The losing party might disagree, but at least they know why they lost and can strengthen their arguments next time.

These rulings form a system of precedents that can be studied. Future judges, lawyers, and parties can cite them, making the adjudication standards searchable, learnable, and predictable.

After UMA voting concludes, there is only a result: YES or NO. The讨论 parties don't know what the voters saw, what they believed, or why they leaned one way. Winners don't know which argument worked; losers don't know where their persuasion fell short. Because the adjudication logic is never made public, the outcomes of disputes are difficult to learn from and accumulate.

Court rulings form a system of precedent; Polymarket's adjudications leave only a result.

III. Final Thoughts

Therefore, Polymarket is never just a market for "guessing events" correctly. It's more like a system that translates real-world events into legal text and then translates that legal text into settlement results.

Understanding the rules is as important as doing research. The pros' advantage often comes from their depth of understanding of the rules, knowing what this system acknowledges and what adjudications will recognize.

Those who realize earlier that a gap exists between "reality" and "the rules" have a better chance of profiting from the price deviations created by misreading, controversy, and emotion.