Author: Stablecoin Insider / McKinsey×Artemis

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: The McKinsey and Artemis joint report did something rare in the industry: breaking down the stablecoin transaction volume data. The conclusion: of the approximately $35 trillion in annual on-chain transaction volume, only about $390 billion (about 1%) represents real payment behavior, of which 58% is business-to-business financial operations, with an annual growth of 733%. Consumer-side stablecoin usage is almost negligible, and this is no accident—the article summarizes five structural reasons explaining why the gap between institutions and individuals is not just a temporary disparity.

Full text as follows:

The stablecoin industry has a headline problem.

On one hand, raw on-chain data shows tens of trillions of dollars flowing on-chain annually, a figure that fuels endless comparisons with Visa and Mastercard, and predictions of SWIFT's imminent replacement.

On the other hand, a landmark report released in February 2026 by McKinsey & Company and Artemis Analytics stripped all this away and asked a more direct question: how much of it is real payments?

The answer is about 1%.

Of the approximately $35 trillion in annualized stablecoin transaction volume, only about $390 billion represents genuine end-user payments, such as supplier invoices, cross-border remittances, payroll disbursements, and card swipes. The rest is trading activity, internal fund shuffling, arbitrage behavior, and automated smart contract loops.

The report concludes that the inflated headline numbers should be "the starting point for analysis, not a proxy for measuring payment adoption."

But within this real $390 billion baseline, there is a story worth examining closely, and it almost entirely revolves around corporate finance, not consumer wallets.

B2B Dominates: What the Data Actually Shows

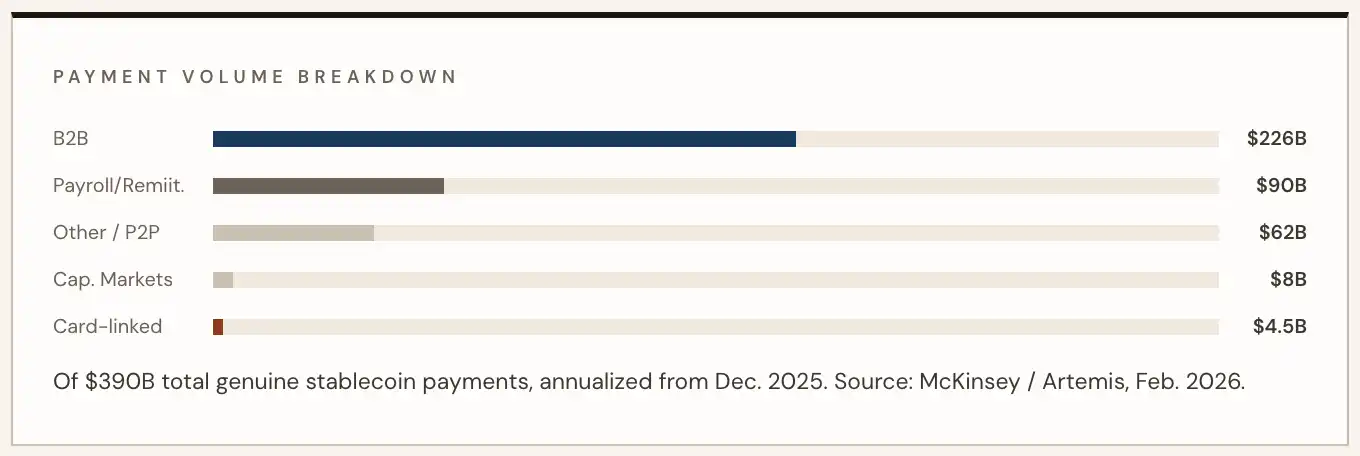

According to the McKinsey/Artemis analysis (benchmarked to activity data from December 2025), business-to-business transactions account for $226 billion of all real stablecoin payment volume, about 58%.

This figure represents a 733% year-on-year increase, primarily driven by supply chain payments, cross-border supplier settlements, and financial liquidity management. Asia leads in geographic activity, but adoption is also accelerating in Latin America and Europe.

The remainder of the real payment space is distributed among payroll and remittances ($90 billion), capital market settlements ($8 billion), and linked card spending ($4.5 billion).

According to McKinsey, card spending associated with stablecoins grew an astonishing 673% year-on-year, but in absolute terms, it remains only a small fraction of B2B flow.

For context: this total of $390 billion represents only 0.02% of McKinsey's estimated global annual payment total of over 2 quadrillion dollars. Specifically, B2B stablecoin flow accounts for about 0.01% of the global $160 trillion B2B payment market.

These numbers are large in the context of stablecoins but remain minuscule in the context of the global financial system.

Monthly run-rate data more intuitively shows where the momentum lies. According to data cited by BVNK from the McKinsey/Artemis report, stablecoin monthly payment volume was only $5 billion in January 2024; by early 2026, this number had exceeded $30 billion—a sixfold increase in less than two years, with the steepest acceleration occurring in the second half of 2025.

Annualized, this run rate now exceeds $390 billion.

"The fact that real stablecoin payments are far lower than conventional estimates does not diminish the long-term potential of stablecoins as a payment rail; it simply establishes a clearer baseline for assessing where the market stands." — McKinsey/Artemis Analytics, February 2026

Why the Gap Exists: Five Structural Forces Excluding Retail

The divergence between the explosive adoption in B2B and the negligible consumer usage is not coincidental but the product of structural asymmetries that systematically favor corporate use cases over retail ones.

Here are the five forces driving the institutional gap:

1) Financial Efficiency Beats Consumer Convenience

Corporate treasurers are driven by specific, quantifiable pain points: SWIFT correspondent banking chains that take one to five business days to settle, currency exchange windows that tie up working capital, and intermediary fees layered on at every transaction point.

Stablecoins solve all three problems simultaneously. For a company paying suppliers in fifteen countries, the economic case is clear; for a consumer buying coffee, it is not. The incentive to switch is orders of magnitude greater on the enterprise side.

2) Programmability Has No Equivalent Value on the Retail Side

The B2B explosion is partly a story of programmable payments. Smart contracts enable conditional logic—invoice triggering, delivery confirmation, escrow release—that can automate entire accounts payable processes at scale.

This is naturally suited to corporate finance operations, as high-value, structured, repetitive payment processes benefit immensely from automation. Retail payments lack similar trigger use cases at any scale.

Consumers buying groceries don't need programmable conditions; they need something that works like swiping a card. The cognitive complexity of blockchain-native payments remains a barrier on the retail side, and programmability does nothing to help that.

3) Regulatory Architecture Favors Institutions

Post the GENIUS Act, institutional operators have adapted to the compliance architecture—AML/CFT, Travel Rule, licensing requirements—and built the legal infrastructure to operate confidently.

Corporate finance teams have dedicated compliance functions that can absorb onboarding friction; individual consumers cannot. The result is that, in most jurisdictions, on-ramps for stablecoins remain operationally complex for retail users, and the merchant acceptance gap persists globally.

Every frictionless B2B payment today is a data point institutions use to justify further investment; the consumer ecosystem, meanwhile, awaits a compliant, user-experience-smooth entry point that has not yet emerged at scale.

4) Closed-Loop Advantage

B2B stablecoin payments succeed precisely because they are closed-loop: business sends to business, both have wallets, both have compliance infrastructure, and neither needs a universal merchant network.

Consumer payments face the classic chicken-and-egg problem: merchants won't invest in stablecoin acceptance infrastructure until consumers demand it; consumers won't enable wallets until they can spend widely.

The institutional world completely bypasses this problem by operating in bilateral or consortium environments, requiring no open merchant network.

5) Institutional Incentives Point Upstream

Corporate treasurers holding stablecoins gain yield, reduce FX exposure, and improve liquidity management—advantages that accrue internally and, if shared downstream, introduce complexity or competitive vulnerability.

Extending stablecoin use to a supplier's supplier, employees, or end consumers requires building a network that benefits those downstream parties, which is not necessarily in the interest of the originating finance team.

In the absence of a clear ROI driving network expansion outward, companies rationally choose to consolidate internal gains.

Market Context

BVNK's own infrastructure data corroborates the dominance of B2B from an operator's perspective. The company processed $30 billion in annualized stablecoin payment volume in 2025, a 2.3x year-on-year increase, with one-third of the volume coming from the US market.

Its client list (Worldpay, Deel, Flywire, Rapyd, Thunes) consists of leaders in cross-border B2B and payroll, not consumer applications.

As BVNK stated in its 2025 year-end review:

"The initial assumption that remittances and consumer transfers would lead stablecoin growth did not materialize as the primary driver; B2B instead assumed that role."

When Will Retail Catch Up—If Ever

The McKinsey/Artemis baseline makes the current situation clear. What it cannot answer is whether the institutional gap will narrow, widen, or permanently solidify.

Here are three possible scenarios for the next 18 months:

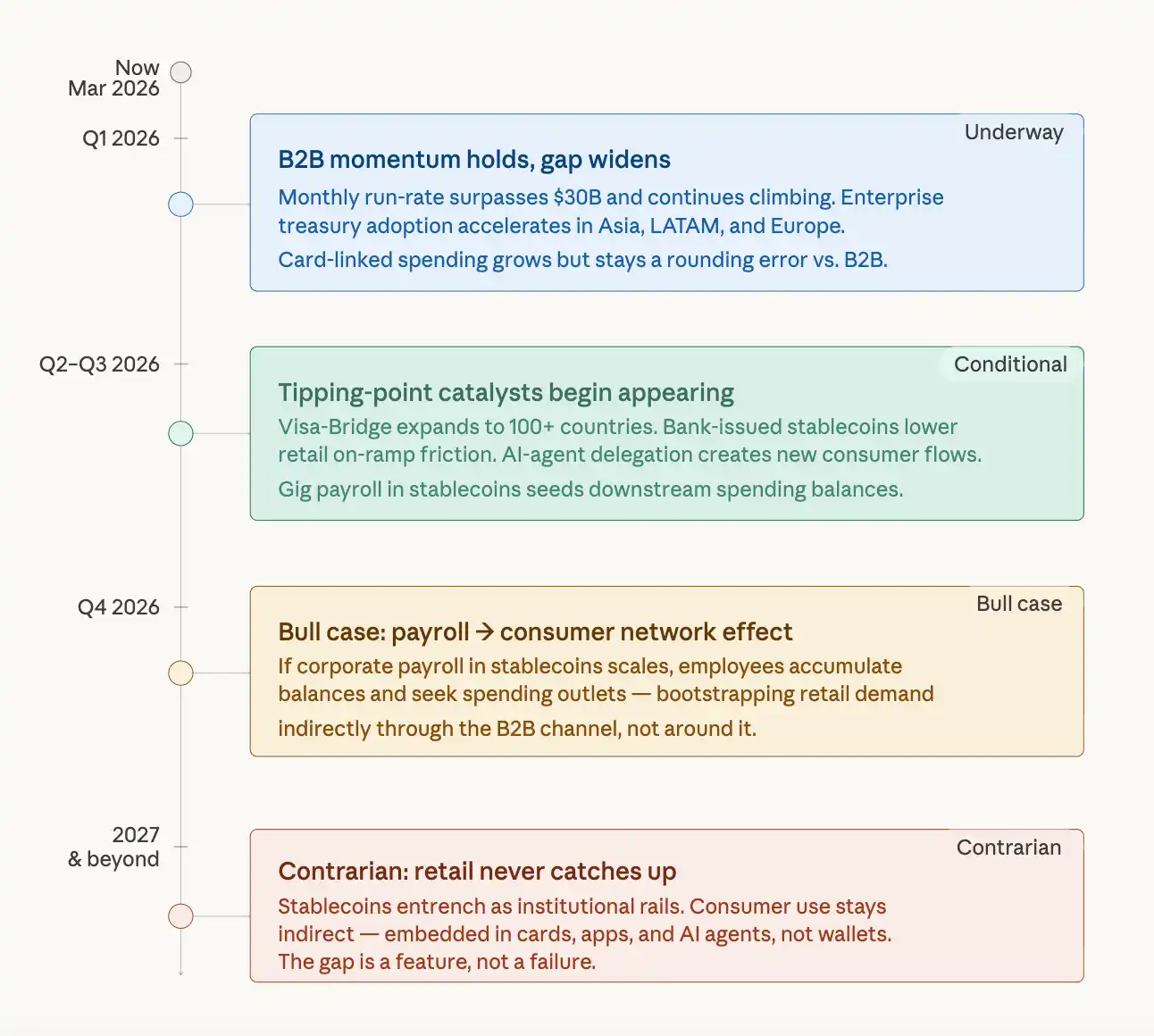

Near Term 2026—The Gap Widens Further

B2B momentum shows no signs of slowing. The monthly run rate of over $30 billion continues its trajectory as more companies use stablecoin rails for cross-border accounts payable and financial operations. Consumer stablecoin card spending grows modestly but remains negligible in absolute terms compared to B2B flow. Even if retail adoption advances slowly in percentage terms, the gap widens in absolute dollar terms.

Mid-Term End-2026 to 2027—Inflection Points Begin to Appear

Several catalysts could begin to bridge the gap: bank-issued multi-currency stablecoins reduce retail on-ramp friction; programmable features extend to consumer applications via AI Agent payment delegation; gig economy wages paid in stablecoins create downstream spending balances for employees.

US Treasury Secretary Scott Bessent predicted that stablecoin supply could reach $3 trillion by 2030, a trajectory implying consumer network effects will eventually emerge.

Counterview—Retail May Never 'Catch Up,' and That Might Be the Point

The most honest reading of the McKinsey data is that stablecoins may be evolving into what the report faintly hints at: a programmable settlement layer on the internet for machines, finance departments, and institutions, with consumer adoption being an indirect, embedded benefit, not the primary use case.

If this framework holds, then the institutional gap is not a failure of adoption but a feature of the technology's natural architecture. Corporate wages paid in stablecoins may eventually create downstream consumer spending, but the path from B2B infrastructure to retail wallets is long, circuitous, and dependent on user experience breakthroughs that have not yet emerged at scale.

An Honest Baseline

The McKinsey/Artemis report did something more valuable than recording stablecoin growth: it established an honest baseline the industry has clearly been missing.

Stripping away trading noise, internal shuffling, and automated smart contract loops reveals a genuinely growing market—real payment volume doubled from 2024 to 2025—but one that is highly concentrated on the institutional side in a structural, non-accidental way.

The 733% growth in B2B is not a deferred consumer story; it is a maturing finance story.

The enterprises building on stablecoin rails today are solving real operational problems—cross-border friction, correspondent banking inefficiencies, working capital delays—problems that have nothing to do with whether consumers hold stablecoin wallets. They will continue building, regardless.