The full report is freely available in PDF format.

Welcome to Strategy Watch #2

Strategy Watch was built to address a clear demand for high-signal, impartial analysis of fund-level performance and allocation trends in digital assets.

The inaugural edition confirmed this demand, reaching a broad audience of key decision makers, from leading global asset managers, hedge funds, major investment banks, top-tier crypto-native funds and Fund of Funds.

Building on this early momentum, our objective is straightforward — to make Strategy Watch a must-read monthly publication for the digital asset investment community.

This publication is strengthened by direct input from market participants. Funds and allocators that contribute data and insights help shape a more complete and valuable view of the landscape.

If you have insights, data, or allocation updates worth sharing, we welcome your contribution.

Present your latest initiatives and updates to a curated audience of institutional allocators.

Inside the Latest Strategy Watch

The report is structured across six core sections, each focused on a distinct dimension of institutional activity in digital assets:

01 Institutional Flow Monitor |

02 Fund and SMA Performance | February was a bloodbath, check this section to see the only strategy type that returned positively last month.

03 Strategy Deep Dive: Macro Strategies | Hear firsthand from a macro portfolio manager on how they are navigating the current geopolitical challenges.

04 On-chain Vault Performance | Are ETH curators underperforming ETH staking yield?

05 Manager Monitor | Find out how more than 300 managers are expecting the crypto market to perform over the next three months.

06 Allocation Updates | New USD 750m Fund of Funds is launching. Check this section to learn more.

The Premier Digital Assets Allocator Platform. Learn more

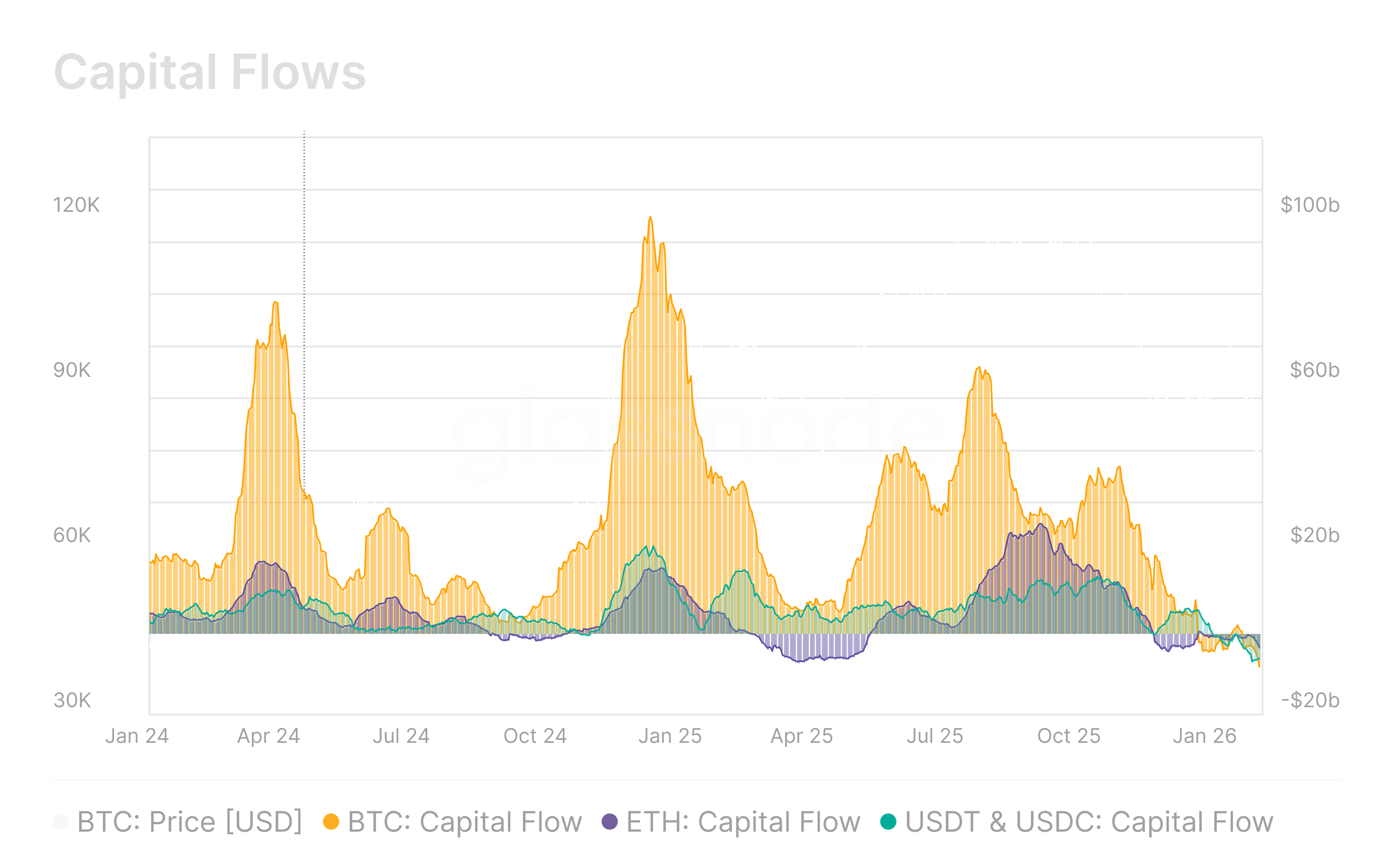

Institutional Flow Monitor

Bitcoin and Ethereum continued to experience sustained net outflows, with BTC and ETH capital flows registering -$9.6B and -$3.2B. However, stablecoins broke from the broader negative trend, flipping to +$6.2B in net inflows. Rather than signaling a broad return of risk appetite, this rotation likely reflects a defensive repositioning, with capital migrating into dollar-denominated on-chain instruments while conviction in spot crypto assets remains under pressure heading into mid-Q1 2026.

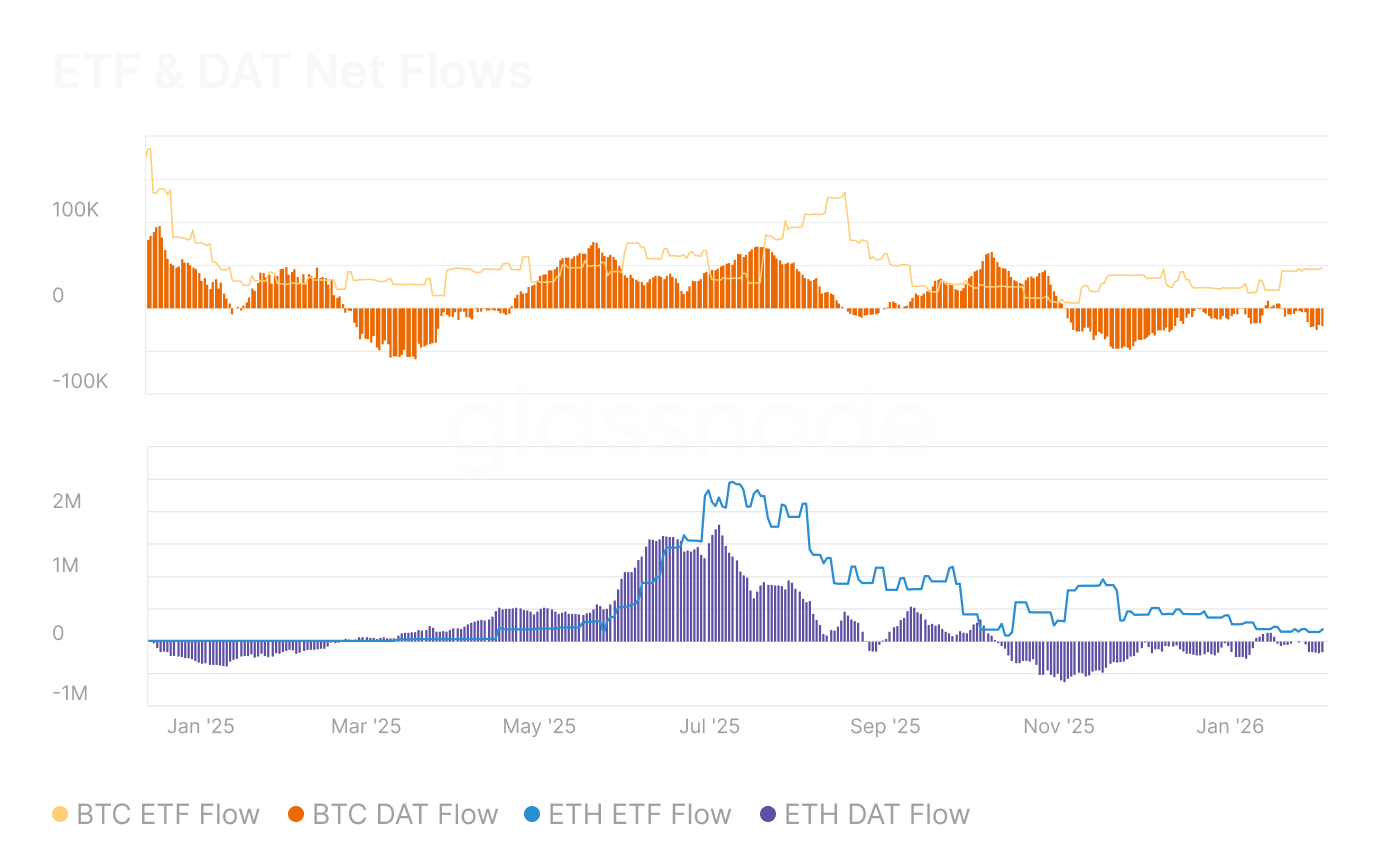

ETF & DAT Net Flows

After sustained February outflows, Bitcoin ETF and DAT flows returned to positive territory, recovering to +28k BTC and +46.8k BTC respectively. Ethereum flows were more measured, with ETF flows near neutral at +46.5k ETH and DAT flows stabilizing at +295.8k ETH. While the directional shift is encouraging, the recovery remains early-stage and uneven, and it would be premature to characterize this as a broad resumption of institutional conviction.

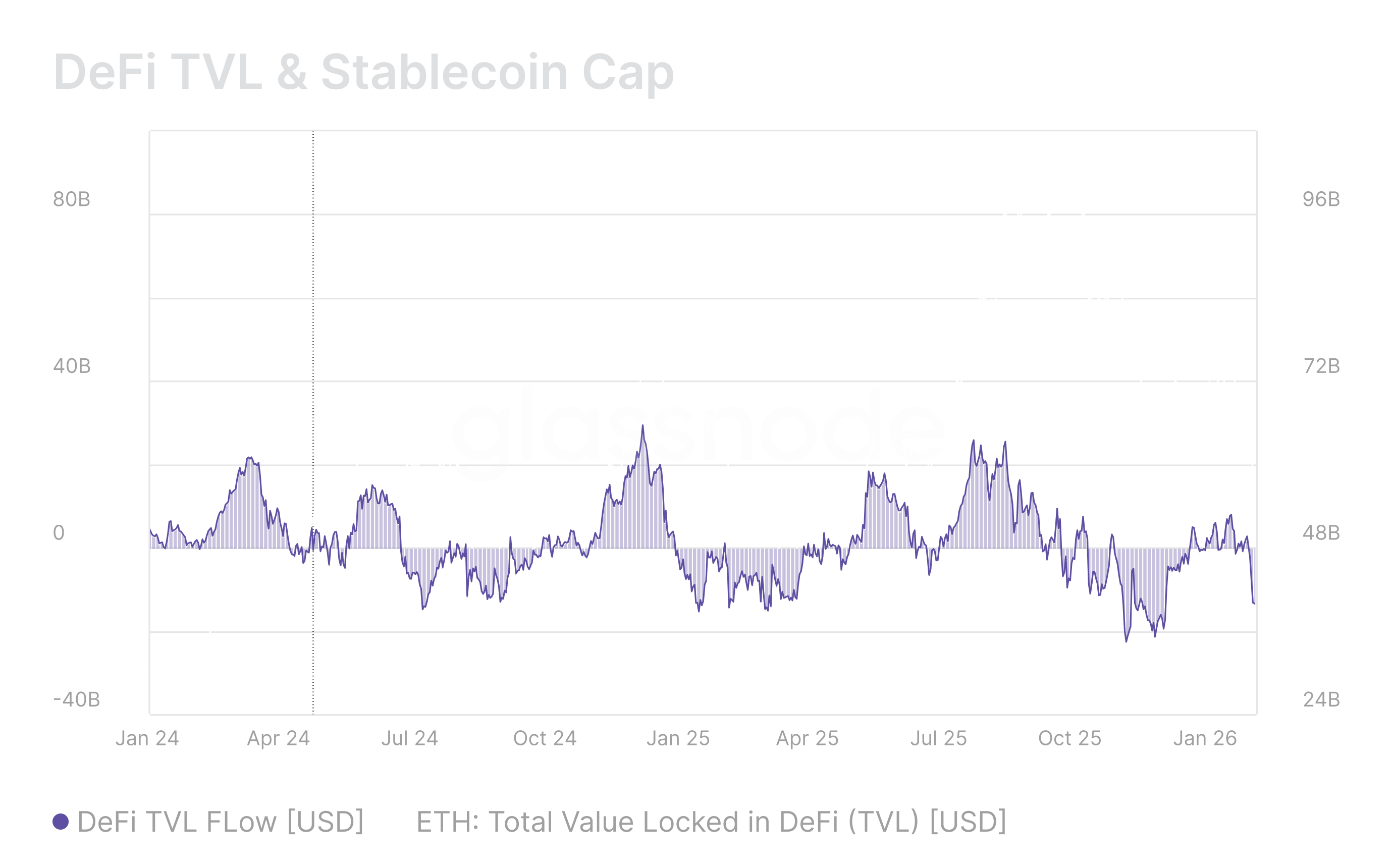

DeFi TVL & Stablecoin Cap

Total Value Locked on Ethereum recorded peak outflows of -$23.7B per month in February, implying sustained withdrawal by larger allocators from on-chain activities such as liquidity provisioning and yield strategies. This slowdown alone is insufficient to signal a reversal, and diminished conviction in DeFi risk-adjusted returns continues to point to shallower liquidity depth across the ecosystem.

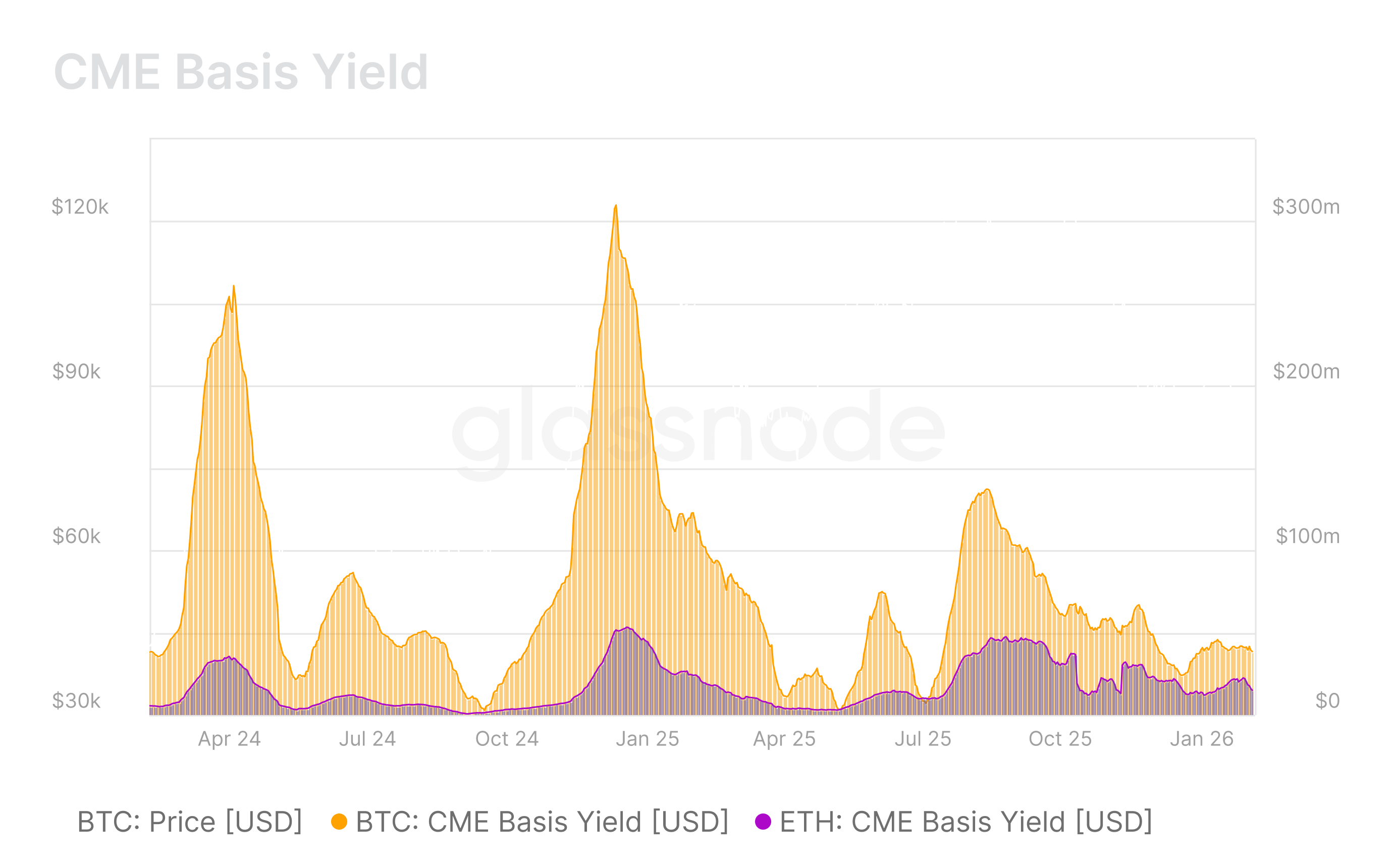

CME Basis Yield

The monthly dollar value captured by institutions via cash-and-carry trades declined notably for both Bitcoin and Ethereum, building on the sharp compression seen since August 2025. This tightening basis reflects reduced leverage deployment, softer futures demand, and continued pullback in balance-sheet commitment amid tighter liquidity conditions persisting from January into early March 2026.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions. Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.