Recently an increasing number of DeFi protocols announced switching to veTokenomics model: Yearn Finance, Synthetix, Pancakeswap and Perpetual protocol.

In this article I ventured to understand why, how veTokenomics works and what makes it special

The analysis covers 20+ vote-escrow (ve) ecosystem protocols.

I analyzed the protocols by type of veTokenomics, TVL, percentage of supply locked, APR, average lock time and unique features/changes done to the original Curve veToken model.

Note that the TVL, APR etc. is fluctuating constantly and is for reference only.

Why veTokenomics?

Summer of 2020.

Compound Finance launches liquidity mining (LM) starting the DeFi bull run.

Millions of dollars flow into Compound smart contracts. Liquidity providers (LPs) maximize returns by lending and then borrowing the same asset just to lend it out again.

Balancer follows with its BAL LM campaign. Andre Cronje gives away YFI ‘valueless token’ as a fair launch. Forks of Uniswap V2 emerge enticing LPs with high yields which finally leads to Sushiswap vampire attack on Uniswap.

The goal here is to farm as many tokens and then dump it for compounded returns.

The price of these DeFi tokens plummets. Yield on deposits drops and LPs leave. It’s a death spiral.

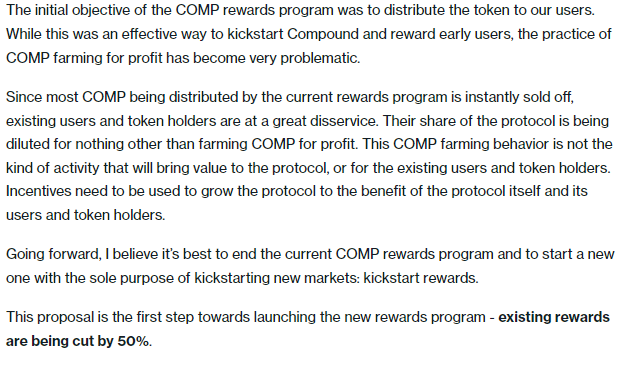

2 years later Compound finally cut rewards by 50% and admitted that distributed COMP ‘is instantly sold off’ thus token holders are ‘diluted for nothing other than farming COMP for profit’.

https://compound.finance/governance/proposals/92

Yet Curve Finance approached liquidity mining differently:

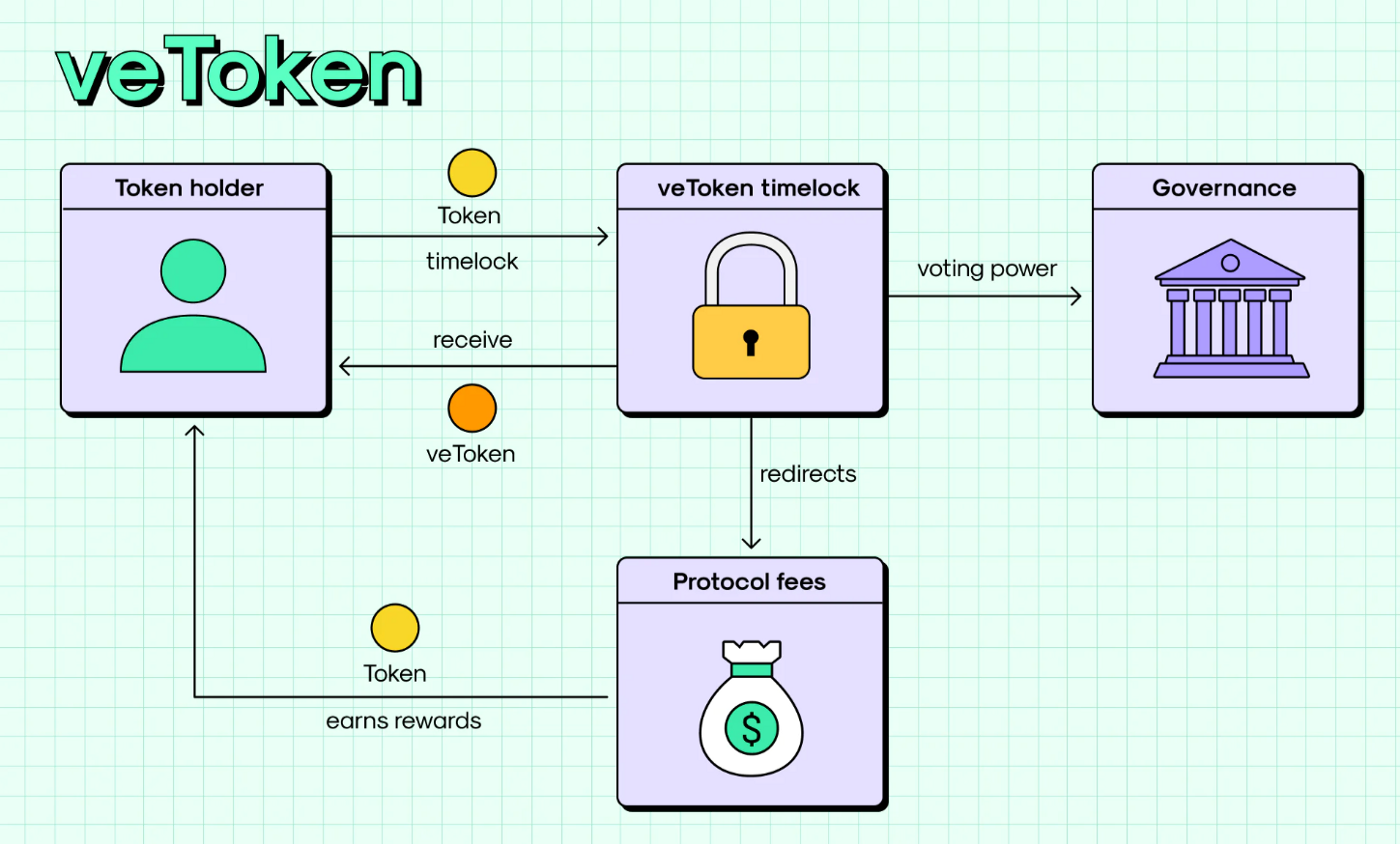

First, to earn higher rewards, LPs need to lock CRV for up to 4 years. The longer you lock, the more vote-escrowed CRV (veCRV) you get.

Secondly, locking is irreversible and tokens are not transferrable.

Third, CRV lockers earn part of the protocol revenue.

The main objective: how to increase TVL without over inflating circulating CRV supply. Currently only 11.8% of all CRV is circulating with $6M USD flowing to the market every week. Even the airdropped CRV was vested for a year.

The result: Curve’s lock ups and vesting buys time to grow the protocol, adoption and revenue. Succeeding means that the value proposition for CRV should be attractive enough so after unlocks CRV wouldn’t be sold at all.

There’s more — influence on CRV emissions

Curve is an AMM for highly correlated assets and yields strong influence on which assets attract the most liquidity depending on where CRV rewards are directed.

Which pools (and how much) receive CRV distribution is voted by veCRV holders in so-called weight gauges.

If you’re building a protocol-owned-stablecoin, for example, you’ll need it to be liquid and Curve is THE AMM for that. Thus you’ll need veCRV to vote on weight gauges in order for your stablecoin pool to receive CRV rewards.

Another option is to make other people vote for you by bribing them with other tokens. This way it increases demand for CRV and yield for veCRV.

https://perpprotocol.mirror.xyz/GzzvxvNFeTjH9au6cllJ_4ffshySn3M3iAmKe34sxdw

These 4 features is the basics of what we call veTokenomics.

Game Theory of veTokenomics

Curve veTokenomics changed the liquidity mining game theory.

The optimal strategy for Compound and other protocols was to farm free tokens and dump for compounded interest. How much dollar value you deposited compared to others is the sole criteria. If you believe in the future of Compound, it’s better to wait until it reaches an inflection point where the token price is low enough relative to adoption.

In veTokenomics you have skin in the game to see the protocol succeed:

To receive boosted rewards you need to lock CRV;

If you choose to farm and dump CRV, you’ll get be betting against your own CRV position;

Yet as other LPs farm and restake CRV, your boost power decreases;

All while you earn part of the protocol revenue and rewards from bribes.

At the time of writing 53.3% of all circulating CRV supply is locked, yielding veCRV 5.63%.

Advantages of veTokenomics

To sum up, veTokenomics has 5 main advantages:

Encourages long term holding.

Reward distribution is more efficient & transparent. No need for DAO proposals.

Token investors are incentivized to become liquidity providers and vice versa.

Stream of revenue incentivizes the team without selling the token.

Attracts other protocols to build on top to boost rewards and increase bribing efficiency. (More on this later).

The focus on long-term holding has attracted more protocols to adapt veTokenomics. Quite many protocols modified the original Curve model to fit their needs.

Top 6 Most Significant Modifications

1.Using LP tokens for vote-escrow.

In Curve, you lock CRV to receive veCRV. Yet in Balancer, you lock 80% BAL and 20% ETH LP tokens to receive veBAL.

Ref Finance has a two token model: veLPT and LOVE, where veLPT consists of REF and NEAR.

Interestingly, the max lock period chosen by both protocols is 1 year.

2. Platypus Finance model.

Trader Joe and Yeti Finance adopted Platypus model where tokens are staked and veTokens are accrued overtime. The higher the veToken balance, the higher the yield.

There’re no lock ups and users can withdraw anytime, but loses the yield boost.

The model rewards early users the most. None have implemented gauge weight yet.

3. Early unlocks with a penalty.

Ribbon Finance allows to unlock veRBN before lock up expires with a penalty. i.e. locking for 2Y and unlocking when 1Y is left, incurs a 50% penalty.

Yearn Finance is adopting the same logic. In both protocols the penalty is redistributed to veToken holders.

DODO’s vDODO has a very different ve model, but allows redeeming DODO by incurring a variable exit fee.

I’d like to add here that Ribbon is interesting with its Bribes Boosting Delegation (receiving extra rewards without being and LP) and Yearn’s YFI is not inflationary so rewards will come from buybacks with 800 YFI already prepared!

4. Three token model.

Pancakeswap is adopting Trader Joe’s model with 3 locked tokens.

Each have a lock mechanism for token sales and another to boost farm yields, but Pancakeswap is launching weight gauge voting token (vCAKE) soon while JOE is expected to follow much later.

5. Velodrome — DEX, Yield farm and bribing protocol in one.

Velodrome is an improved version of Andre Cronje’s failed Solidly project.

By staking VELO for up to 4 years, users get veVELO: an ERC-721 governance token in the form of an NFT, which uses ve(3,3) rebase mechanism.

veVELO voting power diminishes with time, so after every rebase you should claim and restake VELO to restore voting power.

The veVELO weigh voting encourages bribes to distribute VELO rewards. For example, just last week L2DAO bribes in OP token yielded 120% APY extra to veVELO holders.

Theory of a Rational veUser

veTokenomics requires significant efforts to plan and active management to maximize returns. For both: token investors and yield farmers.

Above all, you’ll need to consider:

As an LP, how much CRV and for how long you need to lock for max yield.

Whether to claim and sell CRV rewards or restake.

How often to compound returns accounting for gas fees.

Which weight gauges to vote, especially if you LP into several pools.

Find out who’s offering the best bribes and vote on it…

…and much more.

Most of us have limited resources, so to maximize returns protocols built on top of veTokens emerged — yield/governance aggregators.

Yield/Governance Aggregation

The mission of veAggregators is to minimize investment strategy efforts and maximize returns.

In this research I cover 4 veAggregators:

Convex Finance for CRV and FXS.

Aura Finance: BAL

Vector Finance: PTP and JOE.

StakeDAO: CRV, FXS, ANGLE and BAL.

Convex is by far the biggest with $4.42b in TVL and controls 77% of all circulating CRV. Even Yearn uses Convex vaults now. In comparison, Aura controls 27% share of veBAL.

Although with some differences, they do the following tasks:

Convert veTokens into transferable tokens that accrue veToken rewards, airdrops and extra rewards from veAggregator. For example, deposited CRV into cvxCRV earns 18% APY vs 5.6% on veCRV.

Boost and compounds the yield return for LPs and gives out extra rewards with veAggregator token.

Collectively vote on gauge weights. The voting power is passed from veTokens to veAggregator vote-locked token holders. For example, locking CVX for 16 weeks gives vlCVX. Weight-gauges are not live on Platypus style veTokenomics.

Receive rewards in bribes and redistributes to vlAggregator token holders.

Yet once again, to maximize returns from bribes investors need active participation. A solution: delegate vlAggregator tokens to another platform that evaluates the best incentives ‘so that you can sit back and enjoy the rewards without doing any work.’

For vlCVX holders, Votium does the heavy lifting.

The complexity of veTokenomics offers opportunities for more protocols. Paladin’s Warden app, for example, allows veCRV holders to sell their yield boosts to Curve LPs. In this case LPs can optimize Curve yield without veAggregators.

The veGame of Thrones

veTokenomics is not the perfect solution for every project. They suffer from high inflationary pressure and only CRV outperformed ETH in the past year.

Yet more projects are switching to veTokenomics. YFI, SNX, PERP and CAKE are just a few I covered. I expect more protocols to follow their suit, because there are no better alternatives for highly inflationary tokens in the DeFi market right now.

Thanks to transparent weight gauge voting and bribing system veToken holders are incentivized to participate in the governance. Protocols seeking to increase liquidity on the vePlatform need to compete for the limited token emissions with bribes, which resulted in Curve Wars for CRV emissions.

As more protocols migrate to veTokenomics liquidity will become a commodity in high demand. New emerging protocols seeking to grow fast will need to evaluate on where the liquidity acquisition is the cheapest and fits its growth needs. Whereas previously the team decided on emissions, veToken holders can expect to profit from the liquidity games.